Read and download the CBSE Class 10 Social Science Money and Credit Assignment Set 01 for the 2026-27 academic session. We have provided comprehensive Class 10 Economics school assignments that have important solved questions and answers for Understanding Economic Development Chapter 3 Money And Credit. These resources have been carefuly prepared by expert teachers as per the latest NCERT, CBSE, and KVS syllabus guidelines.

Solved Assignment for Class 10 Economics Understanding Economic Development Chapter 3 Money And Credit

Practicing these Class 10 Economics problems daily is must to improve your conceptual understanding and score better marks in school examinations. These printable assignments are a perfect assessment tool for Understanding Economic Development Chapter 3 Money And Credit, covering both basic and advanced level questions to help you get more marks in exams.

Understanding Economic Development Chapter 3 Money And Credit Class 10 Solved Questions and Answers

Question. Which one of the following is an essential features of barter system?

(a) It promotes local markets

(b) It spread social field of an individual

(c) It requires double coincidence of wants

(d) It is an easy way

Answer : C

Question. Almost all of the borrowers of Grameen bank of Bangladesh are

(a) Men

(b) Women

(c) Senior citizen

(d) All of them

Answer : B

Question. Both parties agree to sell and buy each other’s commodities

(a) Measures of value

(b) Store of value

(c) Double coincidence of wants

(d) Credit

Answer : C

Question. Which one of the following terms not included against loans?

(a) Interest rate

(b) Collateral

(c) Documentation

(d) Lender’s land

Answer : D

Question. About what percentage of their deposits is kept as cash by the banks in India?

(a) 25%

(b) 20%

(c) 15%

(d) 10%

Answer : C

Question. Which of the following has essential feature of double coincidence?

(a) Money system

(b) Barter system

(c) Financial system

(d) Banking system

Answer : B

Question. Banks use the major portion of the deposits to

(a) Keep as reserve so that people may withdraw

(b) Meet their routine expenses

(c) Extend loans

(d) Meet renovation of bank

Answer : C

Question. ……………… help borrowers overcome the problem of lack of collateral and also they are the building blocks of organization of the rural poor.

(a) Government

(b) Banks

(c) Private sector

(d) SHGs

Answer : D

Question. In a SHG most of the decisions regarding savings and loan activities are taken by

(a) Bank.

(b) Members.

(c) Non-government organisation.

Answer : B

Question. Formal sources of credit does not include

(a) Banks.

(b) Cooperatives.

(c) Employers.

Answer : C

Question. Money acts as an intermediate in the exchange process. Which function of money is highlighted here?

(a) Measures of value

(b) Medium of exchange

(c) Store of value

(d) All of them

Answer : B

Question. Swapna is unable to repay the money lender and she is caught in debt. She has to sell a part of the land to pay off the debt. This situation is an example of

(a) Debt-loss

(b) Debt-insecurity

(c) Debt-trap

(d) All of them

Answer : C

Question. An agreement in which the lender supplies the borrower with money, goods or services in return for the promise of future payment.

(a) Credit (loan)

(b) Chit fund

(c) Bank

(d) Cheque

Answer : A

Question. What percent of their deposits do bank hold as cash?

(a) 50%

(b) 80%

(c) 15%

(d) 60%

Answer : C

Question. Which one of the following is the new way of providing loans to the rural poor?

(a) Cooperative societies

(b) Traders

(c) Relatives and friends

(d) SHGs

Answer : D

Question. Why do bank keep a small proportion of a deposits as cash with themselves?

(a) To extend loan to the poor.

(b) To extend loan facility.

(c) To pay salary to their staff.

(d) To pay the depositors who might come to withdraw money.

Answer : D

Question. Formal sector loans from

(i) Banks

(ii) Money lenders

(iii) Cooperatives

(iv) Traders

(a) (i) and (iii)

(b) (ii) and (iv)

(c) (ii) and (iii)

(d) (i) and (iv)

Answer : A

Question. It is important that the formal credit is distributed more equally so that

(a) Poor can benefit from cheaper loan

(b) Rich can get costly loan

(c) Rich can get cheaper loan

(d) None of the above

Answer : A

Question. Krishak Cooperative functioning in a village near Sonpur has……………farmers as members.

(a) 2500

(b) 2400

(c) 2350

(d) 2300

Answer : D

Question. Organization which supervises the credit activities of lenders in the informal sector.

(a) No organization

(b) Reserve bank of India (RBI)

(c) State government

(d) Central government

Answer : A

Question. Professor Muhammad Yunus is the founder of which one of the following banks?

(a) Cooperative Bank

(b) Commercial bank

(c) Grameen bank

(d) Land development bank

Answer : C

Question. What is the main source of income for bank?

(a) Interest on loan

(b) Interest on deposit

(c) Difference between the interest charge on borrowers and depositors

(d) None of the above

Answer : C

Question. The currency notes on behalf of the central government are issued by whom?

(a) State bank of India

(b) Reserve bank of India

(c) Punjab national bank

(d) Central bank of India

Answer : B

Question. Which one of the following is a modern form of currency?

(a) Gold

(b) Silver

(c) Copper

(d) Paper notes

Answer : D

Question. Which of the following is an asset that the borrower owns and uses as a guarantee until the loan is repaid to the lender?

(a) Property

(b) Money

(c) Collateral

(d) Deposits

Answer : C

Question. Which one of the following is the main source of credit for rich urban households in India?

(a) Formal sector

(b) Informal sector

(c) Money lenders

(d) Traders

Answer : A

Question. How many members a typical self – help group should have?

(a) 14-19

(b) 15-20

(c) 20-25

(d) 25-30

Answer : B

Question. Which one of the following statement is most appropriate regarding transaction made in money?

(a) It is the easiest way

(b) It is the safest way

(c) It is the cheapest way

(d) It promotes trade

Answer : A

Question. The informal source of credit does not include which one of the following?

(a) Traders

(b) Friends

(c) Cooperative societies

(d) Money – lenders

Answer : C

Question. It is a paper instructing the bank to pay a specific amount from the person’s account to the person in whose name it has been made is….

(a) Paper note

(b) Cheque

(c) Chit fund

(d) Credit card

Answer : B

Question. Salim, the shoe manufacturer, to meet expenses obtain loans from two sources.

(i) Ask leather supplier to supply leather on credit

(ii) Bank

(iii) Obtains loan in cash as advance payment

(iv) Relatives

(a) (i) and (iii)

(b) (i) and (ii)

(c) (iii) and (iv)

(d) (ii) and (iii)

Answer : A

Question. Money is accepted as a medium of exchange because the currency is authorized by………..

(a) Private sector

(b) Public sector

(c) Government

(d) People

Answer : C

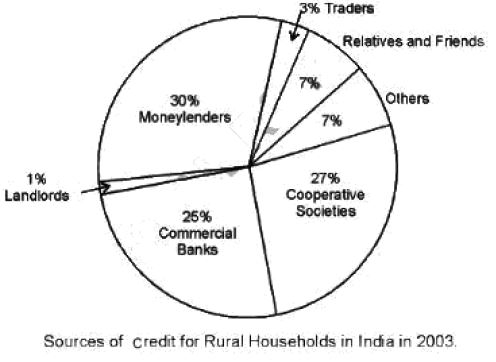

Question. Contribution of commercial banks as a source of credit for rural households in India in 2003 was

(a) 30%

(b) 28%

(c) 25%

(d) 26%

Answer : C

Question. After a year or two, if the SHG is regular in saving, it become eligible for availing loan from

(a) Cooperative societies

(b) Bank

(c) Money lenders

(d) Traders

Answer : B

Question. Deposits in the bank accounts can be withdrawn on demand, therefore these deposits are called

(a) Returnable deposits

(b) Acceptable deposits

(c) Demand deposits

(d) None of the above

Answer : C

Question. Banks provide a higher rates of interest on which one of the following account?

(a) Saving account

(b) Fixed deposits for long period

(c) Current account

(d) Fixed deposits for very short period

Answer : B

Question. In a barter system:

(a) Goods are exchange for money

(b) Goods are exchange for foreign currency

(c) Goods are exchange without the use of money

(d) Goods are exchanged on credit

Answer : C

Question. Formal sector meets only about……. Of the total credit needs of the rural people in 2003.

(a) One third

(b) One fourth

(c) Half

(d) Whole

Answer : C

Question. Anything which is generally accepted by the people in exchange of goods and services

(a) Money

(b) Barter

(c) Credit

(d) Loans

Answer : A

Question. Whether credit would be useful or not, depends on

(i) Whether there is some support in case of loss

(ii) Action of competitors

(iii) Market response

(iv) Risk in the situation

(a) (i) and (iii)

(b) (ii) and (iv)

(c) (ii) and (iii)

(d) (i) and (iv)

Answer : D

Question. Which one of the following is not a feature of money?

(a) Medium of exchange

(b) Lack of divisibility

(c) A store of value

(d) A unit of account

Answer : B

Question. In which one of the following system exchange of goods is done without use of money?

(a) Credit system

(b) Barter system

(c) Banking system

(d) Collateral system

Answer : B

Question. Terms of credit does not include…….

(a) Interest rate

(b) Collateral

(c) Cheque

(d) Mode of repayment

Answer : C

Question. Which among the following authorities issues currency notes?

(a) Government of India

(b) The state bank of India

(c) Central bank

(d) Reserve bank of India

Answer : D

Question. Modern forms of money include……

(i) Gold

(ii) Paper notes

(iii) Coins

(iv) Silver

(a) (i) and (iii)

(b) (ii) and (iv)

(c) (iii) and (iv)

(d) (ii) and (iii)

Answer : D

Question. Compared to the formal lenders, most of the informal lenders charges a much……. Interest on loans.

(a) Lower

(b) Constant

(c) Higher

(d) No interest

Answer : C

Fill in the blanks :

Question. ________ issues currency notes on behalf of the central government.

Answer : RBI

Question. Majority of credit needs of the__________ households are met from informal sources.

Answer : Rural

Question. Banks charges a higher interest rate on loans than what they offer on __________.

Answer : Deposits

Question. ___________ is an asset that the borrower owns and uses as a guarantee until the loan is repaid to the lender.

Answer : Collateral

Question. ___________ Costs of borrowing increase the debt-burden.

Answer : Higher

CASE STUDY Questions:

The Reserve Bank of India supervises the functioning of formal sources of loans. For instance, we have seen that the banks maintain a minimum cash balance out of the deposits they receive. The RBI monitors the banks in actually maintaining cash balance. Similarly, the RBI sees that the banks give loans not just to profit-making businesses and traders but also to small cultivators, small scale industries, to small borrowers, etc. Periodically, banks have to submit information to the RBI on how much they are lending, to who, at what interest rate, etc. There is no organisation which supervises the credit activities of lenders in the informal sector. They can lend at whatever interest rate they choose. There is no one to stop them from using unfair means to get their money back.

Question. RBI gives loans to----------------------------

1. To established cultivators, small scale industries, to small borrowers, etc.

2. To small cultivators, small scale industries, to small borrowers, etc.

3. To small cultivators, large scale industries, to small borrowers, etc.

4. None of the above

Answer : A

Question. There is no organisation which supervises the credit activities of lenders in the---------

1. Informal sector

2. Primary sector

3.Secondary sector

4.Tertiary sector

Answer : A

Question. Which organisation supervises the functioning of formal sources of loans in India? How?

Answer : The Reserve Bank of India supervises the functioning of formal sources of credit in India. It is the central bank of India.

It supervises the functioning of banks in the following ways :

The RBI monitors that the banks actually maintain a minimum cash balance out of the deposits they receive. Banks in India these days, hold about 15 per cent of their deposits as cash.

RBI ensures that the banks give loans not just to profit-making business and traders but also to small cultivators, small-scale industries, small borrowers, etc.

Periodically, banks have to submit information to the RBI on how much they are lending, to whom, at what interest rates, etc.

CASE STUDY Questions:

Modern forms of money include currency-paper notes and coins. Unlike the things that were used as money earlier, modern currency is not made of precious metal such as gold, silver and copper. And unlike grain and cattle, they are neither of everyday use. The modern currency is without any use of its own. Then, why is it accepted as a medium of exchange? It is accepted as a medium of exchange because the currency is authorised by the government as it legalises the use of rupee as a medium of payment that cannot be refused in settling transactions in India. No individual in India can legally refuse a payment made in rupees. Hence, the rupee is widely accepted as a medium of exchange in the country. In India, the Reserve Bank of India issues currency notes on behalf of the central government. As per Indian law, no other individual or organisation is allowed to issue currency. Moreover, the law legalises the use of rupee as a medium of payment that cannot be refused in selling transactions in India. No individual in India can legally refuse a payment made in rupees. Hence, the rupee is widely accepted as a medium of exchange.

Question. Who issues the currency notes in India? Which is our currency used nowadays?

(i) The State Bank of India issues currency notes on behalf of the district government. Nowadays paper notes and coins are used as currency in our country.

(ii) The Reserve Bank of India issues currency notes on behalf of the state government. Nowadays paper notes and coins are used as currency in our country.

(iii) The Reserve Bank of India issues currency notes on behalf of the Central government. Nowadays paper notes and coins are used as currency in our country.

(vi) The Rural Bank of India issues currency notes on behalf of the Central government. Nowadays only coins are used as currency in our country.

Answer : C

Question. What is accepted as the medium of exchange in India? 1

(i) Dollar is accepted as the medium of exchange in India.

(ii) Rupee is accepted as the medium of exchange in India.

(iii) Euro is accepted as the medium of exchange in India.

(iv) Dinar is accepted as the medium of exchange in India.

Answer : B

Question. What does the Indian Law say about the currency?

Answer : As per Indian law, no other individual or organisation is allowed to issue currency. Moreover, the law legalises the use of rupee as a medium of payment that cannot be refused in settling transactions in India.

ASSERTION/REASON TYPE QUESTIONS:

DIRECTION : Mark the option which is most suitable :

(a) If both assertion and reason are true, and reason is the correct explanation of assertion.

(b) If both assertion and reason are true, but reason is not the correct explanation of assertion.

(c) If assertion is true, but reason is false.

(d) If both assertion and reason are false.

Question. Assertion : The modern currency is used as a medium of exchange; however, it does not have a use of its own.

Reason : Modem currency is easy to carry

Answer : B

Question. Assertion : Banks charge a higher interest rate on loans than what

they offer on deposits.

Reason : The difference between what is charged from borrowers and what is paid to depositors is their main source of income.

Answer : A

Question. Assertion : In India, no individual can refuse to accept a payment made in rupees.

Reason Rupee is the legal tender in India.

Answer : A

Question. Assertion : Banks keep only a small proportion of their deposits as cash with themselves.

Reason : Banks in India these days hold about 15 per cent of their deposits as cash.

Answer : B

Question. Assertion : Credit would be useful or not depends on the risk involved in a situation.

Reason : The chance of benefitting from credit is highest in agriculture sector.

Answer : C

Question. Assertion : Rohan took credit in the form of advance payment from a buyer and he delivered the goods to the buyer on time and also earned profit. The credit made Rohan better off in this situation.

Reason : Credit can never push a person into a debt trap.

Answer : C

Question. Assertion : The facility of demand deposits makes it possible to settle payments without the use of cash.

Reason : Demand deposits are paper orders which make it possible to transfer money from one person’s account to another person’s account.

Answer : D

.

Short Answer Type Questions :

Question. How money serves as a medium of exchange?

OR

What is money? Why is modern money currency accepted as a medium of exchange?

OR

How does the use of money make exchange of things easier? Explain with example.

Answer : Money as the Medium of Exchange. People exchange goods and services through the medium of money. Money acts as a medium of exchange or medium of payments. A person holding money can easily exchange it for any commodity or service that he might want. It acts as an intermediary in the process of exchange.

Question. Why are most of the poor households deprived from the formal sector of loans?

Answer : Most of the poor households are deprived from the formal sector loans because of lack of proper documents and absence of collateral.

Question. What are the differences between formal and informal source of credit?

OR

Mention any three points of distinction between formal sector loan and informal sector loan.

Answer : Formal Sector Credit in India. It includes loans from banks and cooperatives. RBI supervises their functions of giving loans. Rich Urban Households depend largely on formal sources of credit. Lower rate of interest on loans is charged as compared to informal sources of credit.

Informal Sector Credit in India. It includes traders, employers, money lenders, relatives, etc. No organization is there to supervise its lending activities. Higher interest on loans is charged as compared to formal sources of credit. Poor households largely depend on informal sources of credit.

Question. What is money? Why is modern money/ currency accepted as a medium of exchange?

Answer : Money is a medium of exchange in transactions. A person holding money can easily exchange it for any commodity or service that he or she might want.

Modem money currency is accepted as a medium of exchange because;

• it is certified for a particular denomination (For example, ₹ 10, ₹ 20,

₹ 100, ₹ 1,000).

• it is issued by the Central Bank of the country

• it is authorized by the government of the country.

Question. What do you understand by demand deposits?

Answer : Banks accept the surplus money from the people as deposits and pay interest for that. People have the provision to withdraw their money as and when they require. Since money can be withdrawn on demand, these deposits are known as demand deposits.

Its features are: Features:

• A demand deposit has the essential characteristic of money. It can be used as a medium of exchange.

• The facility of cheques against demand deposits makes it possible to make payments, without using cash.

• Since demand deposits are accepted widely as a means of payment along with currency, they constitute money in the modem economy

Question. According to data of the year 2003, rich urban households took 90% of their loans from formal sources, whereas 10% from informal sources. Poor households in the urban areas took 85% of their loans from informal sources. What do these fact indicate?

Answer : The rich household are availing of cheap credit from formal lenders, whereas the poor households have to pay a heavy price for borrowing.

Question. ‘Problem of lack of double coincidence of wants exists in barter exchange’ explain.

Answer : Lack of double coincidence of wants under barter exchange...

'Simultaneous fulfillment of mutual wants by buyers and sellers' is known as double coincidence of wants. In barter exchange, this is lacking like the producer of wheat may want shoes in exchange for his wheat. But he may find it difficult to get a shoemaker who is also willing to exchange his shoe for jute. Thus a seller has to find out a person who wants to buy seller's goods and the same time who must have what the seller wants. This is the main drawback of barter exchange.

Question. Even when the banks are presents, it is difficult for poor household to get a loans from the bank than taking a loan from informal sources? Why is it so?

Answer : Bank loans require proper documents and collateral which is rarely available with poor households and it prevents them from getting bank loans.

On the other hand, informal lenders such as moneylenders know the borrower personally and are often willing to give a loan without collateral.

Question. Why are transactions made in money? Explain with suitable examples.

Answer : Because a person holding money can easily exchange it for any commodity or service that he or she might want.

For example, money solve the problems of double coincidence of wants by acting as a medium of exchange. If a shoe manufacturer wants to sell shoes in a market and buy rice under barter exchange, both parties selling shoes and rice have to agree to sell and buy each other’s commodity and this creates a problem which is referred to as double coincidence of wants. This problem is overcome by the introduction of money. Here the shoes manufacturer will first exchange shoes that he has produced for money and then exchange the money for rice.

Question. How does the use of money make exchange of things easier? Explain with example.

Answer : Money as the Medium of Exchange. People exchange goods and services through the medium of money. Money acts as a medium of exchange or medium of payments. A person holding money can easily exchange it for any commodity or service that he might want. It act as an intermediary in the process of exchange.

Question. Why banks are willing to lend to the poor women when organized in SHGs, even though they have no collateral as such?

Answer : Because any case of non - repayment of loan by any one member is followed up seriously by other members in the group. In other words, it is the group which is responsible for the repayment of the loan.

Question. Banks keep only a small proportion of their deposits as cash with themselves. Why?

Answer : This is kept as a provision to pay the depositors who might come to withdraw money from the bank on any given day.

Question. How does money solve the problem of double coincidence of wants? Explain with an example of your own.

Answer : In a barter system where goods are directly exchanged without the use of money, double coincidence of wants is an essential feature. By serving as a medium of exchanges, money removes the need for double coincidence of wants and the difficulties associated with the barter system. For example, it is no longer necessary for the farmer to look for a book publisher who will buy his cereals at the same time sell him books. All he has to do is find a buyer for his cereals. If he has exchanged his cereals for money, he can purchase any goods or service which he needs. This is because money acts as a medium of exchange.

Question. Why are transaction made in money? Explain with suitable example.

Answer : Transactions are made in many because a person holding a money can easily exchange it for any commodity or service that he or she might want.

For example, money solve the problems of double coincidence of wants by acting as a medium of exchange. If a shoe manufacturer wants to sell shoes in a market and buy rice under barter exchange, both parties selling shoes and rice have to agree to sell and buy each other’s commodity and this creates a problem which is referred to as double coincidence of wants. This problem is

overcome by the introduction of money. Here the shoes manufacturer will first exchange shoes that he has produced for money and then exchange the money for rice.

Question. Why do we need to expand formal sources of credit in India?

Answer : We need to expand formal sources of credit in India due to:→ To reduce dependence on informal sources of credit because the latter charge high interest rates and do not benefit the borrower much.

• Cheap and affordable credit is essential for country’s development.

• Banks and co-operatives should increase their lending particularly in rural areas.

Question. Manav needs a loan to set up a small business. On what basis will Manav decide whether to borrow from the bank or the moneylender? Discuss.

Answer : Manav will decide whether to borrow from the bank or the money lender on the basis of the following terms of credit:

• Rate of interest

• Requirements availability of collateral and documentation required by banker.

• Mode of repayment.

• Depending on these factors and of course, easier terms of repayment, Manav has to decide whether he has to borrow from the bank or the moneylender.

Question. How do banks mediate between those who have surplus money and those who need money?

Answer : Banks keep small portion deposits as cash (15%) for themselves (to pay the depositors on demand). They use the major portion of the deposits to extend loans to those who need money. In this way banks mediate between those who have surplus money and those who need money.

Question. How does the money solve the problems of double coincidence of wants? Explain with an example of your own.

Answer : Money solve the problem of double coincidence of wants by acting as a medium of exchange. If a shoe manufacturer wants to sell shoes in a market and buy rice under barter exchange, both parties have to agree to sell and buy each other’s commodities and this creates a problem which is referred to as double coincidence of wants. This problem is overcome by introduction of money. Here the shoe manufacturer will first exchange shoes that he has produced fir money and they exchange the money fir rice.

Question. Explain any four terms of credit with example.

Answer : While giving loan, the lenders specifies certain terms and condition relating to the loan to be followed by borrower which is known as term of credit. It includes,

(i) Interest Rate

(ii) Collateral

(iii) Documentation required

(iv) The mode of repayment.

Before giving loan a bank ensures about the financial capacity of the borrower to repay the loan. For this certain condition/requirement have to be fulfilled. Suppose, person X applies for a home loan to a particular bank then he has to submit documents showing his employment record and salary before bank agrees to give him a loan. Banks can retain the papers of new house as collateral. If the bank not satisfied with the paying capacity of a person and if a person does not submit anything to be considered as collateral, then banks might not be willing to lend to certain borrowers.

Question. Look at a 10 rupee note. What is written on top? Can you explain this statement?

Answer : “Reserve Bank of India” and “Guaranteed by the Government” are written on top. In India, Reserve Bank of India issues currency notes on behalf of the central government. The statement means that the currency is authorized or guaranteed by the Central Government. That is, Indian law legalizes the use of rupee as a medium of payment that can not be refused in setting transaction in India.

Question. Manav need a loan for set up a small business. On what basis Manav will decide whether to borrow from bank or from money lender? Discuss.

Answer : If Manav has all the necessary documents showing his paying capacity and collateral security then he will Good fir formal source of credit I.e., bank. Bank will be the best option as he can get loan at a reasonable rate of interest. If he cannot provide necessary documents required for loan from the bank then he has to depend on the informal sources of credit like money lender who sometime lends higher rate of interest and uses unfair means to get their money back.

Question. In situations with high risks, credit might create further problems for the borrower.

Explain.

Answer : In situations with high risks, credit might create further problems for the borrower. This is also known as a debt-trap. Taking credit involves an interest rate on the loan and if this is not paid back, then the borrower is forced to give up his collateral or asset used as the guarantee, to the lender. If a farmer takes a loan for crop production and the crop fails, loan payment becomes impossible. To repay the loan the farmer may sell a part of his land making the situation worse than before. Thus, in situations with high risks, if the risks affect a borrower badly, then he ends up losing more than he would have without the loan.

Question. Analyse the role of credit for development.

Answer : Cheap and affordable credit plays a crucial role for the country’s development. There is a huge demand for loans for various economic activities. The credit helps people to meet the ongoing expenses of production and thereby develop their business. Many people could then borrow for a variety of different needs. They could grow crops, do business, set up industries etc. In this way credit plays a vital role in the development of a country.

Question. What are the modern forms of money currency in India? Why is it accepted as a medium of exchange? How is it executed?

OR

What is currency? Explain any three features modern Indian currency

Answer : Modern forms of money currency in India are paper notes and coins.

It is accepted as a medium of exchange because currency is authorized by the government of country.

Reserve bank of India issues the currency notes on behalf of the central government. No other organization and individual can issue the currency. Everybody is bound to accept it. Its non-acceptance is an offence.

Question. Explain any two features each of formal sector loans and informal sector loans.

Answer : Features of formal sector loans:

• Here rate of interest is reasonable and lower as compared to informal sector loans.

• RBI supervise the functioning of formal source of loans.

Features of informal sector loans:

• Higher rate of interest is charged.

• There is no organization which supervise the functioning of informal source of loans and there is no one to stopping them for using unfair means to get their money back.

Question. Describe any four advantages of ‘Self-Help Groups’ for the poor.

Answer : (i) It helps in pooling the saving of the members, who are poor women.

(ii) Members can get timely loans for a variety of purposes and at a reasonable rate of interest.

(iii) It helps the borrowers to overcome the problem of lack of collateral.

(iv) It also provides a platform to discuss variety of social issues of their concern.

Question. After a year or two, if a SHG s regular in savings, it becomes eligible for availing loan from the bank. In whose name loan is sanctioned and for what purpose it is meant for?

Answer : Loan is sanctioned in the name of a group and is meant to create self - employment opportunities for the members.

Question. In situation with high risks, credit might create further problems for the borrower. Explain

OR

Why is cheap an affordable credit important for country’s development? Explain with three reasons.

OR

Why is there a great need to expand formal sector credit in India? Explain any three reasons.

Answer : If a farmer has taken a loan for crop production and due to unavoidable factors there is a crop failure then he cannot repay the loan. Now again he has to take a new loan to repay the earlier loan or sell some part of his property or land. Therefore here Credit has created a problems for the borrower as he falls in to a Debt Trap.

(a) It will help in reducing debt and avoid to fall in debt trap.

(b) It would lead to higher incomes of the people.

(c) Many people could then borrow cheaply for a variety of needs e.g., they could grow crops, do business and set up small scale industries.

Question. List some items which are kept as collateral security against loans. What happens if the borrower fail to repay the loans?

Answer : Collateral refers to use of assets by the borrower as a guarantee to a lender until the loan is repaid. Example of items used as collateral security- land titles, deposits with banks, livestock, etc.

The lender has the right to sell the asset or collateral to obtain payment in case borrower fails to repay the loan.

Question. Look at a 10 rupees note. What is written on top? Can you explain this statement?

Answer : On a 10 rupee note, matter written on the top is 'Guaranteed by the Central Government'. This note can be used for the medium of exchange because it is authorized by the government of the country. It cannot refused in payment for transactions. Everybody is bound to accept it in exchange for goods and services and in discharge of debts. None can refuse to accept it because its non-acceptance is an offense.

Question. What does term and credit include?

Answer : While giving loan, the lender specifies certain terms and conditions relating to the loan followed by the borrower which is known as term of credit. It includes interest rate, collateral and documentation required and mode of repayment.

Question. In India, about 80% of farmers are small farmers, who need credit for cultivation.

(i) Why might banks be unwilling to lend to small farmers?

(ii) What are the other sources from which the small farmers can borrow?

(iii) Explain with an example how the terms of credit can be unfavourable for the small farmer.

(iv) Suggest some way by which small farmers can get cheap credit.

Answer : (i) As the farmers find difficult to provide necessary documents / formalities and collateral security required for loan these banks might be unwilling to lend to small farmers.

(ii) These Farmers usually borrowed from informal source of credit like moneylenders, employers, relatives, Friends, etc.

(iii) Terms of credit for small farmers if they borrow from informal sources may carry a very high rate of interest which means that larger part of the earnings is used to repay loan.

(iv) Farmers get cheap credit through cooperatives and SHGs.

Question. Why should credit at reasonable rates be available for all?

Answer : nformal credit tries to exploit the poor farmers and workers by charging a very high rate of interest on loans and imposing unreasonable terms of credit. At present richer household avail the benefits of formal credit and poor have to depend on the informal source due to some weak point like absence of collateral security etc. Therefore it should be ensured that formal credit should provide credit at reasonable rates to all and especially poor ones to help them fulfil their needs.

Question. How does bank mediate with those who have surplus money and those who need money?

OR

What do the banks do with the deposits which they accept from the public? Explain.

Answer : Loans Activities of Banks. Basically, banks borrow money to lend. Banks pay interest (suppose x %) from whom it borrows. After keeping a portion of deposits as reserve, bank lend to people who demand money as a loan and bank charges interest (suppose y %) from them. The difference between what is charged from borrowers and what is paid to depositors is their main source of

income. After meeting all expenses of banks out of this income, the resultant is profit/loss for the bank.

Question. No individual in India can legally refuse a payment made in rupees. Why is it so?

Answer : The law legalize the use of rupee as a medium of payment that cannot be refused in settling transactions in India.

Question. Explain ‘Loans from Cooperatives.’

Answer : Cooperatives accept deposits from its members which becomes the basis (collateral) to obtain huge loan from the banks. These amounts are used for provide loans to members for purposes such as purchase of agricultural implements, loans for cultivation, construction of houses and a variety of other expenses. Another round of lending can take place after existing loans are repaid. There are different type of cooperative such as farmers, weavers, cooperative, etc.

Question. What are ‘Demand Deposits’? Describe any three salient features of Demand Deposits.

Answer : Demand deposits: Deposits in the bank account which are payable on demand are called Demand deposits.

Features of Demand deposits are:

(i) People has the provision to withdraw the money as and when they require.

(ii) Interest is paid by the bank on these deposits (If they come under saving account deposits - personal accounts and non-business account/current account).

(iii) Bank allows the owner of demand deposits to make out a Cheque for a specific amount.

Question. Suppose Swapna could not repay the loan due to the failure of the crop, due to which she had to sell part of the land and repay the loan. Here, credit, instead of helping her to improve earnings, left her worse off. What is this situation called?

Answer : This situation commonly called debt - trap.

Long Answer Type Questions :

Question. Define bank. Also explain the functions of commercial bank.

Answer : Any institution which accepts deposits from the public withdrawable by cheques and advances loans of various sorts is called a bank.

Commercial Bank: It is a financial institution which performs the functions of accepting deposits from the general public and giving loans for investment with the aim of earning profit.

Functions of Commercial Banks.

(i) It accept and collects the deposits from its customers. It can be in the form of saving account deposits, current account deposits, and fixed term deposits.

(ii) It gives loans and advances.

(iii) It provides overdraft facilities.

(iv) It discounts bills of exchange.

(v) It provides agency functions like transfer of funds, collection of funds, payments of various items, purchase and sale of shares and securities, acts as trustee, etc.

(vi) It finances foreign trade.

(vii) It perform general utility service like issue of traveler’s cheques and gift cheques, locker facility, etc.

(viii) It creates credit through loans.

Question. “RBI plays a crucial role in controlling formal sector loan.” Explain.

Or

In what ways does the Reserve Bank of India supervise the functioning of banks?

Answer : (1) The Reserve Bank of India supervises the functioning of formal sources of credit in India. It is the central bank of India.

(2) It supervises the functioning of banks in the following ways :

(i) The RBI monitors that the banks actually maintain a minimum cash balance out of the deposits they receive. Banks in India these days, hold about 15 per cent of their deposits as cash.

(ii) RBI ensures that the banks give loans not just to profit-making business and traders but also to small cultivators, small-scale industries, small borrowers, etc.

(iii) Periodically, banks have to submit information to the RBI on how much they are lending, to whom, at what interest rates, etc.

Question. Self-Help Groups can help in solving the problem of credit in rural areas. Explain.

Or

In what ways do Self-Help Groups help the rural sector of the economy?

Answer : (1) The absence of collateral is one of the major reasons which prevent the poor from getting bank loans. Whereas, there is no need for collateral or difficult paperwork to take loans from SHGs.

(2) SHGs have a lower interest rate than that of moneylenders or traders. They can get timely loans for a variety of purposes.

(3) It creates employment opportunities for the members who are rural poor, particularly women.

(4) It encourages regular savings of the rural poor.

(5) SHGs help rural women not only to become financially self-reliant but also, the regular meetings of the group provide a platform to discuss and act on a variety of social issues such as health, nutrition, domestic violence, etc.

Question. In what ways does the reserve bank of India supervise the functioning of banks? Why is this necessary?

OR

Which government body supervise the functioning of formal sources of loans in India? Explain into functioning.

OR

Who supervise the functioning of banks? In what ways is the supervision done?

Answer : RBI supervise the functioning of banks...

(i) It ensures that the banks actually keep a certain percentage of their deposits as cash balance/cash reserve with the central bank.

(ii) It observe that banks give loans to small activators, small scale industries, small borrowers also and not become a profit-making business.

(iii) Report has to be submitted periodically by the banks to RBI containing details such as how much they have lent, to whom and at what rate of interest, etc.

(iv) Central bank is the lender of last resort. Whenever banks are short of funds, they can take loans from the central bank. Thus it is source of great strength it the banking system.

(v) It acts as a bank of central clearance, settlements and transfers.

It is necessary for central bank to supervise the working of banks. The paper currency standard which is in operation in every country now has to be directed by some central authority like RBI. There are hundreds of banks in country. Sometimes banks due to profit motive and competition do not follow a common policy according to national requirements. Therefore, RBI will compel them to follow the appropriate policy under economic situation is necessary.

Question. Describe the function of money.

Answer : (i) Money as a Medium of Exchange. People exchange goods and services through the medium of money. Money acts as a medium of exchange or medium of payments. A person holding money can easily exchange it for any commodity or service that he might want. It acts as an intermediary in the process of exchange.

(ii) Money as a unit of Account - Money is the measuring rod. Values of all goods and services can be expressed in a single common unit called money.

(iii) Money as the standard of defined payments - Money is the link which connects the values of today with those of the future. Loans are taken and repaid in terms of money.

(iv) Money as a store of value - Money can store value of goods in liquid form. Holding money is equivalent to keeping a reserve of liquid assets because it can be easily converted into other things.

(v) Liquidity of money - Money is the most generally accepted commodity, it is also the most liquid of all resources. Possession of money enables one to get hold of almost any commodity in any place and any money never locks a buyer.

Question. In what ways does the Reserve Bank of India supervise the functions of Banks? Why is this necessary?

Answer : The Reserve Bank of India supervises the functions of banks in a number of ways:

• The commercial banks are required to hold part of their cash reserves with their RBI. RBI ensures that the banks maintain a minimum cash balance out of the deposits they receive.

• RBI observes that the banks give loans not just to profit making businesses and traders but also to small cultivators, small scale industries, small borrowers etc.

• The commercial banks have to submit information to the RBI on how much they arelending, to whom, at what interest rate etc.

This is necessary to ensure equality in the economy of the country and protect especially small depositors, farmers, small scale industries, small borrowers etc. In this process RBI also acts as the lender of the last resort to the banks.

Question. In India, about 80 per cent of farmers are small farmers, who need credit for cultivation.

(a) Why might banks be unwilling to lend to small farmers?

(b) What are the other sources from which the small farmers can borrow?

(c) Explain with an example how the terms of credit can be unfavourable for the small farmer.

(d) Suggest some ways by which small farmers can get cheap credit.

Answer : (a) Bank loans require proper documents and collateral as security against loans. But most of the times the small farmers lack in providing such documents and collateral. Besides, at times they even fail to repay the loan in time because of the uncertainty of the crop. So, banks might be unwilling to lend to small farmers.

(b) Apart from bank, the small farmers can borrow from local money lenders, agricultural traders, big landlords, cooperatives, SHGs etc.

(c) The terms of credit can be unfavorable for the small farmer which can be explained by the following –

Ramu, a small farmer borrows from a local moneylender at a high rate of interest i.e. 3 per cent to grow rice. But the crop is hit by drought and it fails. As a result Ramu has to sell a part of land to repay the loan. Now his condition becomes worse than before.

(d) The small farmers can get cheap credit from the different sources like – Banks, Agricultural Cooperatives, and SHGs.

Question. What are the reasons why the banks might not be willing to lend to certain borrowers?

Answer : The banks might not be willing to lend certain borrowers due to the following reasons:

• Banks require proper documents and collateral as security against loans. Some persons fail to meet these requirements.

• The borrowers who have not repaid previous loans, the banks might not be willing to lend them further.

• The banks might not be willing to lend those entrepreneurs who are going to invest in the business with high risks.

• One of the principle objectives of a bank is to earn more profits after meeting a number of expenses. For this purpose it has to adopt judicious loan and investment policies which ensure fair and stable return on the funds.

Question. What is the basic idea behind the SHGs for the poor? Explain in your own words.

Answer : The basic behind the SHGs is to provide a financial resource for the poor through organizing the rural poor especially women, into small Self Help Groups. They also provide timely loans at a responsible interest rate without collateral.

Thus, the main objectives of the SHGs are:

• To organize rural poor especially women into small Self Help Groups.

• To collect savings of their members.

• To provide loans without collateral.

• To provide timely loans for a variety of purposes.

• To provide loans at responsible rate of interest and easy terms.

• Provide platform to discuss and act on a variety of social issues such education, health, nutrition, domestic violence etc.

Question. Give the meaning of central bank. Describe the functions of central bank.

Answer : Central Bank: It is the apex institution of monetary system of a country. It is banker it the other banks and to government, it issues notes, controls money supply and credit, and maintains monetary stability.

Functions of Central Banks...

(i) It has the solo monopoly of issuing currency.

(ii) It acts as a banker to the government- both central and state governments. It carries out all banking business of the government.

(iii) It puts as an agency to regulate and supervise the proper functioning of other banks in a country.

(iv) It control credit and money supply through its monetary policy like bank rate, CRR, etc.

(v) It is a lender of lest resource for commercial banks.

(vi) It maintains the external value of currency.

(vii) It is the custodian of foreign exchange resources and nation's gold.

(viii) It performs the clearing house function.

(ix) It collect and compiles statistical information relating to banking and other financial sectors of the economy.

Question. Explain the inconvenience of barter – system/exchange.

Answer : (i) Lack of double coincidence of wants - Here, a seller has to find out a person who wants to buy seller's goods and at the same time who must have what the seller wants. This is the main drawback of barter exchange.

(ii) Absence of common measure of value - when thousands of articles are produced and exchanged, there will be unlimited number of exchange ratios. Absence of a common denominator in order to express exchange ratios create many difficulties.

(iii) Lack of Divisibility - If a person wants to purchase where equal to the value of half of his horse, he cannot do so without killing his horse. Thus lack of divisibility makes barter exchange impossible.

(iv) Difficulty in storing wealth - Holding of stocks of goods like cattle, wheat, potatoes, etc., involve costly storage and deterioration.

(v) Lack of satisfactory unit to engage in contracts - It is difficult to engage in contracts which involve future payments due to lack of any satisfactory unit.

Question. (a) “Cheap and affordable credit is essential for poor households both in rural and urban areas.” In the light of the above statement explain the social and economic values attached to it. Why?

OR

(b) “Cheap and affordable credit is crucial for the country’s development.” Assess the statement.

OR

(c) ‘Credit has its own unique role for development’. Justify the statement with arguments.

a. Why is it necessary for the banks and cooperative societies to increase their lending facilities in rural areas? Explain.

b. Why do we need to expand formal sources of credit in India?

OR

d) Study the diagram given below and answer the THREE questions that follows:

1. Which are the two major sources of credit?

2. Which one of them is the most dominant source of credit forrural households?

3. Why are most of the rural households depend on informal sources of credit?

Answer : (a) Cheap and affordable credit is crucial for the country’s growth

and economic development. Credit is in great demand for various kinds of economic activities—big or small investments, to set up business, buying cars, houses, etc.

• In rural areas credit helps in the development of agriculture by providing funds to farmers to buy seeds, fertilizers, expensive pesticides.

• Manufacturers need credit for buying raw material or to meet ongoing expenditure of production. Credit helps in the purchase of plant, machinery, equipment, etc.

• Some people may need to borrow for personal or family needs like marriage, hospitalisation etc.

Thus, cheap and affordable credit is crucial for the country’s growth and economic development.

OR

(b) Banks and Cooperatives can help people in obtaining cheap and affordable loans. This will help people to grow crops, do business, set up small-scale industries or trade in goods and also help indirectly in the country’s development. They should do so, so that relatively poor people do not have to depend on informal sources of credit like the money-lenders.

OR

(c). There is no organisation that supervises the credit activities of lenders in the informal sector. They lend at whatever interest rate they choose.

• No one can stop rural money-lenders from using unfair means to get their money back.

• Informal lenders charge a very high rate of interest on loans and as a result a larger part of the earnings of the borrowers and farmers are used to pay the loans.

• The amount to be repaid is often greater than income, and farmers and other borrowers in villages fall in a debt trap.

Thus, it is necessary that banks and co-operatives increase their lending, particularly in rural areas, so that dependence on informal sources of credit ends.

OR

d). 1.formal and informal sources of credit.

2. Informal lenders

3. i) Money lenders do not ask for collateral Complicated paper work or documentation is not involved

Value Based Questions :

Question. Banks use a major portion of the deposits to extend loans. There is a huge demand for loans for various economic activities. Banks make use of the deposits to meet the loan requirements of the people.

(a) In what way the banks meet the loan requirement of the people?

(b) What value are imbibed from the above paragraph?

Answer : (a) Banks, as a mediators, bring both the depositor and borrower on common platform and depositors get interest on the money deposited and borrower can get timely loan.

(b) Mediation. The banks become an intermediary between the depositors and borrowers.

Question. Explain what is meant by demand deposits? What is the valuable facility offered by demand deposits?

Answer : The people make deposits with bank, because at any given time people need some currency for the daily needs. Banks accept the deposits and also pay an interest on the deposits. People can also withdraw the money as and when needed by them. Since the deposits in the bank accounts are called demand deposits.

The facility offered by the demand deposit is that the payments can also be made through cheques. The payer who has an account with the bank, makes out a cheques for a specific amount. The bank takes the money from the person's account and gives it to the person in whose name the Cheque is issued. The essential characteristics is the medium of exchange.

Question. ‘In recent years, people have tried out some newer ways of providing loans to the poor. The idea is to organize rural poor, in particular women, into small self - help groups.’

Answer : (a) The members can get timely loans and SHG help borrowers overcome the problem of lack of collateral.

(b) (i) Team Spirit

(ii) Mutual Help and Saving

(iii) Social Value

CBSE Class 10 Economics Understanding Economic Development Chapter 3 Money And Credit Assignment

Access the latest Understanding Economic Development Chapter 3 Money And Credit assignments designed as per the current CBSE syllabus for Class 10. We have included all question types, including MCQs, short answer questions, and long-form problems relating to Understanding Economic Development Chapter 3 Money And Credit. You can easily download these assignments in PDF format for free. Our expert teachers have carefully looked at previous year exam patterns and have made sure that these questions help you prepare properly for your upcoming school tests.

Benefits of solving Assignments for Understanding Economic Development Chapter 3 Money And Credit

Practicing these Class 10 Economics assignments has many advantages for you:

- Better Exam Scores: Regular practice will help you to understand Understanding Economic Development Chapter 3 Money And Credit properly and you will be able to answer exam questions correctly.

- Latest Exam Pattern: All questions are aligned as per the latest CBSE sample papers and marking schemes.

- Huge Variety of Questions: These Understanding Economic Development Chapter 3 Money And Credit sets include Case Studies, objective questions, and various descriptive problems with answers.

- Time Management: Solving these Understanding Economic Development Chapter 3 Money And Credit test papers daily will improve your speed and accuracy.

How to solve Economics Understanding Economic Development Chapter 3 Money And Credit Assignments effectively?

- Read the Chapter First: Start with the NCERT book for Class 10 Economics before attempting the assignment.

- Self-Assessment: Try solving the Understanding Economic Development Chapter 3 Money And Credit questions by yourself and then check the solutions provided by us.

- Use Supporting Material: Refer to our Revision Notes and Class 10 worksheets if you get stuck on any topic.

- Track Mistakes: Maintain a notebook for tricky concepts and revise them using our online MCQ tests.

Best Practices for Class 10 Economics Preparation

For the best results, solve one assignment for Understanding Economic Development Chapter 3 Money And Credit on daily basis. Using a timer while practicing will further improve your problem-solving skills and prepare you for the actual CBSE exam.

You can download free PDF assignments for Class 10 Economics Chapter Understanding Economic Development Chapter 3 Money And Credit from StudiesToday.com. These practice sheets have been updated for the 2026-27 session covering all concepts from latest NCERT textbook.

Yes, our teachers have given solutions for all questions in the Class 10 Economics Chapter Understanding Economic Development Chapter 3 Money And Credit assignments. This will help you to understand step-by-step methodology to get full marks in school tests and exams.

Yes. These assignments are designed as per the latest CBSE syllabus for 2026. We have included huge variety of question formats such as MCQs, Case-study based questions and important diagram-based problems found in Chapter Understanding Economic Development Chapter 3 Money And Credit.

Practicing topicw wise assignments will help Class 10 students understand every sub-topic of Chapter Understanding Economic Development Chapter 3 Money And Credit. Daily practice will improve speed, accuracy and answering competency-based questions.

Yes, all printable assignments for Class 10 Economics Chapter Understanding Economic Development Chapter 3 Money And Credit are available for free download in mobile-friendly PDF format.