Read DK Goel Solutions Class 12 Accountancy Chapter 3 Admission of a Partner 2026. Students should study DK Goel Solutions Class 12 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 12 Accountancy have been prepared by expert teachers. These DK Goel Class 12 Solutions have been designed as per the latest accountancy DK Goel Book for Class 12 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 12 Accounts Chapter 3 Admission of a Partner DK Goel Solutions

DK Goel Solutions for Chapter 3 Admission of a Partner Class 12 Accounts have been provided below based on the latest DK Goel Class 12 book. The answers have been prepared based on the latest 2026 book for the current academic year. DK Goel Solutions Class 12 will help students to improve their concepts and easily solve accountancy questions for Class 12.

Chapter 3 Admission of a Partner DK Goel Class 12 Solutions

Short Answer Questions

Question 1.

Solution 1 Below are the matters that need adjustments at the time of admission of a partner:-

(i) Adjustment of Accumulated Profit, Reserves and Losses.

(ii) Adjustment of Goodwill.

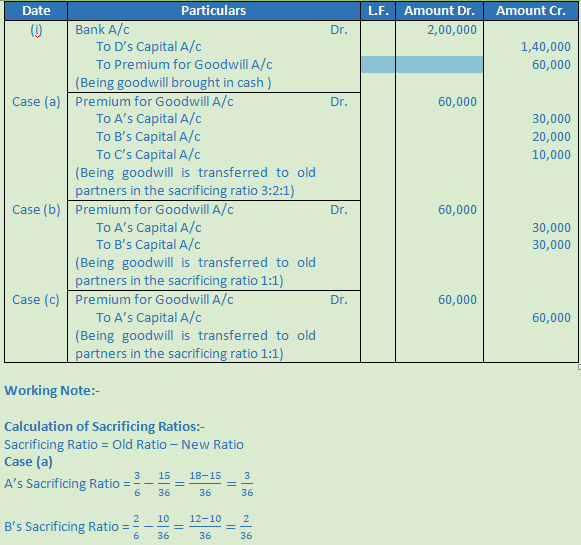

Question 2.

Solution 2

(i) For bringing goodwill in cash:

Bank A/c Dr.

To Premium for goodwill A/c

(ii) For distributing the amount of goodwill brought in by new partner;

Premium for goodwill A/c Dr.

To Sacrificing Partner’s Capital A/c (in sacrificing ratio)

Question 3.

Solution 3

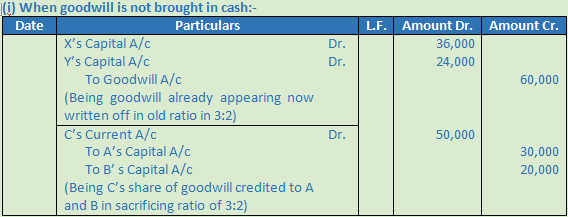

(i) For writing off the goodwill account already appearing in the book:

Old Partner’s Capital A/c Dr.

To Goodwill A/c

(ii) For bringing goodwill in cash:

Bank A/c Dr.

To Premium for goodwill A/c

(iii) For distributing the amount of goodwill brought in by new partner;

Premium for goodwill A/c Dr.

To Sacrificing Partner’s Capital A/c (in sacrificing ratio)

Question 4.

Solution 4 New Partner’s Current A/c Dr. (with his share of goodwill)

To Sacrificing Partner’s Capital A/c (in sacrificing ratio)

Question 5.

Solution 5 The value of goodwill is hidden in the question. In Such cases, The amount of goodwill is calculated on the basis of total capital of the firm and the profit sharing ratio of the partners.

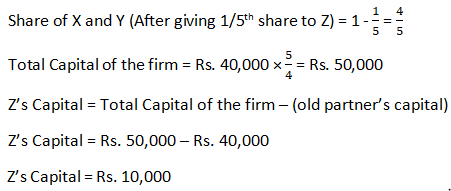

For example: X and Y are partners with capitals of Rs. 30,000 and Rs. 20,000 respectively. They admit Z as a partner with 1/4th share. Z is to contribute Rs. 24,000 as his capital. In such a case, the total capital of the firm, based on Z’s share ought to be Rs. 24,000 × 4/1 = Rs. 96,000. But the combined capital of X, Y and Z becomes only Rs. 74,000 (Rs. 30,000 + Rs. 20,000 + Rs. 24,000). As such the value of total goodwill of the firm should be taken as Rs. 96,000 – Rs. 74,000 = Rs. 22,000.

Question 6.

Solution 6 When a new partner is admitted, assets are revalued and liabilities are reassessed so that the gain or loss arising on account of such revaluation up to the date of admission of a new partner may be ascertained and adjusted in the Old partners’ Capital Account in their old profit-sharing ratio and the new partner should neither gain nor suffer because of change in the value of assets or amount of liabilities.

Question 7.

Solution 7 Sometimes the capital of the new partner is not given in the question. He may be required to bring in proportionate capital. In such cases the new partner’s capital will be calculated on the basis of the capitals of the old partners remaining after all adjustments and revaluation.

For example:- The capital of X and Y after all the adjustments and revaluations are Rs. 24,000 and Rs. 16,000 respectively. They admitted Z as a new partner with 1/5th share in the profits. Z’s Capital will be calculated as:

Question 8.

Solution 8 Puja must have given the argument that in the absence of Partnership deed partnership Act 1932 prevails, which have convinced Disha and Gayatri.

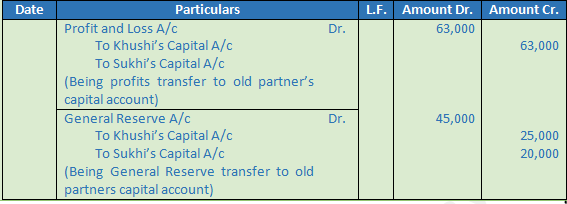

Question 9.

Solution 9 Mohan and Naresh would have given the argument that General Reserve came into existence when Om was not a partner. Hence, it should be shared only by Mohan and Naresh in their old profit sharing ratio.

Question 10.

Solution 10 Dushaynt would have given the argument that the liability belonged to the period when he was not a partner. Hence, it should be borne by old partners in their old profit sharing ratio.

Numerical Questions

Question 1.(A)

Solution .1 (A)

Question 1. (B)

Solution .1 (B)

Question 2. (A)

Solution .2 (A)

Question 2. (B)

Solution .2 (B)

Question 2. (C)

Solution .2 (C)

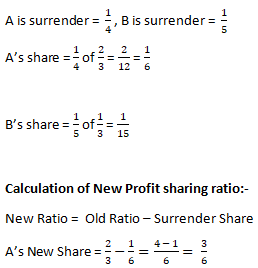

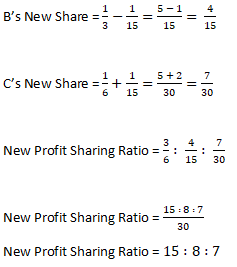

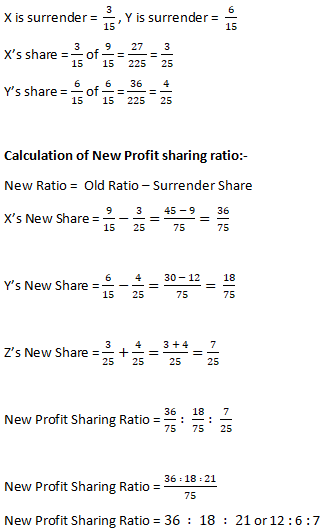

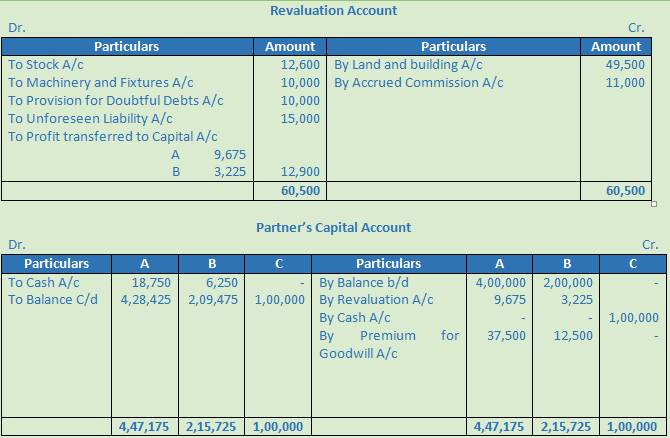

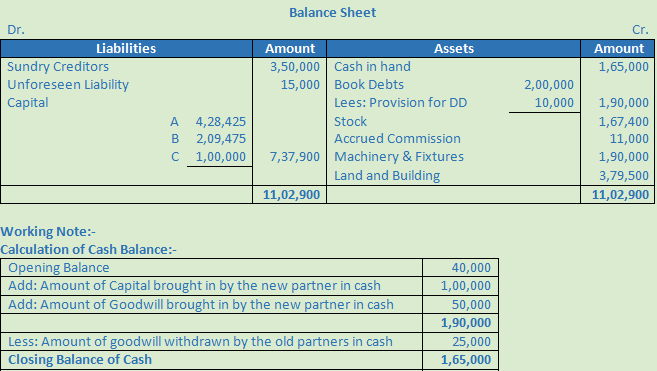

Question 3.

Solution .3

Question 4. (A)

Solution .4 (A)

Question 4. (B)

Solution .4 (B)

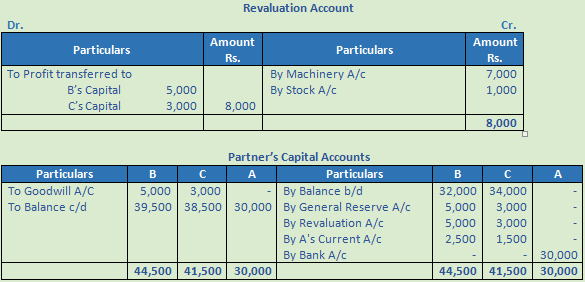

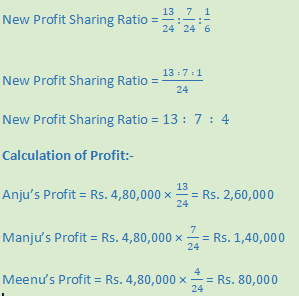

Question 5.

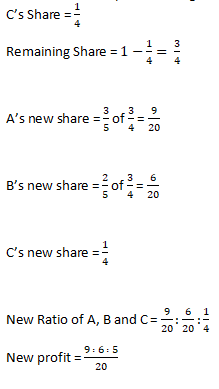

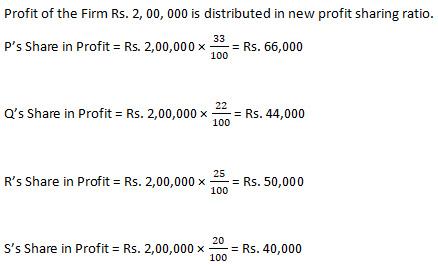

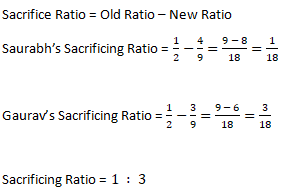

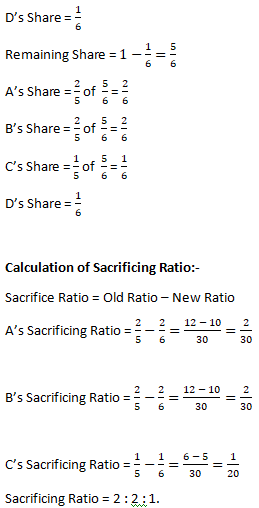

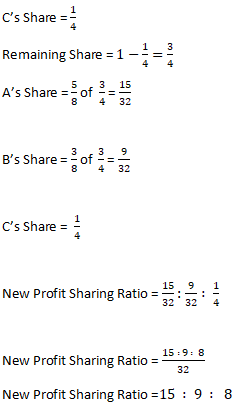

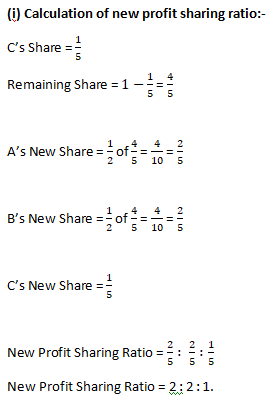

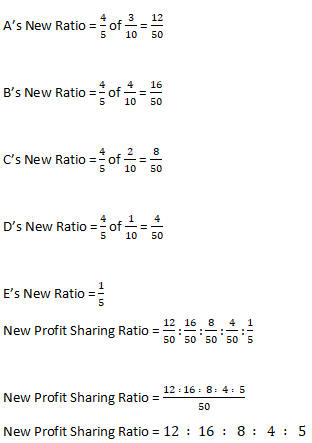

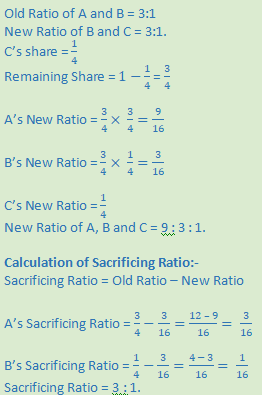

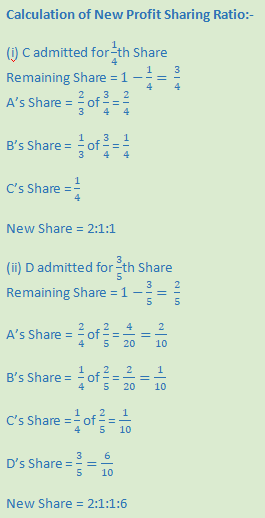

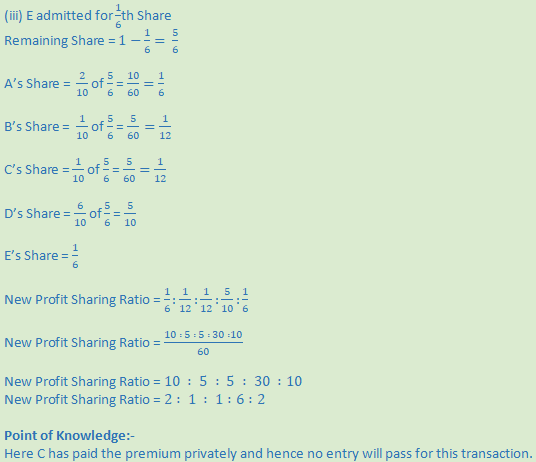

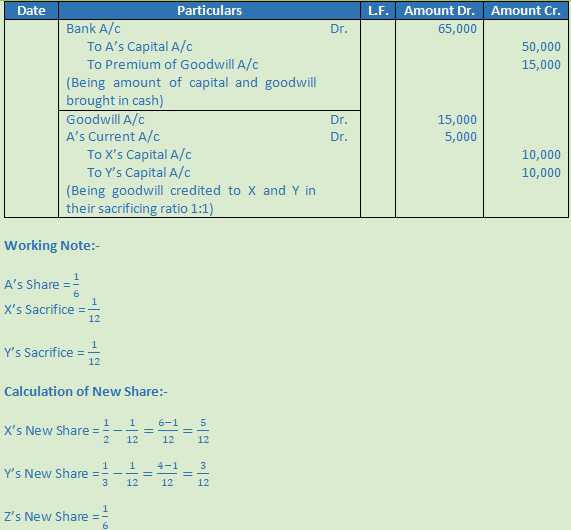

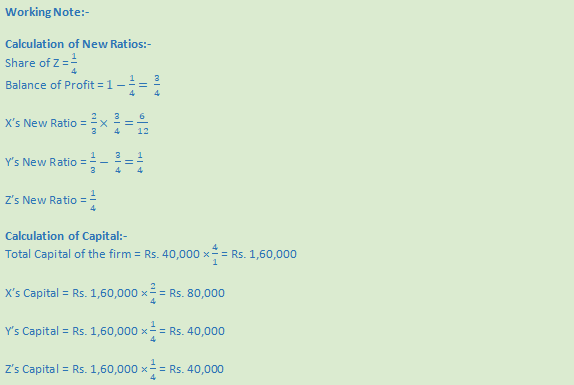

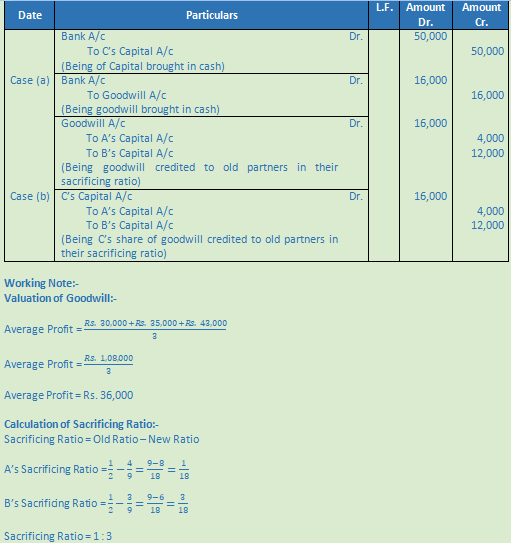

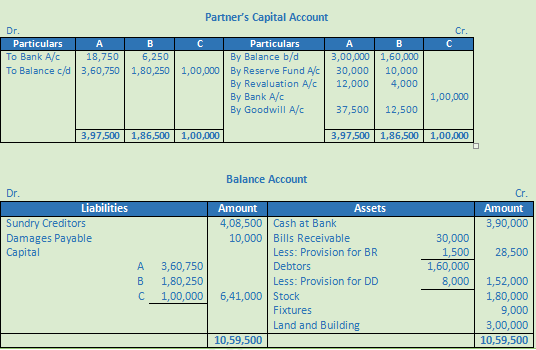

Solution 5. Profit Sharing ratio of A, B and C = 1 : 2 : 3.

D’s Share = 1/6

Question 6.

Solution .6

Question 7.

Solution .7

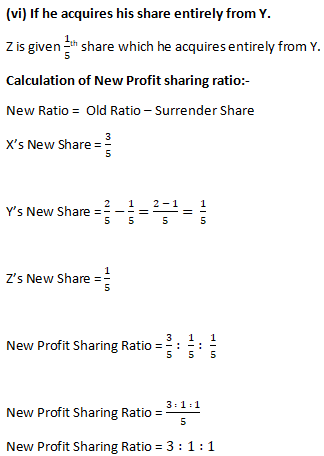

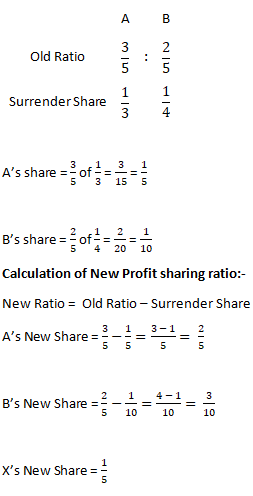

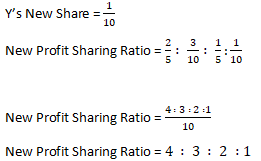

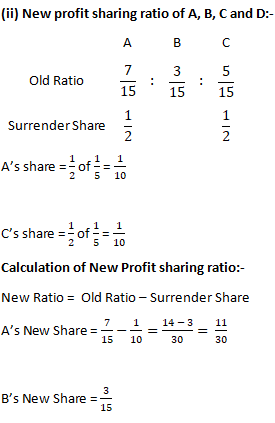

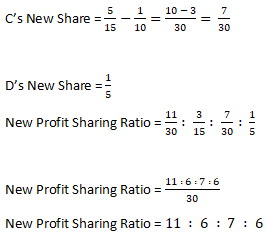

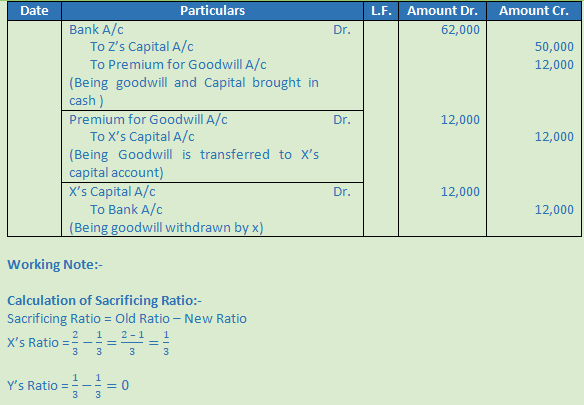

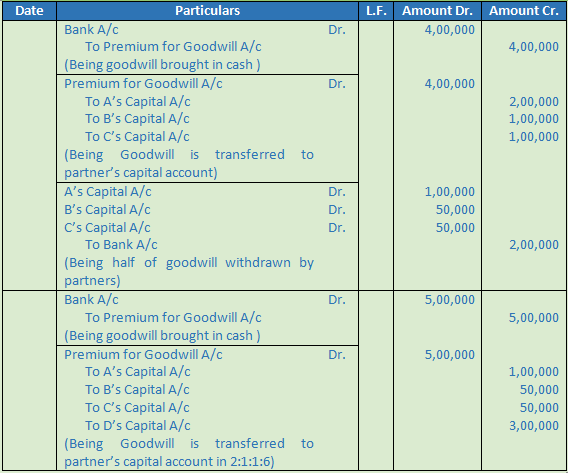

Question 8 A (new).

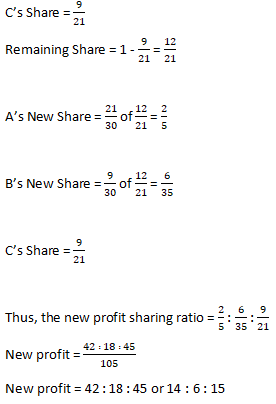

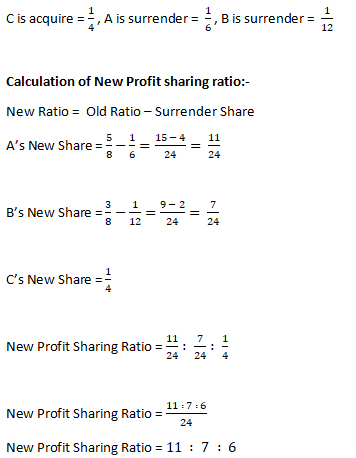

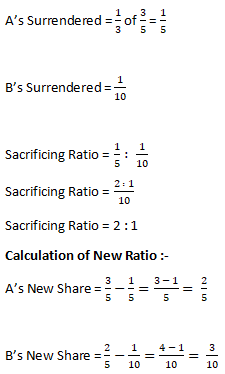

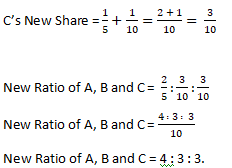

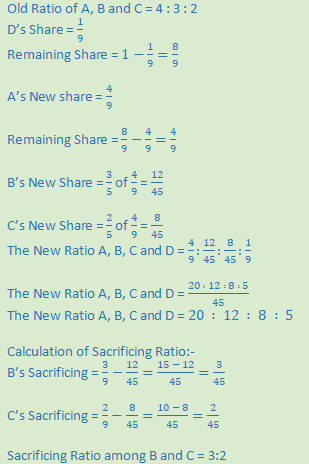

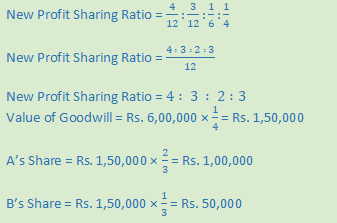

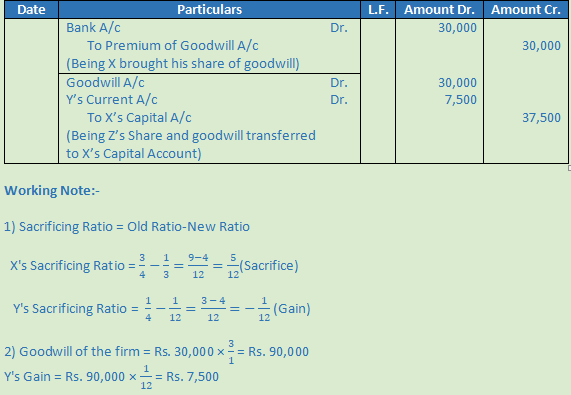

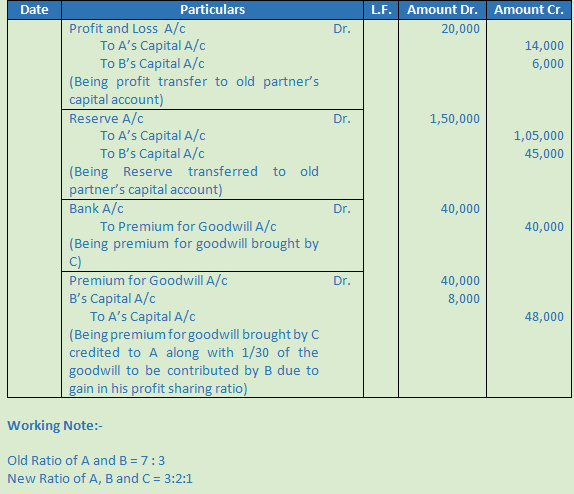

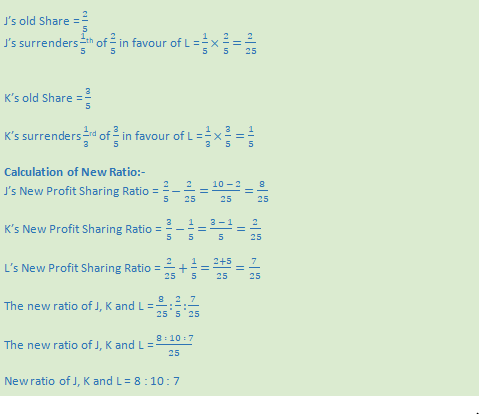

Question 8. (A) A and B are partners in a firm sharing profits in the ratio of 2:1. C joins the firm. A surrenders 1/4th of his share and B 1/5th of his share in favour of C. Find the new profit sharing ratio.

Solution 8 (A)

Question 8. (B)

Solution .8 (B)

Question 8. (C)

Solution .8 (C)

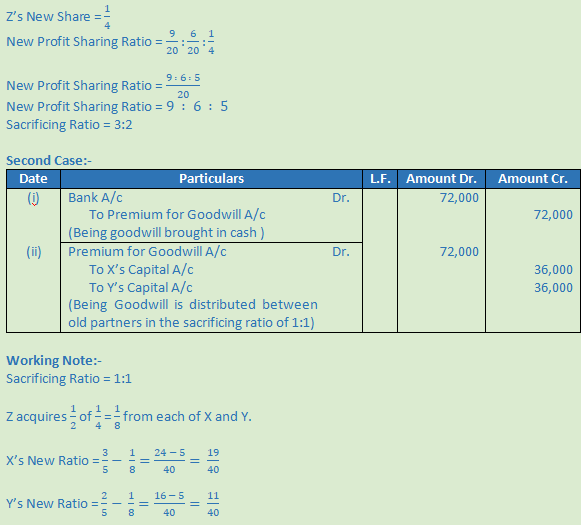

Question 9.

Solution .9

Question 10.

Solution .10

Question 11.

Solution .11

Question 12.

Solution .12

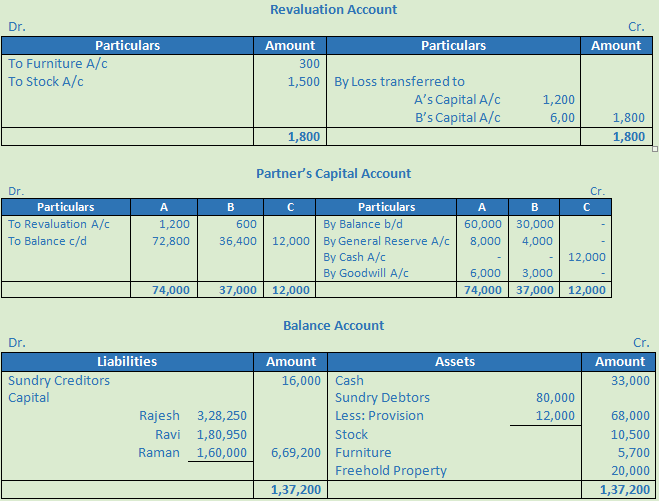

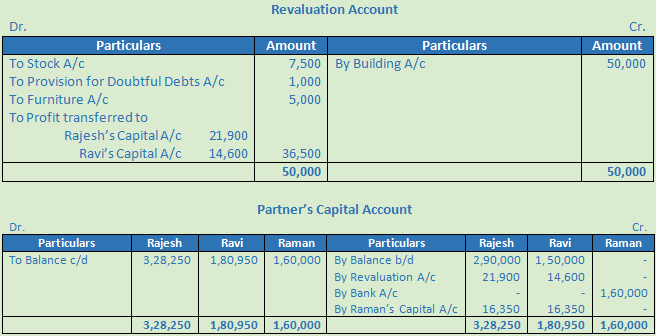

Question 13. (A)

Solution .13 (A)

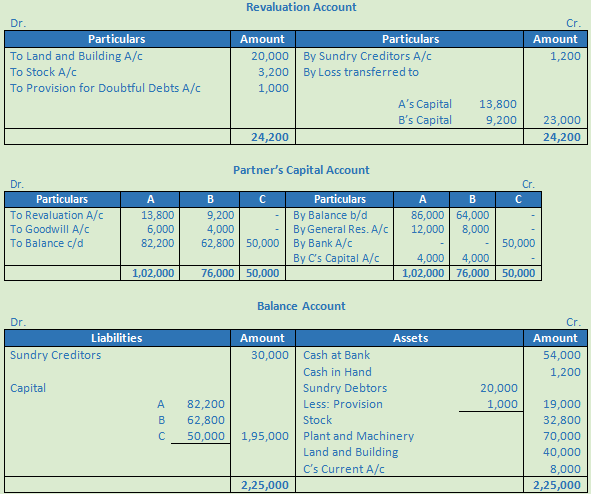

Question 13. (B)

Solution .13 (B)

Question 14. (A)

Solution .14 (A)

Question 14. (B)

Solution .14 (B)

Question 15.

Solution .15

Question 16. (A)

Solution .16 (A)

Question 16. (B)

Solution .16 (B)

Question 17.

Solution .17

Question 18.

Solution .18

Question 19.

Solution .19

Question 20.

Solution .20

Question 21.

Solution .21

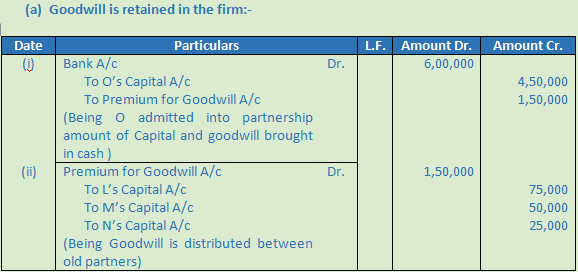

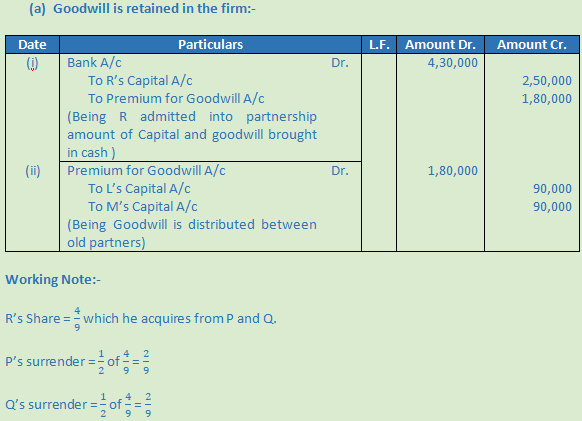

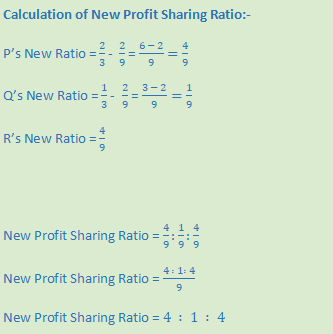

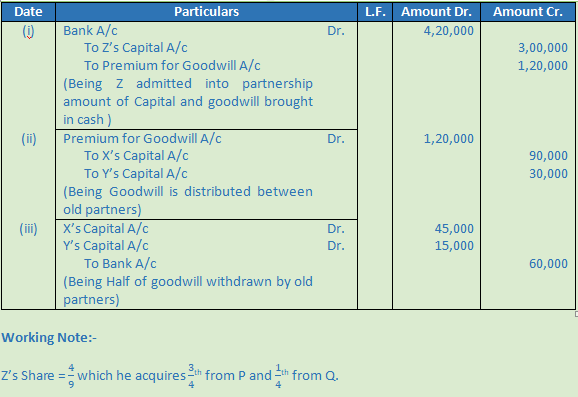

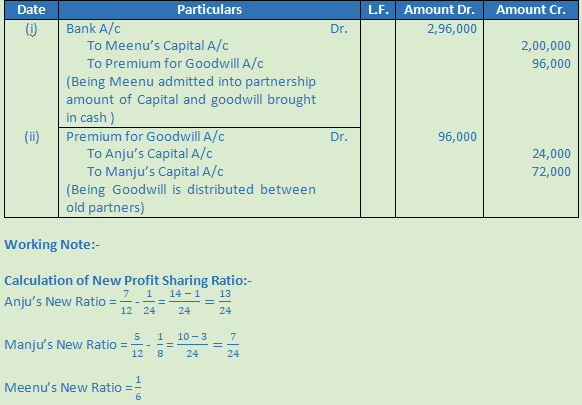

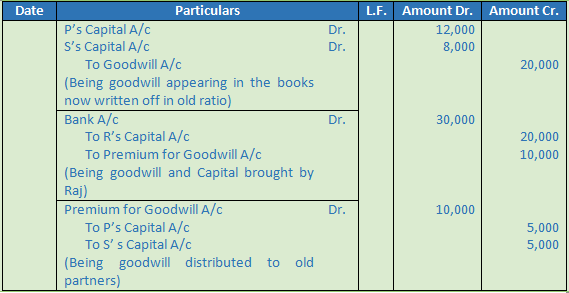

(a) Goodwill is retained in the firm:-

Question 22.

Solution .22

Question 23.

Solution .23

Question 24.

Solution .24

Question 25.

Solution .25

Question 26.

Solution .26

Question 27.

Solution .27

Question 28.

Solution .28

Question 29.

Solution .29

Question 30.

Solution .30

Question 31.

Solution .31

Question 32.

Solution .32

Question 33.

Solution .33

Question 34.

Solution .34

Question 35.

Solution .35

Question 36.

Solution .36

Question 37. (A)

Solution .37 (A)

Question 37. (B)

Solution .37 (B)

Question 37. (C)

Solution .37 (C)

Question 38.

Solution .38

Question 39.

Solution .39

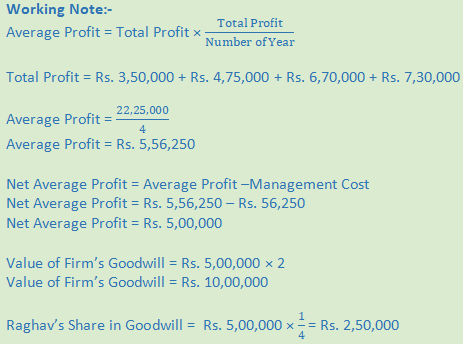

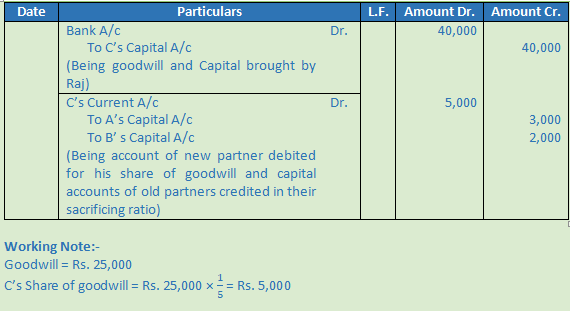

Question 40 (new).

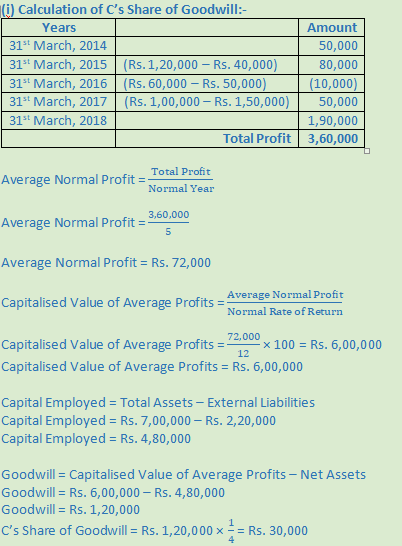

Solution (new). Profit of year 2014 = Rs. 50,000

Profit of year 2015 = Rs. 1,20,000 – Rs. 40,000 = Rs. 80,000

Profit of year 2016 = (Rs. 60,000) + Rs. 50,000 = (Rs. 10,000)

Profit of year 2017 = (Rs. 1,00,000) + (Rs. 1,50,000) = Rs. 50,000

Profit of year 2018 = Rs. 1,90,000

Total Profit = Rs. 50,000 + Rs. 80,000 – Rs. 10,000 + Rs. 50,000 + Rs. 1,90,000

Total Profit = Rs. 3,60,000

Average Profit = (Total Profit )/(Number of Years)

Average Profit = 3,60,000/5

Average Profit = Rs. 72,000

Net Assets = Assets - Liabilities

Net Assets = 7,00,000 – 2,20,000

Net Assets = 4,80,000

Capitalised Value = Average Profits × 100/(Normal rate of return)

Capitalised Value = Rs. 72000 × 100/12

Capitalised Value = Rs. 6,00,000

Calculation of Goodwill:-

Goodwill = Capitalised Value - Net Assets

Goodwill = Rs. 6,00,000 – Rs. 4,80,000

Goodwill = Rs. 1,20,000

a) C’s Goodwill = Rs. 1,20,000 × 1/4 = Rs. 30,000

Question 40.

Solution .40

Question 41.

Solution .41

Question 42.

Solution .42

Question 43.

Solution .43

Question 44.

Solution .44

Question 45.

Solution .45

Question 46.

Solution .46

Question 47.

Solution .47

Question 48.

Solution .48

Question 49.

Solution .49

Question 50.

Solution .50

Question 51.

Solution .51

Question 52.

Solution .52

Question 53.

Solution .53

Question 54.

Solution .54

Question 55.

Solution .55

Question 56.

Solution .56

Question 57.

Solution .57

Question 58.

Solution .58

Question 59. (A)

Solution .59 (A)

Question 59. (B)

Solution .59 (B)

Question 60.

Solution .60

Question 61.

Solution .61

Question 62.

Solution .62

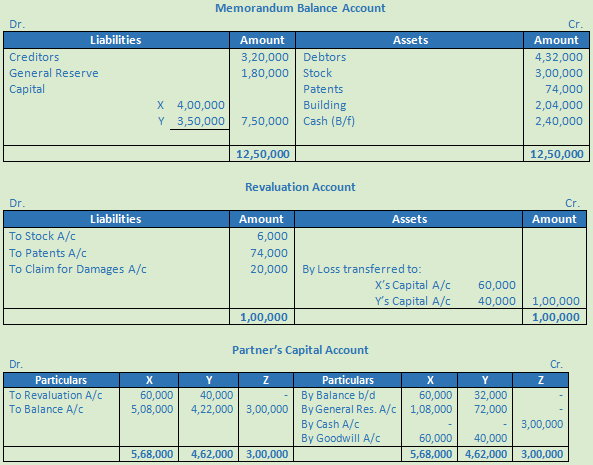

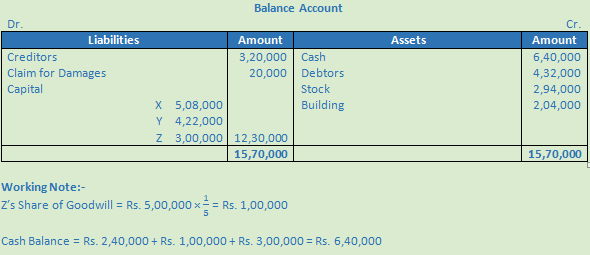

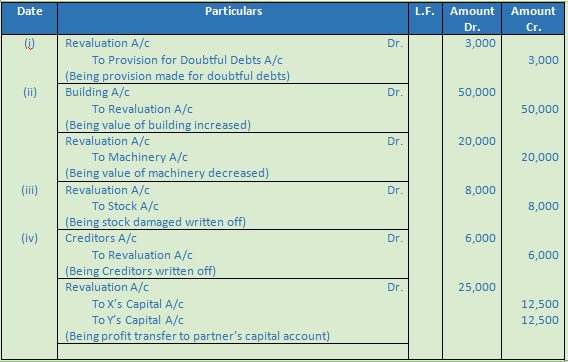

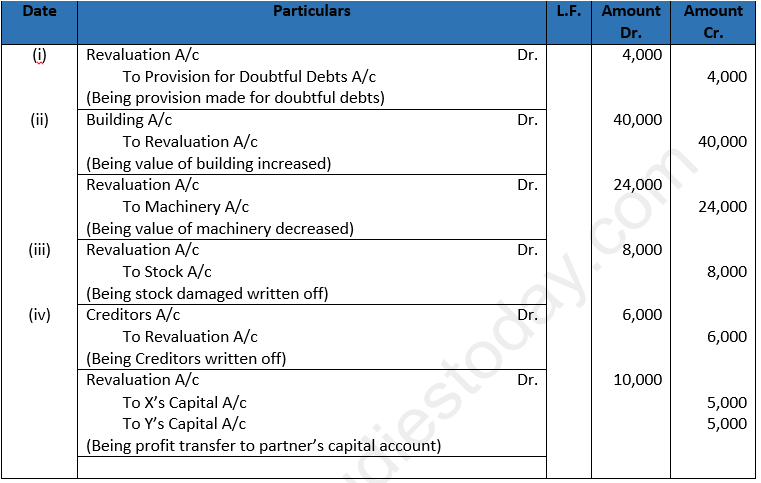

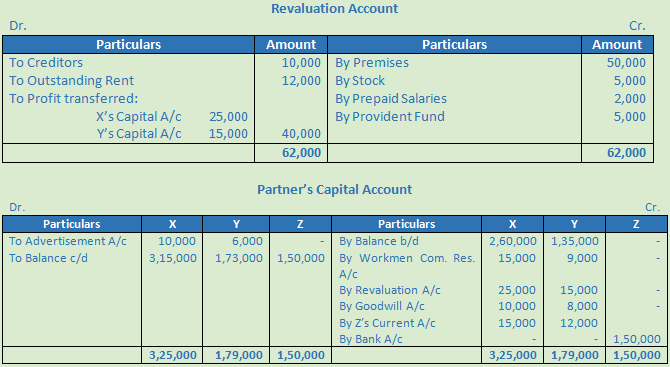

Question 63 (new).

Solution 63 (new).

Question 63.

Solution .63

Question 64.

Solution .64

Question 65.

Solution .65

Question 66.

Solution .66

Question 67.

Solution .67

Question 68. (A)

Solution .68 (A)

Question 68. (B)

Solution .68 (B)

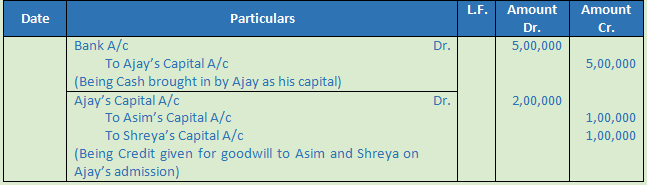

Question 69.

Solution .69

Working Note:-

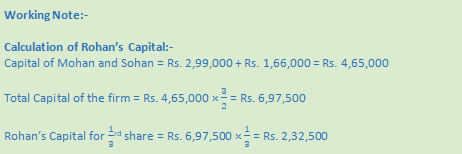

Calculation of Hidden Goodwill

Net Worth = Sundry Assets – Outside Liabilities

Net Worth = Rs. 15,00,000 – Rs. 5,00,000

Net Worth = Rs. 10,00,000

Net Worth = Rs. 10,00,000 + Rs. 5,00,000 = Rs. 15,00,000

Total Capital of the firm based on Ajay’s Capital = 5,00,000 ×5/1 = Rs. 25,00,000

Goodwill of the firm = Rs. 25,00,000 – Rs. 15,00,000 = Rs. 10,00,000

Hidden Goodwill = Goodwill of the firm – Showing in P & L

Hidden Goodwill = Rs. 10,00,000

Ajay’s Share of Goodwill = Rs. 10,00,000 ×1/5 = 2,00,000

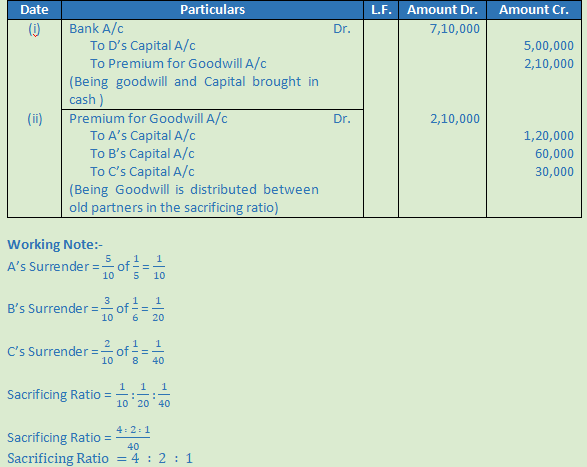

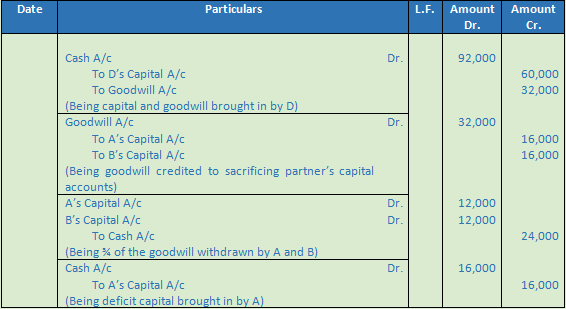

Question 70.

Solution .70

Working Note:-

Calculation of Hidden Goodwill

Net Worth = Rs. 3,00,000 + Rs. 2,00,000 + Rs. 1,80,000 + Rs. 2,00,000

Net Worth = Rs. 8,80,000

Total Capital of the firm based on D’s Capital = 2,00,000 × 5/1 = Rs. 10,00,000

Hidden Goodwill = Rs. 10,00,000 – Rs. 8,80,000 = Rs. 1,20,000

D’s Share of Goodwill = Rs. 1,20,000 ×1/5 = 24,000

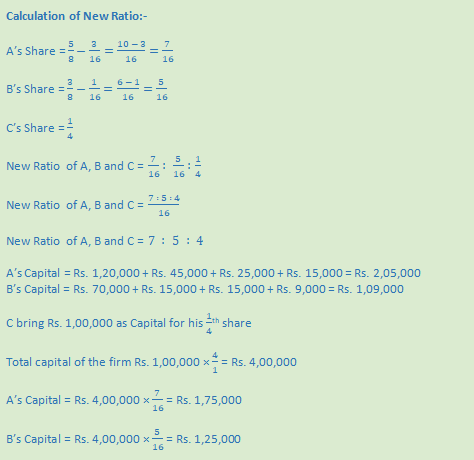

Question 71.

Solution .71

Question 72.

Solution .72

Question 73.

Solution .73

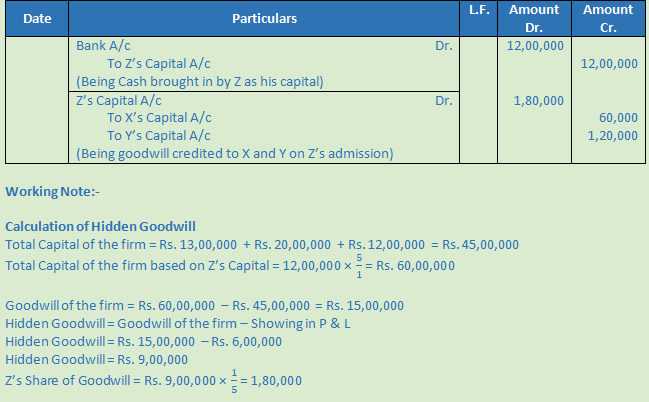

Question 74 (new).

Solution (new). Calculation of Hidden Goodwill of the firm:

Total Capital of the firm based on new partner’s capital: Rs. 1,50,000 × 10/1 = 15,00,000

Less: Net worth of the business:

Adjusted Capital of all the partners

(Capital + Workmen Compensation Reserve + Creditors)

A = 5,00,000 + (12,000) + (18,000) + 36,000 = 5,06,000

B = 4,00,000 + (6,000) + (9,000) + 18,000 = 4,03,000

C = 2,00,000 + (2,000) + (3,000) + 6,000 = 2,01,000

D = 1,50,000

Net worth of the business = Rs. 5,06,000 + Rs. 4,03,000 + Rs. 2,01,000 + Rs. 1,50,000 = 12,60,000

Hidden Goodwill = Rs. 15,00,000 – Rs. 12,60,000

Hidden Goodwill = Rs. 2,40,000

D’s Share of Goodwill = Rs. 2,40,000 × 1/10 = Rs. 24,000

Question 74.

Solution .74

Question 75. (A)

Solution .75 (A)

Question 75. (B)

Solution .75 (B)

Question 76.

Solution .76

Question 77.

Solution .77

Question 78.

Solution .78

Question 79.

Solution .79

Question 80.

Solution .80

Question 81.

Solution .81

Question 82.

Solution .82

Question 83.

Solution .83

Question 84.

Solution .84

Question 85.

Solution .85

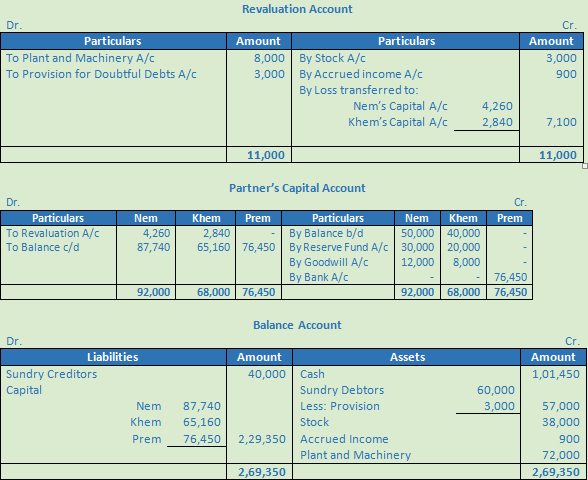

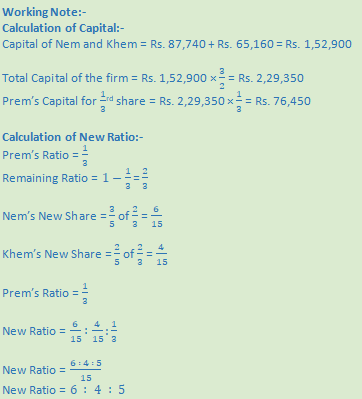

Question 86.

Solution .86

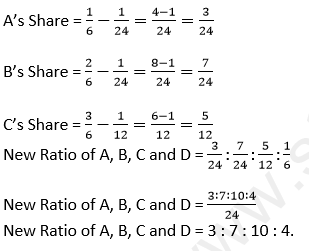

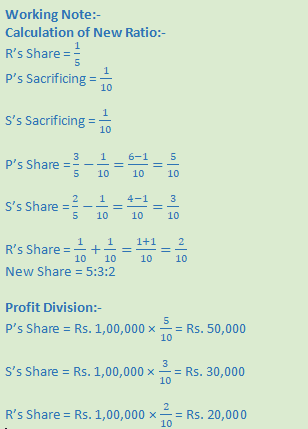

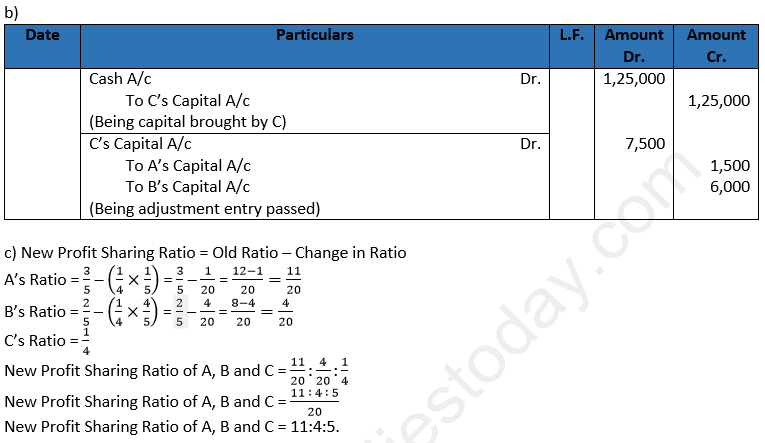

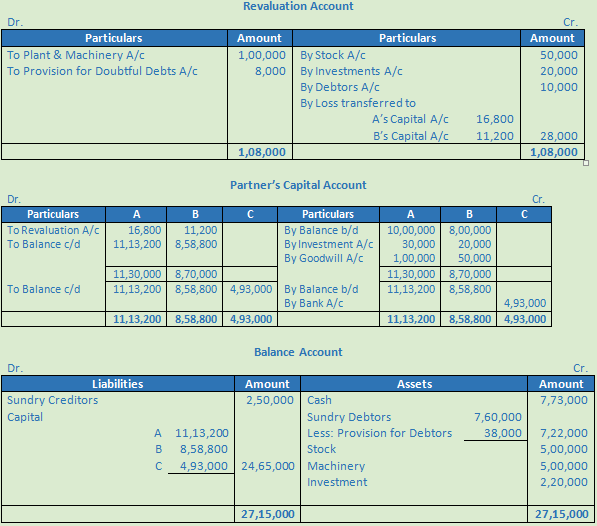

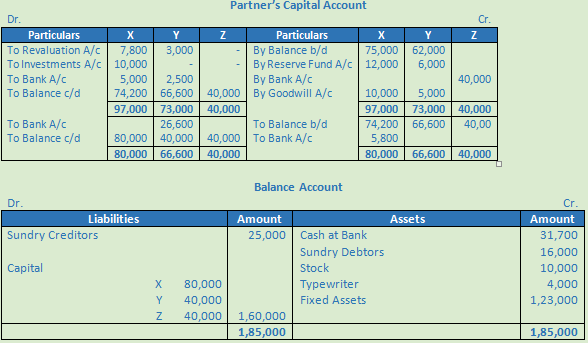

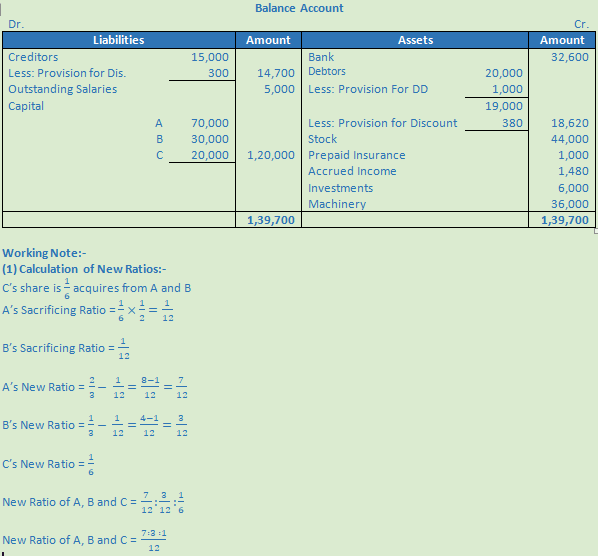

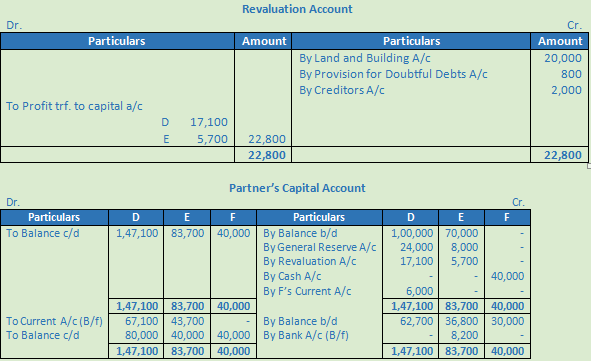

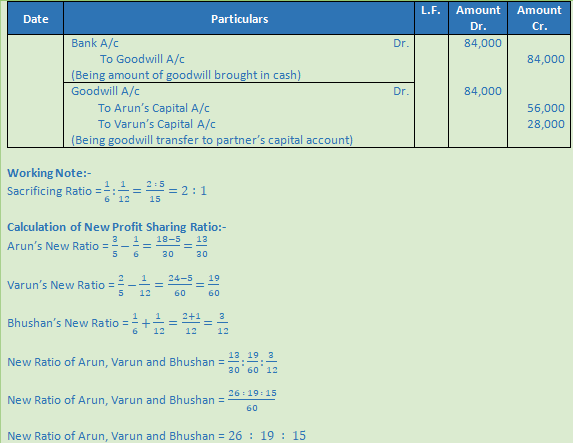

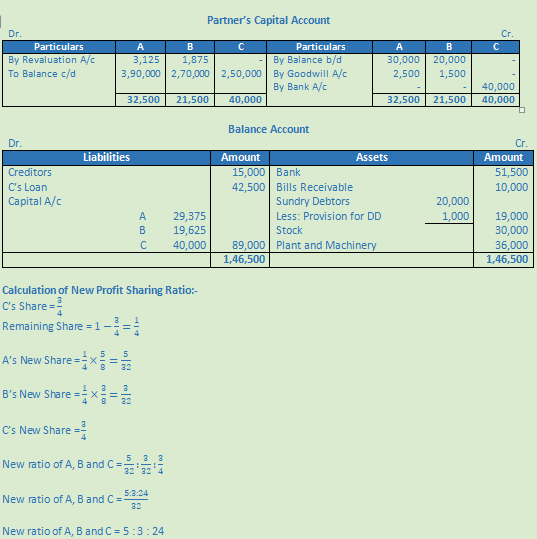

New Ratio of A, B and C =

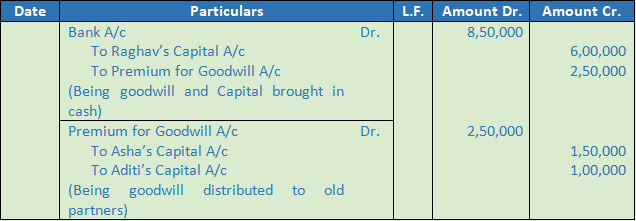

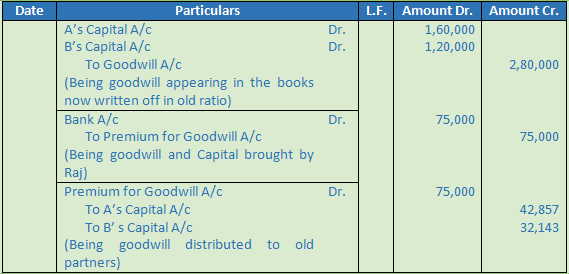

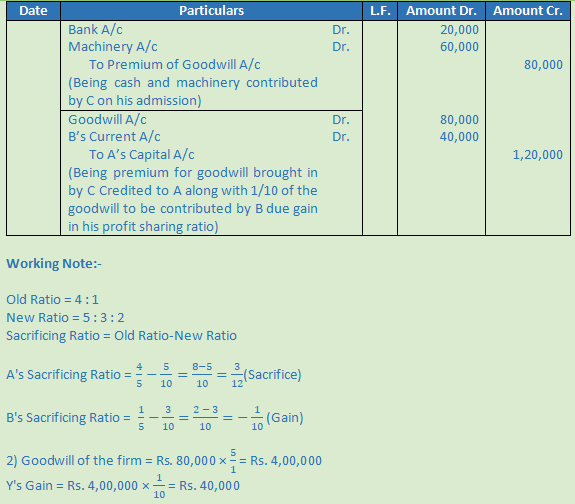

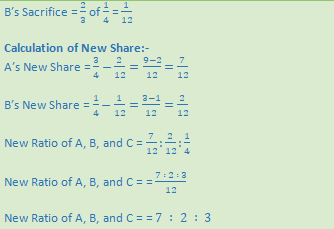

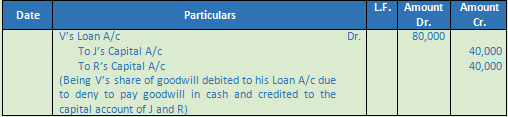

(2) A’s Capital should be Rs. 70,000 whereas his existing capital is only Rs. 66,000. He will be bring Rs. 70,000 – Rs. 66,600 = Rs. 3,400

(3) B’s Capital should be Rs. 30,000 whereas his existing capital is only Rs. 43,800. He will be bring Rs. 43,800 – Rs. 30,000 = Rs. 13,800 will be refunded.

Question 87.

Solution .87

Question 88.

Solution .88

Question 89. (A)

Solution .89 (A)

Question 89. (B)

Solution .89 (B)

Question 89. (C)

Solution .89 (C)

Question 90. (A)

Solution .90 (A)

Question 90. (B)

Solution .90 (B)

Question 91.

Solution .91

Question 92.

Solution .92

Question 93.

Solution .93

Question 94.

Solution .94

Question 95.

Solution .95

Question 96.

Solution .96

Question 97.

Solution .97

Question 98.

Solution .98

Question 99.

Solution .99

Question 100.

Solution .100

Question 101.

Solution .101

Question 102 (new).

Solution .102

2016-17 | 90,000 |

2017-18 | 1,30,000 |

2018-19 | 86,000 |

During the year 2018-19 there was a loss of Rs. 20,000 due to fire which was not accounted for while calculating the profit.

Calculate the value of goodwill and pass the necessary journal entries for the treatment of goodwill

Working Note:-

Calculation of Average Profit:-

Average Profit = (90,000 + 1,30,000 + 86,000)/3

Average Profit = (90,000 + 1,30,000 + 86,000)/3

Average Profit = 3,06,000/3

Average Profit = Rs. 1,02,000

Calculation of Goodwill:-

Goodwill of the firm = Average Profits × Number of Years’ Purchase

Goodwill of the firm = Rs. 1,02,000 × 2

Goodwill of the firm = Rs. 2,04,000

Manik’s Goodwill = Rs. 2,04,000 × 1/4 = Rs. 51,000

Question 102.

Solution .102

Question 103.

Solution .103

Question 104.

Solution .104

Question 105.

Solution .105

Question 106.

Solution .106

Question 107.

Solution .107

Question 108.

Solution .108

Question 109.

Solution .109

Question 110.

Solution .110

Question 111.

Solution .111

Question 112.

Solution .112

Question 113.

Solution .113

Question 114.

Solution .114

Question 115.

Solution .115

Question 116.

Solution .116

Question 117.

Solution .117

Question 118.

Solution .118

Question 119.

Solution .119

Question 120.

Solution .120

Working Note:-

Calculation of Goodwill :-

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 2,20,000 – Rs. 1,40,000

Super Profit = Rs. 80,000

Goodwill = Super profit × No. of Year Purchases

Goodwill = Rs. 80,000 × 4

Goodwill = Rs. 3,20,000

C’s Share = Rs. 3,20,000 × 1/4 = Rs. 80,000

Question 121.

Solution .121

Question 122 (new).

Solution 122 (new).

Question 122.

Solution .122

Question 123.

Solution .123

Question 124.

Solution .124

Question 125.

Solution .125