Read TS Grewal Solution Class 12 Chapter 7 Death of a Partner 2026. Students should study TS Grewal Solutions Class 12 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 12 Accountancy have been prepared by expert teachers. These TS Grewal Class 12 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 12 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 12 Accounts Chapter 7 Death of a Partner TS Grewal Solutions

TS Grewal Solutions for Chapter 7 Death of a Partner Class 12 Accounts have been provided below based on the latest TS Grewal Class 12 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 12 will help students to improve their concepts and easily solve accountancy questions for Class 12.

Chapter 7 Death of a Partner TS Grewal Class 12 Solutions

About this chapter: TS Grewal Class 12 Chapter 7 Death of a Partner is a very important chapter if you have to understand the concepts of accounting to be done in the event if death of a partner of a partnership firm. The chapter mainly focuses on the dissolution of the partnership firm, and the settlement of accounts of the deceased partner, and the surviving partners. There are various important topics explained such as need for a partnership deed that clearly defines the terms and conditions of the partnership and actions to be taken when a partner dies, accounting aspects relating to sale of assets, settlement of liabilities, distribution of profits, and the settlement of the capital account of the deceased partner.

Along with the concepts there are detailed examples which have been provided in the TS Grewal book which will help the students to understand how to solve questions relating to this topic when they are asked in exams. There are lot of practical questions too. Our teachers have provided detailed solutions to all questions which will help them to score more marks in examinations.

Solutions for TS Grewal's Double Entry Book Keeping: Accounting for Not-for-Profit Organizations and Partnership Firms (Vol.1)

Textbook for CBSE Class 12

TS Grewal Solutions Class 12 Accountancy

Chapter 7

Death of a Partner

Question 10. A, B and C are partners in a firm sharing profit and losses in the ratio 3:2:1. B died on 1st April, 2018. C, Son of B, is of the opinion that he is the rightful owner of his father’s share of profit, and the profit of the firm should be now shared between A and C equally. A does not agree. Settle the dispute between A and C by giving reason.

C is not correct in his claim, unless agreed; new profit-sharing ratio of the continuing partners remains same as their old profit – sharing ratio i.e. 3:1.

Short Answer Type Questions:-

Question 1. What problems arise when a partner dies? How would you deal with them as an accountant?

Below are the problems arise when a partner dies:-

1.) Change in profit sharing Ratio

2.) Treatment of goodwill

3.) Revaluation of assets and liabilities

4.) Accumulated profit, reserve, losses etc.

5.) Adjustment of Joint life Policy

6.) Adjustment of Capital

Below adjustment should be deal with them as an accountant:-

1.) Amount standing to the credit of the deceased Partner’s Capital Account and Current Account, if Capital Accounts are maintained following Fixed Capital Accounts Method.

2.) His share in the goodwill of the firm.

3.) His share of profit earned from the beginning of the financial year to the date of death.

4.) His share of gain on revaluation of assets and reassessment of liabilities.

5.) His share of accumulated profit and reserves.

6.) Interest on capital up to the date of his death, if allowed by the Partnership Deed.

7.) His salary or commission up to the date of his death, if allowed by the Partnership Deed.

Question 2. Explain the estimation of profit up to the date of death on the basis of time period involved.

It the time basis is used, the profit are assumed to have arisen uniformly over the year. Suppose, the profit for the previous year is Rs. 24,000 and a partner dies after tow months of the close of previous year. The profit for the two months will be Rs. 4,000 i.e. Rs 24,000 × . If the deceased partner 3/10th share of profit, his share of profit till the date of dearth will be Rs. 1200, the deceased partner’s share of profit is calculate das its agreed to among all the partner. It may be calculated on the basis of the provision year profit akledd it may be as or on basis of average profit of certain year.

EXERCISE..............

DEATH OF A PARTNER

Calculation of Profit of a Deceased Partner

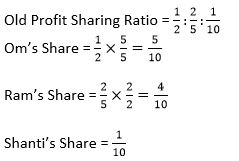

Question 1: Om, Ram and Shanti were partners sharing profits in the ratio of ½, 2/5 and 1/10. Find the new profit sharing ratio of the remaining partners if Shanti dies.

Answer 1:

Shanti Died. Hence, the new profit sharing Ratio = 5:4.

About Solution:-

The amount due to the retiring partner is paid according to the terms of partnership agreement. The retiring partners’ claim consists of

(a) The credit balance of Capital Account;

(b) His/her share in the Goodwill of the firm;

(c) His/her share in the Gain/Profit on Revaluation;

(d) His/her share in General Reserve and Accumulated Profit and

(f) Interest on Capital

Things to Remember:

The following deductions are made from the balance in his/her Capital Account on account:

(a) His/her share in the Loss on Revaluation;

(b) His/her Drawings and Interest on Drawings up to the date of retirement;

(c) His/her share of any accumulated losses and

(d) Loan taken from the firm.

Important Notes:

The total amount so calculated is the claim of the retiring partner. He/she is interested in receiving the amount at the earliest. Total payment may be made immediately after his/her retirement. However, the resources of the firm may not be adequate to make the payment to the retiring partner in lumpsum. The firm makes payment to retiring partner in instalments.

Question 2: A, B and C were partners sharing profits in the ratio of 4:3:2. A died, B and C will share profits in the ratio of 2:1. Determine the gaining ratio.

Answer 2:

Calculation of Gaining Ratio:-

Old Ratio = 4:3:2

New Ratio = 2:1

About Solution:-

Retiring partners’ claim is paid either out of the funds available with the firm or out of funds brought in by the remaining partners. The following journal entry is made for disposal of-the amount payable to the retiring partner:

On payment of cash in lump sum.

Retiring Partner’s Capital A/c Dr.

To Cash/Bank A/c (Amount paid to the retiring partner)

Things to Remember:

In this case the amount due to retiring partner is paid in instalments. Usually, some amount is paid immediately on retirement and the balance is transferred to his loan account. This loan is paid in one or more instalments. The loan amount carries some interest. In the absence of any agreement the rule under Section 37 of the Indian Partnership Act 1932 applies.

Important Notes:

According to this rule, if the amount due to the retiring partner is not paid immediately on his retirement, he can claim interest @ 6% p.a. on the amount due.

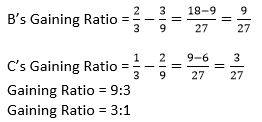

Question 3: A, B and C were partners sharing profits in the ratio of 4:3:2. A died, B and C will share profits in the ratio of 2:1. Determine the gaining ratio.

Answer 3:

Old Ratio = 4:3:2

A died

New Ratio = 2:1

B’s Gaining Ratio = 2/3-3/9 = 18-9/27 = 9/27

C’s Gaining Ratio = 1/3-2/9 = 9-6/27 = 3/27

New Profit Sharing Ratio = 9:3 = 3:1

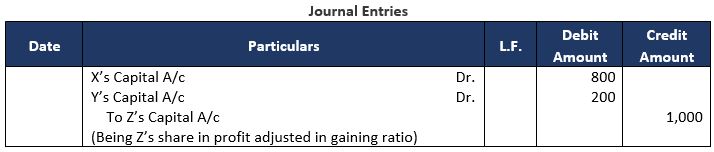

Question 4: (a) W, X, Y and Z are partners sharing profits and losses in the ratio of 1/3, 1/6, 1/3 and 1/6 respectively. Y died and W, X and Z decide to share the profits and losses equally in future. Calculate gaining ratio.

(b) A, B and C are partners sharing profits and losses in the ratio of 4:3:2. C died, A takes 4/9 of C’s share and balances is taken by B. Calculate the new profit sharing ratio and gaining ratio.

Answer 4:

About Solution:-

An instalment consists of two parts:

(i) Principal Amount of instalment due to retiring partner.

(ii) Interest at an agreed rate,

Things to Remember:

Interest due on loan amount is credited to retiring partners’ loan account. Instalment inclusive of interest then is paid to the retiring partner as per schedule agreed upon.

Important Notes:

On part payment in cash and balance transferred to his/her loan account.

Retiring Partner’s Capital A/c Dr.

To Cash/Bank A/c

To Retiring Partner’s Loan A/c

(Part payment made and balance transferred to loan A/c)

Question 5: Keshav, Nirmal, and Pankaj are partners sharing profits in the ratio of 5:3:2. Pankaj died and his share is taken by Keshav. Calculate the new profit-sharing ratio of Keshav and Nirmal.

Answer 5:

Calculation of New Profit Sharing Ratio:-

Old Ratio = 5:3:2

Keshav’s New Profit = 5/10 + 2/10 = 7/10

Nirmal’s New Profit = 3/10 + 0 = 3/10

New Profit sharing ratio = 7:3

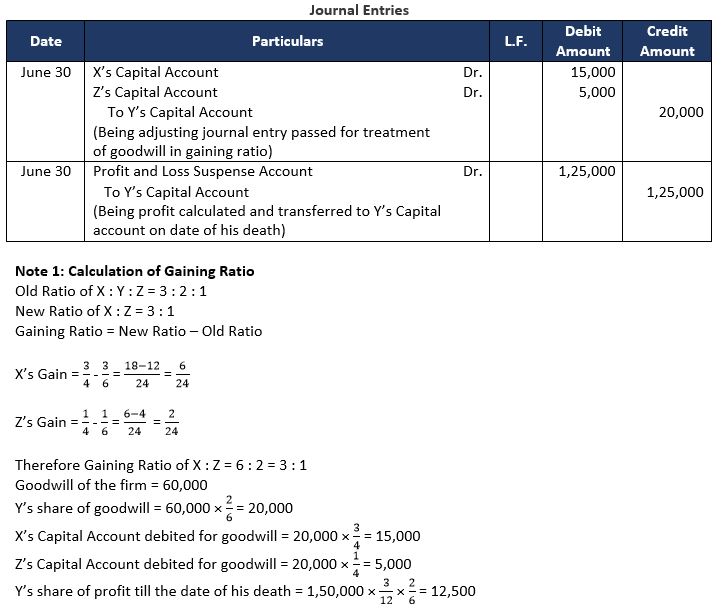

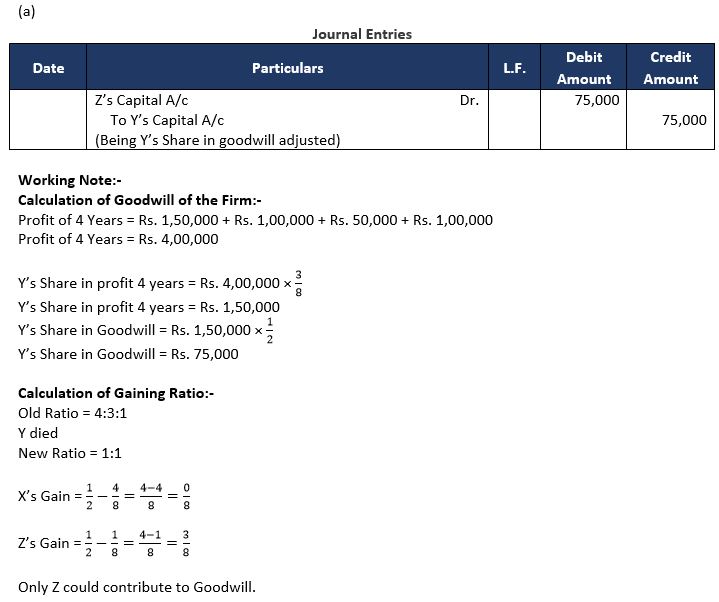

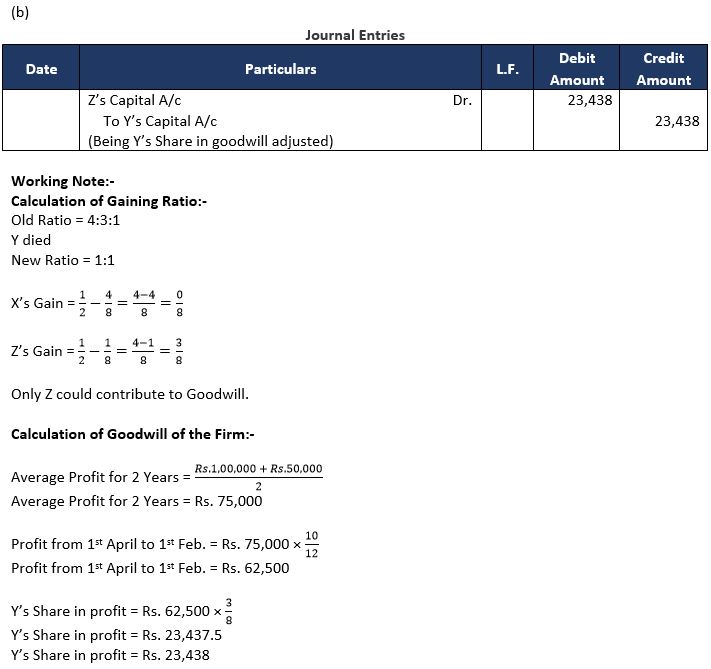

Question 6: X, Y and Z were partners in a firm sharing profit in 3:2:1 ratio. The firm closes its books on 31st March every year. Y died on 30th June, 2023. On Y's death the goodwill of the firm was valued at Rs. 60,000. Y's share in the profits of the firm till the time of his death was to be calculated on the basis of previous year's profit which was Rs. 1,50,000.

Pass necessary journal entries for the treatment of goodwill and Y's share of profit at the time of his death.

Answer 6:

About Solution:-

In this case, it is assumed that profit has been earned uniformly throughout the year.

Things to Remember:

In this method, we have to take into consideration the profit and the total sales of the last year. Thereafter the profit upto the date of death is estimated on the basis of the sale of the last year. Profit is assumed to be earned uniformly at the same rate.

Important Notes:

If the death of a partner occurs on any day during the year the executors of the deceased partner will also be entitled to the share of profits earned by the firm from the beginning of the year till the date of his death. Such profit may be ascertained from any of the following method:-

1.) On time basis

2.) On Turnover or Sales Basis.

Question 7: P, R and S are in partnership sharing profits 4/8, 3/8 and 1/8 respectively. It is provided in the partnership deed that on the death of any partner his share of goodwill is to be valued at one half of the net profit credited to his account during the last four completed years.

R died on 1st April, 2023. The firm’s profits for the last four years ended 31st March, were as:

2021- Rs. 1,20,000; 2022- Rs. 80,000; 2023- Rs. 40,000; 2023- Rs. 80,000

(a) Determine the amount that should be credited to R in respect of his share of Goodwill.

(b) Pass Journal entry for adjustment of Goodwill

Answer 7:

Profit for Last 4 Years = Rs. 1,20,000 + Rs. 80,000 + Rs. 40,000 + Rs. 80,000

Profit for Last 4 Years = Rs. 3,20,000

R’s Share in Profit = Rs. 3,20,000 × 3/8 = Rs. 1,20,000

R’s Share in Goodwill = Rs. 1,20,000 × 1/2 = Rs. 60,000

Gaining Ratio = 4:1

P’s Contribution = Rs. 60,000 × 4/5 = Rs. 48,000

S’s Contribution = Rs. 60,000 × 1/5 = Rs. 12,000

Question 8: P, Q and R were partners in a firm sharing profits in the ratio of 3 : 2 : 1. P dies and the new profit sharing ratio of Q and R was agreed to be equal. On P’s death, goodwill of the firm was valued at ₹ 60,000.

Pass the necessary entries for the treatment of goodwill under the following conditions:

(a) When Goodwill does not exist in the books of account; and

(b) When Goodwill exists in the books of account at ₹ 30,000.

Answer 8:

Question 9: Dinkar, Navita and Vani were partners sharing profits and losses in the ratio of 3:2:1. Navita died on 30th June, 2017. Her share of profit for the intervening period was based on the sales during that period, which were ₹ 6,00,000. The rate of profit during the past four years had been 10% on sales. The firm closes its books on 31st March every year. Calculate Navita’s share of profit.

Answer 9:

Calculation of Navita’s Share in Profit:-

Profit Sharing Ratio = 3:2:1

Navita Died

Sales of the firm upto 30th June 2017 = Rs. 6,00,000

Rate of Profit = 10%

Profit (1st April to 30th June) = Rs. 6,00,000 × 10%

Profit (1st April to 30th June) = Rs. 60,000

Navita’s Profit = Rs. 60,000 × 2/6

Navita’s Profit = Rs. 20,000

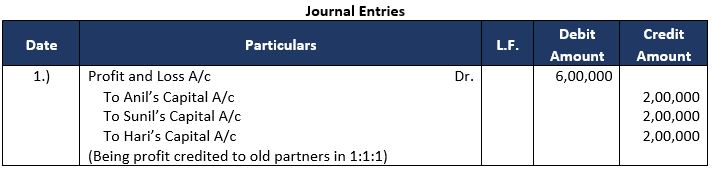

Question 10: Anil, Sunil and Hari were partners sharing profits equally. Suni died on 31st December 2022. In terms of the partnership deed, accounts were prepared for the period ended 31st December 2022 and net profit was determined at ₹ 6,00,000. Pass the Journal entry for the profit share of the partners.

Answer 10:

Question 11: A, B and C were partners in a firm sharing profits and losses in the ratio of 2:2:1. On 25th February 2019, B died, B’s share of profit till the date of his death was calculated at ₹ 5,000. Pass the necessary Journal entry for the same in the books of the firm.

Answer 11:

Question 12: A, B and C are partners sharing profits and losses in the ratio of 3:2:1. B died on 30th June, 2022, for the year ended 31st March, 2023, proportionate profits of 2022 is to be taken into consideration. During the year ended 31st March, 2023, bad debts of ₹ 2,000 had to be adjusted. Profit for the year ended 31st March, 2022 was ₹ 14,000 before adjustment of bad debts. Calculate B’s share of profit till the date of his death.

Answer 12:

Calculation of B’s Share:-

Profit for the year ended 31st March = Rs. 14,000 – Rs. 2,000

Profit for the year ended 31st March = Rs. 12,000

Profit upto 30th June = Rs. 12,000 × 3/12

Profit upto 30th June = Rs. 3,000

B’s Share in Profit = Rs. 3,000 × 2/6

B’s Share in Profit = Rs. 1,000

Question 13: Ram, Manu and Hari were partners in a firm. Hari died on 30th June, 2023. His share of profit from the closure of the last accounting year till the date of death was to be calculated on the basis of the average of three completed financial years of profits before death. Profits for the years ended 31st March, 2021, 2022 and 2023 were ₹ 1,10,000; ₹ 1,20,000 and ₹ 1,30,000 respectively. Calculate Hari’s share of profit till the date of his death and pass necessary Journal entry for the same.

Answer 13:

Calculation of Hari’s Share:-

Average Profit = 1,10,000 + 1,20,000 + 1,30,000 / 3

Average Profit = 3,60,000/3

Average Profit = Rs. 1,20,000

Profit upto 30th June = Rs. 1,20,000 × 3/12

Profit upto 30th June = Rs. 30,000

Hari’s Share in Profit = Rs. 30,000 × 1/3

Hari’s Share in Profit = Rs. 10,000

Question 14: X, Y and Z were partners sharing profits and losses in the ratio of 3:2:1. Y died on 30th June, 2022. Profit from 1st April, 2022 to 30th June, 2022 was ₹ 3,60,000. X and Z decided to share future profits in the ratio of 3:2 with effect from 1st July, 2022.

Pass the necessary Journal entries to record Y’s share of profit up to the date of death

Answer 14:

Question 15: Radha, Tina and Reeta were partners sharing profits equally. Reeta died on 31st July 2022. Radha and Tina decided to continue the business. Share of profit or loss of the deceased partner from the beginning of the year up to the date of death was to be determined on the basis of last year’s profit, which was ₹ 4,50,000. Pass necessary Journal entry to record Reeta’s share of profit/loss up to the date of death.

Answer 15:

Working Note:-

Calculation of Reeta’s Share in Profit:-

Profit for the year = Rs. 4,50,000

Profit upto 31st July = Rs. 4,50,000 × 4/12

Profit upto 31st July = Rs. 1,50,000

Reeta’s Share in Profit = Rs. 1,50,000 × 1/3

Reeta’s Share in Profit = Rs. 50,000

Question 16: Manoj, Rakesh and Harsh were partners sharing profits in the ratio of 2:2:1. Manoj died on 30th June, 2022. Rakesh and Harsh decided to continue the business. Share of profit or loss of the deceased partner from the beginning of the year up to the date of death was to be determined on the basis of last year’s profit. Last year’s loss was ₹ 2,00,000.

Pass necessary Journal entry to record Manoj’s share of profit/loss up to the date of death.

Answer 16:

Working Note:-

Loss of the year = Rs. 2,00,000

Loss upto 30th June = Rs. 2,00,000 × 3/12

Loss upto 30th June = Rs. 50,000

Manoj’s Share in Loss = Rs. 50,000 × 2/5

Manoj’s Share in Loss = Rs. 20,000

Question 17: A, B and C were partners sharing profits in the ratio of 3 : 2 : 1. The firm closes its books on 31st March every year. B died on 30th June, 2022. On his death, Goodwill of the firm valued at ₹ 6,00,000. B’s share in profit or loss till the date was to be calculated on the basis of previous year’s profit which was ₹ 15,00,000 (Loss). Pass necessary Journal entries for goodwill and his share of loss.

Answer 17:

Working Note:-

Calculation of Goodwill:-

Goodwill of the Firm = Rs. 6,00,000

B’s Share in Goodwill = Rs. 6,00,000 × 2/6

B’s Share in Goodwill = Rs. 2,00,000

Gaining Ratio = 3:1

A’s Contribute = Rs. 2,00,000 × 3/4 = Rs. 1,50,000

C’s Contribute = Rs. 2,00,000 × 1/4 = Rs. 50,000

Calculation of B’s share in loss:-

Loss of the year = Rs. 15,00,000

B’s share in loss = Rs. 15,00,000 × 3/12 × 2/6

B’s share in loss = Rs. 1,25,000

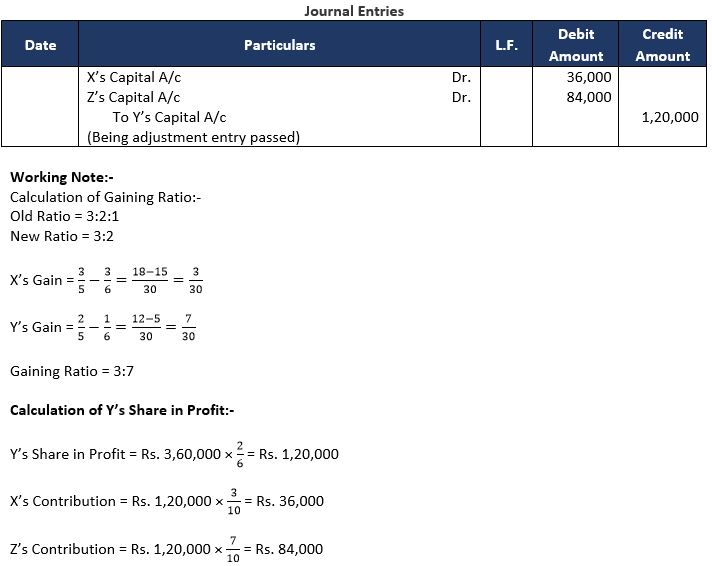

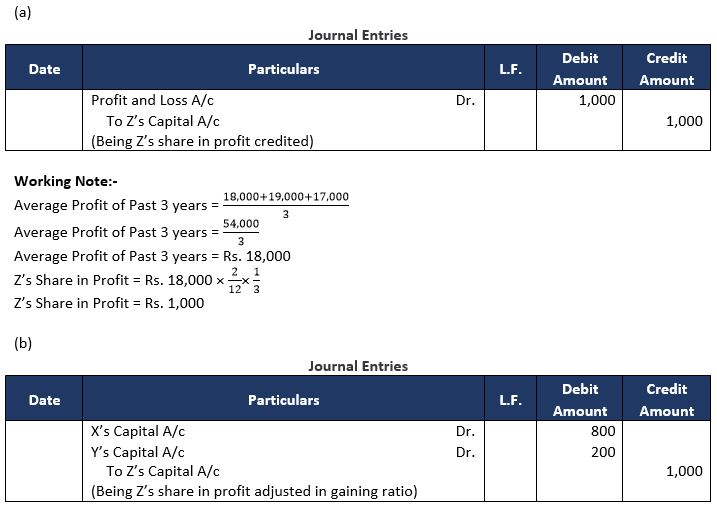

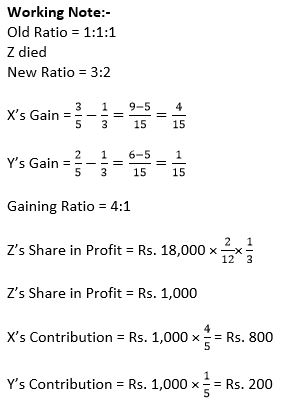

Question 18: X, Y and Z were partners in a firm. Z died on 31st May, 2022. His share of profit from the closure of the last accounting year till the date of death was to be calculated on the basis of the average of three completed years of profits before death. Profits for the years ended 31st March, 2020, 2021 and 2022 were ₹ 18,000; ₹ 19,000 and ₹ 17,000 respectively.

Calculate Z’s share of profit till his death and pass necessary Journal entry for the same when:

(a) Profit sharing ratio of remaining partners does not change, and

(b) Profit sharing ratio of remaining partners changes and new ratio being 3:2.

Answer 18:

Question 19: A, B and C were partners sharing profits and losses in the ratio of 2 : 2 : 1. C died on 30th June, 2023. Profit and sales for the year ended 31st March, 2023 were ₹ 1,00,000 and ₹ 10,00,000 respectively. Sales during April to June, 2023 were ₹ 1,50,000. You are required to calculate share of profit of C till the date of his death. Calculation

Answer 19:

Calculation of Profit upto 30th June:-

Profit for the year = Rs. 1,00,000

Sales for the year = Rs. 10,00,000

Question 20: Ajay, Bhawna and Shreya were partners sharing profits in the ratio of 2:2:1. On 1st July, 2022 Shreya died. The books of accounts are closed on 31st March every yer. Sales for the year 2021-22 ₹ 5,00,000 and that from 1st April to 30th June, 2022 were ₹ 1,40,000. Rate of profit during the past three years had been 10% on sales. Since Shreya’s legal representative was her only son, who is differently abled, it was decided that the profit for the purpose of settling Shreya’s account is to be calculated as 20% on sales.

Calculate Shreya’s share of profits till the date of her death and pass necessary Journal entry for the same.

Answer 20:

Working Note:-

Sales from 1st April 2020 to 30th June 2020 = Rs. 1,40,000

Profit = 20% of sales

Sales from 1st April 2020 to 30th June 2020 = Rs. 1,40,000 × 20% = Rs. 28,000

Shreya’s Share in Profit = Rs. 28,000 × 1/5

Shreya’s Share in Profit = Rs. 5,600

Question 21: Raman, Param and Karan were partners sharing profits and losses in the ratio of 3:2:1. Param died on 31st December, 2022. Accounts of the firm are closed on 31st March every year. Sales for the year ended 31st March, 2022 was ₹ 12,00,000 and sales for the nine months ended 31st December, 2022 was ₹ 6,00,000. Loss for the year ended 31st March, 2022 was ₹ 90,000. Calculate deceased partner’s share of profit/loss from the beginning of the accounting year up to 31st December, 2022.

Answer 21:

Calculation of Param’s Share in Loss:-

Total Sales = Rs. 12,00,000

Loss for the year ended = Rs. 90,000

Loss Percentage = 90,000/12,00,000 × 100

Loss Percentage = 7.5%

Sales from 1st April to 31st Dec. = Rs. 6,00,000

Loss for the same period = Rs. 6,00,000 × 7.5%

Loss for the same period = Rs. 45,000

Param’s Share in Loss = Rs. 45,000 × 2/6

Param’s Share in Loss = Rs. 15,000

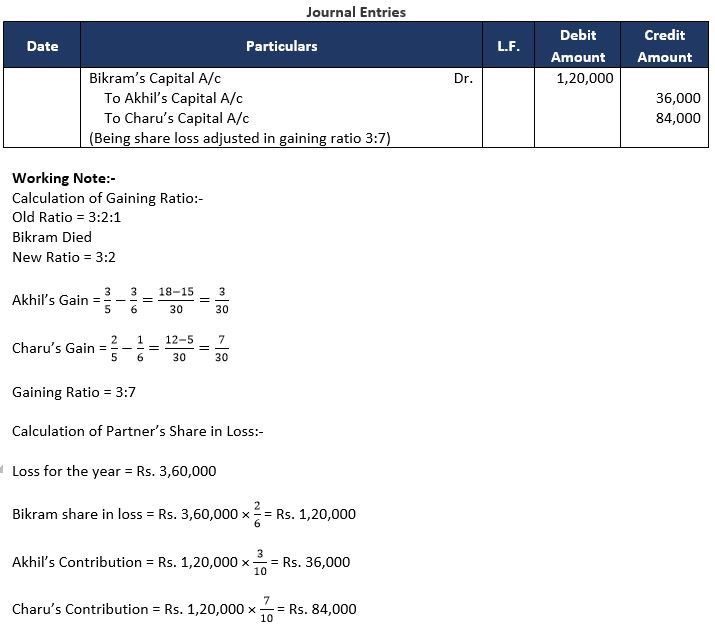

Question 22: Akhil, Bikram and Charu were partners sharing profits and losses in the ratio of 3:2:1. Bikram died on 30th September, 2022. Loss from the beginning of the accounting year till the date of death was estimated at ₹ 3,60,000. Akhil and Charu decided to share future profits in the ratio of 3:2 w.e.f. 1st October, 2022. Pass the necessary Journal entry to record Bhuwan’s share of profit/loss up to the date of death.

Answer 22:

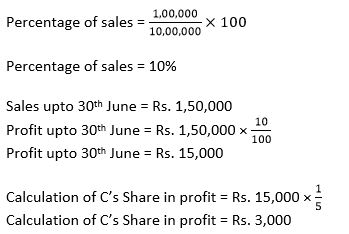

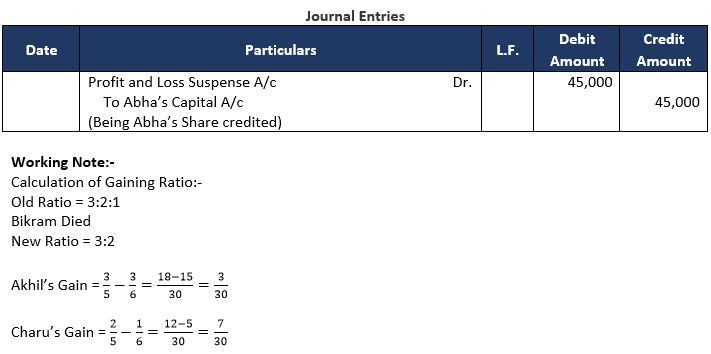

Question 23: Abha, Beena and Chanda were partners in a firm sharing profits and losses in the ratio of 5:3:2. Abha died on 1st July, 2023. The partnership Deed provided that Abha’s executors are entitled to her share of profit till the date of death calculated on the basis of sales for the immediate previous year. Sales for the year ended 31st March, 2023 was ₹ 12,00,000 and the profit for the same year was ₹ 3,00,000. Sales shows a growth trend of 20% and percentage of profit earning remains the same. Journalise the transaction along with working notes.

Answer 23:

Gaining Ratio = 3:7

Calculation of Partner’s Share in Profit:-

Sales for the Previous Year = Rs. 12,00,000

Profit for the year = Rs. 3,00,000

Percentage of profit = 3,00,000/12,00,000×100

Percentage of profit = 25%

Sales for the Current Year = Rs. 12,00,000 + (Rs. 12,00,000 × 20%)

Sales for the Current Year = Rs. 12,00,000 + Rs. 2,40,000

Sales for the Current Year = Rs. 14,40,000

Sales for 1st April to 30th June = Rs. 14,40,000 × 3/12

Sales for 1st April to 30th June = Rs. 3,60,000

Profit for 1st April to 30th June = Rs. 3,60,000 × 25%

Profit for 1st April to 30th June = Rs. 90,000

Abha’s Share in Profit = Rs. 90,000 × 5/10

Abha’s Share in Profit = Rs. 45,000

Question 24: X, Y and Z were partners in a firm sharing profits in the ratio of 4:3:1. The firm closes its books on 31st March every year. On 1st February, 2024, Y died and it was decided that the new profit sharing ratio between X and Z will be equal. Partnership Deed provided for the following on the death of a partner:

(a) His share of goodwill be calculated on the basis of half of the profits credited to his account during the previous four completed years. The firm’s profits for the last four years were:

(b) His share of profit in the year of his death was to be computed on the basis of average profit of past two years.

Pass necessary Journal entries relating to goodwill and profit to be transferred to Y’s Capital Account.

Answer 24:

Question 25: Iqbal and kamal are in partnership sharing profits and losses in 3 : 2. Kamal died three months after the date of the last Balance Sheet. According to the Partnership Deed, his legal heir is entitled to the following:

(a) His capital as per the last Balance Sheet.

(b) Interest on above capital @ 3% p.a. till the date of death.

(c) His share of profit till the date of death calculated on the basis of last year’s profits

Answer 25:

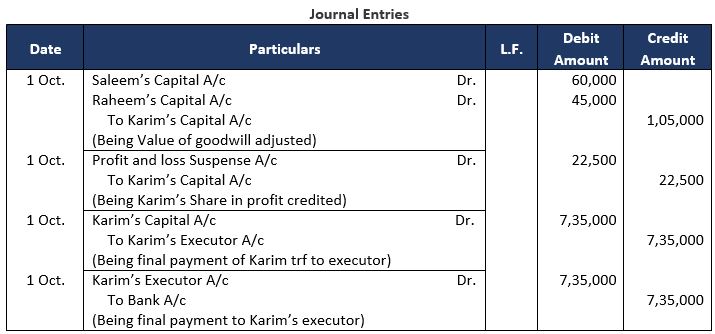

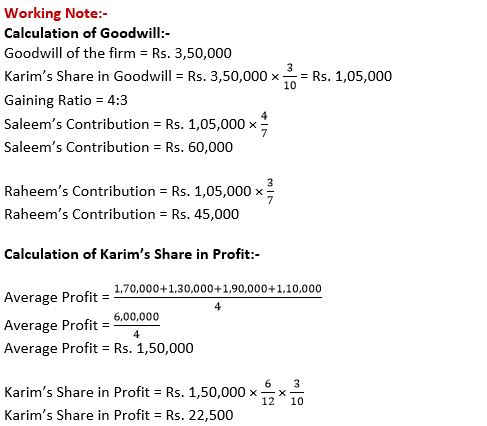

Question 26: Karim, Saleem and Raheem were partners in a firm sharing profits and losses in the ratio of 3:4:3. The firm closes its books on 31st March every year. On 1st October, 2019, Karim died. On Karim’s death, the goodwill of the firm was valued at ₹ 3,50,000. Karim’s share in the profits of the firm in the year of his death was to be calculated on the basis of average profits of last four years. The profits for the last four years were 2015 – 16 – ₹ 1,70,000; 2016 – 17 – ₹ 1,30,000; 2017 – 18 – ₹ 1,90,000 and 2018-19 – ₹ 1,10,000. The total amount payable to Karim’s executors on his death was ₹ 7,35,000. It was paid on 15th October 2019.

Pass necessary Journal entries for the above transactions in the books of the firm.

Answer 26:

About Solution:-

Accounting Standard 26 (Ind AS-38) specifies that goodwill can be recorded in the books only when some consideration is money or money’s worth has been paid for it. Hence, only purchased goodwill can be recorded in the books and the goodwill account cannot be raised.

Things to Remember:

As such in case of retirement or death of a death of a partner, the adjustment for goodwill will be made through partner’s capital accounts. The retiring or deceased partner’s capital account will be credited with his share of goodwill and continuing partner’s capital accounts will be debited in their gaining ratio.

Important Notes:

Journal entry will be recorded:-

Continuing Partner’s Capital A/c Dr.

To Retiring/Deceased Partner’s Capital A/c

(Retiring/Decrease partner’s share goodwill adjustment to continuing partners in the gaining ratio

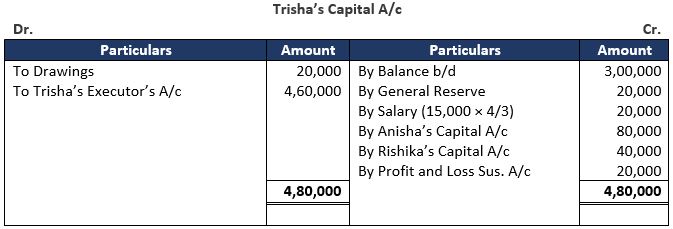

Question 27: Trisha, Anisha and Rishika were partners in a firm sharing profits and losses in the ratio of 2:2:1. Their Balance sheet as at 31s March, 2022 was as follows:

Trisha died on 31st July, 2022. According to the partnership deed, the executors of the deceased partner were entitled to:

(i) Balance in Partner’s Capital Account.

(ii) Salary @ ₹ 15,000 per quarter.

(iii) Share of goodwill calculated on the basis of twice the average of past three year’s profits.

(iv) Share of profits from the closure of the last accounting year till the date of death on the basis of last year’s profit. Profit for 2019-20, 2020-21 and 2021-22 were ₹ 1,00,000, ₹ 2,00,000 and ₹ 1,50,000 respectively.

(v) Trisha withdrew ₹ 20,000 on 1st May, 2022 for her personal use.

Showing your working clearly, prepare Trisha’s Capital Account to be rendered to her executors.

Answer 27:

Working Note:-

Calculation of Goodwill:-

Average Profit = (1,00,000+2,00,000+1,50,000)/3

Average Profit = 4,50,000/3

Average Profit = Rs. 1,50,000

Goodwill of the firm = Average Profit × Number of year purchases

Goodwill of the firm = Rs. 1,50,000 × 2

Goodwill of the firm = Rs. 3,00,000

Karim’s Share in Goodwill = Rs. 3,00,000 × 2/5 = Rs. 1,20,000

Gaining Ratio = 2:1

Saleem’s Contribution = Rs. 1,20,000 × 2/3

Saleem’s Contribution = Rs. 80,000

Raheem’s Contribution = Rs. 1,20,000 × 1/3

Raheem’s Contribution = Rs. 40,000

Calculation of Tanisha’s Profit upto 31st July:-

Profit for the year = Last year profit = Rs. 1,50,000

Taisha’s Share in profit = Rs. 1,50,000 × 2/5 × 4/12

Taisha’s Share in profit = Rs. 20,000

About Solution:-

In case of death of the partner, partnership will come to an end immediately. In such a case remaining partners may continue the business. All amounts due to the deceased partner will be paid to his legal representative/Executor.

Things to Remember:

Executor is the person named in a Will or appointed by a court to wind up the deceased partner’s financial affairs after death. He is entitled to all the amounts due to the deceased partner.

Important Notes:

If a partner dies on any date after the date of the Balance Sheet, then his share of profits is calculated from the beginning of the year to the date of death on the following basis: 1. On the Basis of Time: When share of profit is calculated on the basis of time, it may be on the basis of previous years’ profit or average profit of the last year.

Profit from the date of last balance sheet to the date of death = (Number of days or month from the date of last balance sheet to the date of death/ 365 or 12) × Previous years’ profit or Average profits of given number of past years.

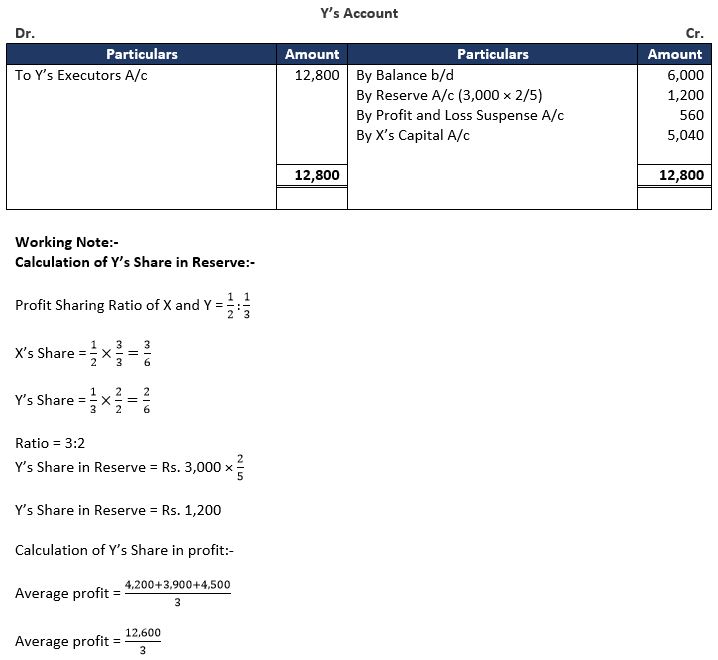

Question 28: X and Y are partners. The Partnership Deed provides inter alia:

(a) That the Accounts be balanced on 31st March every year.

(b) That the profits be divided as: X one-half, Y one-third and carried to a Reserve one-sixth.

(c) That in the event of the death of a partner, his Executors be entitled to be paid:

(i) The capital to his credit till the date of death.

(ii) His proportions of profits till the date of death based on the average profits of the last three completed years.

(iii) By way of Goodwill, his proportion of the total profits for the three preceding years.

Profits for three years ended 31st March, were: 2021 – ₹ 4,200; 2022 – ₹ 3,900; 2023 – ₹ 4,500. Y died on 1st August, 2023. Prepare necessary accounts.

Answer 28:

Average profit = Rs. 4,200

Profit from 1st April to 1st Aug. = Rs. 4,200 × 4/12

Profit from 1st April to 1st Aug. = Rs. 1,400

Y’s Share in Profit = Rs. 1,400 × 2/5

Y’s Share in Profit = Rs. 560

About Solution:-

According to provision of the Partnership Act, 1932 profit and losses are share equally by the partners; interest on capital is not paid, interest on drawings is not charged from partners, interest on loan is paid @6%, remuneration is not paid, new partner cannot be admitted unless all the partners agree.

Things to Remember:

If there is no agreement as to the rate of interest, he is entitled to receive interest on loan @6% per annum.

Important Notes:

Interest on a partner's loan is a gain for the company (since this revenue does not accrue on a regular and continuous basis). The interest on a partner's loan is credited to the Profit and Loss A/c.

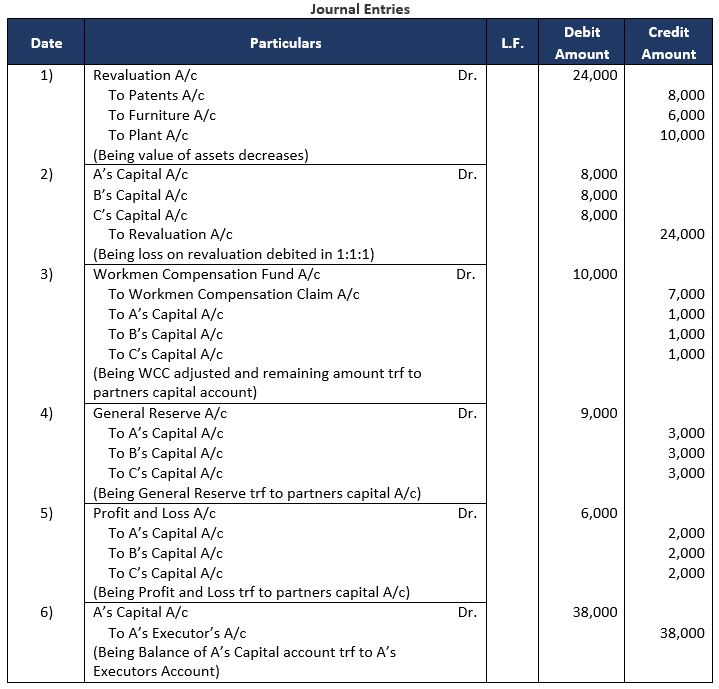

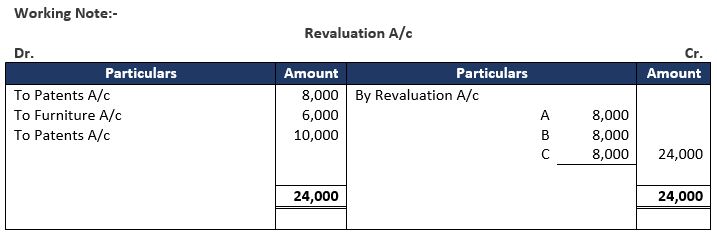

Question 29: A, B and C were partners in a firm. A died on 31st March, 2018 and the Balance Sheet of the firm on that date was as under:

On A’s death it was found that patents were valueless, furniture was to be brought down to Rs. 24,000, plant was to be reduced by Rs. 10,000 and there was a liability of Rs. 7,000 on account of workmen’s compensation. Pass the necessary Journal entries for the above at the time of A’s death.

Answer 29:

About Solution:-

An executor's account in accounting is a record of any form of account that an executor must reconcile if they are required to distribute the estate's assets. Retirement accounts and life insurance plans are two examples of this.

Things to Remember:

Profit sharing ratio of remaining partners is decided according to the mutual agreement among the remaining partners.

Important Notes:

There is no need to compute the gaining ratio when the continuing partners decide to share profits in the same ratio that existed among them prior to retirement.

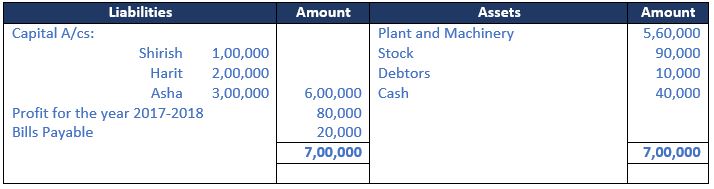

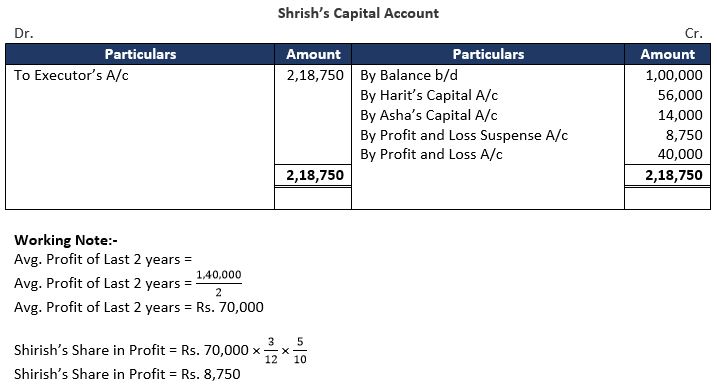

Question 30: Shirish, Harit and Asha were partners in a firm sharing profits in the ratio of 5:4:1. Shirish died on 30th June, 2018. On this date, their Balance Sheet was follows:

According to the Partnership Deed, in addition to deceased partner’s capital his executor is entitled to:

(i) Share in profit in the year of death on the basis of average of last two years’ profit. Profit for the year 2016-17 was Rs. 60,000.

(ii) Goodwill of the firm was to be valued at 2 years’ purchase of average of last two years’ profits.

Prepare Shrish’s Capital Account to be presented to his executor.

Answer 30:

Calculation of Goodwill of the Firm:-

Goodwill of the firm = Average Profit × Number of Year purchases

Goodwill of the firm = Rs. 70,000 × 2

Goodwill of the firm = Rs. 1,40,000

About Solution:-

Assets and liabilities are revalued because the profit or loss due to their revaluation is divided between all partners in their old profit sharing ratio.

Things to Remember:

If amount due to a retiring partner or legal representative of a deceased partner is not paid in full, they have the choice to get either of the following:

(i) Interest @6% per annum on the balance amount.

(ii) Share in subsequent profit of the firm in proportion to the balance amount.

Important Notes:

Gaining ratio is required because the continuing partners will pay the amount of goodwill to the retiring partner or executor of decease partner in their gaining ratio.

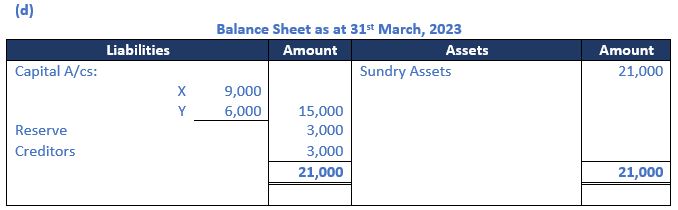

Question 31: The Balance Sheet of A, B and C who were sharing profits in the ratio of 3:3:4 as at 31st March, 2019 was as follows:

A died on 1st October, 2019. The partnership deed provided for the following on the death of a partner:

(a) Goodwill of the firm be valued at two year’s purchases of average profits for the last three years.

(b) The Profit for the year ending 31st March, 2019 was Rs. 50,000.

(c) Interest on Capital was to be provided @ 6% p.a.

(d) The average profits of the last three years were Rs. 35,000.

Prepare A’s Capital Account to be rendered to his executors.

Answer 31:

Working Note:-

Calculation of Partners Share in Goodwill:-

Goodwill of the Firm = Rs. 35,000 × 2

Goodwill of the Firm = Rs. 70,000

A’s Share in Goodwill = Rs. 70,000 × 3/10

A’s Share in Goodwill = Rs. 21,000

Gaining Ratio = 3:4

B’s Contribution = Rs. 21,000 × 3/7 = Rs. 9,000

C’s Contribution = Rs. 21,000 × 4/7 = Rs. 12,000

Calculation of A’s share in Profit:-

A’s Share in Profit = Rs. 50,000 × 6/12 × 3/10

A’s Share in Profit = Rs. 7,500

About Solution:-

After retirement of a partner the remaining partners may decide to adjust their capital. Often the remaining partners determine the total amount of capital of the reconstituted firm and decide to keep their respective capital accounts in proportion to the new profit sharing ratio. The total capital of the firm may be more or less than the total of their capital at the time of retirement.

Things to Remember:

The new capitals of the partners are compared with the balance standing to the credit of respective partner’s capital account. If there is a surplus in the capital account, the amount is withdrawn by the concerned partner. The partner brings cash in case the balance in the capital account is less than the calculated amount.

Important Notes:

In this case the total amount of adjusted capital of the remaining partners is rearranged as per agreed proportion in which they share profit of the reconstituted firm. The following steps may be adopted:

(i) Add the balance standing to the credit of the remaining partners’ capital accounts.

(ii) The total so obtained is the total capital of the firm.

Question 32: X, Y and Z were partners in a firm sharing profits in the ratio of 2:2:1. On 31st March, 2022, their Balance Sheet was as follows:

Y died on 30th June, 2023. Partnership Deed provided for following on the death of a partner:

(i) Goodwill of the business was to be calculated on the basis of 2 times the average profit of the past 5 years. Profit for the years ended 31st March, 2023, 31st March, 2022, 31st March, 2021, 31st March, 2020 and 31st March, 2019 were Rs. 3,20,000 (Loss); Rs. 1,00,000; Rs. 1,60,000; Rs. 2,20,000 and Rs. 4,40,000 respectively.

(ii) Y’s share of profit or loss from 1st April, 2023 till his death was to be calculated on the basis of the profit or loss for the year ended 31st March, 2023.

You are required to calculate the following:

(a) Goodwill of the firm and Y’s share of goodwill at the time of the death.

(b) Y’s share in the profit and loss of the firm till the date of his death.

(c) Prepare Y’s Capital Account at the time of his death to be presented to his executors

Working Note:-

Calculation of Goodwill:-

Average Profit of 5 years = 4,40,000+2,20,000+1,60,000+1,00,000-3,20,000/5

Average Profit of 5 years = 6,00,000/5

Average Profit of 5 years = Rs. 1,20,000

Goodwill of the Firm = Rs. 1,20,000 × 2

Goodwill of the Firm = Rs. 2,40,000

Calculation of Y’s share in Goodwill:-

Y’s Share in Goodwill = Rs. 2,40,000 × 2/5

Y’s Share in Goodwill = Rs. 96,000

X’s Contribution = Rs. 96,000 × 2/3 = Rs. 64,000

Z’s Contribution = Rs. 96,000 × 1/3 = Rs. 32,000

About Solution:-

On the death of a partner, the accounting treatment regarding goodwill, revaluation of assets and reassessment of liabilities, accumulated reserves and undistributed profit are similar to that of the retirement of a partner. On the death of partner the amount payable to him/her is paid to his/her legal representatives.

Things to Remember:

The legal representatives are entitled to the followings:

(a) The amount standing to the credit of the capital account of the deceased partner.

(b) Interest on capital, if provided in the partnership deed upto the date of death.

(c) Share of goodwill of the firm.

(d) Share of undistributed profit or reserves.

(e) Share of profit on the revaluation of assets and liabilities.

(f) Share of profit upto the date of death.

(g) Share of Joint Life Policy.

Important Notes:

The following amounts are debited to the account of the deceased partner’s legal representatives:

(i) Drawings

(ii) Interest on drawings

(iii) Share of loss on the revaluation of assets and liabilities;

(iv) Share of loss that has occurred till the date of his/her death.

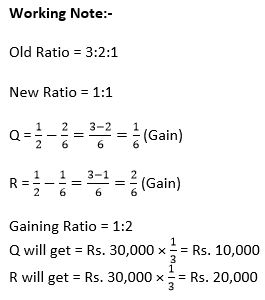

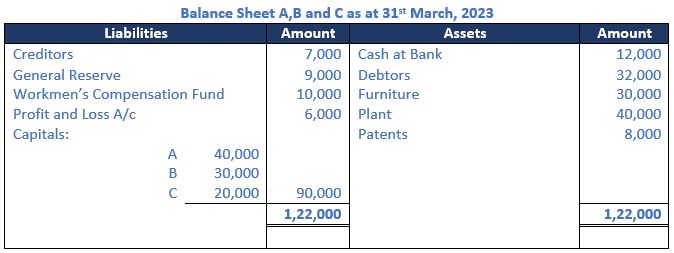

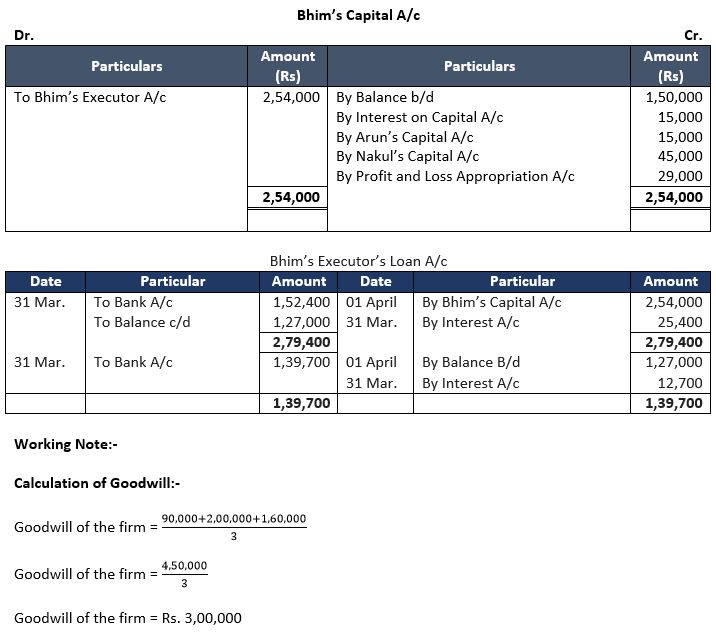

Question 33: Arun, Bhim and Nakul are partners in a firm sharing profits in the ratio of 1 : 1 : 3. Their Capital Accounts showed the following balances on 1st April, 2020:

Arun – ₹ 2,00,000; Bhim – ₹ 1,50,000 and Nakul – ₹ 4,50,000.

Firm closes its accounts every year on 31st March, Bhim died on 31st March, 2021. In the event of death of any partner, the Partnership Deed provides for the following:

(i) Interest on capital will be allowed to deceased partner only from the first of day of the accounting year till the date of his death @ 10% p.a.

(ii) The deceased partner’s share in the Goodwill of the firm will be calculated on the basis of 2 year’s purchase of the average profit of the last three years. The Profits of the firm for the last three years ended 31st March, were: 2019 – ₹ 90,000; 2020 – ₹ 2,00,000 and 2021 – ₹ 1,60,000.

(iii) His share of profits till the date of Death: The profit of the firm for the year ended 31st March, 2021 was ₹ 1,60,000 before providing for interest on capital. Bhim’s Executor was paid the sum due in two equal annual installments with interest @ 10% p.a.

Prepare Bhim’s Capital Account as on 31st March, 2021 to be presented to his executor and his Executor’s Loan Account for the year ending 31st March, 2022 and 31st March, 2023.

Answer 33:

Calculation of Partner’s Share in Goodwill:-

Bhim’s Share in Goodwill = Rs. 3,00,000 × 1/5 = Rs. 60,000

Gaining Ratio = 1:3

Arun’s Contribution = Rs. 60,000 × 1/4 = Rs. 15,000

Nakul’s Contribution = Rs. 60,000 × 3/4 = Rs. 45,000

Calculation of Bhim’s Share in Profit:-

Net Profit after Interest = Rs. 1,60,000 – Rs. 15,000

Net Profit after Interest = Rs. 1,45,000

Bhim’s Share in profit = Rs. 1,45,000 × 1/5

Bhim’s Share in profit = Rs. 29,000

About Solution:-

The Indian Partnership Act of 1932 states. Deceased partners are those who ended the relationship as a result of their passing. The passing of a partner does not void the partnership agreement; additionally, the inheritance of a deceased partner is not liable for any actions taken by the business after his passing.

Things to Remember:

When a partner retires, and in the event of a deceased partner, his possessions are passed to his legal enforcers and settled in a manner identical to the partner who is retiring.

Important Notes:

Accounting treatments at the time of Death of a Partner is an extension of the Retirement of a Partner. In the above-mentioned list, Salary, Interest on capital, Interest on Drawings etc. items is exactly the same both for retirement & death. There will be no effect of date of death.

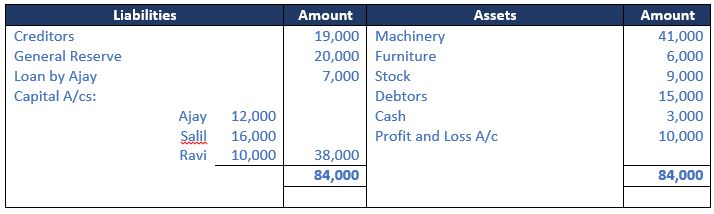

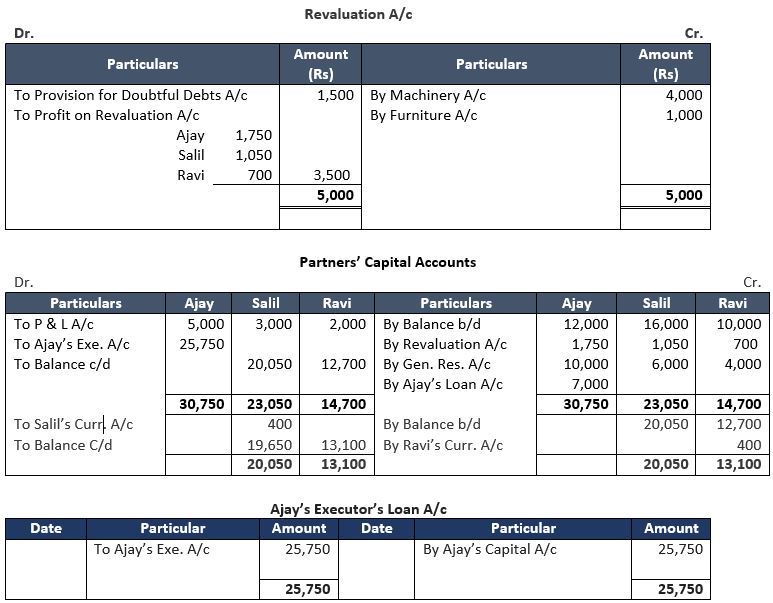

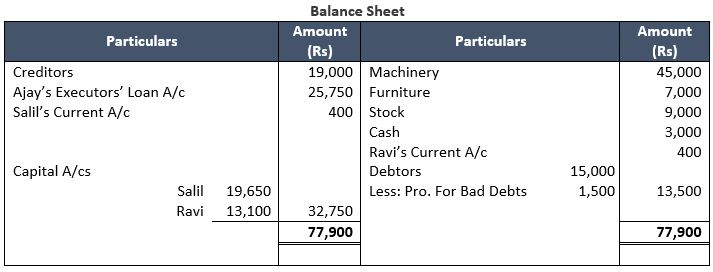

Question 34: Ajay, Salil and Ravi were partners in a firm sharing profits in the ratio of 5 : 3 : 2. Ajay died on 20th February 2023. The Balance Sheet of the firm on that date was as follows:

According to the Partnership Deed, on the death of a partner, the executor of the decreased partner will be entitled to:

(i) Balance in Capital Account.

(ii) His share in profit/loss on revaluation of assets and reassessment of liabilities which were as follows:

(a) Machinery is to be revalued at Rs. 45,000 and furniture at Rs. 7,000.

(b) A provision of 10% was to be created for Doubtful Debts.

(iii) The amount payable to Ajay was transferred to his Executors’ Loan Account which was to be paid later.

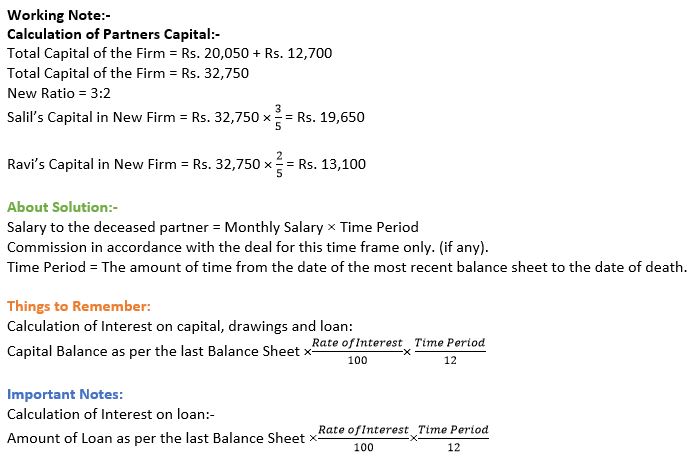

Prepare Revaluation Account, Partners’ Capital Accounts, Ajay’s Executors’ Account and the Balance Sheet of Salil and Ravi who decided to continue the business keeping their capital balance in their new profit sharing ratio. Any surplus or deficit was to be transferred to Current Accounts of the partners.

Answer 34:

Question 35: Ramesh, Suresh and Dinesh were partners sharing profits and losses in the ratio of 3:2:1. Dinesh died on 1st May, 2023 on which date the capitals of Ramesh, Suresh and Dinesh after all necessary adjustments stood at ₹ 1,20,000, ₹ 80,000 and ₹ 50,000 respectively. Ramesh and Suresh decide to carry on the business for 8 months without setling the account of Dinesh. During the period of 8 months ended 31st December 2022, profit of ₹ 40,000 is earned by the firm. State which of the two options available with Dinesh’s Executor under Section 37 of the Indian Partnership Act, 1932 should be exercised. Also calculate the total amount payable to Dinesh’s Executor if Ramesh and Suresh clear the dues of Dinesh on 31st December, 2023.

Answer 35:

Calculation of Dinesh’s Final Payment:-

Final Payment to Dinesh = Capital + Profit

Final Payment to Dinesh = Rs. 50,000 + Rs. 8,000

Final Payment to Dinesh = Rs. 58,000

Calculation of Dinesh’s Profit:-

(i) Interest on Balance Amount @ 6% = Rs. 50,000 × 6% × 8/12

Interest on Balance Amount @ 6% = Rs. 2,000

About Solution:-

The history of commercial partnerships dates back to the 14th century. The first partnership was started by a Florentine businessman named Francesco di Marco Datini. This new approach to company establishment altered the commercial landscape of Europe.

Things to Remember:

This system made it easier for individuals to combine their resources and start a business. Since the Middle Ages, partnerships have existed and been very successful. All administrations and governments have established the necessary rules and laws for the administration and taxation of such companies. Additionally, for the smooth operation of the company or group, each partnership creates its own set of rules.

Important Notes:

Any partner leaving the partnership signifies a major change for the organization he was a part of. It could be brought on by a number of things, from a change in the partner's interests to the death of any relationship. All the formal actions that must be done in these circumstances are specified in the partnership agreement. The deed stipulates that up until the passing of the particular partner, the legal representatives are entitled to a portion of the entity's profits. It can be written with the consent of all the surviving partners if such clauses are not present.

Old Questions

Question : Kumar, Verma and Naresh were partners in a firm sharing profits and Loss in the ratio of 3 : 2 : 2 . On 23rd January, 2015 Verma died. Verma's share of profit till the date of his death was calculated at Rs 2,350. Pass necessary journal entry for the same in the books of the firm.

Answer :

The Journal entry for transferring Verma’s share of profit to his capital account is given below

Answer :

Determination of Amount Payable to Executors of a Deceased Partner

Question : P, Q and R were partners in a firm sharing profits in 2 : 2 : 1 ratio. The Partnership Deed provided that on the death of a partner his executors will be entitled to the following:

(a) Interest on Capital @ 12% p.a.

(b) Interest on Drawings @ 18% p.a.

(c) Salary of Rs 12,000 p.a.

(d) Share in the profit of the firm( up to the date of death) on the basis of previous year's profit.

P died on 31st May, 2108. His capital was Rs 80,000. He had withdrawn Rs 15,000 and interest on his drawings was calculated as Rs 1,200. Profit of the firm for the previous year ended 31st March, 2018 was Rs 30,000.

Prepare P's Capital Account to be rendered to his executors

Answer :

Points of Knowledge:

(a) Interest on P’s Capital @12% p.a. till the date of death

= 80,000 × 12/100 × 2/12 = 1,600

(b) P’s share of profits till the death calculated on the basis of last year’s profits

= 30,000 × 2/12 × 2/5 = 2,000

(c) P’s salary = 12,000 × 2/12 = 2,000

Question : Vikas, Gagan and Momita were partners in a firm sharing profits in the ratio of 2 : 2 : 1 . The firm closes its books on 31st March every year. On 30th September, 2014 Momita died. According to the provisions of Partnership Deed the legal representatives of a deceased partner are entitled for the following in the event of his/her death:

(a) Capital as per the last Balance Sheet.

(b) Interest on capital at 6% per annum till the date of her death.

(c) Her share of profit to the date of death calculated on the basis of average profit of last four years.

(d) Her share of goodwill to be determined on the basis of three years' purchase of the average profit of last four years. The profits of last four years were;

![]() The balance in Momita's Capital Account on 13st March, 2014 was Rs. 60,000 and she had withdrawn Rs. 10,000 till date of her death. Interest on her drawings was Rs. 300. Prepare Momita's Capital Account to be presented to her executors.

The balance in Momita's Capital Account on 13st March, 2014 was Rs. 60,000 and she had withdrawn Rs. 10,000 till date of her death. Interest on her drawings was Rs. 300. Prepare Momita's Capital Account to be presented to her executors.

Answer :

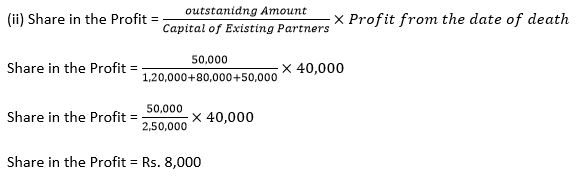

Question : A, B and C were partners in a firm sharing profits in the ratio of 5 : 3 ; 2 . On 31st March, 2017, their Balance Sheet was as follows:

A died-on 1st October, 2017. It was agreed among his executors and the remaining partners that:

(i) Goodwill to be valued at 212/212 years' purchase of the average profit of the previous 4 years , which were 2013-14: Rs 13,000; 2014-15: Rs 12,000; 2015-16: Rs 20,000 and 2016-17: Rs 15,000.

(ii) Patents be valued at Rs 8,000; Machinery at Rs 28,000; and Building at Rs 25,000.

(iii) Profits for the year 2017-18 be taken as having accrued at the same rate as that of the previous year .

(iv) Interest on capital be provided @ 10% p.a.

(v) Half of the amount due to A to be paid immediately to the executors and the balance transferred to his ( Executors) Loan Account.

Prepare A's Capital Account and A's Executors Account as on 1st October, 2017.

Answer :

Question : Virad, Vishad and Roma were partners in a firm sharing profits in the ratio of 5 : 3 : 2 respectively. On 31st March, 2103, their Balance Sheet was as under:

Virad died on 1st October, 2013. It was agreed between his executors and the remaining partners that:

(i) Goodwill of the firm be valued at 212/212 years purchase of average profits for the last three years. The average profits were Rs. 1,50,000.

(ii) Interest on capital be provided at 10% p.a.

(iii) Profits for the 2013-14 be taken as having accrued at the same rate as that of the previous year which was Rs.1,50,000.

Prepare Virad's Capital Account to be presented to his Executors as on 1st October, 2013.

Answer :

Question : Kavita, Leena and Monica are partners in firm sharing profits in the ratio of 1 : 1 : 3 respectively. Their Capital Accounts showed the following balances on 31st March, 2012: Kavita Rs 70,000; Leena Rs 65,000 and Monica Rs 2,10,000. Firm closes its accounts every year on 31st March. Kavita died on 30th September, 2012. In the event of death of any partner, the Partnership Deed provides for the following :

(a) Interest on capital will be calculated at the rate of 6% p.a.

(b) The deceased partner's share in the goodwill of the firm will be calculated on the basis of 2 years' purchase of the average profit of last three years. The profits of the firms for the last three years were Rs 90,000; Rs 1,00,000 and Rs 1,10,000 respectively.

(c) Her share in the Reserve Fund of the firm will be paid. The Reserve Fund of the firm was Rs 60,000 at the time of Kavita's death.

(d) Her share of profit till the date of death will be calculated on the basis of sales. It is also specified that the sales during the year 2011-12 were Rs 20,00,000. The sales from 1st April, 2012 to 30th September, 2012 were Rs 4,00,000. The profit of the firm for the year ending 31st March, 2012 was Rs 2,00,000.

Prepare Kavita's Capital Account to be presented to his legal representative.

Answer :

Points of Knowledge :

Note 1 : Calculation of New Ratio and Gaining Ratio

Question : A, B and C are partners in a firm sharing profits in the proportion of 3 : 2 : 1 . Their Balance Sheet as at 31st March, 2018 stood as follows:

B died on 30th June , 2018 and according to the deed of the said partnership his executors are entitled to be paid as under:

(a) The capital to his credit at the time of his death and interest thereon @ 10% per annum.

(b) His proportionate share of General Reserve.

(c) His share of profits for the intervening period will be based on the sales during that period. Sales from 1st April, 2018 to 30th June, 2018 were as Rs 12,00,000. The rate of profit during past three years had been 10% on sales.

(d) Goodwill according to his share of profit to be calculated by taking twice the amount of profits of the last three years less 20%. The profit of the previous three years were: 1st Year: Rs. 82,000; 2nd year: Rs 90,000; 3rd year Rs 98,000.

(e) The investments were sold at par and his executors were paid out in full.

Prepare B's Capital Account and his Executors' Account.

Answer :

Question : Babita, Chetan and David are partners in a firm sharing profits in the ratio of 2 : 1 : 1 respectively. Firm closes its accounts on 31st March every year. Chetan died on 30th September, 2012. There was a balance of Rs 1,25,000 in Chetan's Capital Account in the beginning of the year. In the event of Death of any partner, the Partnership Deed provides for the following:

(a) Interest on capital will be calculated at the rate of 6% p.a.

(b) The executor of deceased partner shall be paid Rs 24,000 for his share of goodwill.

(c) His share of Reserve Fund of Rs 12,000, shall be paid to his executor.

(d) His share of profit till the date of death will be calculated on the basis of sales. It is also specified that the sales during the year 2011-12 were Rs 4,00,000. The sales from 1st April, 2012 to 30th September, 2012 were Rs 1,20,000. The profit of the firm for the year ending 31st March, 2012 was Rs 2,00,000. Prepare Chetan's Capital Account to be presented to his executor.

Answer :

Question : Sunny, Honey and Rupesh were partners in a firm. On 31st March, 2014, their Balance Sheet was as follows:

Honey died on 31st December, 2014. The Partnership Deed provided that the representative of the deceased partner shall be entitled to :

(a) Balance in the Capital Account of the deceased partner.

(b) Interest on Capital @ 6% per annum up to the date of his death.

(c) His share in the undistributed profits or losses as per the Balance Sheet.

(d) His share in the profits of the firm till the date of his death , calculated on the basis of rate of net profit on sales of the previous yea . The rate of net profit on sales of previous year was 20%. Sales of the firm during the year till 31st December, 2014 was Rs 6,00,000.

Prepare Honey's Capital Account to be presented to his executors.

Answer :

Points of Knowledge:

Note1: Calculation of New Ratio

Old Ratio of Sunny: Honey: Rupesh = 1: 1: 1

New Ratio of Sunny: Rupesh = 1:1

Note2: Calculation of Profit to be given to the dead partner’s Representatives:

Honey’s share of profit = Sales during the Period × % of Normal Profit × Honey’s Profit Share

= 6, 00,000 × 20/100 × 1/3 = 40,000

Question : R, S and T were partners sharing profits and losses in the ratio of 5 : 3 : 2 respectively. On 31st March, 2018, Their Balance Sheet stood as:

T died on 1st August , 2018 . It was agreed that:

(a) Goodwill be valued at 212/212 years' purchase of average of last 4 years' profits which were:

2014-15: Rs 60,000; 2016-17: Rs 80,000 and 2017-18: Rs 75,000.

(b) Machinery be valued at Rs 1,40,000; Patents be valued at Rs 40,000; Leasehold be valued at Rs 1,25,000 on 1st August, 2018..

(c) For the purpose of calculating T's share in the profits of 2018-19, the profits in 2018-19 should be taken to have accrued on the same scale as in 2017-18.

(d) A sum of Rs 21,000 to be paid immediately to the Executors of T and the balance to be paid in four equal half-yearly instalments together with interest @ 10% p.a.

Pass necessary journal entries to record the above transactions and T's Executors ' Account .

Answer :

Question : Akhil, Nikhil and Sunil were partners sharing profits and losses equally. Following was their Balance Sheet as at 31st March, 2018:

Sunil died on 1st August, 2018. The Partnership Deed provided that the executor of a deceased partner was entitled to :

(a) Balance of Partners' Capital Account and his share of accumulated reserve.

(b) Share of profits from the closure of the last accounting year till the date of death on the basis of the profit of the preceding completed year before death.

(c) Share of goodwill calculated on the basis of three times the average profit of the last four years.

(d) Interest on deceased partner's capital @ 6% p.a.

(e) Rs 50,000 to be paid to deceased's executor immediately and the balance to remain in his Loan Account.

Profits and Losses for the preceding years were: 2014-15——Rs 80,000 Profit; 2015-16——Rs 1,00,000 Loss; 2016-17——Rs 1,20,000 Profit; 2017-18——Rs 1,80,000 Profit.

Pass necessary journal entries and prepare Sunil's Capital Account and Sunil's Executor Account .

Answer :

Question : B, C and D were partners in a firm sharing profits in the ratio of 5 :3 : 2 . On 31st December, 2008, their Balance Sheet was as follows:

B died on 31st March, 2009. The Partnership Deed provided for the following on the death of a partner:

(a) Goodwill of the firm was to be valued at 3 years' purchase of the average profit of last 5 years. The profits for the years ended 31st December, 2007, 31st December 2006, 31st December 2005, and 31st December 2004 were Rs 70,000 ; Rs 60,000 and Rs 40,000 respectively.

(b) B's share of profit and loss till the date of his death was to be calculated on the basis of the profit and loss for the year ended 31st December, 2008.

You are required to calculate the following :

(i) Goodwill of the firm and B's share of goodwill at the time of his death.

(ii) B's share in the profit or loss of the firm till the date of his death .

(iii) Prepare B's Capital Account at the time of his death to be presented to his Executors .

Answer :

Question : The Balance Sheet of X, Y and Z as at 31st March, 2018 was:

The profit-sharing ratio was 3 : 2 : 1 . Z died on 31st July, 2018 . The Partnership Deed provides that:

(a) Goodwill is to be calculated on the basis of three years' purchase of the five years' average profit. The profits were: 2017-18: Rs 24,000; 2016-15: Rs 20,000; 2014-15: Rs 10,000 and 2013-14: Rs 5,000.

(b) The deceased partner to be given share of profits till the date of death on the basis of profits for the previous year.

(c) The Assets have been revalued as: Stock Rs. 10,000; Debtors Rs 15,000; Furniture Rs 1,500; Plant and Machinery Rs 5,000; Building Rs 35,000. A Bill Receivable for Rs 600 was found worthless.

(d) A Sum of Rs 12,233 was paid immediately to Z's Executors and the balance to be paid in two equal annual instalments together with interest@ 10% p.a. on the amount outstanding .

Give journal entries and show the Z's Executors' Account till it is finally settled .

Answer :

Points of Knowledge :

Note 1: Calculation of New Ratio and Gaining Ratio

Question : X, Y and Z were partners in a firm sharing profits and losses in the 5 ; 4 : 3 . Their Balance Sheet on 31st March, 2018 was as follows:

X died on 1st October, 2018 and Y and Z decide to share future profits in the ratio of 7 : 5 . It was agreed between his executors and the remaining partners that :

(i) Goodwill of the firm be valued at 212/212 years' purchase of average of four completed years' profit which were:

(ii) X's share of profit from the closure of last accounting year till date of death be calculated on the basis of last years' profit.

(iii) Building undervalued by Rs 2,00,000; Machinery overvalued by Rs 1,50,000 and Furniture overvalued by Rs 46,000.

(iv) A provision of 5% be created on Debtors for Doubtful Debts.

(v) Interest on Capital be provided at 10% p.a.

(vi) Half of the net amount payable to X's executor was paid immediately and the balance was transferred to his loan account which was to be paid later.

Prepare Revaluation Account , X's Capital Account and X's Executors Account as on 1st October, 2018.

Answer :

Question : X, Y and Z were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1 . Z died on 30th June, 2018. The Balance Sheet of the firm as at that 31st March, 2018 is as follows:

The following decisions were taken by the remaining partners:

(a) A Provision for Doubtful Debts is to be raised at 5% on Debtors .

(b) While Machinery to be decreased by 10% , Furniture and Stock are to be appreciated by 5% and 10% respectively.

(c) Advertising Expenses Rs 4,200 are to be carried forward to the next accounting year and , therefore , it is to be adjusted through the Revaluation Account .

(d) Goodwill of the firm is valued at Rs 60,000.

(e) X and Y are to share profits and losses equally in future.

(f) Profit for the year ended 31st March, 2018 was Rs 16,000 and Z's share of profit till the date of death is to be determined on the basis of profit for the year ended 31st March, 2018.

(g) The Fixed Capital Method is to be converted into the Fluctuating Capital Method by transferring the Current Account balances to the respective Partners' Capital Accounts.

Prepare the Revaluation Account, Partners' Capital Accounts and prepare C's Executors’ Account to show that C's Executors were paid in two half-yearly instalments plus interest of 10% p.a. on the unpaid balance. The first instalments were paid on 31st December, 2018.

Answer :

Question : X, Y and Z are partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2 . Their Balance Sheet as at 31st March, 2018 was as follows:

Z died on 1st April, 2018, X and Y decide to share future profits and losses in ratio of 3 : 5 . It was agreed that:

(i) Goodwill of the firm be valued 212/212 years' purchase of average of four completed years' profits which were: 2014-15——Rs 1,00,000; 2015-16——Rs 80,000; 2016-17——Rs 82,000.

(ii) Stock undervalued by Rs 14,000 and machinery overvalued by Rs 13,600.

(iii) All debtors are good. A debtor whose dues of Rs 400 were written off as bad debts paid 50% in full settlement.

(iv) Out of the amount of insurance premium which was debited entirely to Profit and Loss Account, Rs 2,200 be carried forward as an unexpired insurance premium.

(v) Rs 1,000 included in Sundry Creditors is not likely to arise.

(vi) A claim of Rs 1,000 on account of Workmen Compensation to be provided for.

(vii) Investment be sold for Rs 8,200 and a sum of Rs 11,200 be paid to execution of Z immediately. The balance to be paid in four equal half-yearly instalments together with interest @ 8% p.a. at half year rest.

Show Revaluation Account, Capital Accounts of Partners and the Balance Sheet of the new firm.

Answer :