Read DK Goel Solutions Class 12 Accountancy Chapter 5 Accounting Ratios 2026. Students should study DK Goel Solutions Class 12 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 12 Accountancy have been prepared by expert teachers. These DK Goel Class 12 Solutions have been designed as per the latest accountancy DK Goel Book for Class 12 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 12 Accounts Chapter 5 Accounting Ratios DK Goel Solutions

DK Goel Solutions for Chapter 5 Accounting Ratios Class 12 Accounts have been provided below based on the latest DK Goel Class 12 book. The answers have been prepared based on the latest 2026 book for the current academic year. DK Goel Solutions Class 12 will help students to improve their concepts and easily solve accountancy questions for Class 12.

Chapter 5 Accounting Ratios DK Goel Class 12 Solutions

Short Answer Questions

Question . 1.

Solution . 1 Ratio analysis is the quantitative measurement of the performance of a business. It ignores the qualitative factors. For example while calculating the credit analysis of a customer seeking credit, he may deserve the credit to be granted on the basis of financial statements submitted by him but in reality his character and credit worthiness mat be doubtful.

Question . 2.

Solution . 2

(a) Analysis for short term debts :- Liquidity Ratio

(b) Analysis for long term debts :- Solution vency Ratio

Question . 3.

Solution . 3 The Current Ratio of a Company is 3:1 means that current assets of a business thrice of its current liabilities. The higher the ratio the better it is, because the firm will be able to pay its current liabilities more easily. But a much higher ratio may be considered to be adverse from the view point of management on account of the following reasons:

1.) A much higher ratio indicates that inventory might be pilling up because of poor sales.

2.) Large amount is locked up in trade receivables due to inefficient collection policy.

Question . 4.

Solution . 4 Window Dressing: Some companies in order to cover up their bad financial position resort to window dressing i.e., showing a better position than the one which really exists. They change their balance sheet in such a way that the important fact and truth may be concealed.

Question . 5.

Solution . 5 Some companies in order to cover up their bad financial position resort to window dressing i.e., showing a better position than the one which really exists. They change their balance sheet in such a way that the important fact and truth may be concealed. For example, the current assets of a company are Rs. 1,00,000 and its current liabilities are Rs. 50,000, so the current ratio is 2:1. After this, it purchased goods for Rs. 50,000 for credit in the month of March. If it records the purchases, the current assets will increase to Rs. 1,50,000 and current liabilities will increase to Rs. 1,00,000. As a result, the current ratio will be reduced to 3:2. The company may pass the entry for purchase in the beginning of the next year or may postpone the purchase itself for a few days.

Question . 6.

Solution . 6 Current Ratio:- The ratio explains the relationship between current assets and current liabilities of a business. The formula for calculating the ratio is

![]()

Quick Ratio:- Quick ratio indicates whether the firm is in a position to pay its current liabilities within a month or immediately. As such, the quick ratio is calculated by dividing liquid assets (Quick Current Assets) by current liabilities:

![]()

Question . 7.

Solution . 7 Quick Ratio is a better test of short-term financial position of the company than the current ratio, as it considers only those assets which can be easily and readily converted into cash. Inventory is not included in liquid assets as it may take a lot of time before it is converted into cash.

Question . 8.

Solution . 8 Shareholder’s Funds included Share Capital and Reserve & Surplus.

Question . 9.

Solution . 9 Equity shareholders fund included Equity Share Capital.

Question . 10.

Solution . 10 This ratio expresses the relationship between long term debts and shareholder’s funds. It indicates the proportion of funds which are acquired by long-term borrowings in comparison to shareholder’s funds. This ratio is calculated to ascertain the soundness of the long-term financial policies of the firm.

![]()

Question . 11.

Solution . 11 The higher ratio of inventory turnover ratio indicates that inventory is selling quickly. In a business where inventory turnover ratio is high goods can be sold at a low margin of profit and even then the profitability may be quite high.

A low inventory turnover ratio indicates that inventory does not sell quickly and remains lying in the godown for quite a long time. This results in increased storage costs, blocking of funds and losses on accounts of goods becoming obsolete or un-sale able.

Question . 12.

Solution 12.

Working Note:-

Credit Revenue from Operations = Total Revenue from Operations – Cash Revenue from Operations

Credit Revenue from Operations = Rs. 2,00,000 – Rs. 40,000

Credit Revenue from Operations = Rs. 1,60,000

Trade Receivables Turnover Ratio indicates the relationship between credit Revenue from Operations and average trade receivables during the year.

Question . 13.

Solution . 13 I. A too low trade receivables turnover ratio will indicate the liberal and inefficient credit and collection policy of the management. It shows that more money is being locked-up in trade receivables which will result in higher bad-debts, increase in cost of collection and also the loss of interest on the money due form trade receivables.

II. The higher ratio of inventory turnover ratio indicates that inventory is selling quickly. In a business where inventory turnover ratio is high goods can be sold at a low margin of profit and even then the profitability may be quite high.

Question .14.

Solution . 14 A too low trade receivables turnover ratio will indicate the liberal and inefficient credit and collection policy of the management. It shows that more money is being locked-up in trade receivables which will result in higher bad-debts, increase in cost of collection and also the loss of interest on the money due form trade receivables.

Question . 15.

Solution . 15 A high trade receivables turnover ratio indicates the prompt payment by trade receivables but a too high ratio may be the result of restrictive credit and collection policy of the management which may curtail the sales and hence may adversely affect the profits.

Question . 16.

Solution . 16 There may be different accounting policies adopted by different firms with regard to providing depreciation, creation of provision for doubtful debts, method of valuation of closing inventory etc. For instance, one firm may adopt the policy of charging depreciation on straight-line basis, while other way charges on written-down value method. Such difference makes the accounting ratios incomparable.

Question . 17.

Solution . 17 Price level over the years goes on charging, therefore, the ratio of various years cannot be compared. For example, one firm sells 1,000 Machines for Rs. 10 Lakhs during 2017; it again sells 1,000 Machines of the same type in 2018 but owing to rising price the sale price was Rs. 15 Lakhs. On the basis of ratios it will be concluded that the sales have increased by 50%, whereas in actual, sales have not increased at all. Hence the figures of the past year must be adjusted in the light of price level changes before the ratios for these years are compared.

Question . 18.

Solution . 18 (i) Debt-Equity Ratio:- This ratio expresses the relationship between long term debts and shareholder’s funds. It indicates the proportion of funds which are acquired by long-term borrowings in comparison to shareholder’s funds. This ratio is calculated to ascertain the soundness of the long-term financial policies of the firm.

Question . 19.

Solution . 19 (i) Gross Profit Ratio:- This Ratio establishes a relationship between Gross Profit and Revenue from Operations i.e. Net Sales. This ratio is computed and presented in percentage. The formula for computing this ratio is:

Question . 20.

Solution . 20 (i) Debt-Equity Ratio:- This ratio expresses the relationship between long term debts and shareholder’s funds. It indicates the proportion of funds which are acquired by long-term borrowings in comparison to shareholder’s funds. This ratio is calculated to ascertain the soundness of the long-term financial policies of the firm.

Question . 21.

Solution . 21 (i) Gross Profit Ratio:- This Ratio establishes a relationship between Gross Profit and Revenue from Operations i.e. Net Sales. This ratio is computed and presented in percentage. The formula for computing this ratio is:

Numerical Questions:-

Question .1.

Solution .1

Question .2.

Solution .2

Question .3.

Solution .3.

Comment: The short term financial position of the company is quite satisfactory because its current ratio is 3;2;1, which is more than the ideal current ratio of 2:1. Liquid ratio of the company is 1.4:1, which is also more than the ideal liquid ratio of 1:1.

Therefore, it can be said that the company is in a position to pat its current liabilities instantly.

Question .4

Solution . 4

Comment: The ideal current ratio should be 2:1. But in this case the current ratio is 1.92:1 which is less than the ideal ratio. Therefore, it can be said that the short-term financial position of the company is not satisfactory.

The ideal quick ratio should be 1:1. But in this case the quick ratio is .78: 1, hence, the short- term financial position cannot be said to be satisfactory.

Question .5.

Solution .5

Question .6.

Solution .6

Question .7 (A)

Solution .7(A) Current Ratio as given in the question is 2:1. In order to understand the question in a simple manner, it may be assured that current assets are Rs. 2,00,000 and current liabilities are Rs. 1,00,000.

Question .7 (B)

Solution .7 (B) Current Ratio as given in the question 2.5:2. Hence, it may be assured that Current Assets are Rs. 2,50,000 and current Liabilities are RS. 1,00,000.

Question .8.

Solution .8 Statement showing the effect of various transactions on Current Ratio:

Question .9.

Solution .9

Statement showing the effect of various transactions on Current Ratio;

Question .10.

Solution .10

Question .11.

Solution .11

Question .12.

Current liabilities = Total debt – Long term Debt

= Rs. 2,00,000 – Rs. 80,000 = Rs. 1,20,000

Current Assets = Working Capital + Current Liabilities

= Rs. 1,92,000 + Rs. 1,20,000 = Rs. 3,12,000

![]()

Question .13.

Solution .13 Current liabilities = Trade Payables – Bank Overdraft

= Rs. 2,00,000 – Rs. 40,000 = Rs. 2,40,000

Current Assets = Working Capital + Current Liabilities

= Rs. 4,80,000 + Rs. 2,40,000 = Rs. 7,20,000

![]()

Question .14. .

Solution .14.

Question .15 (A).

Solution .15 (A)

Question .15 (B).

Solution .15 (B)

Question .16.(A).

Solution .16 (A)

Given: Question uick Ratio=1.5, Current Liabilities = Rs. 1,60,000

Question uick Assets = Rs. 1,60,000 × 1.5 = RS. 2,40,000

Inventory = Current Assets – liquid Assets

= Rs. 3,20,000 – Rs. 2,40,000 = RS. 80,000

Question .16.(B).

Solution .16 (B)

Given: Quick Ratio=0.95

Calculated: Current Liabilities = Rs. 6,80,000

Quick Assets = Rs. 6,80,000 × 0.95 = RS. 6,46,000

Inventory = Current Assets – liquid Assets

= Rs.17,00,000 – Rs.6,46,000 = RS. 10,54,000

Question .16.(C).

Solution .16(C)

Question .17.

Solution .17

Working Capital = Current Assets – Current Liabilities

Current Ratio = 4:1 , therefore, based on current ratio, the working capital is 4-1=3

If Working Capital is 3, Current Assets = 4

Question .18.

Solution .18

Comment: the short term financial position of the enterprise is satisfactory because its liquid ratio is 1.35:1, which is above the ideal ratio of 1:1.

Question .19.

Solution .19

Question .20.

Solution .20

Question .21.

Solution .21

Current Ratio is 4.5 and Question uick ratio is 3

Difference between current ratio and quick ratio is inventory.

Therefore, inventory is 4.5-3=1.5.

If Inventory is 1.5, Current Assets = 4.5

Question .22.(A)

Solution .22 (A)

Calculation of Quick Ratio:

Quick Assets (Liquid Assets) = Current Assets – Inventory – Prepaid Expenses

= Rs. 85,000 – Rs. 22,000 – Rs. 3,000

= Rs. 60,000

Current Liabilities = Current Assets – working Capital

= Rs. 85,000 -Rs. 45,000

= Rs. 40,000

![]()

Question .22.(B)

Solution .22(B) Calculation of Current Ratio:

Current Assets = Quick Assets – Inventory – Prepaid Expenses

= Rs. 90,000 – Rs. 1,08,000 – Rs. 2,000

= Rs. 2,00,000

Current Liabilities = Current Assets – working Capital

= Rs. 2,00,000 -Rs. 1,50,000

= Rs. 50,000

![]()

Question .23.

Solution .23.

Current Liabilities = Total debt – Long term Debt

= Rs. 16,00,000 – Rs. 10,00,000

= Rs. 6,00,000

Current Assets = Current Liabilities + working Capital

= Rs. 6,00,000 -Rs. 4,80,000

= Rs. 10,80,000

Liquid Assets = Current Assets – Inventory – prepaid Insurance

= Rs. 10,80,000 – Rs. 3,40,000 – RS. 20,00

= Rs. 7,20,000

![]()

Question .24

Solution .24 Payment of current liabilities will result in equivalent reduction both in the amount of current assets as well as current liabilities.

Let the amount of current liabilities to be paid =

![]()

Or RS. 40,00,000 – 2

= 8,00,000.

Current liabilities to the extent of Rs. 8,00,000 should be paid to achieve the Current Ratio at the level of 2:1.

Question .25.

Solution .25

Therefore, current Assets of RS. 1,00,000 should be acquired on credit to maintain a Current Ratio of 2:1

Question .26.

Solution .26

Question .27

Solution .27

Question .28.

Solution .28

(i) Long term financial position of the Company can be assessed by calculating Debt-Equity Ratio.

Question .29.

Solution .29

![]()

Long term Debts = Long term Borrowings + Long term Provisions

= Rs. 16,00,000 + Rs. 1,50,000

= Rs. 17,50,000

Shareholder’s Funds = Non-Current Assets + Working Capital – Non- Current Liabilities

Non- Current Assets = Tangible Fixed Assets + Intangible Fixed Assets

=Rs. 24,50,000 + Rs. 3,00,000

=Rs. 27,50,000

Working Capital = Current Assets – Current Liabilities

= Rs. 3,34,000 – Rs. 84,000

= Rs. 2,50,000

Non -Current Liabilities refer to Long term Debts Thus,

Shareholder’s Funds = RS. 27,50,000 + RS. 2,50,000 – Rs. 17,50,000

= RS. 12,50,000

![]()

Question .30.

Solution .30

Question .31.

Solution .31

![]()

In the above question, Debt – Equity Ratio is given as 1:2, therefore, it may be assumed that Long term Debts are Rs. 1,00,000 and share holders’ fund shares worth Rs. 2,00,000.

(i) Issue of Equity Shares : Suppose equity shares worth Rs. 1,00,000 are issued them by the issue of Equity shares, shareholder’s Funds will be increases and will stand at Rs. 2,00,000 + Rs. 1,00,000 = Rs. 3,00,000 therefore, the revised ratio will be ;

![]()

Therefore, it can be concluded that increased in shareholder’s funds decreased the ratio.

(ii) Cash Received from Trade Receivables: By receiving cash from Trade receivables there will be affect on the cash and trade receivables only. Hence, there will be no change in debt equity ratio because neither the long – term debt nor the shareholder’s funds are affected.

(iii) Sale of goods on cash Basis: Goods sold on cash will affect only the Inventories and Cash. Hence, there will be no change in debt- equity ratio because neither the long -term debts nor the Shareholder’s Funds are affected.

(iv) Repayment of long term Borrowings: Suppose there is repayment of long term borrowings for Rs. 50,000 then by the repayment of long-term borrowing of Rs. 50,000, Long Term Debts will be reduced by Rs. 50,000 and these will stand at Rs. 1,00,000 – Rs. 50,000 = Rs. 50,000. Therefore, the revised ratio will be:

![]()

(v) Purchase of Goods on credit: Goods purchased on Credit will affect only the inventories and trade payables. Hence, there will be no change in debt- equity ratio because neither the long -term debts nor the Shareholder’s Funds are affected.

Question .32.

Solution .32

Statement showing the effect of various transactions on Debt-Equity Ratio:-

Question .33.

Solution .33

Question .34.

Solution .34.

Note: Reserve and Surplus will be ignored since it is already included in Shareholder’s fund

Question .35

Solution .35

Note: Surplus i.e., Balance is Statement of profit & loss will be ignored since it is already included in Reserve ad Surplus

Question .36

Solution .36

Question .37

Solution .37.

Question .38

Solution .38

Question .39

Solution .39

Question .40

Solution .40

Question .41.

Solution .41

Question .42.

Solution .42

Question .43.

Solution .43

Question .44.

Solution .44

Comment: Proprietary Ratio is only 20 % which means that the long term financial position of the company is not satisfactory because only 20% of the total assets of the company are funded by equity.

Comment: Normally, acceptable interest- coverage ratio is 6 or 7 times, where as the actual ratio for this company is 4. It means that the company may face difficulty in paying the interest on long- term loans regularly in case of fall of profits.

Question .45.

Solution .45

Question .46.

Solution .46

Note : Carriage outwards, Salaries and Rent will by ignored while calculating Inventory Turnover Ratio.

Question .47.

Solution .47

Note : Carriage outwards, Salaries and Rent will by ignored while calculating Inventory Turnover Ratio.

Question .48.

Solution .48

Question . 49.

Solution . 49

Question .50.

Solution .50

Question .51

Solution .51

Question .52

Solution .52

Question .53.

Solution .53

Cost of revenue from Operations = Revenue from Operations (Sales) + Gross Profit

= Rs. 5,00,000 – 16% of 5,00,000 = Rs. 5,80,000

Cost of revenue from Operations Opening Inventory + Purchases + Freight – Closing Inventory

Rs. 5,80,000 = Opening Inventory + RS. 5,70,000 + RS. 20,000 – Rs. 70,000

RS. 5,80,000 = Opening Inventory + RS. 5,20,000

Opening Inventory = Rs. 60,000

Question .54.

Solution .54

Question .55.

Solution .55.

Cost of revenue from Operations = Opening Inventory + Purchases + Direct Charges (i.e., Wages, carriage Inwards) – Closing Inventory

Rs. 5,60,000 = Rs. 75,000 + Rs. 4,40,000 + RS. 1,30,000 + Rs. 15,000 – Closing Inventory

Closing Inventory = RS. 6,60,000 = RS. 5,60,000 + Closing inventory

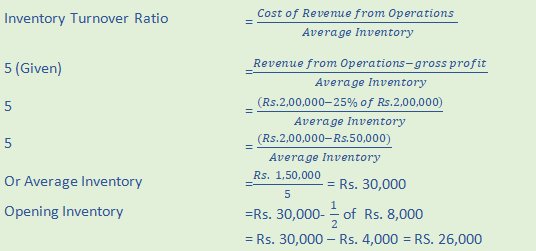

Question .56

Solution . 56 Cost of revenue from Operations = Revenue from operations – Gross profit

= RS. 2,00,000 – 25% of 2,00,000

= RS. 2,00,000 – RS. 50,000= RS. 1,50,000

Question .57.

Solution .57

Gross Profit is 25% on cost. Therefore, goods costing RS. 100 is sold for RS. 125.

Hence, if Revenue from Operations are Rs. 125,

Cost of Revenue from Operations = Rs. 100

If Revenue from Operations are Rs. 10,00,000

Question .58.

Solution .58

Question .59

Solution .59

Question .60(A)

Solution .60(A)

Question .60 (B).

Solution .60 (B)

Question .61.

Solution .61

Question .62.

Solution .62

Cost of Revenue from Operations = 6 × 60,000 = Rs. 3,60,000

Revenue from Operations add a profit of 20% on sales.

Goods costing RS. 80 which have been sold for Rs. 100. As such:

If Cost of Revenue from operations is Rs. 80, revenue from Operations are 100.

If Cost of Revenue from Operations is 3,60,000, Revenue from Operations are 100/80× 3,60,000 = RS. 4,50,000

Question .63.

Solution .63

Gross profit is 25% od cost. Therefore, goods costing RS. 100 is sold for RS. 125.

If Revenue from Operations are 125, Cost is 100

Current Liabilities are RS. 50,000 and Quick Ratio is 1 Therefore,

(iv) Quick Assets = RS. 50,000 × 1 = Rs. 50,000

(v) Current Assets = Quick Assets + Closing Inventory

= RS. 50,000 + Rs. 50,000 = RS. 1,00,000

Question .64.

Solution .64

Question .65.

Solution .65

Question .66.

Solution .66

Question .67

Solution .67

Question . 68

Solution .68

In order to ascertain the Trade Receivables Turnover ratio, the figure of Credit Revenue from Operations will have to be ascertained. It is as follows:

If credit revenue from operations are 100, Cash revenue from operations will be 20 Therefore, Total revenue from operations will be 100 + 20 = 120

Again, if total revenue from operations are 120,

Credit revenue from operations=100

If total revenue from operations are 4,80,000,

It is to be noted that any fraction of a day such as .48 would, in practice, mean that the payment will be received next day. Hence, in the above case, 68.48 days would imply 69 days.

Question .69.

Solution .69

Question .70.

Solution .70

Calculation of closing receivables:

Opening Trade Receivables + Closing Trade Receivables = Average Trade receivables × 2

=RS. 36,000 × 2= Rs. 72,000

As Closing Trade Receivables = Rs. 40,000,

Opening Trade Receivables = Rs. 72,000 – Rs. 40,000 = Rs. 32,000.

Question .71

Solution .71

Question .72

Solution .72

Question .73.

Solution .73

Question .74.

Solution .74

Question .75.

Solution .75

Comment: 1.

In 2017, Trade Receivables Turnover ratio has increased from 6 times to 7.5 times. It indicates that amount from trade receivables is being collected more quickly.

2. In 2017, Inventory Turnover Ratio has also increased. It indicates that inventory is being rotated into revenue from operations more quickly. As such, the sales policy of the management is quite efficient.

Question .76.

Solution .76

Question .77

Solution .77

Question .78

Solution .78

Question .79.

Solution .79.

Net Revenue from Operations =Credit Revenue from Operations + Cash Revenue from operations- Revenue from Operations return

= Rs. 8,00,000 + Rs. 12,60,000 – Rs. 80,000

= Rs. 19,80,000

Working Capital =Current Assets – Current liabilities

= Rs. 7,20,000 – Rs. 3,24,000 = Rs. 3,96,000

Question .80

Solution .80

Current Assets = Inventory + Trade receivables + cash

= Rs. 6,00,000 + Rs. 5,00,000 + Rs. 1,00,000

= Rs. 12,00,000

Current Liabilities = Trade Payables + Bank Overdraft

= Rs. 2,00,000 + Rs. 1,20,000

= Rs. 3,20,000

Working Capital =Current Assets – Current liabilities

= Rs. 12,00,000 – Rs. 3,20,000

= Rs. 8,80,000

Question .81.

Solution .81

Question .82.

Solution .82

Question .83

Solution .83

Question .84.

Solution .84

Question .85.(A)

Solution .85(A)

Question .85. (B)

Solution .85(B)

Comment: Gross Profit Ratio has decreased considerably, which indicates that the price of materials Purchased, wages and other direct changes ,may have gone up but the sales price may not have increased in the same proportion.

Question .86(A)

Solution .86(A)

Question .86 (B)

Solution .86(B)

Question .87.

Solution .87

Question .88.

Solution .88.

Question .90

Solution .90

Gross Profit is 40% of Cost

Therefore, goods costing Rs. 100 must have been sold for Rs. 140

Hence, If Revenue from operations are Rs. 140, G.P. = Rs. 40

Question .91 (A)

Question .91 (B)

Question .92

Solution .92

Net Revenue from operations = Cash revenue from operations + Credit Revenue from Operations

= Rs. 25,000 + Rs. 75,000 = Rs. 1,00,000

Net Purchases = Cash Purchases + Credit Purchases – Return Outwards

= Rs. 15,000 + Rs. 60,000 – Rs. 2,000 = Rs. 73,000

Cost of Revenue from operations = Purchases + (Opening Inventory – Closing Inventory) + Direct expenses Purchases + Decrease in inventory + Carriage inwards = wages

= Rs. 73,000 + Rs. 10,000 + Rs. 2,000 + Rs. 5,000

= Rs. 90,000

Gross profit = Revenue from Operations – Cost of Revenue from operations

= Rs. 1,00,000 – Rs. 90,000

= Rs. 10,000

Question .93

Solution .93

Question .94.

Solution .94

Gross Profit = Revenue from Operations – Cost of Revenue from Operations

= Rs. 3,40,000 – Rs. 1,20,000

= Rs. 2,20,000

Question .95.

Solution .95

Question .96.

Solution .96

Question .97

Solution .97

Question .98

Solution .98

Hence, Cost of Revenue from Operations + Operating Expenses = 90% of Net Revenue from Operations

Cost of Revenue from Operations + Rs. 30,000 + Rs. 20,000 = 90% of Rs. 6,60,000

Cost of Revenue from Operations + Rs. 50,000 = Rs. 5,94,000

Cost of Revenue from Operations =Rs. 5,94,000 -Rs.50,000

= Rs. 5,44,000

Question .99

Solution .99

Question .100.

Solution .100

Question .101.

Solution .101

![]()

Net Revenue from Operations = Rs. 4,00,000- Rs. 15,000 = Rs. 3,85,000

Cost of revenue from operations = Rs.. 4,00,000 – RS. 15,000 = Rs. 3,85,000

Cost of revenue from Operations = Opening Stock + purchases – Purchases returns – Closing Stock

= Rs. 10,000 + Rs. 1,20,000 – Rs. 5,000 – RS. 60,000 = Rs. 65,000

Gross Profit = Net Revenue from operations – Cost of Revenue from operations

=Rs. 70,000 – Rs. 40,000

= Rs. 1,10,000

Operating Expenses = Selling Expenses + Administrative Expenses

= Rs. 70,000 + Rs. 40,000

= Rs. 1,10,000

Question .102.

Solution . 102.

Question .103

Solution .103.

Question .104

Solution .104 Credit revenue from operations were 90% of total revenue from Operations.

It means cash revenue from operations were 10% of total revenue from operations.

If cash revenue from operations were 10, total revenue from operations were 1000

If cash revenue from operations were RS. 5,00,000. Total revenue from operations were

Question .105

Solution .105

Question .106.

Solution .106

Question .107

Solution .107

Question .108.

Solution .108

Question .109.

Solution .109

Question .110.

Solution .110

Question .111.

Solution .111

Question .112.

Solution .112

Question .113.

Solution .113

Question .114.

Solution .114.

Question .115

Solution .115

Question .116

Solution .116

Question .117

Solution .117

Question .118.

Solution .118

Short Term financial position can be ascertained by analyzing its Liquidity Ratios.

Liquidity Ratio include the following two ratios:

(a) Current Ratio and (b) Quick Ratio

Comments: Short Term finance position of the company is sound because its Current Ratio is 3:1 which is more than the ideal ratio of 2:1. Similarly, quick ratio is 1.7:1 which is more than the ideal ratio of 1:1.

Question .119.

Solution .119

Short term financial position can be commented upon with the help of Liquidity Ratios. Liquidity Ratios include the following two ratios:

(a) Current Ratio and (b) Quick Ratio

Comments: Short Term finance position of the company is unsatisfactory because its Current Ratio is 1.85:1 which is less than the ideal ratio of 2:1. Similarly, quick ratio is .8:1 which is more than the ideal ratio of 1:1.

Question .120.

Solution .120

Question .121.

Solution .121

Question .122.

Solution .122

Question .123.

Solution .123.

Question .124

Solution .124

Question .125.

Solution .125

Question .126.

Solution .126

Question .127.

Solution .127

Question .128.

Solution .128

Question .129.

Solution .129

Question .130.

Solution .130

Question .131.

Solution .131

Question .132.

Solution .132

Question .133.

Solution .133

Question .134.

Solution .134.

Question .135.

Solution .135

Question .136.

Solution .136

Question .137

Solution .137.

Question .138.

Question .139.

Solution .139

Question .140.

Solution .140

Question .141.

Solution .141

Question .142.

Solution .142

Question .143.

Solution .143

Question .144.

Solution .144

Question .145.

Solution .145

Question .146

Solution .146

Therefore, Current Liabilities of Rs. 3,00,000 must be paid maintain the Current Ratio of 2:1.

Question .147.

Solution .147

Question .148.

Solution .148

Question .149.

Solution .149

Question .150

Solution .150.

Question . 151

Solution . 151

Comment: Interest coverage ratio of the company is satisfactory because, the interest coverage ratio is equal to the acceptable interest coverage ratio of 6 or 7 times.

Question .152

Solution .152

Question .153.

Solution .153

Question .154

Solution .154

Question .155.

Solution .155.

Question .156

Solution .156

Question .157.

Solution .157

Question .158.

Solution .158

Question .159.

Solution .159

Question .160. .

Solution .160

Question .161.

Solution .161

Question .162.

Solution .162

Since figure of opening inventory is not given, it may be calculated as follows:

Cost of revenue from operations = Opening Inventory + Purchases – Carriage- Closing Inventory

Hence, Opening Inventory = Cost of reserve from Operations – Purchases – Carriage + closing Inventory

= RS. 1,50,000 – Rs. 1,40,000 – 4,000 + 22,000

=Rs. 28,000

Question .163.

Solution .163

Question .164.

Solution .164

Question .165.

Solution .165

Question .166.

Solution .166.

Question .167

Solution .167

Question . 168

Solution .168

Question .169

Solution .169

Question .170

Solution .170

Question .171

Solution .171

Question .172

Solution .172

Question .173.

Solution .173

Question .174.

Solution .174

Question .175.

Solution .175

Question .176.

Solution .176

Question .177.

Solution .177

Question .178.

Solution .178

Question .179.

Solution .179.

Question .180.

Solution .180

Question .181.

Solution .181

Question .182.

Solution .182

Question .183.

Solution .183

Question .184.

Solution .184

Question .185.

Solution .185

If Total Revenue from Operations is Rs. 100, cash Revenue from Operations will be RS. 25 and Credit Revenue from Operations RS. 75

Hence, If Credit Revenue from Operations is Rs. 75

Total Revenue from operations will be RS. 100

If Credit Revenue from Operations is RS. 6,00,000

Question .186.

Solution .186

Question .188.

Solution .188.

Question .189.

Solution .189

Question .190

Solution .190

Question .191.

Solution .191

We do not coincide with Mr. Arun Birla. The manager is not very effective. Although his revenue from operations has doubled this year compared to the last year, his gross profit ratio has come down from 25% to 20%. This can either be due to lower selling prices or higher purchase prices or due to disorganization.

Question .192.

Solution .192

Question .193.

Solution .193

Question .194.

Solution .194

Question .195.

Solution .195

Question .196.

Solution .196

Question .197.

Solution .197

Question .198.

Solution .198

![]()

Operating Profit = Gross Profit – Operating Expenses

Gross Profit = Net Revenue from operations – Cost of Revenue from operations

=(Cash Revenue from Operations – Credit Revenue from Operations – Revenue from Operations Return ) -Cost of Revenue from Operations

=(Rs. 2,00,000 + Rs. 1,30,000 – Rs. 10,000) – Rs. 1,80,000

= Rs. 3,20,000 – Rs. 1,80,000

= Rs. 1,40,000

Operating Expenses = Selling Expenses +Office Administrative Expenses

= Rs. 36,000 + Rs. 40,000

= Rs. 76,000

Operating Profit = Gross Profit – Operating Expenses

=Rs. 1,40,000 – Rs. 76,000 = Rs. 64,000

Question .199.

Solution .199

Question .200.

Solution .200

Question .201.

Solution .201

Operating Profit Ratio = 100 - Operating Ratio

Operating Profit Ratio = 100 – 78%

Operating Profit Ratio = 22%

Question .202.

Solution . 202