Access free TS Grewal Solution Class 12 Chapter 2 Accounting for Partnership Firms Fundamentals 2026 below. Students can now access free TS Grewal Solutions for Class 12 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 12 Math Chapter 2 Accounting for Partnership Firms Fundamentals TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 2 Accounting for Partnership Firms Fundamentals Class 12 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 2 Accounting for Partnership Firms Fundamentals TS Grewal Class 12 Solved Exercises

About this chapter: TS Grewal Class 12 Chapter 2 Accounting for Partnership Firms – Fundamentals is a very important topic for commerce students in Class 12 studying accountancy. This chapter provides details and covers all the fundamental concepts and principles that are essential to get an understanding relating to accounting for partnership firms. TS Grewal has provided topics such as introduction to partnership firms, definition, features and types of partnerships. The concepts relating to the process of creating a partnership firm, the importance of partnership deeds, agreements, and registration has also been provided in the chapter. It also includes details relating to fixed and fluctuating capital methods. Students should also understand concepts relating to the distribution of profits and losses amongst partners. There are many other important topics that have been explained in detail including the preparation of Profit and Loss Appropriation Account, distribution of profits among partners.

Apart from concepts, there are lot of solved and unsolved questions given in each chapter. Our Accountancy teachers have provided detailed solutions which will help the students. The following can be used as a comprehensive guide to accounting for partnership firms.

Answer:

Below are the rights of partners:-

Answer:

Partnership Deed is an important legal document which defines relationship among the partners. It is important to have written Partnership Deed to avoid and settle possible dispute.

Question 12. X and Y are partners. Y wants to admit his son K into business. Can K become the partner of the firm? Give reason.

K, cannot become the partner of the firm.

Reason: As per Section 31(1) of the Indian Partnership Act, 1932, a person can be admitted as a new partner only with the consent of all the existing partners unless otherwise agreed upon.

Question 13. Pratibha, partner of a firm, has advanced loan to the firm of 1,00,000. The firm does not have a Partnership Deed. Will Pratibha get interest on the loan? If yes, at which rate and why?

Yes, Pratibha get the interest on loan by 6%. In the absence of partnership deed, interest rate would be 6% p.a. This interest on loan would be paid because it is a charge against profits.

Question 14. Neha, a partner, owns a building in which the firm carries its business. The firm pays her 10,000 as rent of the building. To which account rent will be debited?

Yes, Rent is paid to Neha is to be debited to profit and loss account because it is paid against the profit.

Question 15. What is meant by 'Fixed Capital of a Partner?

‘Fixed Capital’ of a partner means that the capital remains unchanged unless additional capital is introduced or withdrawal is made from the existing capital.

Question 16. What is meant by 'Fluctuating Capital of a Partner?

It is a method of maintaining Capital Accounts of partners under which all transactions related to a partner (such as his share of profit/loss, drawings, interest on capital or drawings, salary, etc.) are recorded in his Capital Account.

Question 17. Distinguish between 'Fixed Capital Account' and 'Fluctuating Capital Account' on the basis of credit balance.

Fixed Capital Account always shows a credit (positive) balance, while Fluctuating Capital Account may show debit (negative) or credit (positive) balance.

Question 18. A firm maintains a Capital Account and a Current Account for each partner. What is the term used when this method of maintaining Capital Accounts is followed?

If a firm maintains a Capita Account and a Current Account this approach is called Fixed Capital Account Method.

Question 19. Give two items which may appear on the debit side of a Partner's Current Account

Current Account of each partner is debited with:-

- Drawings by a partner against profit

- Interest on drawings

Question 20. State the two methods of maintaining Capital Accounts of partners.

Two methods of maintaining Capital Account of Partners:-

- Fixed Capital Account Method

- Fluctuating Capital Accounts Method

Question 21. If interest on capital, salary to the partner and share of profit are credited while interest on drawings, drawings and share of loss are debited to the Partners' Capital Accounts, what is the method followed to maintain the Capital Accounts?

Fluctuating Capital Accounts Method is maintain, If interest on capital, salary to the partner and share of profit are credited while interest on drawings, drawings and share of loss are debited to the Partners' Capital Accounts.

Question 22. Interest on capital is credited to Partner's Current Account. Name the method of maintaining Capital Account.

Fixed Capital Accounts Method used if Interest on capital is credited to Partner’s Current Account.

Question 23. Under which Capital Account Method, Current Accounts of partners are maintained?

Fixed Capital Accounts Method, Current Accounts of partners are maintained.

Question 24. Under which Capital Account Method, Current Accounts of partners are not maintained?

Fluctuating Capital Accounts Method, Current Accounts of partners are not maintained.

Question 25. Give four items that may appear on the credit side of the Partner's Current Account.

Current Account of each partner is credited with:-

- Interest on Capital

- Salary or Commission

- Share of profit

- Transfer of any amount from Capital Account permanently.

Question 26. Give three items that may appear on the debit side of the Partner's Current Account.

Current Account of each partner is debited with:-

- Drawings by a partner against profit

- Interest on drawings

- Share of loss.

Question 27. M/S RSA maintains Partners' Capital Accounts under Fixed Capital Accounts Method. Accountant of the firm has credited their salary and interest on capital to their Capital Accounts. Do you agree with the treatment? Give reasons for your answer.

No, we don’t agree with the treatment as salary and interest on capital are to be credited to the partner’s current account under fixed capital account method.

Question 28. Give two circumstances in which the Fixed Capitals of partners may change.

Two circumstances in which the Fixed Capitals of partners may change:

- When Additional Capital is introduced.

- When a part of capital is permanently withdrawn.

Question 29. List the item that may appear on the debit side of a Partner's Fixed Capital Account.

Below items may appear on the debit side of a Partner’s Fixed Capital Account:-

- Cash (Permanent capital withdrawn)

- Balance c/d

Question 30. ABC, a partnership firm, does not have a Partnership Deed. The firm wants to pay remuneration to the partners. How can it do so?

In absence of partnership deed, partners are not allowed get remuneration so, ABC cannot pay remuneration.

Question 31. If the Partnership Deed does not specify the profit-sharing ratio, in what ratio is the profit or loss shared by the partners?

If the Partnership Deed does not specify the profit-sharing ratio, the partners will equally distribute the profit or loss.

Question 32. What share of profit would a sleeping partner who has contributed 75% of the total capital get in the absence of a deed?

In the absence of Partnership deed, if nothing is fixed about sharing of profits and losses by the partners in the deed, then partners share profits and losses in an equal ratio.

So, in this case, even if the sleeping partner has contributed 75% of the total capital of the firm, the provisions of Partnership deed implies distribution of profits and losses will be shared by all the partners equally.

Question 33. If the Partnership Deed does not specify the rate of interest payable on loan by a partner, at what rate will the interest be paid? If not, why?

Interest on loan will be payable @ 6%.

Reason:- In the absence of Partnership Deed, the provision of the Indian Partnership Act, 1932 will apply. It provides that interest @ 6% p.a. will be paid on partner’s loan, in the absence of Partnership Deed.

Question 34. State the provisions of Indian Partnership Act regarding the payment of remuneration to a partner for the services rendered.

As per the Provision of Indian Partnership Act, 1930, in the absence of Partnership Deed, no remuneration is to be provided to a partner.

Question 35. If the Partnership Deed does not specify the rate of interest chargeable on drawings, will the interest still be charged? If yes, at what rate? If not, why?

No, there is no interest chargeable on drawings.

Reason:- In the absence of Partnership Deed there is no provision to provide interest on drawings to partner’s.

Question 36. State the provisions of Partnership Act, 1932, in the absence of a Partnership Deed regarding (i) Interest on Partner's Drawings, and (ii) Interest on Advances other than capital.

(i) Interest on Partner's Drawings:- In the absence of Partnership Deed there is no provision to provide Interest on Partner’s Drawings in Partnership Act, 1932.

(ii) Interest on Advances other than capital:- Advance other than capital are treated as Loan to the firm. In the absence of Partnership deed, according to Partnership Act of 1932, the partners are entitled for 6% p.a. interest on loan forwarded by them to the firm.

Question 37. Can a partner be exempted from sharing losses in a firm? If yes, under what circumstances?

Yes, a partner may be exempted from bearing losses in a Partnership Firm. If a partner is admitted for the benefits of partnership, in such cases, minors are entitled to share only profit of the firm.

Question 38. A and B are partners in a firm without a Partnership Deed. A is an active partner and claims a salary of 18,000 per month. State with reason whether the claim is valid or not.

A’s Claim is invalid because there is no partnership deed and in the absence of partnership deed no partner can claim any salary.

Question 39. Somesh and Ramesh are partners in a firm with capitals of 3,00,000 and 4,00,000 respectively. They do not have a Partnership Deed. Ramesh wants to share the profits in the ratio of capitals. State with reasons whether the claim is valid.

Ramesh’s Claim is invalid because there is no partnership deed and in the absence of partnership deed profit and loss will be shared equally.

Question 40. Chander and Suman are partners in a firm without a Partnership Deed. Chander's capital is Rs. 10,000 and Suman's capital is Rs. 14,000. Chander has advanced a loan of 5,000 and claims interest @ 12% p.a. on it. State with reasons whether his claim is valid or not.

Chander’s Claim is Invalid because in the absence of a Partnership Deed, a partner is entitled to receive interest on loan and advances provided to the firm at the rate of 6% p.a.

Question 41. State the provisions of Indian Partnership Act, 1932 regarding interest on partner's capital and interest on partner's loan when there is no Partnership Deed.

(1) Interest on partner's capital:- According to provisions of Indian Partnership Act, 1932 interest on capital is not paid to partners.

(2) Interest on partner's Loan:- According to provisions of Indian Partnership Act, 1932 Interest on loan is paid @ 6% p.a. Interest on partner’s loan is charge against profit. It means interest is payable even if there is a loss.

Question 42. What is Profit and Loss Appropriation Account?

A partnership firm, like a proprietorship firm prepares Trading Account, Profit and Loss Account and Balance Sheet. In addition, a partnership firm prepares Profit and Loss Appropriation Account to which net profit or net loss as per the Profit and Loss Account is transferred to show its appropriation.

Question 43. List the items that are debited to profit and Loss Appropriation Account.

Below are the item’s which is debited into profit and loss appropriation account:-

- Net Loss transferred from Profit and Loss Account.

- Interest on Capital

- Partner’s Salaries

- Partner’s Commission

- Reserve

Question 44. List the items that are credited to Profit and Loss Appropriation Account.

Below are the item’s which is credited into profit and loss appropriation account:-

- Net Profit transferred from Profit and Loss Accounts

- Interest on Drawings

Question 45. To which account salary, commission to partners and interest on capital be debited? Why?

Salary, Commission to partners and interest on capital to be debited in Profit and Loss Appropriation Account because these are the loss for the firm and income for the partners.

Question 46. Under what circumstances Average Method of calculating interest on drawings is applied?

Average Method is used when drawings are on regular basis or when:

(a) The amount of drawings is uniform

(b) The time interval between the two drawings is also uniform.

Question 47. If a fixed amount is withdrawn on 15th day of every month of a calendar year, for what period will the interest on total amount withdrawn be calculated?

A fixed amount is withdrawn on 15th day of every month; interest would be calculated by Average Period Method. Total amount withdraw will be calculated for an average period of 6 month.

Question 48. If A draws 15,000 every month at the end of the month, what will be the interest @ 5% p.a.?

Calculation of Interest on Drawings:-

Question 49. How is interest on drawings calculated, if the drawings are made at regular intervals, as on the 15th day each month?

Calculation of Interest on Drawings:-

Question 50. How will you calculate interest on the drawings of equal amount made on the last day of every month a calendar year?

If a partner withdraws fixed amount at the end of every month, interest is charged for 5.5 months on the total amount.

Question 51. Explain briefly the meaning of guarantee of minimum profit.

A new partner may be admitted in the firm with minimum guaranteed profit from the business. The profit may be guaranteed to an existing or incoming partner by:

(a) All the remaining partners in an agreed ratio

(b) One or more f the existing or old partners.

When the guaranteed partner’s or new partner’s share of profit is more than guaranteed amount, his actual share of profit is given to him instead of the guaranteed amount of profit.

Question 52. State one difference between Fixed Capital Account and Fluctuating Capital Account of partners.

Fixed Capital Account cannot have a debit balance but Fluctuating Capital Account can have a debit balance.

Question 53. Why is it that the Capital Account of a partner does not show a Debit Balance' in spite of regular and consistent losses year after year?

The Capital Account of a partner shows a debit balance when partner withdraws amount from his Capital or he leave from the partnership.

It does not show debit balances in spite of regular and consistent losses year after year because these losses are first applied to the company’s assets or are recorded as part of a company's liability.

Question 54. A Partnership Deed provides for the payment of interest on capital but there was a loss instead of profit during the year 2010-11. At what rates will the interest on capital be allowed?

In case of Loss, there is no interest on Capital allowed to partner. Interest on capital is allowed only when there is any profit.

Question 55. What is meant by 'unlimited liability of a partner'?

Unlimited liability means that the liability of a partner is joint and several. The personal assets of the partner can be utilised for paying a firm’s debts.

Question 56. When the partners' capitals are fixed, where will the drawings made by a partner be recorded?

When the partner’s capital is fixed, drawings made by a partner will be debited to the Partner’s Current Account.

Question 57. If the partners' capitals are fixed, where will you record interest charged on drawings?

When the partner’s capital is fixed, interest charge on drawings will be credited to the Partner’s Current Account.

Question 58. Name the method of calculating Interest on Drawings of the partner if different amounts are withdrawn on different dates.

When drawings are made in unequal amount at different dates, interest on drawings is calculated by Product Method.

Short Answer Type Questions

Question 1. Mention the items that may appear on the credit side of the Capital Account of a Partner when the capitals are fluctuating.

List of the items that appear on the Credit side of the Capital account:-

- Credit opening balance

- Additional Capital

- Interest on Capital

- Commission

- Partners Salary

- Profit

Question 2. Mention the items that may appear on the debit side of the Capital Account of a Partner when the capitals are fluctuating.

List of the items that appear on the Debit side of the Capital account:-

- Debit Opening Balance

- Drawings against Capital

- Drawings against Profit

- Interest on Drawings

- Loss

Question 3. List any four items appearing on the Profit and Loss Appropriation Account.

List of the items that appear in Profit and Loss Appropriation account at debit side:-

- Net Loss Transferred from Profit and Loss Account

- Interest on Capital

- Partner’s Salaries

- Partner’s Commission

Question 4. State any four features of a Partnership.

The essential characteristics of partnership are:

1. Two or More Persons:- There must be at least two persons to form a partnership and all such persons must be competent to contract. According to Indian Contract Act, 1872 every person except the following is competent to contract:

(a) Minor (b) Persons of unsound mind (c) Persons disqualified by any law.

Section 464 of the Companies Act, 2013 empowers the Central Government to prescribe maximum number of partners in a firm but the number of partners so prescribed cannot be more than 100. The Central Government has prescribed maximum number of partners in a firm to be 50 vide Rule 10 of the Companies (Miscellaneous) Rules, 2014. Thus, in effect, a partnership firm cannot have more than 50 members.

2. Agreement:- Partnership comes into existence by an agreement, either written or oral. The agreement among the partners is the basis of their relationship which may be for a particular venture, for a period or at will. The written agreement among the partners is known as Partnership Deed.

3. Lawful Business:- A partnership is formed to do a lawful business. Business includes trade, vocation and profession. A joint ownership or charitable activity (such as running of a charitable clinic) is not business as it does not function with the objective of earning profit. Therefore, Partnership Deed is not drawn.

4. Profit-sharing:- The agreement between/among the partners must be to share profits or losses of the business. It is not essential that all the partners must share losses also. There may be a provision in the Partnership Deed that a particular partner or partners shall not bear the losses.

Question 5. List any four contents of a Partnership Deed.

It is a legal document signed by all the partners and has clause on the following:

(i) Description of the Partners:- Names, description and addresses of the partners.

(ii) Description of the Firm:- Name and address of the firm.

(iii) Principal Place of Business:- Address of the principal place of business.

(iv) Nature of Business:- Nature of business that the firm shall carry on.

Question 6. Discuss the main provisions of the Indian Partnership Act, 1932 that are relevant to partnership accounts if there is no Partnership Deed.

Below are the Important Provisions of the Indian Partnership Act, 1932:-

(i) If all the partners agree, a minor may be admitted for the benefit of partnership.

(ii) A person may be admitted as a partner either with the consent of all the existing partners or in accordance with an express agreement among the partners.

(iii) A partner may retire from the firm either with the consent of all the other partners or in accordance with an express agreement among the partners.

(iv) Registration of the firm is optional and not compulsory.

(v) Unless otherwise agreed by the partners in the Partnership Deed, a firm is dissolved on the death of a partner.

Question 7. Distinguish between Fixed and Fluctuating Capitals.

Question 8. State the two situations in which interest on Partners' Capital is generally provided.

Below are the situations in which interest on Partner’s capital is allowed:-

- When there is a provision in partnership deed about interest on partner’s capital.

- When credit balance in the Partner’s Capital Account.

EXERCISE ::---->

Partnership Deed

Question 1: In the absence of Partnership Deed, what are the rules relation to :

(a) Salaries of partners.

(b) Interest on partner’s capitals.

(c) Interest on partner’s loan.

(d) Division of profit.

(e) Interest on partner’s drawings.

(f) Interest on Loan to partner’s

a) Salaries of Partners – No Salary are Payable to any partner.

b) Interest on Partners Capital – No interest on capital is allowed or paid to any partner.

c) Interest on Partners Loan – Interest on Partner’s Loan is allowed @ 6% to the partners.

d) Division of Profit – Profit are divided equally.

e) Interest on Partner’s drawings – No interest on Partner’s drawings is charged from the Partners.

f) Interest on Loan to partners – No interest on Loan’s drawings is charged from the Partners.

Point of Knowledge:-

Some Rights of Partners:-

1. Every partner has the right to participate in the management of the business.

2. Every partner has the right to be consulted about the affairs of the business.

3. Every partner has the right to inspect the books of accounts and have a copy of it.

4. Every partner has the right to share profit or losses with others in the agreed ratio.

Question 2: Mahesh, Ramesh, and Suresh are partners in a firm. They do not have a Partnership Deed. At the end of the first year of the Business, they faced the following problems:

a) Mahesh wants that interest on capital should be allowed to the partners but Ramesh and Suresh do not agree.

b) Ramesh wants that the partners should be allowed to draw salaries but Mahesh and Suresh do not agree.

c) Mahesh and Ramesh want that Suresh should pay interest on the loan given to him by the firm but Suresh does not agree.

d) Mahesh and Ramesh having contributed larger amounts of capital, desire that the profits should be distributed in the ratio of their capital contribution but Suresh does not agree.

State how will these disputes be settled.

Answer:

a) In the absence of a partnership deed. Provisions of the Indian Partnership Act 1932 would apply. No interest on the partner’s capital would be allowed. Ramesh and Suresh both are correct.

b) In the absence of a partnership deed. Provisions of the Indian Partnership Act 1932 would apply. No salary would be allowed to partners. Mahesh and Suresh are correct.

c) In the absence of a partnership deed. Provisions of the Indian Partnership Act 1932 would apply. No interest on a loan to a partner by the firm is charged. Mahesh and Ramesh are incorrect

d) In the absence of a partnership deed. Provisions of the Indian partnership Act 1932 would apply. The Profit-Sharing ratio would be equal (1:1:1). Mahesh and Suresh are incorrect.

Question 3: Following difference has arisen among P, Q, and R. State who is correct in each case:

a) P used ₹ 50,000 belonging to the firm and earned a profit of ₹ 5000. Q and R want the amount to be given to the firm.

b) Q used ₹ 10,000 belonging to the firm and incurred a loss of ₹ 1,000. He wants the firm to bear the loss.

c) P and Q want to purchase goods from Star Ltd. R does not agree.

d) Q and R want to admit W as a partner, but P does not agree.

e) R had given a loan of ₹ 2,00,000 to the firm and demanded interest @ 10%. P and Q do not want to pay the interest.

Answer:

a) If any partner uses the money of the firm and earned a profit. He has to pay back the used money with profit. Hence, p has to back ₹ 55,000 to the firm.

b) If any partner uses the firm money and incurred a loss. He has to bear the loss and the full amount of money taken by the partner has to return back the firm. Hence Q has to pay ₹ 10,000 to the firm.

c) Any business decision is decided by the majority. Hence P and Q want to purchase goods from star Ltd is accepted as there are only 3 partners and the majority.

d) W as a partner cannot be admitted as to admit a new partner, all partners must agree.

e) In the absence of a partnership deed. Provisions of the Indian Partnership Act 1932 would apply. Only a 6% p.a. rate of interest on the loan of partners to the firm would be charged. Hence, In the place of 10% p.a., only a 6% p.a. rate of interest would be charged.

Question 4: Barun, Tarun, and Shivam are partners in a firm and do not have a partnership Deed. Barun introduced further capital of ₹ 5,00,000 on 1st October 2022. Whereas Shivam took a loan of ₹ 50,000 from the firm on 1st October 2022. Disputes have arisen among them on the following:

a) Barun demands interest @ 10% p.a. on ₹ 5,00,000 being his extra capital.

b) Tarun desires that his son Deep should be admitted as a partner and he will give him half of his share. Barun and Shivam do not agree.

c) Barun and Tarun are of the view that Shivam should be charged interest on loans from the firm at the lending rate of the banks, which is 12% p.a.

d) Tarun has withdrawn ₹ 50,000 from the firm for his personal use. Barun and Shivam are of the view that Tarun should be charged interest @ 10% p.a.

Give a Solution to each issue of dispute.

Answer:

a) In the case of the absence of a Partnership deed. Provisions of the Indian Partnership Act 1932 would apply. No interest on capital would be allowed.

b) In the case of the absence of a partnership deed. Provisions of the Indian Partnership Act 1932 would apply. Tarun’s son Deep would not be admitted. As all partners do not agree.

c) In the case of the absence of a Partnership deed. Provisions of the Indian Partnership Act 1932 would apply. No interest on a loan to Shivam from the firm is charged

d) In the case of the absence of a partnership deed. Provisions of the Indian Partnership Act 1932 would apply. No interest on drawing would be charged.

Point of Knowledge:-

In the absence of Partnership deed Profit will be equally divided between partners.

Question 5: Harshad and Dhiman are in partnership since 1st April, 2023. No partnership agreement was made. They contributed Rs. 4,00,000 and 1,00,000 respectively as capital. In addition, Harshad advance an amount of Rs. 1,00,000 to the firm on 1st October, 2023. Due to long illness, Harshad could not participate in business activities from 1st August to 30th September, 2023. The profit for the year ended 31st March, 2024 amounted to Rs 1,80,000. Dispute has arisen between Harshad and Dhiman.

Harshad Claims:

(i) He should be given interest @ 10% per annum on capital and loan;

(ii) Profit should be distributed in proportion of capital;

Dhiman Claims:

(i) Profit should be distributed equally;

(ii) He should be allowed Rs. 2,000 p.m. as remuneration for the period he managed the business in the absence of Harshad;

(iii) Interest on Capital and loan should be allowed @ 6% p.a.

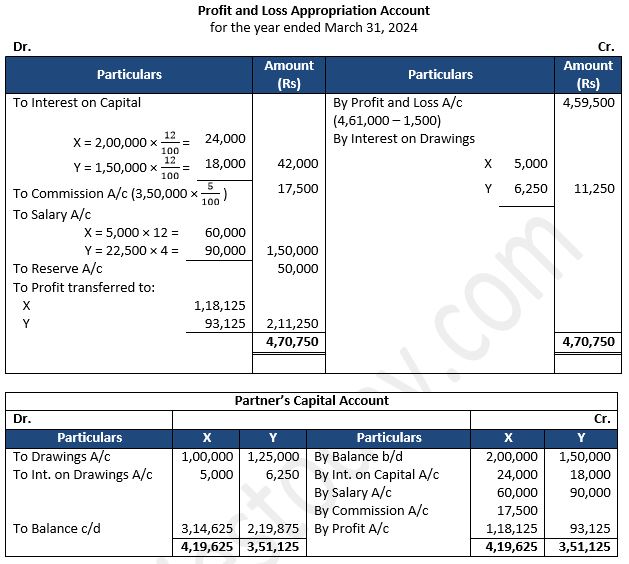

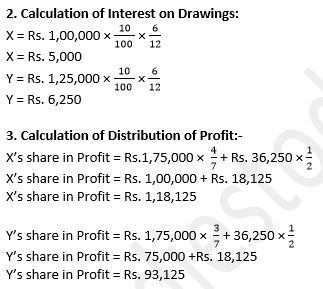

You are required to settle the dispute between Harshand and Dhiman. Also prepare Profit and Loss Appropriation Account.

Answer:

(i) He should get only interest on loan @ 6% p.a. as per the law.

(ii) In the absence of partnership deed, Profit should be distributed in equal ratio not in proportion of capital.

Dhiman Claims:

(i) His Claim is correct and profit should be distributed in equal ratio.

(ii) He should not be allowed any salary for managing business.

(iii) Payment of interest on loan will be @ 6% p.a. as per the law and no interest on capital will be allowed.

Point of Knowledge:-

Question 6: A and B are partners from 1st April, 2024, without a Partnership Deed and they introduced capitals of Rs. 35,000 and Rs. 20,000 respectively. On 1st October, 2024, A advances a loan of Rs. 8,000 to the firm without any agreement as to interest. The profit and Loss Account for the year ended 31st March, 2025 shows a profit of Rs. 15,000 but the partners cannot agree on payment of interest and on the basis of division of profits.

You are required to divide the profits between them giving reasons for your method.

Answer:

2. Profit will be divided equally as per the law.

Point of knowledge-

1. Calculation of interest on loan

Loan Amount = Rs. 8,000

Time = 6 months (01st Oct. To 31st March)

Rate = 6% (In the absence of partnership deed)

About Solution:

Section 4 of the Indian partnership act 1932 defines

Partnership is the relation between person who have agreed to share the profit of a business carried on by all or any of them acting for all

Things to Remember:

Two or more person – there must be at least two person to form a partnership and such person must be competent to contract as per the Indian contract act, 1872 every person expect the following and competent to contract:-

1) Minor

2) Person of unsound mind

3) Person disqualified by any law

Important Notes:

Partnership act does not specify the maximum number of partner but the central government has prescribed maximum number of partners in a firm to be 50 vide rule 10 of the companies (miscellaneous) rules 2014

Interest on partner’s loan to the firm

Question 7: Sita and Geeta are partners in a firm sharing profits in the ratio of 3:2. They had given a loan to the firm Rs. 30,000 in their profit-sharing ratio on 1st October, 2023. The Partnership Deed is silent on interest on loans from partners. Compute interest payable by the firm to the partners, assuming the firm closes its books every year on 31st March.

Answer:

Interest on Partner’s Loan to the Firm:

According to the Indian Partnership Act, 1932 in the absence of any information and Partnership Deed, the interest on partner’s loan will be allowed at 6% p.a

About Solution:

Interest on partner’s loan being a charge against profit is paid or credited to partner’s loan Account even if profit is less than the amount of interest on loan. The resulting loss is distributed among partners in the profit sharing ratio.

Things to Remember:

A minor cannot be admitted as a partner in the firm however, he is allowed to participate in the profit of the firm.

Important Notes:

Partnership is the result of an agreement it must come into existence by an agreement and not by and operation of on the country a hindu undivided into family comes into existences by the operation of law and not by and agreement such and agreement can be either oral or in writing the agreement forms the basis of mutual rights and duties of partners.

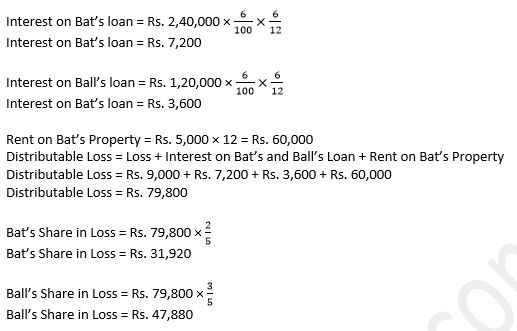

Question 8: Bat and Ball are partners sharing profits and losses in the ratio of 2:3 with capitals Rs. 1,20,000 and Rs. 60,000 respectively. On 1st October, 2023, Bat and Ball gave loans of Rs. 2,40,000 and Rs. 1,20,000 respectively to the firm. Bat had allowed the firm to use his property for business for a monthly rent of Rs. 5,000. Loss for the year ended 31st March 2024 before rent and interest amounted to Rs. 9,000. Show distribution of profit/loss.

Answer:

Calculation of Partner’s Share in Profit and Loss:-

About Solution:

1) As per the provision of Indian Partnership Act, 1932, partner’s loan is repayable on dissolution before payment of capital to partners.

2) In the absence of any agreement, partners are entitled to get interest @ 6% p.a. on loan advanced whereas they are not entitled to interest on capital.

Things to Remember:

Partnership can be formed for the purpose of carrying on some business with the intention of earning profit and such business must be legal a joint ownership of some property by itself cannot be called a partnership.

Important Notes:

The agreement between the partners must be aimed at sharing the profit of business if some person join hands to run some charitable activity it will not be called partnership further if a partner is deprived of his right to share the profit of the business he cannot be called a partner but it is not necessary that all partner should share the loss also it may be agreed between the partner that one or more of them shall not be liable for losses.

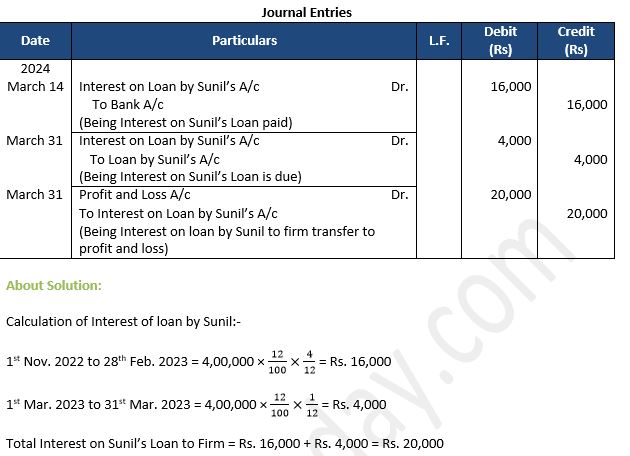

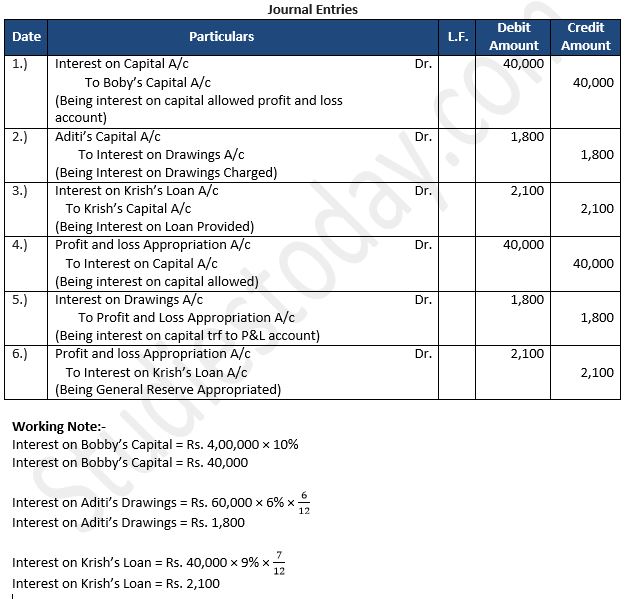

Question 9: Akhil, Sunil, and Parvesh are partners sharing profits in the ratio of 3:2:1. Sunil had given a loan to the firm on 1st November 2022 of ₹ 4,00,000. Interest payable was agreed @ 12% p.a. Interest was paid by cheque up to February 2023 on 1st March 2023 and the balance was yet to be paid. Pass the Journal entries for interest on the loan by the partner.

Answer:

Things to Remember:

Each partner is an agent as well as a principal of the firm an agent because he can bind the other partners by his act and a principal because of himself can be bound by the acts of the other partners.

Important Notes:

It means that each partner’s can participants in the conduct of business and each partner’s is bound by the act of other partner in respect to the business of the firm.

Question 10: Akhil and Bimal are partners sharing profits in the ratio of 3:2. Akhil gave a loan to the firm of ₹ 1,00,000 on 1st January 2024. On the same date, the firm gave a loan to Bimal of ₹ 1,00,000. They do not have an agreement as to interest. Akhil had also given his personal property for the firm’s godown at a monthly rent of ₹5,000. Firm earned a profit of ₹1,03,000 (before the above adjustments) for the year ended 31st March 2024. Show the distribution of profit for the year.

Answer:

Interest on Akhil’s Loan (1st Jan to 31st March)= Rs. 1,00,000 × 6/100 × 3/12

Interest on Akhil’s Loan (1st Jan to 31st March)= Rs. 1,500

Rent on Akhil’s Property = Rs. 5,000 × 12 = Rs. 60,000

Distributable Profit = Rs. 1,03,000 – Rs. 6,000 – Rs. 1,500

Distributable Profit = Rs. 41,500

Akhil’s Share in Profit = Rs. 41,500 × 3/5

Akhil’s Share in Profit = Rs. 24,900

Bimal’s Share in Profit = Rs. 41,500 × 2/5

Bimal’s Share in Profit = Rs. 16,600

Things to Remember:

A partnership firm has no separate existence form its member it mean all agreement entered with the firm will be enforceable against each partner separately (however, partnership firm is a separate business entity form accounting point of view).

Important Notes:

1) Every Partner has the right to share profit or losses with their partner in the agreed ratio.

2) Every Partner has the right to take part in the conduct of the business.

Question 11: Nirmal and Pawan are partners sharing profits in the ratio of 3:2. The firm had given loan to Pawan of Rs. 5,00,000 on 1st April, 2023. Interest was to be charged @10% p.a. The firm took loan of Rs. 2,00,000 from Nirmal on 1st December, 2023. Before giving effect to the above, the firm incurred a loss of Rs. 10,000 for the year ended 31st March, 2024. Determine the amount to be transferred to Profit and loss Appropriation Account.

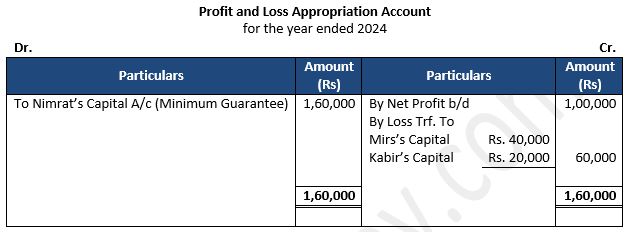

Answer:

Interest on Loan given by firm to Pawan (1st April to 31st March)= Rs. 5,00,000 × 10/100

Interest on Loan given by firm to Pawan = Rs. 50,000

Interest on Loan of Nirmal to Firm (1st Dec. to 31st March)= Rs. 2,00,000 × 6/100× 4/12

Interest on Loan given by firm to Pawan = Rs. 4,000

Net Profit transferred to Profit and Loss Appropriation = Loss + Interest on Loan to Pawan – Interest on Loan by Nirmal

Net Profit transferred to Profit and Loss Appropriation = -10,000 + 50,000 – 4,000

Net Profit transferred to Profit and Loss Appropriation = 36,000

About Solution:

Here Net Profit is given after debiting Z’s Salary, so we have to add Z’s Salary to net profit given in question.

Things to Remember:

1) Every partner has to right to be consulted in the matter related to partnership business.

2) Every partner has the right to inspect and have a copy of the books of account.

Important Notes:

1) Every partner has a right to disallow the admission of a new partner.

2) Every partner is the joint owner of the partnership property.

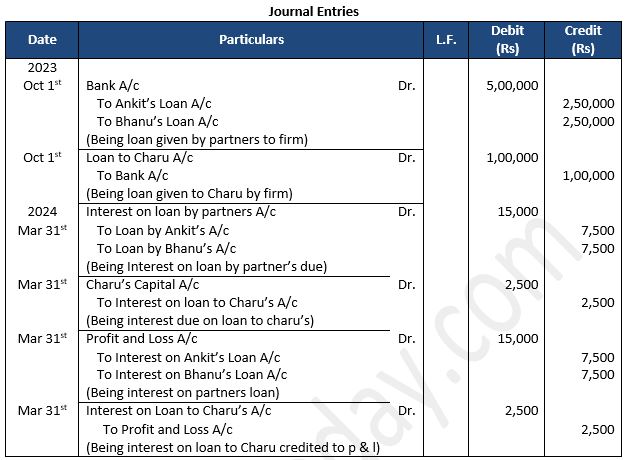

Question 12: Ankit, Bhanu, and Charu are partners in a firm sharing profits and losses equally with a capital of ₹ 2,50,000 each. On 1st October 2023, Ankit and Bhanu gave loans of ₹ 2,50,000 each to the firm whereas Charu took a loan of ₹ 1,00,000 from the firm on 1st November, 2023. It was agreed among the partners that Charu will be charged interest @ 6% p.a.. Interest on loans from partners was paid on 10th April 2024. The firm closes its books on 31st March each year.

Pass the Journal entries in the books of the firm for the year ended 31st March 2024.

Answer:

About Solution:

Calculation of Partners Loan:-

Interest on Ankit’s Loan to Firm (1st Oct. to 31st March) = Rs. 2,50,000 × 6% × 6/12

Interest on Ankit’s Loan to Firm = Rs. 7,500

Interest on Bhanu’s Loan to Firm (1st Oct. to 31st March) = Rs. 2,50,000 × 6% × 6/12

Interest on Bhanu’s Loan to Firm = Rs. 7,500

Interest on Bhanu’s Loan to Firm (1st Nov. to 31st March) = Rs. 1,00,000 × 6% × 5/12

Interest on Bhanu’s Loan to Firm = Rs. 2,500

Things to Remember:

If a partner has given loan to a firm he has a right to receive interest agreed rate.

If the rate of interest is not agreed it is paid @6%p.a.

Important Notes:

If a partner incurs expenses or makes payment on behalf of the firm he has a right to be indemnified by the firm.

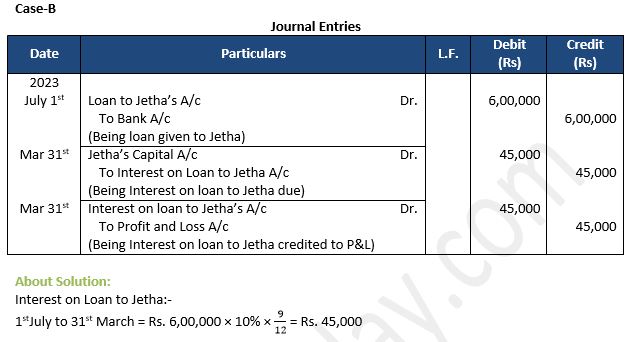

Question 13: Atul, Jetha, and Tarak are partners sharing profits equally. Jetha was given a loan by the firm on 1st July 2023 of ₹ 6,00,000. Books are closed on 31st March, What Journal entries will be passed if

(a) Rate of Interest is not agreed; and

(b) Rate of interest to be charged is agreed @ 10% p.a.?

Answer:

Case-A

No Journal Entries will pass as Interest on loan to Jetha’s Loan is not agreed.

Things to Remember:

The limited liability partnership (LLPs) in India came into existence with the enactment of limited liability partnership act 2008 which lay down the law for the formation and regulation of limited liability partnerships

Important Notes:

1) A LLP is a body corporate formed and incorporated under this act

2) It is a legal entity separate from that of its partners

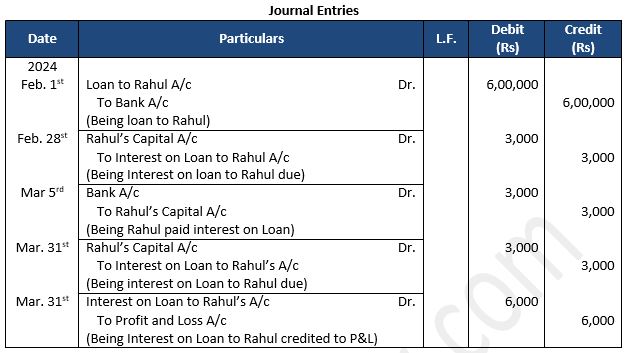

Question 14: Parul, Paresh, and Rahul are partners in a firm. The firm gave a loan to Rahul on 1st February 2024 of ₹ 6,00,000. Interest was agreed to be charged @ 6% p.a. Interest was paid by cheque up to February 2024 by Rahul on 5th March 2024 and the balance was paid by him on 5th April, 2024.

Pass the Journal entries for interest on loan to partners.

Answer:

Working Note:

1.) Calculation of Interest on loan:-

Interest on Rahul’s Loan = Rs. 6,00,000 × 6% × 1/12

Interest on Rahul’s Loan = Rs. 3,000

About Solution:

1) The firm has incurred loss, so no interest on capital and salary will be allowed to the partners.

Things to Remember:

1) A LLP shall have perpetual succession.

2) Any change in the partner of a LLP shall not affect the existence right or liability of the LLP.

Important Notes:

Since partnership is the outcome of an agreement it is essential that there must be some term and condition agreed upon by all the partners such term and condition may be either oral or written the law does not make it compulsory to have a written agreement duty and signed and registered and under the act such a written document which contain the term of agreement is called partnership deed it is also called partnership article of partnership.

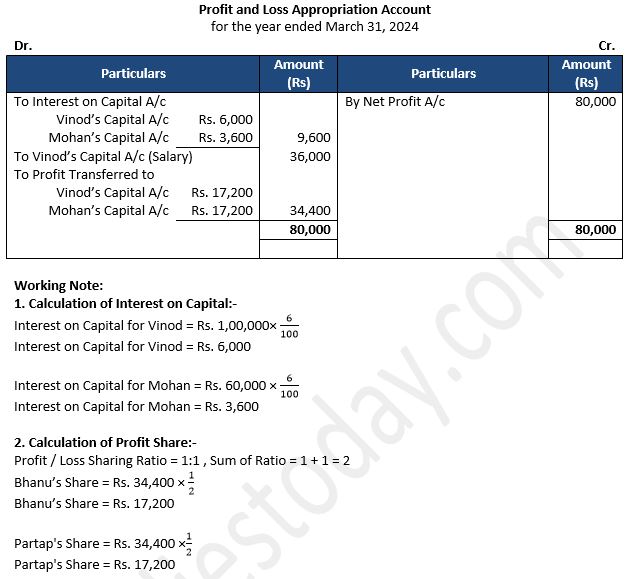

Question 15: Vinod and Mohan are partners. Vinod’s Capital is Rs. 1,00,000 and Mohan’s Capital is Rs. 60,000. Interest on Capital is payable @6% p.a. Vinod is to get a salary of Rs. 3,000 per month. Net profit for the year is Rs. 80,000.

Prepare Profit and Loss Appropriation Account.

Answer:

About Solution:

1) It regulates the rights, duties and liabilities of each partner

2) It helps to avoid any misunderstanding amongst the partner because all the term and condition of partnership have been laid down before hand in the deed.

Important Notes:

In the absence of a partnership deed or verbal agreement or if the partnership deed is a silent on a certain point the following provision of partnership act, 1932.

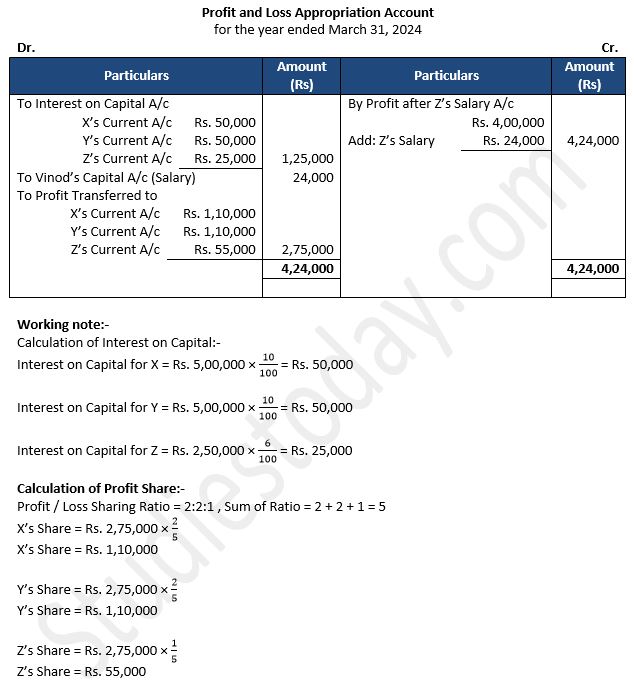

Question 16: X, Y, and Z are partners in a firm sharing profits in the ratio of 2:2:1. Fixed Capitals of the partners were: X ₹ 5,00,000; Y ₹ 5,00,000 and Z ₹ 2,50,000 respectively. The Partnership Deed provides that interest on capital is to be allowed @ 10% p.a. Z is to be allowed a salary of ₹ 2,000 per month. Profit of the firm for the year ended 31st March, 2024 after Z’s salary was ₹ Prepare Profit and Loss Appropriation Account.

Answer:

About Solution:

In the absence of partnership deed profits and losses are to be shared equally irrespective of their capital contribution.

Things to Remember:

1) In the absence of partnership deed no interest on capital shall be allowed to be partners if there is a provision for the interest on capitals in the partnership deed it will be allowed only when there is a profit.

Important Notes:

In the absence of partnership deed no interest to be charged on drawings

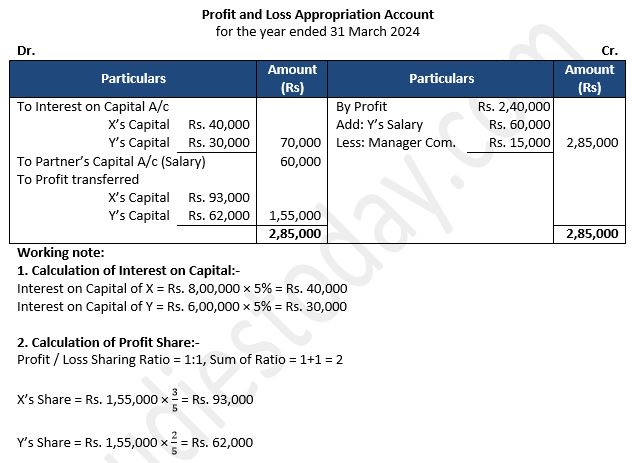

Question 17: X and Y are partners sharing profits in the ratio of 3 : 2 with capitals of ₹ 8,00,000 and ₹ 6,00,000 respectively. Interest on capital is agreed @ 5% p.a. Y is to be allowed an annual salary of ₹ 60,000 which has not been withdrawn. Profit for the year ended 31st March 2024 before interest on capital but after charging Y’s salary was ₹ 2,40,000.

A provision of 5% of the net profit is to be made in respect of commission to the Manager. Prepare a Profit and Loss Appropriation Account showing the allocation of profits.

Answer:

About Solution:

In the absence of partnership deed no partner is entitled to any salary or commission for taking part in running the firm’s business.

Things to Remember:

In the absence of partnership deed interest on the rate of 6% per annum is to be allowed on a partner’s loan to the firm such interest shall be paid even if there are losses to the firm.

Important Notes:

In the absence of partnership deed without the consent for all existing partners no new partner can be admitted to the firm.

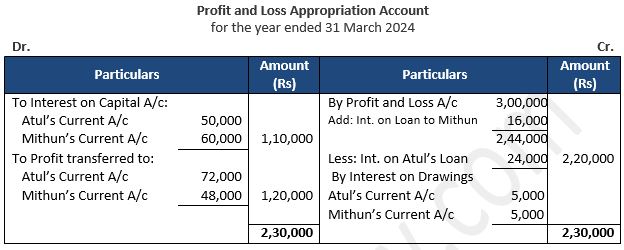

Question 18: Atul and Mithun are partners sharing profits in the ratio of 3 : 2. Balances as on 1st April 2023 were as follows:

Capital Accounts (Fixed): Atul – ₹ 5,00,000 and Mithun – ₹ 6,00,000.

Loan Account: Atul – ₹ 3,00,000 (Cr.) and Mithun – ₹ 2,00,000 (Dr.)

It was agreed to allow and charge interest @ 8% p.a. Partnership Deed was provided to allow interest on capital @ 10% p.a. Interest on Drawings was charged ₹ 5,000 each.

Profit before giving effect to above was ₹ 2,28,000 for the year ended 31st March 2024.

Prepare Profit and Loss Appropriation Account.

Answer:

Working capital:

1. Calculation of interest on partners Loan:-

Interest on Loan to Mithun = Rs. 2,00,000 × 8%

Interest on Loan to Mithun = Rs. 16,000

Interest on Loan from Mithun = Rs. 3,00,000 × 8%

Interest on Loan from Mithun = Rs. 24,000

2. Calculation of Interest on Capital:-

Interest on Atul’s Capital = Rs. 5,00,000 × 10%

Interest on Loan to Mithun = Rs. 50,000

Interest on Mithun’s Capital = Rs. 6,00,000 × 10%

Interest on Mithun’s Capital = Rs. 60,000

About Solution:

In the absence of partnership deed each partner can participate in the conduct of business.

Things to Remember:

Entry of transfer of net profit to profit & loss appropriation account:-

Profit and loss A/C

To Profit and Loss Appropriation A/C

(Net profit transferred)

Important Notes:

Profit and Loss a/c is prepared just after the profit and loss account hence it is an extension of profit and loss account it is prepared only by partnership deed.

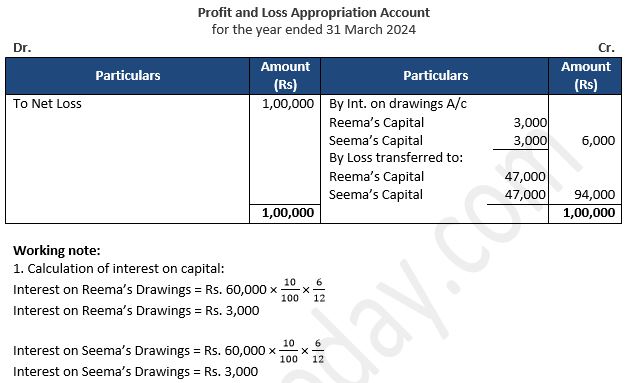

Question 19: Reema and Seema are partners sharing profits equally. The Partnership Deed provides that both Reema and Seema will get a monthly salary of ₹ 15,000 each, Interest on Capital will be allowed @ 5% p.a. and Interest on Drawings will be charged @ 10% p.a. Their capitals were ₹ 5,00,000 each and drawings during the year were ₹ 60,000 each.

The firm incurred net loss of ₹ 1,00,000 during the year ended 31st March 2024.

Prepare Profit and Loss Appropriation Account for the year ended 31st March 2024.

Answer:

About Solution:

Any amount payable to a partner such a salary, commission , interest on capital etc ( except interest on a partner ‘loan and rent payable to a partner) is treated as appropriation of profit and not a charge against profit hence these item are debited to profit and loss appropriation a/c instead of profit and loss a/c

Things to Remember:

Profit and loss A/C is a nominal account it shows how the net profit for the accounting period is appropriated (distributed) among the partner.

Important Notes:

1) On allowing interest on capital

Interest on capital account

To partner’s capital account Dr

( interest on capital at …..%p.a.)

2) On closure of interest on capital A/C:

Interest on capital is closed by transferring it to the debit side of profit and loss appropriation a/c as this is expenses for the firm the entry will be

Profit and loss appropriation A/c Dr

To interest on capital A/c

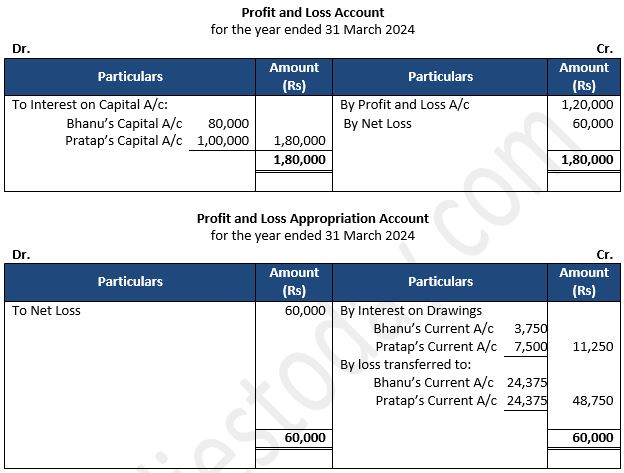

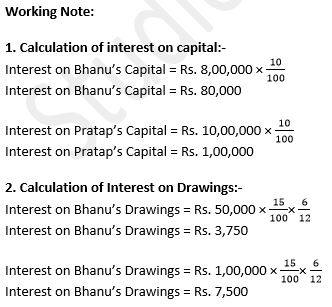

Question 20: Bhanu and Partap are partners sharing profits equally. Their fixed capitals as on 1st April 2023 were ₹ 8,00,000 and ₹ 10,00,000 respectively. Their drawings during the year were ₹ 50,000 and ₹ 1,00,000 respectively. Interest on Capital is a charge and is to be allowed 10% p.a. and interest on drawings is to be charged @ 15% p.a. Net Profit for the year ended 31st March 2024 before giving effect to the above) was ₹ 1,20,000.

Prepare Profit and Loss Appropriation Account.

Answer:

About Solution:

Profit and loss A/C entries in this account are made giving effect to the partnership deed and /or the Indian partnership act, 1932.

Things to Remember:

Entry for interest on Drawing:

1) On charging interest on drawing:

Partner’s capital A/c Dr.

To interest on drawing A/c

2) On closure on interest on drawing A/c

Interest on drawing is closed by transferring it to the credit side of profit and loss appropriation A/c as these the income of the firm the entry will be:

Interest on drawing A/c Dr.

To Profit & Loss appropriation A/C

Important Notes:

As already stated interest on partner’s capital is to be allowed only when it is expressly agreed to among partner if interest on capital is to be allowed as per agreement it should be calculated with respect to the time rate of interest and the amount of capital.

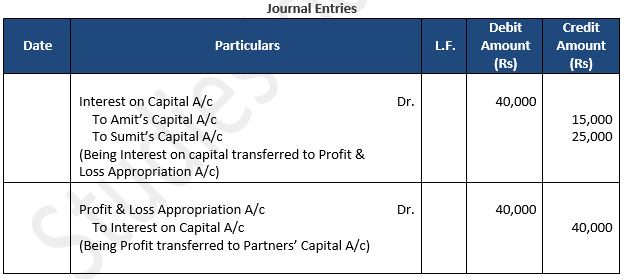

Question 21: Amit and Sumit entered into a partnership on 1st April 2023 and invested ₹ 1,50,000 and ₹ 2,50,000 respectively as capital. The Partnership Deed provided for interest on capital @ 10% p.a. It also provided that Capital Accounts shall be maintained following the Fixed Capital Accounts Method. The firm earned a net profit of ₹ 1,00,000 for the year ended 31st March 2024. Pass the Journal entry for interest on capital.

Answer:

Working Note:-

Calculation of Interest on Capital:-

Interest on Amit’s Capital = 1,50,000 × 10%

Interest on Amit’s Capital = 15,000

Interest on Sumit’s Capital = 2,50,000 × 10%

Interest on Sumit’s Capital = 25,000

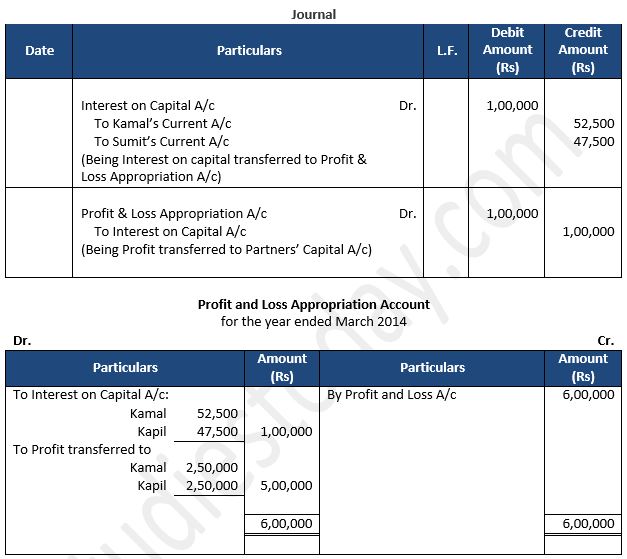

Question 22: Kamal and Kapil are partners having fixed capitals of ₹ 5,00,000 each as on 1st April 2023. Kamal introduced further capital of ₹ 1,00,000 on 1st January 2024 whereas Kapil withdrew ₹ 1,00,000 on 1st January 2024 out of capital.

Interest on capital is to be allowed @ 10% p.a.

The firm earned a net profit of ₹ 6,00,000 for the year ended 31st March 2024. Pass the Journal entry for interest on capital and prepare Profit and Loss Appropriation Account.

Answer:

Point of Knowledge:

Calculation of Interest on Partners Capital:-

Kamal’s Interest on Capital:-

(1st April to 30th September) = Rs. 5,00,000 × 10% × 9/12

(1st April to 30th September) = Rs. 37,500

(1st Oct to 31th March) = Rs. 6,00,000 × 10% × 3/12

(1st Oct to 31th March) = Rs. 15,000

Total Interest on Komal’s Capital = Rs. 37,500 + Rs. 15,000 = Rs. 52,500

Kapil’s Interest on Capital:-

(1st April to 30th September) = Rs. 5,00,000 × 10% × 9/12

(1st April to 30th September) = Rs. 37,500

(1st Oct to 31th March) = Rs. 4,00,000 × 10% × 3/12

(1st Oct to 31th March) = Rs. 10,000

Total Interest on Komal’s Capital = Rs. 37,500 + Rs. 10,000 = Rs. 47,500

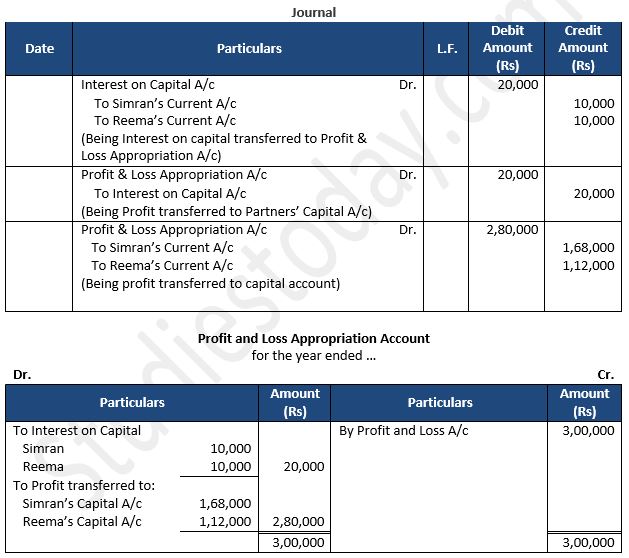

Question 23: Simran and Reena are partners sharing profits in the ratio of 3:2. Their capital as on 1st April, 2023 were Rs. 2,00,000 each whereas Current Account had balance of Rs. 50,000 and Rs. 25,000 respectively. Interest on capital is to be allowed @5% p.a. Net profit of the firm for the year ended 31st March, 2024 was Rs. 3,00,000.

Pass the Journal entries for interest o capital and distribution of profit. Also prepare Profit and Loss Appropriation Account for the year.

Answer:

Points of knowledge:

1. Calculation of Interest on Capital:-

Interest on Simran’s Capital = 2,00,000 × 5/100

Interest on Simran’s Capital = Rs. 10,000

Interest on Reema’s Capital = 2,00,000 × 5/100

Interest on Reema’s Capital = Rs. 10,000

2. Calculation of Partner’s Share in Profit:-

Simran’s Share in Profit = Rs. 2,80,000 × 3/5

Simran’s Share in Profit = Rs. 1,68,000

Reema’s Share in Profit = Rs. 2,80,000 × 2/5

Reema’s Share in Profit = Rs. 1,12,000

Question 24: Anita and Ankita are partners sharing profit equally. Their capital, maintained following Fluctuating Capital Accounts Method, as on 1st April, 2023 were Rs. 5,00,000 and Rs. 4,00,000 respectively. Partnership Deed provided to allow interest on capital @10% p.a. The firm earned net profit of Rs. 2,00,000 for the year ended 31st March, 2024.

Pass the Journal entry for interest on capital.

Answer:

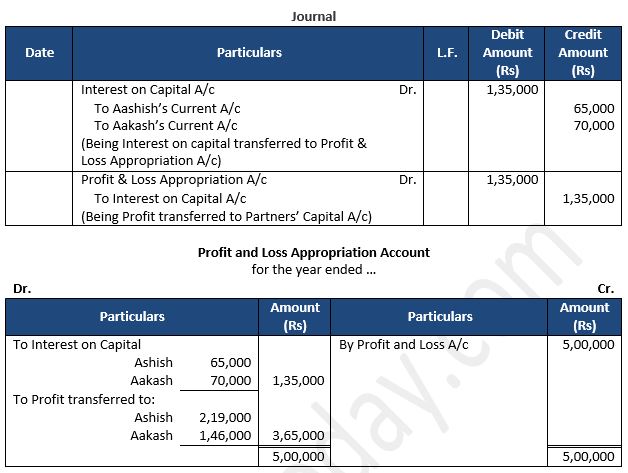

Question 25: Ashish and Aakash are partners sharing profits in the ratio of 3:2. Their Capital Accounts had credit balances of Rs. 5,00,000 and Rs. 6,00,000 respectively as on 31st March, 2024 after debit of drawings during the year of Rs. 1,50,000 and Rs. 1,00,000 respectively. Net profit for the year ended 31st March, 2024 was Rs. 5,00,000. Interest on capital is to be allowed @ 10% p.a.

Pass the journal entry for interest on capital and prepare Profit and Loss Appropriation Account.

Answer:

Working Note:-

Calculation of opening capital of Ashish:-

Opening Capital = Closing Capital + Drawings

Opening Capital = Rs. 5,00,000 + Rs. 1,50,000

Opening Capital = Rs. 6,50,000

Calculation of opening capital of Aakash:-

Opening Capital = Closing Capital + Drawings

Opening Capital = Rs. 6,00,000 + Rs. 1,00,000

Opening Capital = Rs. 7,00,000

Calculation of Partners interest on capital:-

Interest on Capital of Ashish = Rs. 6,50,000 × 10%

Interest on Capital of Ashish = Rs. 65,000

Interest on Capital of Aakash = Rs. 7,00,000 × 10%

Interest on Capital of Aakash = Rs. 70,000

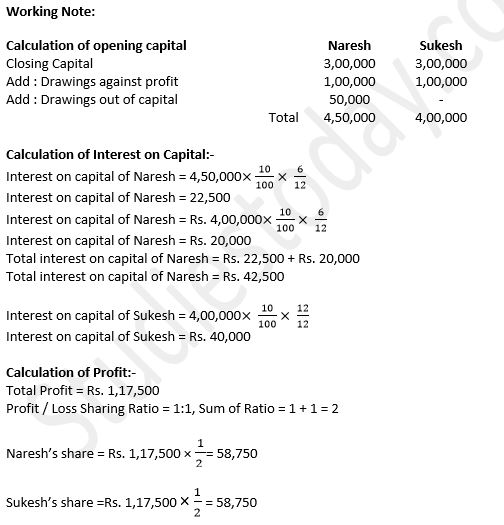

Question 26: Naresh and Sukesh are partners with capitals of Rs. 3,00,000 each as on 31st March, 2023. Naresh had withdrawn Rs. 50,000 against capital on 1st October, 2022 and also Rs. 1,00,000 besides the drawings against capital. Sukesh also had drawings of Rs. 1,00,000. Interest on capital is to be allowed @ 10% p.a. Net profit for the year was Rs. 2,00,000, which is yet to be distributed. Pass the journal entries for interest on capital and distribution of profit.

Answer:

Every partner is an agent of the other partners. Every partner can bind the firm and all other partners by his/her acts. Each partner will be responsible and liable for the acts of all other partners.

Things to Remember:

The liability of each partner, except that of a minor, is unlimited. Their liability extends to their personal assets also. If the assets of the firm are insufficient to pay off its debts, the partners’ personal property can be used to satisfy the claim of the creditors of the partnership firm.

Important Notes:

All the partners have a right to manage the business. However, they may authorize one or more partners to manage the affairs of the business on their behalf.

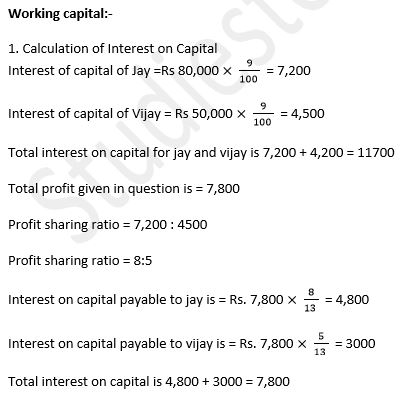

Question 27: On 1st April, 2013, Jay and Vijay entered into partnership for supplying laboratory equipment to government schools situated in remote and backward areas. They contributed capitals of Rs. 80,000 and Rs. 50,000 respectively and agreed to share the profits in the ratio of 3:2. The partnership Deed provided that interest on capital shall be allowed at 9% per annum. During the year the firm earned a profit of Rs. 7,800. Showing your calculations clearly, prepares 'Profit and Loss Appropriation Account' of Jay and Vijay for the year ended 31st March, 2014.

About Solution:

No partner can transfer his/her share to anyone including his/her family member without the consent of all other partners.

Things to Remember:

The persons who have agreed to carry on a business and share its profits and losses. They are the persons who have agreed upon the terms and conditions of partnership.

Important Notes:

Partners who carry on the business are collectively known as firm. The name under which the business is carried on is called firm name.

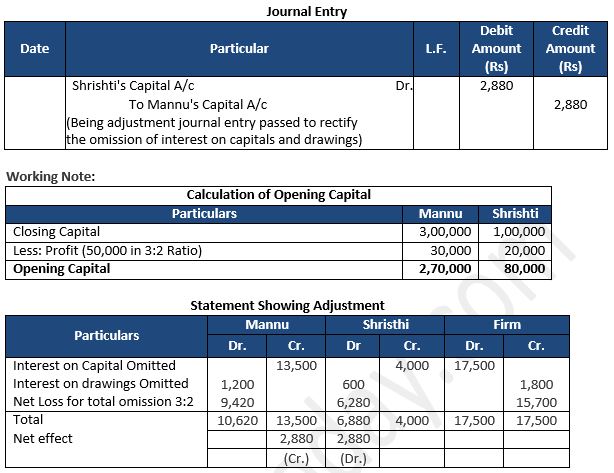

Question 28: A and B are partners in the ratio of 3 : 2. The firm maintains Fluctuating Capital Accounts and the balance of the same as on 31st March 2020 amounted to ₹ 1,60,000 ad ₹ 1,40,000 for A and B respectively. Their drawings during the year were ₹ 30,000 each.

As per Partnership Deed, interest on capital @ 10% p.a. on opening capitals had been provided to them. Calculate the opening capital of partners given that their profit was ₹ 90,000. Show your working clearly.

Answer:

Working Note:-

Total Opening Capital of the Firm = Closing Capital of the Partners + Drawing – Profit

Total Opening Capital of the Firm = 1,60,000 – 1,40,000 + 30,000 + 30,000 – 90,000

Total Opening Capital of the Firm = Rs. 2,70,000

Distribution of Profit:-

A’s Profit Share = 63,000 × 3/5

A’s Profit Share = Rs.37,800

B’s Profit Share = 63,000 × 2/5

B’s Profit Share = Rs.25,200

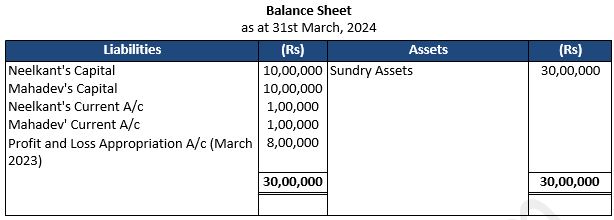

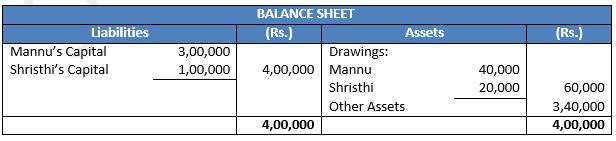

Question 29: Following is the extract of the Balance Sheet of Neelkant and Mahadev as on 31st March, 2024.

During the year, Mahadev's drawings were Rs. 30,000. Profits during the year ended 31st March, 2024 is Rs. 10,00,000. Calculate interest on capital @ 5% p.a. for the year ending 31st March, 2024.

Answer:

Calculation of interest of capital:-

1. Interest on capital of Neelkant = Rs. 10,00,000 × 5/100

Interest on capital of Neelkant = Rs. 50,000

2. Interest on capital of Mahadev = Rs. 10,00,000 × 5/100

Interest on capital of Mahadev = Rs. 50,000

About Solution:

The Capital of both the partners are fixed as current accounts are given in the balance sheet.Hence interest on capital will be calculated on fixed capital balances.

Things to Remember

Sometimes, a partner is admitted in the firm on guarantee in respect of his minimum share of profit from the business. Such a guarantee can be given even to an existing partner also

(a) The firm i.e. by all the old partners in an agreed ratio, or

(b) Some of the old partners or any one of the old partners

Important Note:

When all the partners guarantee that one of the partners shall be given a minimum amount of profit, we should calculate the following two amounts separately:

1) Share of profit of the guaranteed partner as per profit sharing ratio, and

2) Minimum guaranteed amount of profit of the granted partner.

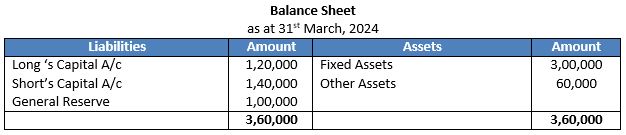

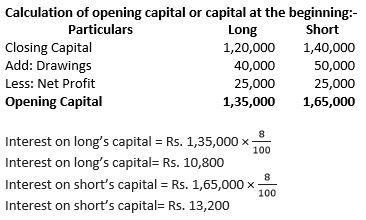

Question 30: From the following Balance Sheet of Long and Short, calculate interest on capital @ 8% p.a. for the year ended 31st March, 2024.

During the year, Long withdrew Rs. 40,000 and Short withdrew Rs. 50,000. Profit for the year wasRs.1,50,000 out of whichRs.1,00,000 was transferred to General Reserve.

Answer:

About Solution:

1. Interest on capital is calculated on opening capital balances only.

2. In the absence of any profit sharing ratio it will be taken as equal.

3. Drawings given in the additional information has been deducted out of opening capital and drawings if given in the asset side of the balance sheet indicates no deduction of drawings out of capital.

Things to Remember:

The higher of the above two is to be given to that partner. The balance of profit (total profit minus profit given to the guaranteed partner) is to be shared by the remaining partners in their respective profit -sharing ratio. When the new partner’s share of profit is more than the guaranteed amount, his actual share of profit is given to him instead of the guaranteed amount of profit.

Important Note:

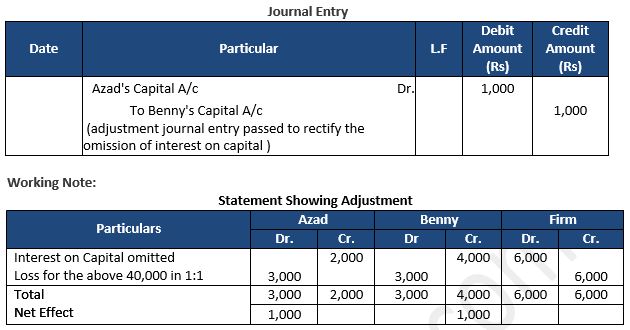

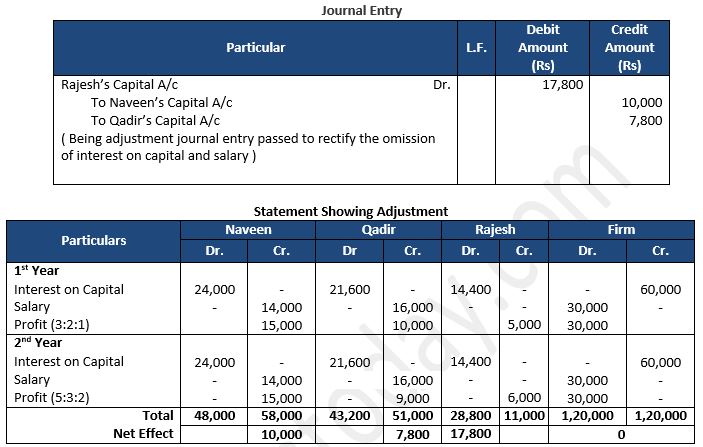

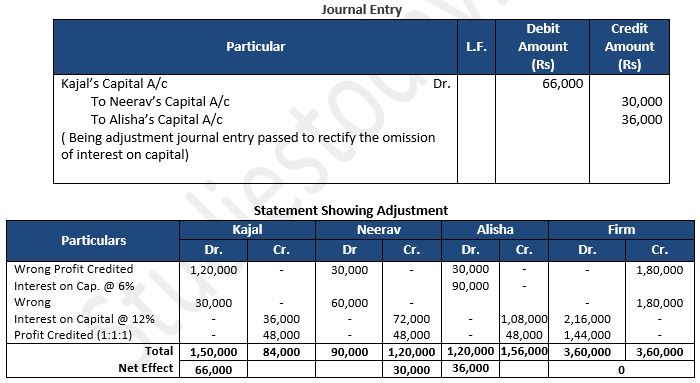

Sometimes, after closing the accounts of the partnership firm at the end of the financial year, it is discovered that there had been some errors or omissions in the accounts. In such cases, instead of altering the old accounts and the signed Balance Sheet an adjustment entry for such errors or omissions is made at the beginning of the next year

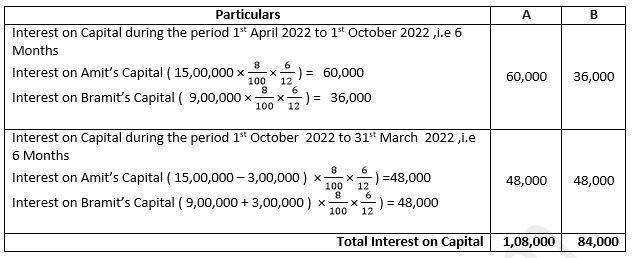

Question 31: Amit and Bramit started business on 1st April, 2023 with capitals of Rs. 15,00,000 and Rs. 9,00,000 respectively. On 1st October, 2023, they decided that their capitals should be Rs. 12,00,000 each. The necessary adjustments in capitals were made by introducing or withdrawing by cheque. Interest on capital is allowed @ 8% p.a. Compute interest on capital for the year ended 31st March, 2024.

Answer:

Calculation of Interest on Capital:-

About Solution:

Charge means full interest is to be allowed whether there are profits or losses.

Things to Remember:

Appropriation means interest is to be allowed only out of profits. It means that the interest on capital cannot exceed the amount of profit.

Important Note:

It the partnership deed is silent, no interest will be allowed on capital.

Question 32: Moli and Bholi contribute Rs. 20,000 and Rs. 10,000 respectively towards capital. They decide to allow interest on capital @ 6% p.a. Their respective share of profits is 2 : 3 and the net profit for the year is Rs. 1,500. Show distribution of profits:

(i) Where there is no agreement except for interest on capitals; and

(ii) Where there is an agreement that the interest on capital as a charge.

Since the amount of net profit is less than the total amount of interest on capital, So interest on capital will be allowed in the ratio of interest on capital amount.

X’s Share = Rs. 300×2/5= Rs. 120

Y’s Share =Rs. 300×2/5 = Rs. 180

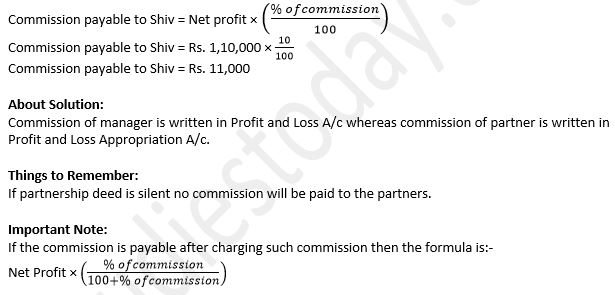

Question 33: Shiv, Moha and Gopal are partners sharing profits and losses in the ratio of 2:2:1 respectively. A is entitled to a commission of 10% on the net profit. Net profit for the year is Rs. 1,10,000. Determine the amount of commission payable to A.

Answer:

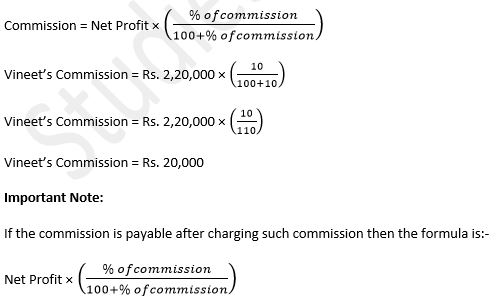

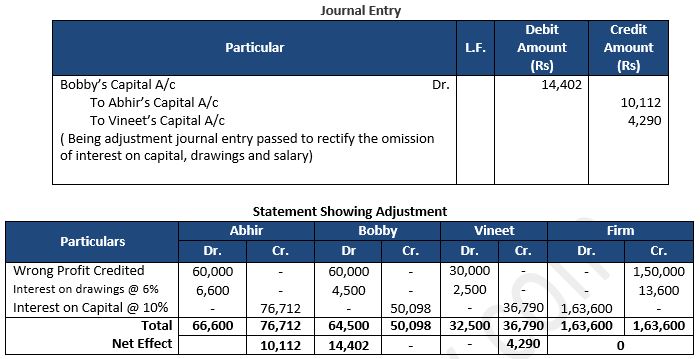

Question 34: Abha, Bobby, and Vineet are partners sharing profits and losses equally. As per Partnership Deed, Vineet is entitled to a commission of 10% on the net profit after charging such commission. Net Profit before charging commission is ₹ 2,20,000. Determine the amount of commission payable to Vineet.

Answer:

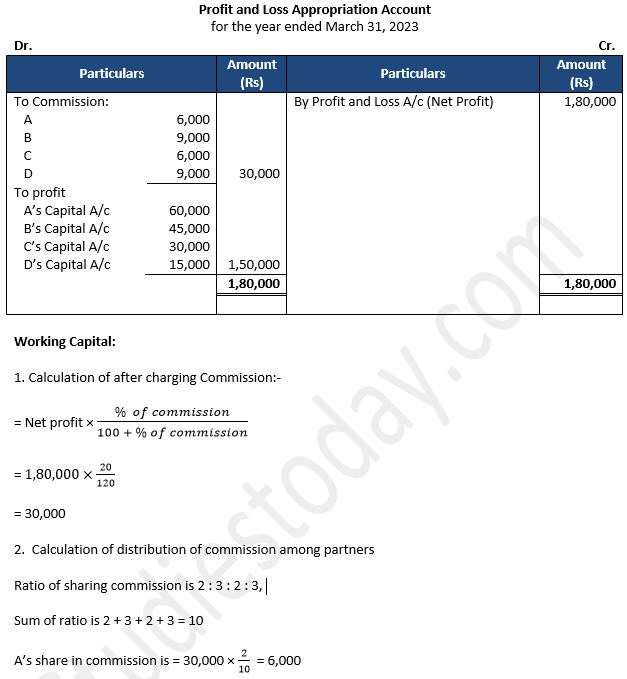

Question 35: A, B, C, and D are partners in a firm sharing profits as 4 : 3 : 2 : 1. The firm earned net profit of Rs. 1,80,000 for the year ended 31st March, 2024. As per the Partnership Deed, they are to charging the commission @ 20% of the profit after charging such commission which they will share as 2:3:2:3. You are required to show appropriation of profits among the partners.

Answer:

About Solution:

1) Distribution of Profit: Partners are entitled to share profits equally.

2) Interest on Capital: Interest on capital is not allowed.

3) Interest on Drawings: No interest on drawing of the partners is to be charged.

Things to Remember:

1) Interest on Partner’s Loan: A Partner is allowed interest @ 6% per annum on the amount of loan given to the firm by him/her.

2) Salary and Commission to Partner: A partner is not entitled to any salary or commission or any other remuneration for managing the business.

Important Note:

Partners contribute their share of capital in business. These are recorded in their respective accounts named as capital accounts. Suppose there are two partners A and B, there will be A’s capital account and B’s capital account. These accounts may be maintained in two ways.

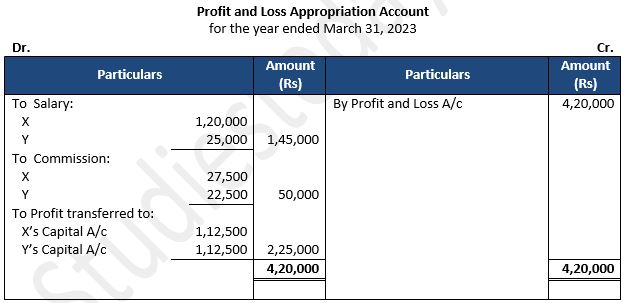

Question 36: X and Y are partners in a firm. X is entitled to salary of Rs. 10,000 per month and commission of 10% of the net profit after partners' salaries but before charging commission. Y is entitled to a salary of Rs. 25,000 p.a. and commission of 10% of the net profit after charging all commission and partners' salaries. Net profit before providing for partners' salaries and commission for the year ended 31st March, 2023 was Rs. 4,20,000, show distribution of profit.

Answer:

Working Capital:

1. Calculation of salary given to both partners:-

X is taking salary Rs. 10,000 per months

X’s salary = Rs. 10,000 × 12

X’s salary = Rs. 1,20,000

Y’s salary = Rs. 25,000

2. Calculation of distribution of commission to both partners

Distributable Profit = Net profit - salary

Distributable Profit = 4,20,000- 1,45,000

Distributable Profit= 2,75,000

X is taking 10% before charging commission

X’s share in commission = 2,75,000 × 10/100

X’s share in commission = 27,500

Y is taking 10% after charging such commission

Y’s share in commission = 2,75,000 – 27500(x’scommission) = 2,47,500

Y’s share in commission= 2,47,500 × 10/110 = 22,500

Total commission given to both the partners is 27500 + 22500 = 50,000

3. Calculation of distribution Net profit among partners

Total profit = 4,20,000 – 1,45,000 (salary) – 50,000 (commission) = 2,25,000

Profit / Loss Sharing Ratio =1:1

Sum of Ratio = 1+1 = 2

X’s share in profit = Rs. 2,25,000 × 1/2

X’s share in profit = Rs. 1,12,500

Y’s share in profit = Rs. 2,25,000 × 1/2

Y’s share in profit is = Rs. 1,12,500

About Solution:

In fixed capital account, the closing balance of the capital account is same as that of opening balance except when additional capital is introduced or there is permanent withdrawal during the current accounting year. Items relating to capital account such as interest on capital, interest on drawings and share of profit etc., are recorded incapital account. But in this case a separate account is opened for each partner to record these items. This account is known as ‘current account’. A current account may show a debit or a credit balance. Format of the fixed capital account and the current account is as under

Things to Remember:

When capital account for each partner is so maintained that in addition to the capital amount other items related to capital account such as interest on capital, drawings, net profit or net loss etc. are written in this account, it is termed as fluctuating capital. In this case there is no need to maintain a separate account for recording of these adjustments.

Important Note:

Let us now study about calculation of interest on capital. As you know that, interest on capital is allowed when it is provided in the Partnership Deed. If it is so provided, therate of interest will be as agreed upon by the partners. Interest is charged on the opening balance of the partner’s capital account. When additional capital is introduced and some capital is withdrawn permanently, the interest will be calculated on the amount of the capital used in the business during a particular period. Interest is treated as an expense as it is a charge on the profits of the firm.

Question 37: Ram and Mohan, two partners, drew for their personal use Rs. 1,20,000 and Rs. 80,000. Interest is chargeable @ 6% p.a. on the drawings. What is the amount of interest chargeable from each partner?

Answer:

Calculation of interest on drawings of both the partners:

Interest is chargeable on drawings is 6% p.a:-

Interest on Ram’s drawings = 1,20,000 × 6 / 12 × 6 / 100

Interest on Ram’s drawings = 3,600

Interest on Mohan’s drawings = 80,000 × 6 / 12 × 6 / 100

Interest on Mohan’s drawings = 2,400

Total interest on drawing = Rs. 3,600 + Rs. 2,400

Total interest on drawing = 6,000

About Solution:

When the rate of is interest is given without the words ‘per annum’ interest will be charged without considering time of date of drawings . in other words interest will be charged for 12 months.

Things to Remember:

The higher of the above two is to be given to that partner. The balance of profit (total profit minus profit given to the guaranteed partner) is to be shared by the remaining partners in their respective profit -sharing ratio. When the new partner’s share of profit is more than the guaranteed amount, his actual share of profit is given to him instead of the guaranteed amount of profit.

Important Note:

Sometimes, after closing the accounts of the partnership firm at the end of the financial year, it is discovered that there had been some errors or omissions in the accounts. In such cases, instead of altering the old accounts and the signed Balance Sheet an adjustment entry for such errors or omissions is made at the beginning of the next year.

Question 38: Brij and Mohan are partners in a firm. They withdrew Rs. 48,000 and Rs. 36,000 respectively during the year evenly in the middle of every month. According to the partnership agreement, interest on drawings is to be charged @ 10% p.a. Calculate interest on drawings of the partners using the appropriate formula.

Answer:

Calculation of interest on drawings of both the partners

Interest is chargeable on drawings is 10% p.a.

Interest on Brij’s drawings = Rs. 48,000 × 6 / 12 × 10 / 100

Interest on Brij’s drawings = Rs. 2,400

Interest on Mohan’s drawings = Rs. 36,000 × 6 / 12 × 10 / 100

Interest on Mohan’s drawings = Rs. 1,800

About Solution:

When a partner withdrawn an equal amount at the middle of the every month, then Interest on drawings is to be calculated for six months.

Things to Remember:

For Interest on Capital

Interest on Capital A/c Dr.

To Partner’s Capital A/c (Individually)

(Crediting ‘Interest on Capital’ to Capital Account)

Important Note:

Interest can be calculated directly i.e. simple interest is to be calculated by taking the principal amount, period and rate of interest. Alternately interest can be calculated by product method i.e. by converting the principal amount into monthly products depending upon number of months for which principal amount remained in business. Then the interest is calculated by taking monthly rate of interest.

Question 39: Dev withdrew ₹ 10,000 on the 15th day of every month. Interest on drawings was to be charged @ 12% per annum. Calculate interest on Dev’s Drawings.

Answer:

Question 40: One of the partners in a partnership firm has withdrawn Rs. 9,000 at the end of each quarter, throughout the year, Calculate interest on drawings at the rate of 6% per annum.

Answer:

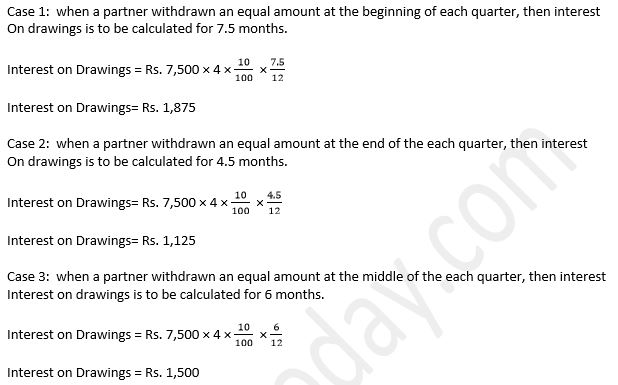

Calculation of interest on drawings when one of the partner’s has withdrawn Rs. 9,000 at the end of each quarter throughout the year:

Interest on drawings =

![]()

About Solution:

When a partner withdrawn an equal amount at the beginning of every month for the first six Months then interest on drawings is to be calculated for 4.5 months.

Things to Remember:

A fixed amount may be withdrawn every month/ half yearly/ annually. The interest has to be calculated for the period for which the amount has been utilised for personal purposes by the partners. The calculation of amount of interest to be charged in different situations is shown as under

Important Note:

A fixed amount is withdrawn by the partners, at equal time interval, say each month or each quarter. The calculation of total time period, in such situations will depend upon whether the money was withdrawn at the beginning of the month, middle of the month or at the end of the month.

Question 41: A and B are partners sharing profits equally. A drew regularly Rs. 4,000 in the beginning of every month for six months ended 30th September, 2023. Calculate interest on drawings @ 5% p.a. for a period of six months ended 30th September, 2023.

Answer:

Calculation of interest on drawings

Interest is chargeable on drawings is 5 % p.a

Interest on A’s drawings = Rs. 4,000 × 6 × 5/100 × 3.5/12

Interest on A’s drawings = Rs. 350

About Solution:

When a partner withdrawn an equal amount at the beginning of every month for the first six Months then interest on drawings is to be calculated for 3.5 months.

Things to Remember:

When a partner withdraws cash from the firm for domestic use, the withdrawal of cash is termed as drawings. If the partnership deed has a provision of charging interest on drawings, the firm may charge interest on drawings from partners. Interest on drawing is a gain for the firm. It is calculated at the agreed rate. The amount of interest on drawings will be credited to Profit and Loss Appropriation Account and will be debited to partner’s capital account/current account (Individually)

Important Note:

The journal entry will be:

Partner’s Capital/Current A/c Dr.

To Interest on Drawings A/c

(Charging interest on drawings to Partner’s Capital account)

Question 42: A and B are partners sharing profits equally. A drew regularly Rs. 4,000 at the end of every month for six months ended 30th September, 2023. Calculate interest on drawings @ 5% p.a. for a period of six months ended 30th September, 2023.

calculation of interest on drawings

Interest is chargeable on drawings is 5 % p.a

![]()

About Solution:

When a partner withdrawn an equal amount at the end of every month for the first six Months then interest on drawings is to be calculated for 2.5 months.

Things to Remember:

If the money is withdrawn by the partners in the beginning of each quarter, the interest is calculated on total money withdrawn during the year for an average period of seven and half months.

Important Note:

When the amounts are withdrawn at the end of each quarter the amount of interest is calculated on total drawings for a period of four and a half months.

Question 43: B and C are partners sharing profits equally. C regularly withdrew ₹ 5,000 per month in the beginning of the month for six months ended 30th September 2023. Calculate interest on drawings @ 12% p.a. for the year ended 31st March 2024.

Answer:

Question 44: Calculate interest on drawings of Sanjay @ 10% p.a. for the year ended 31st March, 2024, in each of the following alternative cases:

Case 1. If he withdrew Rs. 7,500 in the beginning of each quarter.

Case 2. If he withdrew Rs. 7,500 at the end of each quarter.

Case 3. If he withdrew Rs. 7,500 during the middle of each quarter.

Answer:

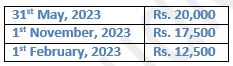

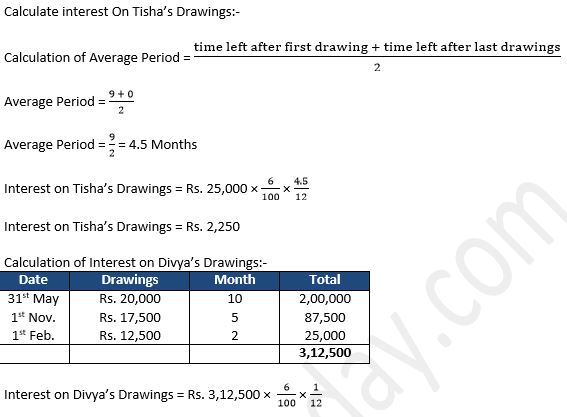

Question 45: The capital accounts of Tisha and Divya showed credit balances of ₹ 10,00,000 and ₹ 7,50,000 respectively after taking into account drawings and net profit of ₹ 5,00,000. The drawings of the partners during the year ended 31st March, 2024 were:

(i) Tisha withdrew ₹ 25,000 at the end of each quarter

(ii) Divya’s drawings were:

Calculate interest on partner’s Capitals @ 10% p.a. and interest on partner’s drawings @ 6% p.a. for the year ended 31st March 2024.

Answer:

Interest on Divya’s Drawings = Rs. 1,562.5 or Rs. 1,563 (round off)

Calculation of Interest on Tisha’s Capital:-

Opening Capital = Closing Capital + Drawings – Profit

Opening Capital = Rs. 10,00,000 + Rs. 1,00,000 – Rs. 2,50,000

Opening Capital = Rs. 8,50,000

Tishs’s Interest on Capital = Rs. 8,50,000 × 10%

Tishs’s Interest on Capital = Rs. 85,000

Calculation of Interest on Divya’s Capital :-

Opening Capital = Closing Capital + Drawings – Profit

Opening Capital = R. 75,000 + Rs. 50,000 – Rs. 2,50,000

Opening Capital = Rs. 5,50,000

Tishs’s Interest on Capital = 8,50,000 × 10%

Tishs’s Interest on Capital = 85,000

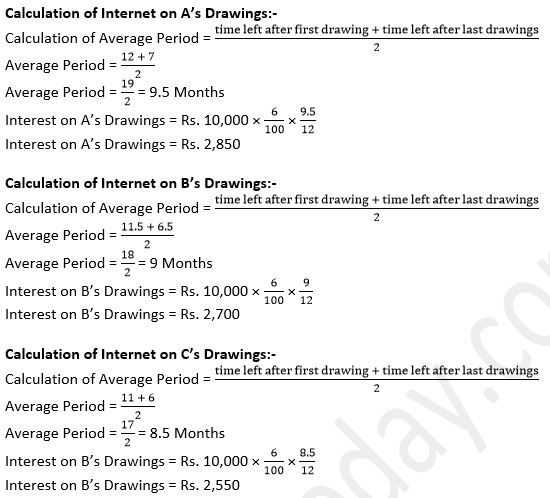

Question 46: A, B, and C are partners. During the year ended 31st March 2023, each of the partners withdrew ₹ 10,000 regularly. A withdrew in the beginning of the first 6 months of the year, B withdrew in the middle of the month for the first 6 months of the year and C withdrew at the end of the month for the first 6 months. Calculate interest on drawings @ 6% p.a. for the year ended 31st March 2023.

Answer:

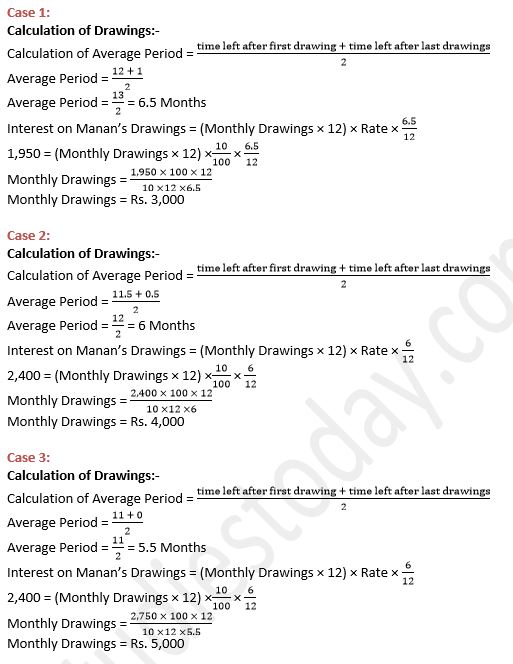

Question 47: Calculate the amount of Manan’s monthly drawings for the year ended 31st March, 2024, in the following alternatives cases when Partnership Deed allows interest on drawings @ 10% p.a.:

(i) If interest on drawings is ₹ 1,950 and he withdrew a fixed amount in the beginning of each month.

(ii) If interest on drawings is ₹ 2,400 and he withdrew a fixed amount in the middle of each month.

(iii) If interest on drawings is ₹ 2,750 and he withdrew a fixed amount at the end of each month.

Answer:

Question 48: Calculate the amount of Shiv’s quarterly drawings for the year ended 31st March 2024, in the following alternative cases when Partnership Deed allows interest on drawings @ 12% p.a.:

(i) If interest on drawings is ₹ 1,500 and he withdrew a fixed amount in the beginning of each quarter.

(ii) If interest on drawings is ₹ 1,200 and he withdrew a fixed amount in the middle of each quarter.

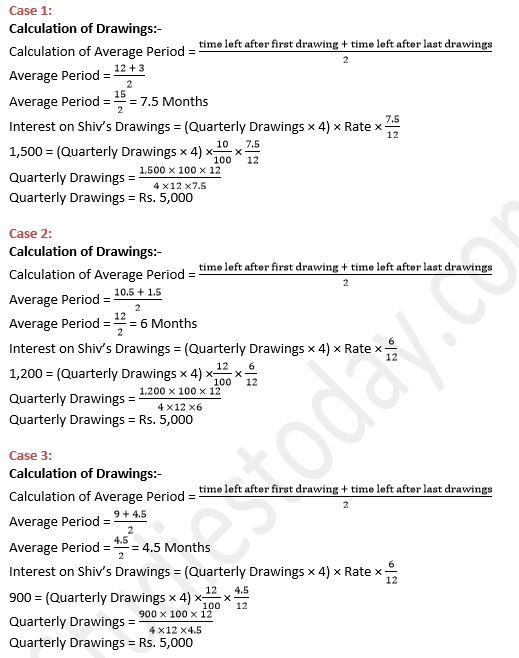

(iii) If interest on drawings is ₹ 900 and he withdrew a fixed amount at the end of each quarter.

Answer:

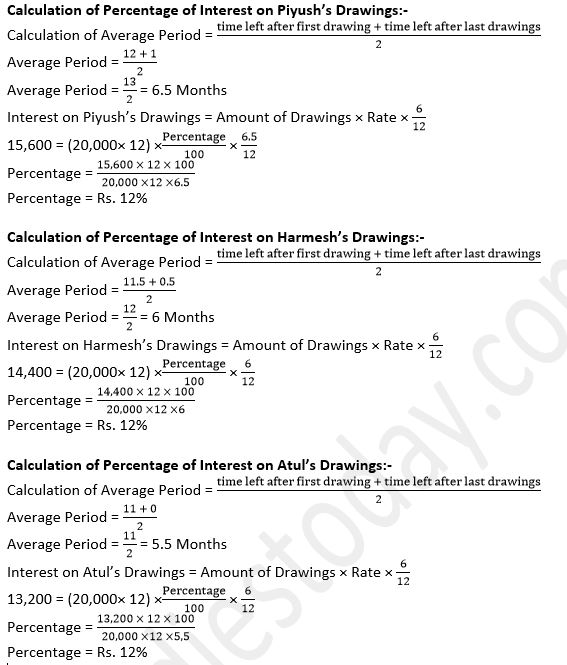

Question 49: Piyush, Harmesh, and Atul are partners. Each partner regularly withdrew ₹ 20,000 per month is given below.

a) Piyush withdrew in the beginning of the month;

b) Harmesh withdrew in the middle of the month; and

c) Atul withdrew at the end of the month.

Interest on drawings charged for the year ended 31st March 2023 was ₹ 15,600, ₹ 14,400, and ₹ 13,200 respectively.

Determine the rate of interest charged on drawings.

Answer:

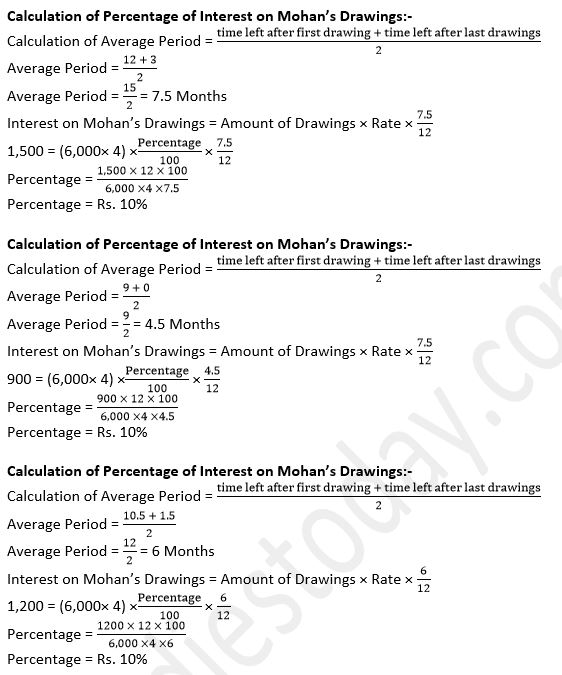

Question 50: Calculate the Rate of interest on Drawings of Mohan in the following cases:

a) If he withdrew ₹ 6,000 in the beginning of each quarter for the year ended 31st March 2023 and interest on drawings is ₹ 1,500.

b) If he withdrew ₹ 6,000 at the end of each quarter for the year ended 31st March 2023 and interest on drawings is ₹ 900.

c) If he withdrew ₹ 6,000 per quarter for the year ended 31st March 2023 and interest on drawings is ₹ 1,200.

Answer:

Question 51: Amit and Vijay started a partnership business on 1st April 2022. Capital invested by them were ₹ 2,00,000 and ₹ 1,50,000 respectively. The partnership deed provided as follows:

(a) Interest on Capital be allowed @ 10% p.a.

(b) Amit to get a salary of ₹ 2000 per month and Vijay ₹ 3000 per month.

(c) Profits are to be shared in the ratio of 3 : 2.

Net Profit for the year ended 31st March 2023 was ₹ 2,16,000. Interest charged on drawings was ₹ 2,200 for Amit and ₹ 2,500 for Vijay.

Prepare Profit and Loss Appropriation Account.

Answer:

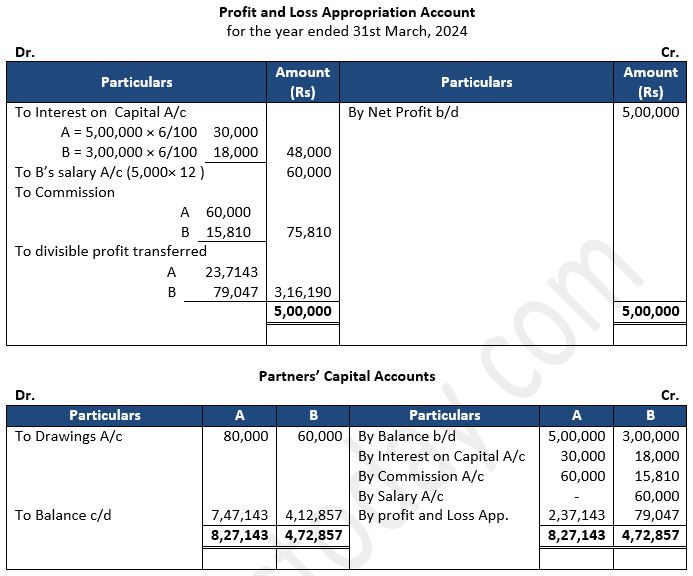

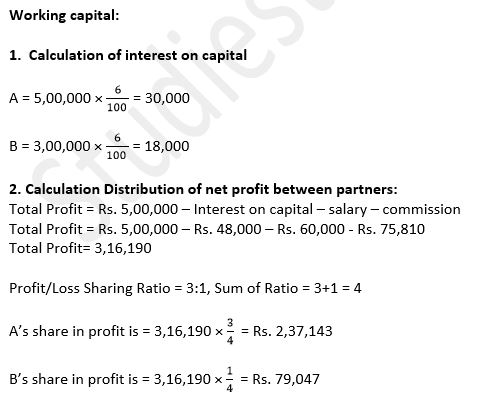

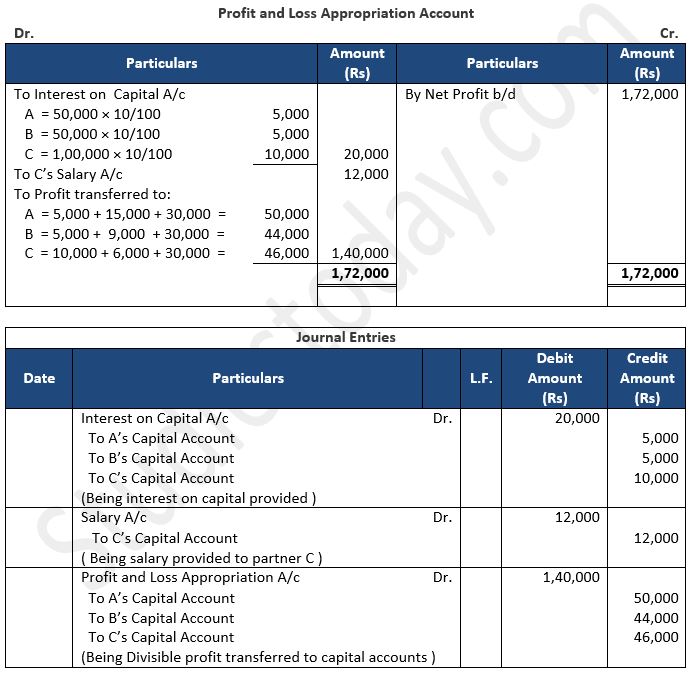

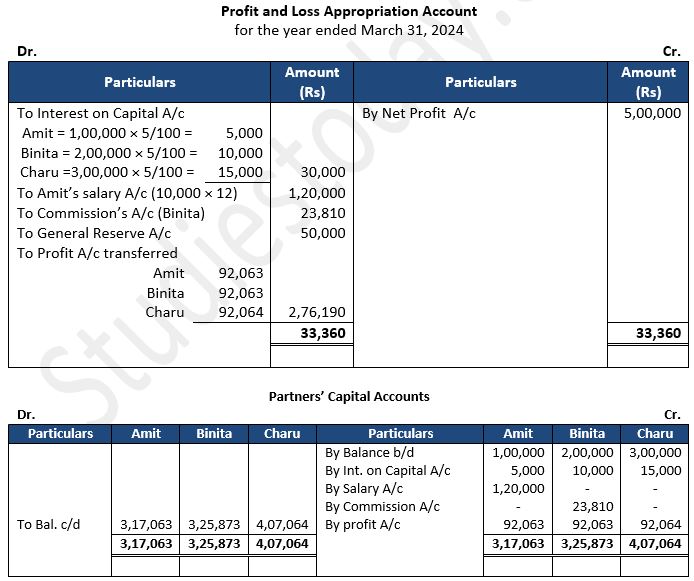

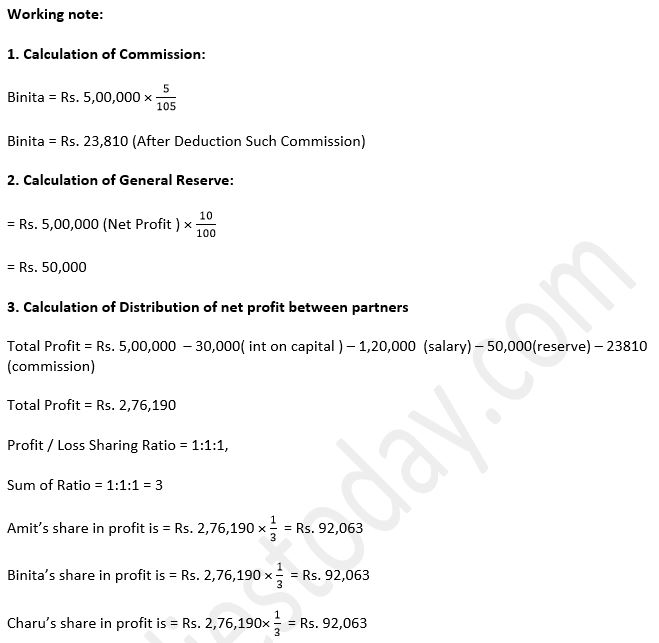

Question 52: A and B are partners sharing profits and losses in the ratio of 3:1. On 1st April, 2023, their capitals were: Rs. 5,00,000 and B Rs. 3,00,000. During the year ended 31st March, 2024 they earned a net profit of Rs. 5,00,000. The terms of partnership are:

(a) Interest on capital is to allowed @ 6% p.a.

(b) A will get a commission @ 2% on net sales.

(c) B will get a salary of Rs. 5,000 per month.

(d) B will get commission of 5% on profits after deduction of all expenses including such commission.

Partners' drawings for the year were: A Rs. 80,000 and B Rs. 60,000. Net Sales for the year was Rs. 30,00,000. After considering the above facts, you are required to prepare Profit and Loss Appropriation Account and Partners' Capital Accounts.

Answer:

About Solution:

In the absence of information, manager’s commission will be calculated on profit before any adjustment is made according to partnership deed i.e. before adjustment in respect of partner’s salary interest of capital etc.

Things to Remember: