Read TS Grewal Solution Class 12 Chapter 4 Change in Profit Sharing Ratio Among the Existing Partners 2026. Students should study TS Grewal Solutions Class 12 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 12 Accountancy have been prepared by expert teachers. These TS Grewal Class 12 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 12 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 12 Accounts Chapter 4 Change in Profit Sharing Ratio Among the Existing Partners TS Grewal Solutions

TS Grewal Solutions for Chapter 4 Change in Profit Sharing Ratio Among the Existing Partners Class 12 Accounts have been provided below based on the latest TS Grewal Class 12 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 12 will help students to improve their concepts and easily solve accountancy questions for Class 12.

Chapter 4 Change in Profit Sharing Ratio Among the Existing Partners TS Grewal Class 12 Solutions

About this chapter: The TS Grewal Class 12 Chapter 4 on Change in Profit Sharing Ratio among partners is an important topic for class 12 students. Concepts relating to a partnership firm's profit-sharing ratio and how it can be changed have been explained in this chapter. There is a detailed explanation relating to the concept of a partnership firm and its importance. It also explains the concept relating to the profit sharing ratio and its significance in the partnership business. The chapter further details the conditions under which the profit-sharing ratio can be changed among the existing partners. It explains the different scenarios of impact on profit sharing ratio due to admission of a new partner, retirement of a partner, and death of a partner. Each of these topics has been explained in detail along with a lot of questions which the students can practice which will help them to get more marks in Class 12 board examinations. There are a lot of solved and unsolved questions also in the chapter. Our Class 12 Accountancy teachers have provided step-by-step solutions for all questions given in this chapter. TS Grewal Class 12 Chapter 4 is an important topic for all students as it will help them to understand the complexities of partnership firms' profit-sharing ratios.

About Solution:-

The ratio in which one or more partners of the firm forsake their share of profit in favour of one or more partners of the firm is known as the sacrificing ratio.

Things to Remember:

By comparing the previous and new profit sharing ratios, the sacrifice or gain may be computed. Gain occurs when a partner's new share exceeds his or her previous portion, and vice versa.

Important Notes:

Sacrifice ratio = Old ratio- New ratio

Note:- If the result is in negative it is gain.

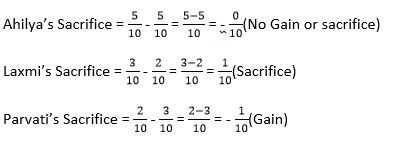

Answer 2:

Old Ratio Ahilya: Laxmi: Parvati = 5:3:2

New Ratio Ahilya: Laxmi: Parvati = 5:3:2

Sacrificing Ratio = Old Ratio − New Ratio

About Solution:-

When we receive zero from the computation of the gaining and sacrificing ratio, we know we have no gain and no scarifies.

Things to Remember:

It is important to know that in every case the total sacrifice is equal to the total gain.

Important Notes:

Gaining Ratio = New ratio- Old ratio

Note:- If the result is in negative it is sacrifice.

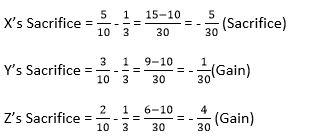

Answer 3:

Old Ratio X:Y:Z = 5:3:2

New Ratio X:Y:Z = 1:1:1

Sacrificing Ratio = Old Ratio − New Ratio

About Solution:-

The Gaining Ratio is the ratio in which one or more partners gain a portion of profit as a result of one or more partners of the company sacrificing a share of profit.

Things to Remember:

The ratio of remaining partners is known as New Profit Sharing Ratio, in which they will share the future profits. When a partner retires from the firm, the remaining partners acquired share of retiring partner either in their old ratio or in specified ratio.

Important Notes:

1. When new profit sharing ratio of continuing partners is not given, in such a situation, it is assumed that they will share profits in their old ratio.

2. When new profit sharing ratio of continuing partner is given.

3. When continuing partners acquire retiring partners share in some specified proportion.

4. When retiring partner sells his share to the continuing partners.

About Solution:-

Whenever there is a change in the profit sharing ratio, one or more of the existing partners have to surrender some of their old share in favour of one or more of other partners.

Things to Remember:

By comparing the previous and new profit sharing ratios, the sacrifice or gain may be computed. Gain occurs when a partner's new share exceeds his or her previous portion, and vice versa.

Important Notes:

Sacrifice ratio = Old ratio- New ratio

Q5: Pranav, Karan, and Rahim are partners sharing profits and losses in an agreed ratio. With effect from 1st April 2023, they agreed to share profit in the ratio of 3 : 3 : 4. To arrive at the new ratio, Rahim takes 1/5th share equally from Pranav and Karan. Calculate the old profit-sharing ratio.

Answer 5:

Accounting treatment of goodwill

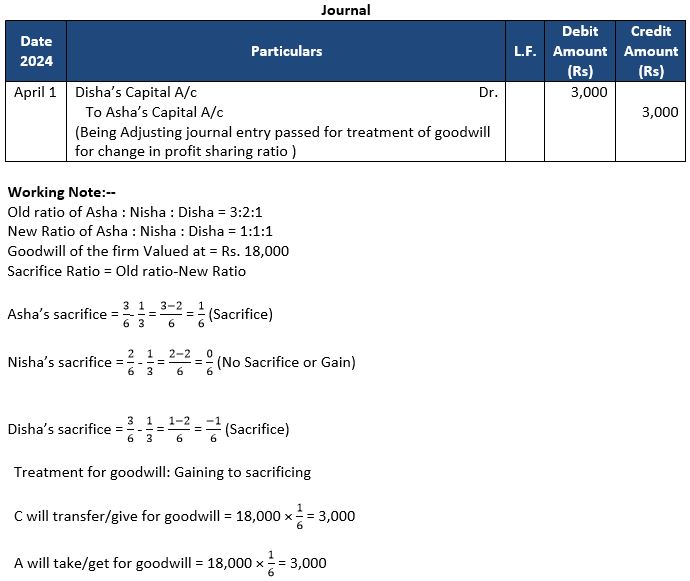

Question 6: Asha, Nisha and Disha shared profits and losses in the ratio of 3:2:1 respectively. With effect from 1st April, 2024, they agreed to share profits equally. The goodwill of the firm was valued at Rs. 18,000. Pass necessary Journal entries to record the above change.

Answer 6:

About Solution:-

Goodwill means the good name or the reputation earned by a firm through the hardwork and honestly of its owners. If a firm renders good service to the customers the customers who feel satisfied will come again and again and the firm will be able to earn more profits in future.

Things to Remember:

Goodwill belongs to the category of intangible assets such as patents, trade mark, copyright etc. It does not suffer wear and tear and as such the question of depreciation does not arise on it, as is the case of the assets.

Important Notes:

While goodwill does not depreciate, it’s value is liable to constant fluctuation. It is always present as a silent asset in a business where there are super profit(i.e., more than the normal) but declines in the value with the decline in earnings.

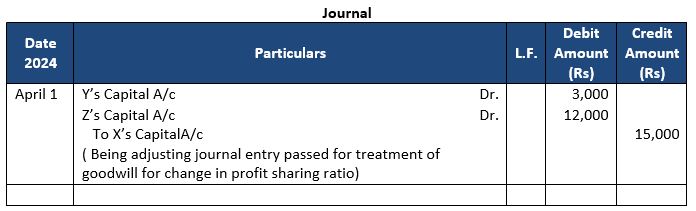

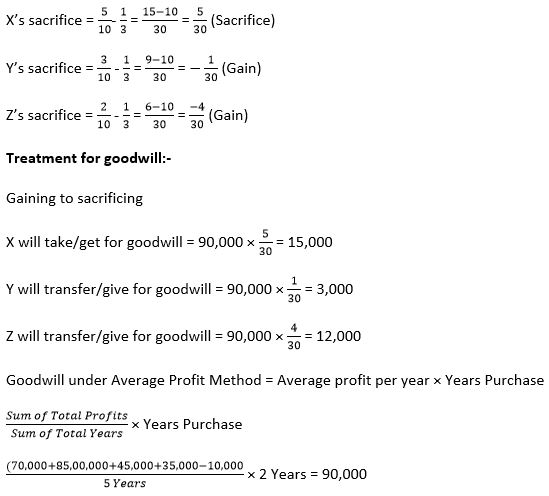

Question 7: X, Y and Z are partners sharing profits and losses in the ratio of 5:3:2. From 1st April, 2023, they decided to share profits and losses equally. The Partnership Deed provides that in the event of any change in the profit-sharing ratio, the goodwill should be valued at two years' purchase of the average profit of the preceding five years. The profits and losses of the preceding years are:

You are required to calculate goodwill and pass journal entry.

Answer 7:

Working Note:-

Old ratio of X:Y:Z = 5:3:2

New Ratio of X:Y:Z = 1:1:1

Sacrifice Ratio = Old Ratio-New Ratio

About Solution:-

Change in Profit Sharing Ratio among the Existing Partners: Sometimes the existing partners decide to change their profit sharing ratio. The change is necessitated due to the change in capital contribution or in active participation in management. As a result of change in profit sharing ratio, one or more of the existing partners may acquire extra share in profits at the cost of one or more of other partners. In such a case, in order to maintain equity among the partners, it is necessary to make adjustments for goodwill, revaluation of assets and liabilities, reserves, accumulated profits and losses etc. These adjustments are similar to those made at the time of admission or retirement of a partner.

Things to Remember:

Whenever there is a change in the profit sharing ratio, one or more of the existing partners have to surrender some of their old share in favour of one or more of other partners. The ratio of surrender of profit sharing ratio is called sacrificing ratio. It is calculated as follows:

Sacrificing Ratio = Old Ratio - New Ratio

Important Notes:

Adjustments required at the time of change in the profit sharing ratio: Various matters that need to be considered at the time of change in profit sharing ratio are:

(1) Determination of Sacrificing Ratio and Gaining Ratio

(2) Accounting for Goodwill

(3) Accounting Treatment of Reserves and Accumulated Profits

(4) Accounting for Revaluation of Assets and Liabilities

(5) Adjustment of Capitals

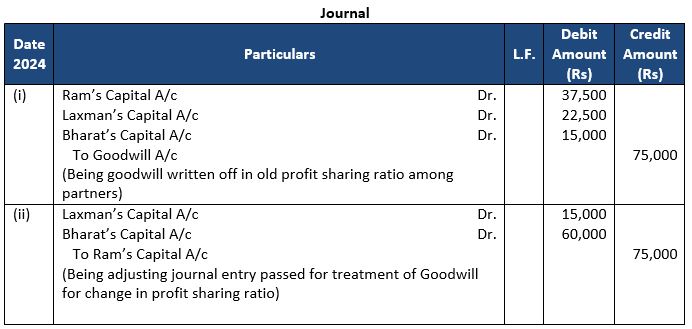

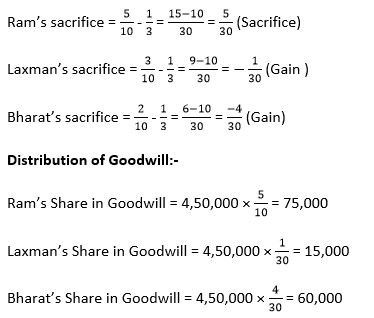

Question 8: Ram, Laxman and Bharat who were sharing profits and losses in the ratio of 5 : 3 : 2, decide to share profits and losses equally with effect from 1st April, 2023. The goodwill of the firm is valued at ₹ 4,50,000. Goodwill is appearing in the books is at ₹ 75,000.

Pass necessary Journal entries to record the above change.

Answer 8:

Working Note:-

Old Ratio of X:Y:Z = 5:3:2

New Ratio of X:Y:Z = 1:1:1

Sacrifice Ratio = old ratio-New Ratio

About Solution:-

Goodwill is the value of the reputation of a firm which enables it to earn higher profits in comparison to the normal profits earned by other firms in the same trade.

Things to Remember:

Goodwill is an Intangible Asset. Goodwill belongs to the category of intangible assets such as patents, trademarks, copy rights etc. It does not suffer wear and tear and as such the question of depreciation does not arise on it, as is the case of other assets.

Important Notes:

Goodwill is value is Liable to Constant Fluctuations: While goodwill does not depreciate, its value is liable to constant fluctuations. It is always present as a silent asset in a business where there are super profits (i.e., more than the normal) but declines in value with the decline in earnings.

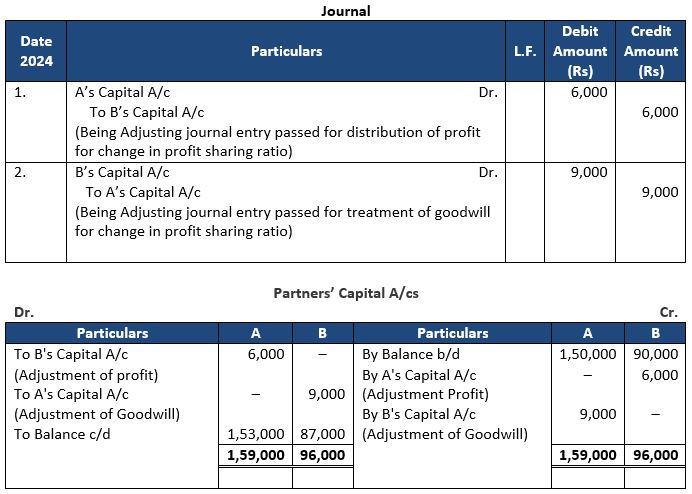

Question 9: A and B are partners in a firm sharing profits in the ratio of 2:1. They decided with effect from 1st April, 2023, that they would share profits in the ratio of 3:2. But, this decision was taken after the profit for the year 2023-24 amounting to Rs. 90,000 was distributed in the old profit sharing ratio.

Firm's goodwill was valued on the basis of aggregate of two years' profits preceding the date decision became effective.

Profits for the year ended 31st March, 2022 and 2023 were Rs. 60,000 and Rs. 75,000 respectively. Capital Accounts of the partners as at 31st March, 2024 stood at Rs. 1,50,000 for A and Rs. 90,000 for B.

Pass necessary Journal entries and prepare Partner’s Capital Accounts.

Answer 9:

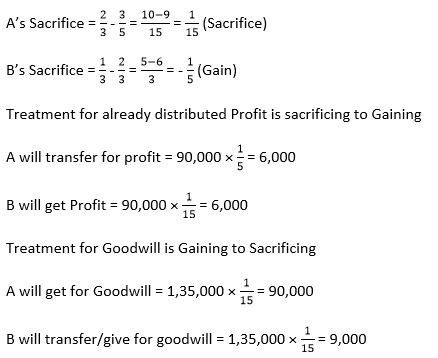

Working note:-

Old Ratio of A : B = 2 : 1

New Ratio = A : B = 3 : 2

Sacrificing Ratio = Old Ratio – New Ratio

About Solution:-

Goodwill is an intangible asset since it has no physical existence and cannot be seen or touched. But it is not a fictitious asset because fictitious assets do not have a value whereas goodwill has a value in case of profit making concerns. It can be sold, though a sale will be possible along with the sale of entire business.

Things to Remember:

The goodwill is the extra earning capacity of a business. Thus all factors which help a firm in earning profits affect the goodwill of the firm. Following factors affect the goodwill of a firm: 1. Favourable Location of the Business: If the business is located at a convenient or prominent place, it will attract more customers and therefore will have more goodwill.

Important Notes:

Efficiency of Management: If the business is run by experienced and efficient management, its profits will go on increasing, which results in increase in the value of goodwill.

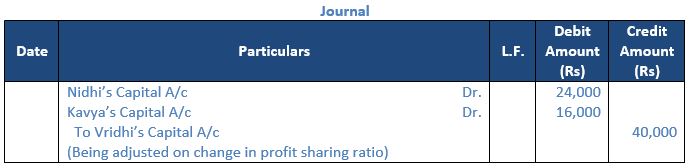

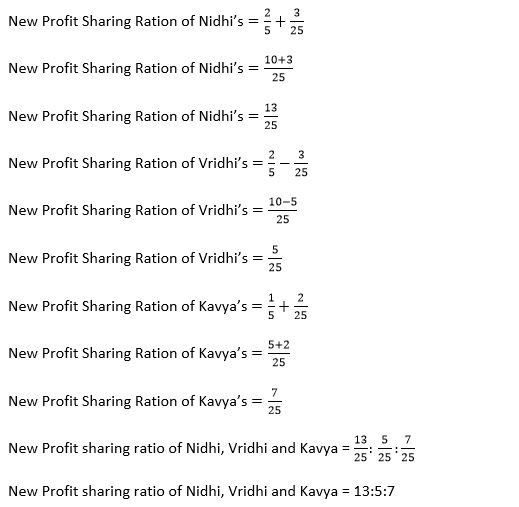

Question 10: Nidhi, Vidhi and Kavya are partners sharing profits and losses in the ratio of 2 : 2 : 1. From 1st April 2023, they decide to change the profit-sharing ratio. They pass the following adjustments entry for goodwill in the books:

What will be the new profit sharing ratio of partners assuming capital of partners are fixed?

Answer 10:

Calculation of New Profit sharing Ratio:-

Old Ratio = 2:2:1

Sacrificing Ratio = 24,000 : 16,000

Sacrificing Ratio = 3 : 2

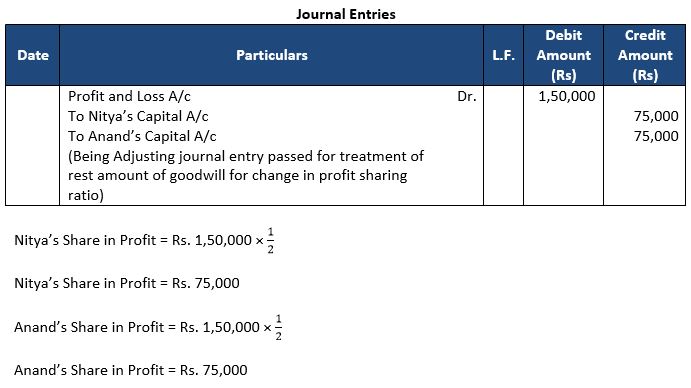

Question 11: Nitya and Anand are partners in a firm sharing profits and losses equally. With effect from 1st April 2023, they decided to share future profits in the ratio of 3 : 2. On the date of the change in the profit sharing ratio, the Profit & Loss Account had a credit balance of ₹ 1,50,000. Pass the necessary Journal entry for the distribution of the balance in the Profit & Loss Account before the change in the profit-sharing ratio.

Answer 11

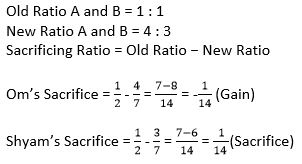

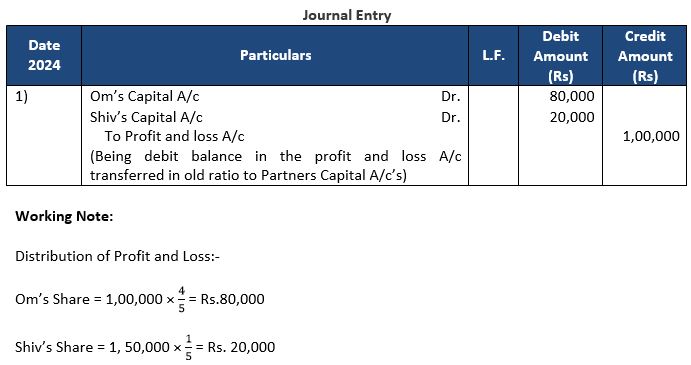

Question 12: Om and Shiv are partners in a firm sharing profits in the ratio of 4:1. They decided to share future profits in the ratio of 3:2 w.e.f. 1st April,2024. On that day, Profit and Loss A/c showed a debit balance of Rs 1,00,000. Pass journal entry to give effect to the above.

Answer 12:

About Solution:-

Other factors:-

(i) Good industrial relations regulations

(ii) Favourable Government

(iii) Stable political conditions

(iv) Research and development efforts

(v) Effective advertising to establish brand

(vi) Popularity of product in terms of quality

Things to Remember:

Goodwill can be classified into two categories:

(1) Purchased Goodwill, and

(2) Self-Generated Goodwill or Inherent Goodwill

Important Notes:

1. When there is a change in the profit sharing ratio among the existing partners;

2. When a new partner is admitted;

3. When a partner retires or dies;

4. When the firm is sold; and

5. When the firm is amalgamated with another firm.

Question 13: A, B and C who are presently sharing profits and losses in the ratio of 5:3:2 decide to share future profits and losses in the ratio of 2:3:5. Give the journal entry to distribute ' Workmen Compensation Reserve' of Rs. 1,20,000 at the time of change in profit-sharing ratio, when:

(i) no information is given; (ii) there is no claim against it.

Answer 13:

About Solution:-

Workmen compensation reserve is a liability to the company so we are debited it for zero effect of this.

Things to Remember:

The following factors should be taken into account while calculating the average profits:

(i) Abnormal income of a year should be deducted out of the net profit of that.

(ii) Abnormal loss of a year should be added back to the net profit of that year.

(iii) Income from Investments should be deducted out of the net profits of that year, because this income is received from outside the business.

Important Notes:

Weighted Average Profit Method is a modified version of average profit method. As per this method each year's profit is assigned a weight. The highest weight is attached to the profit of the most recent year

Question 14: X, Y and Z who are presently sharing profits and losses in the ratio of 5:3:2 decide to share future profits and losses in the ratio of 2:3:5. Give the journal entry to distribute ' Workmen Compensation Reserve' of Rs. 1,20,000 at the time of change in profit-sharing ratio, when there is a claim of Rs. 80,000 against it.

Answer 14:

About Solution:-

Workmen Compensation Reserve is created out of firm’s profits to pay compensation to employees. At the time of change in profit sharing ratio it is treated as follows:-

1.) If there is no claim against Workmen Compensation Reserve.

2.) If the claim for workmen compensation is lower than the amount of workmen Compensation Reserve.

3.) If the claim is equal to workmen compensation reserve.

4.) If the claim is more than the amount of workmen compensation reserves.

Things to Remember:

If there is no claim against Workmen Compensation Reserve, the entire amount of workmen compensation reserve is credited to the capital account of partners in their old profit sharing ratio:

Workmen Compensation Reserve A/c Dr.

To Partner’s Capital A/c

(Workmen compensation reserve credited to

partners’ capital accounts in their old profit

sharing ratio)

Important Notes:

If the claim for workmen compensation is lower than the amount of workmen Compensation Reserve:-

Workmen Compensation Reserve A/c Dr.

To Provision for workmen compensation claim A/c

To Partner’s Capital A/c

(Amount of claim transferred to liability and balance to

partner’s capital account in their old profit sharing ratio)

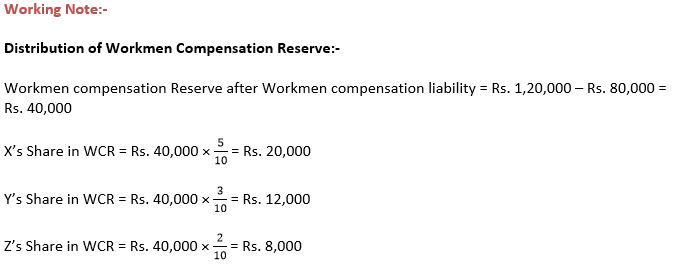

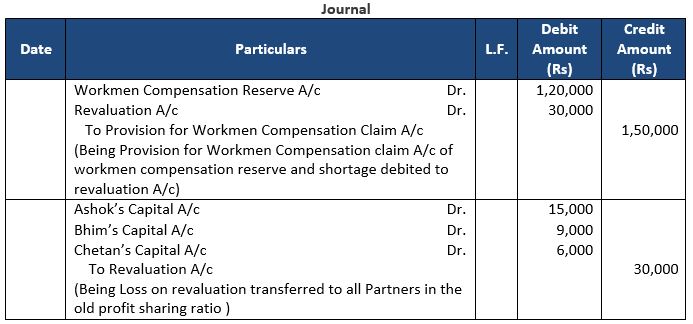

Question 15: Ashok, Bhim and Chetan who are presently sharing profits and losses in the ratio of 5:3:2 decide to share future profits and losses in the ratio of 2:3:5 with effect from 1st April, 2024. Workmen Compensation Reserve appears at Rs. 1,20,000 in the Balance Sheet as at 31st March, 2024 and Workmen Compensation Claim is estimated at Rs. 1,50,000. Pass journal entries for the accounting treatment of Workmen Compensation Reserve.

Answer 15:

About Solution:-

If the claim is equal to workmen compensation reserve:-

Workmen compensation reserve a/c Dr.

To Provision for Workmen Compensation claim a/c

Things to Remember:

If the claim is more than the amount of workmen compensation reserves:-

(i) Workmen compensation reserve A/c Dr.

Revaluation A/c

To Provision for Workmen Compensation claim A/c

(Amount of claim debited to workmen compensation

Reserve and revaluation a/c)

(ii) Partners Capital A/c Dr.

To Revaluation A/c

(Loss on revolution transferred to capital accounts of partners in their old profit sharing ratio)

Important Notes:

Entire amount of workmen compensation reserve along with the excess claim is credited to ‘provision for workmen compensation claim a/c’. The amount of excess claim is debited to ‘Revaluation Account’ because the loss must be borne by partners in their old profit sharing ratio.

Question 16: A, B and C who are presently sharing profits and losses in the ratio of 5:3:2 decide to share future profits and losses in the ratio of 2:3:5. Give the journal entry to distribute 'Investments Fluctuation Reserve' of Rs. 20,000 at the time of change in profit-sharing ratio, when investment (market value Rs. 95,000) appears in the books at Rs. 1,00,000.

Answer 16:

About Solution:-

Fall in the value less than investment fluctuation fund. The entry is:-

Investment fluctuation Reserve A/c Dr.

To Investment A/c

To Partner’s Capital A/cs

(Being transfer of excess i.f.r to partners’ capital a/c in their old profit sharing ratio)

Things to Remember:

Investment fluctuation fund is created out of firms profit to meet the fall in market value of investment.

Important Notes:

At the time of change in profit sharing ratio this reserve is created as follows:

1. When book value of investment is same as value of market investment.

2. If market value of investment is less than the book value.

3. Fall in the value less than investment fluctuation fund.

4. Fall in value is equal to investment fluctuation fund.

5. Fall in value is more than investment fluctuation fund.

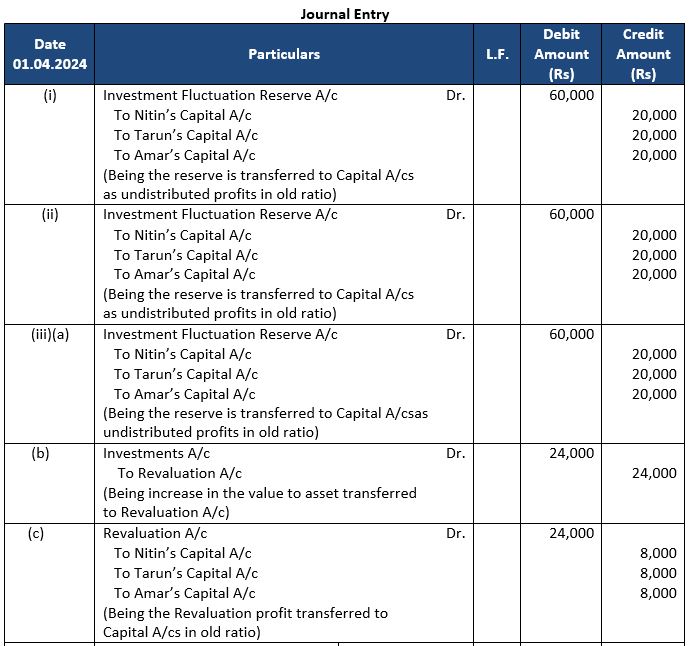

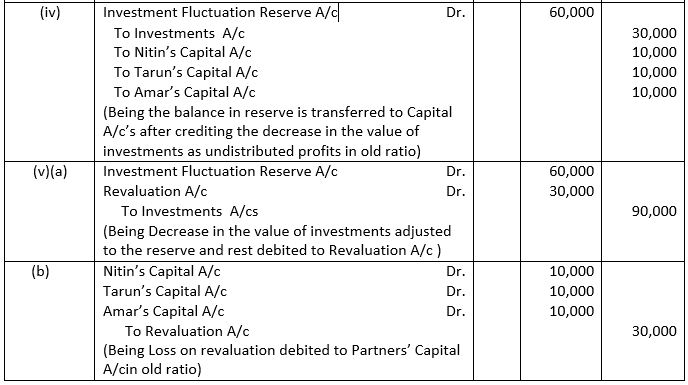

Question 17: Nitin, Tarun and Amar are partners sharing profits equally and decide to share profits in the ratio of 2:2:1 w.e.f . 1st April, 2024. The extract of their Balance Sheet as at 31st March, 2024 is as follows:

Pass the journal entries in each of the following situations:

(i) When its Market Value is not given;

(ii) When its Market Value is given as Rs 4,00,000;

(iii) When its Market Value is given as Rs 4,24,000;

(iv) When its Market Value is given as Rs 3,70,000;

(v) When its Market Value is given as Rs 3,10,000.

Answer 17:

About Solution:-

When book value of investment is same as value of market investment: in such case, the entire amount of investment fluctuation reserve is transferred to capital account of partners in their of profit sharing ratio.

Things to Remember:

When book value of investment is same as value of market investment: the entry is

Investment fluctuation reserve A/c Dr.

To partner’s capital a/c

(Being transfer of excess i.f.r to partners’ capital a/c in their old profit sharing ratio)

Important Notes:

Excess amount of Investment fluctuation reserve is transferred to partner’s capital account.

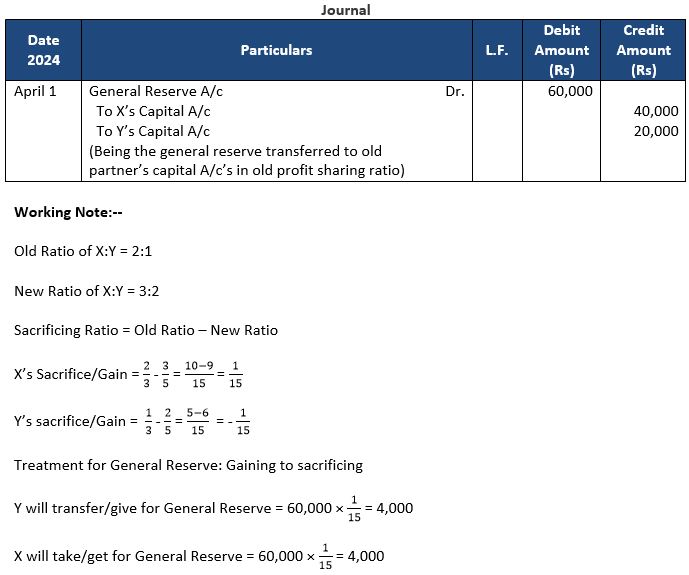

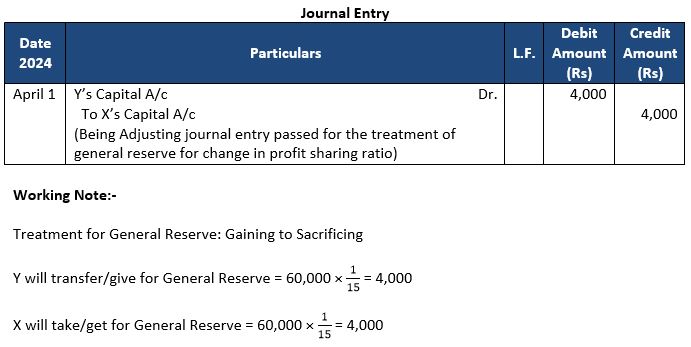

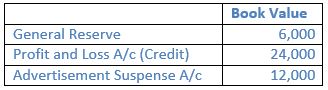

Question 18: Bootstrap and Davy Jones partners sharing profits in the ratio of 2:1. On 31st March, 2024, their Balance Sheet showed General Reserve of Rs. 60,000. It was decided that in future they will share profits and losses in the ratio of 3:2. Pass necessary journal entry in each of the following alternative cases:

(i) If General Reserve is not to be shown in the new Balance Sheet.

(ii) If General Reserve is to be shown in the new Balance Sheet.

Answer 18:

(i) If they do not want to show the General Reserve in the new Balance Sheet or When the partners want to transfer the general reserve to their capital A/c’s.

(ii) If they want to show General Reserve in the new Balance Sheet or when they don’t want to transfer the general reserve to their capital A/c’s and prefer to record an adjusting entry for the same.

About Solution:-

When market value of investment is less than the book value:-

(i) Fall in the value is less than investment fluctuation reserve.

(ii) Fall in the value is equal to investment fluctuation reserve.

(iii) Fall in the value is more than investment fluctuation reserve.

Things to Remember:

If fall in the value is equal to investment fluctuation fund is:-

Investment Fluctuation Fund A/c Dr.

To Investment A/c

(Being reserve transferred to Investment Account)

Important Notes:

There are three cases if market value of investment is less than book value:

1.) Fall in the value less than investment fluctuation fund.

2.) Fall in value is equal to investment fluctuation fund.

3.) Fall in value is more than investment fluctuation fund.

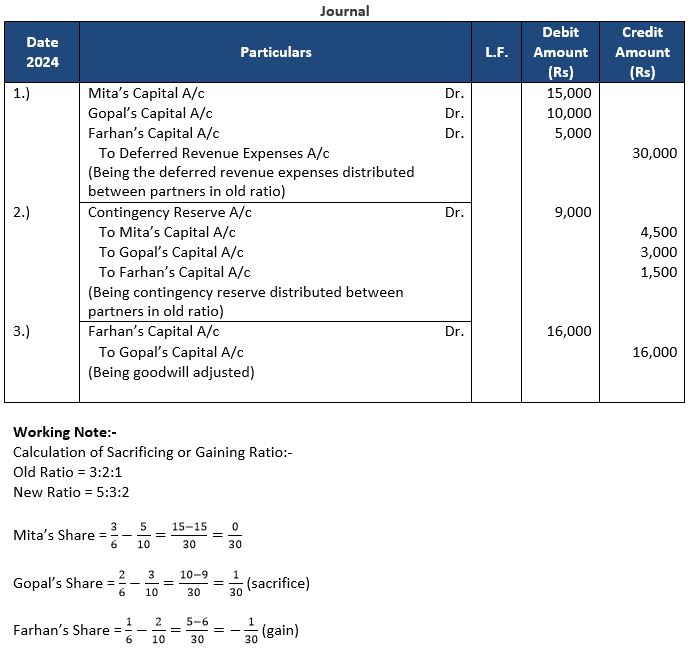

Question 19: Mita, Gopal and Farhan were partners sharing profits and losses in the ratio 3 : 2 : 1. On 31st March, 2018 they decided to change the profit sharing ratio to 5 : 3 : 2. On this date, the Balance Sheet showed Deferred Advertisement Expenditure ₹ 30,000 and Contingency Reserve ₹ 9,000.

Goodwill was valued at ₹ 4,80,000. Pass the necessary Journal entries for the above transactions in the books of the firm on its reconstitution.

Answer 19:

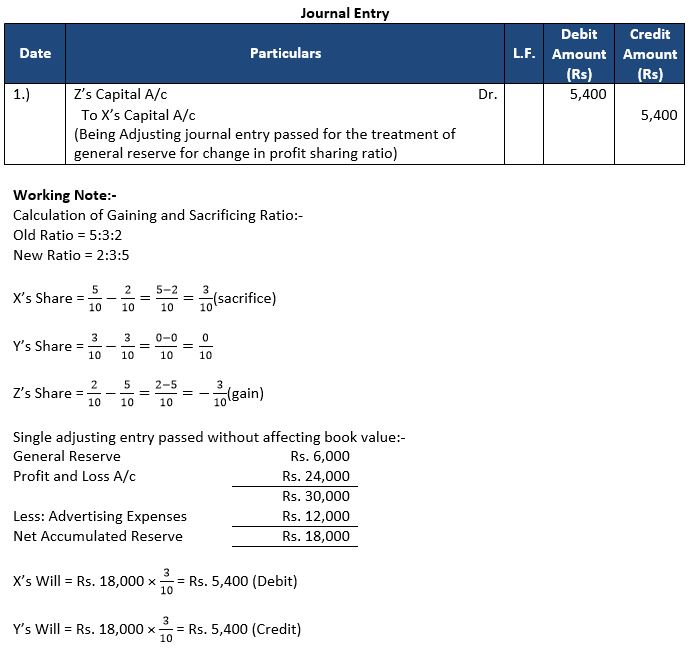

Question 20: X, Y, and Z are sharing profits and losses in the ratio of 5 : 3 : 2. They decide to share future profits and losses in the ratio of 2 : 3 : 5 with effect from 1st April, 2023. They also decide to record the effect of the following accumulated profits, losses and reserves without affecting their book values by passing a single entry.

Pass and Adjustment entry.

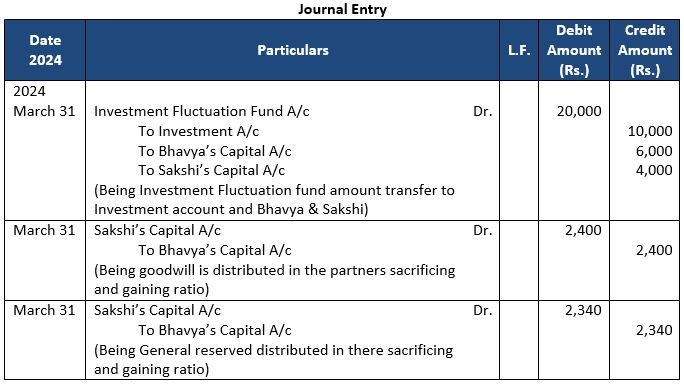

Answer 20:

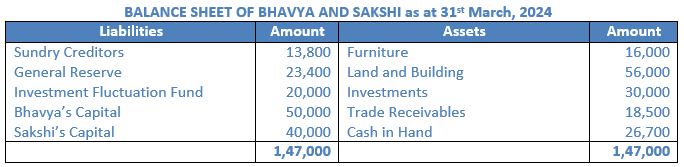

Question 21: Bhavya and Sakshi are partners in a firm, sharing profits and losses in the ratio of 3:2. On 31st March, 2024 their balance sheet was as under:

The partners have decided to change their profit sharing ratio to 1 : 1 with immediate effect. For the purpose, they decided that:

(i) Investments to be valued at Rs. 20,000.

(ii) Goodwill of the firm be valued at Rs. 24,000.

(iii) General Reserve not to be distributed between the partners.

You are required to pass necessary Journal entries in the books of the firm. Show workings.

Answer 21:

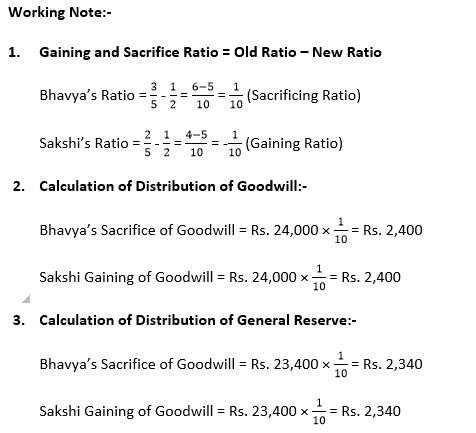

Point of Knowledge:-

Sacrificing Ratio = Old ratio – New Ratio

Things to Remember:

At time of change in profit sharing ratio the assets and liabilities of a firm is to be revalued.The reason is to realize the actual value at time of change in profit sharing ratio.

Important Notes:

When revised value are to be recorded in the books:

In the case of revaluation of assets and liabilities is to done with Revaluation Account.

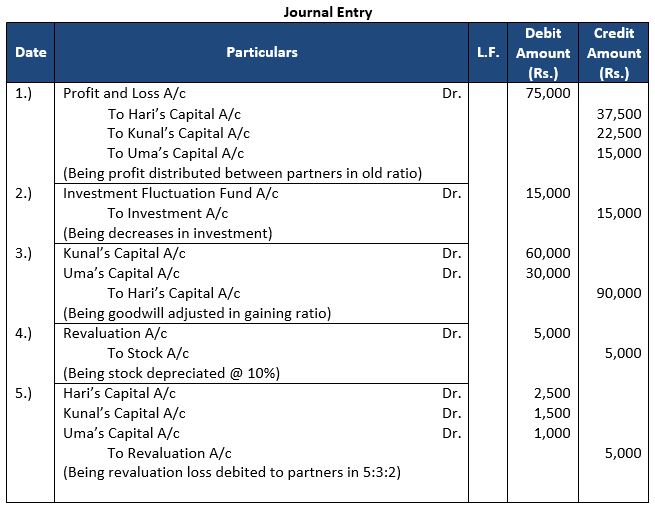

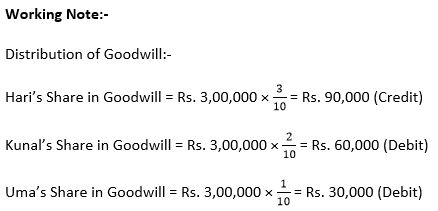

Question 22: Hari, Kunal and Uma are partners in a firm sharing profits and losses in the ratio of 5 ; 3 : 2. From 1st April 2018 they decided to share future profits and losses in the ratio of 2 : 5 : 3. Their Balance sheet showed a balance of ₹ 75,000 in the Profit and Loss Account and a balance of ₹ 15,000 in investment Fluctuation Fund. For this purpose, it was agreed that:

i) Goodwill of the firm was valued at ₹ 3,00,000.

ii) That investment (having a book value of ₹ 50,000) was valued at ₹ 35,000.

Answer 22:

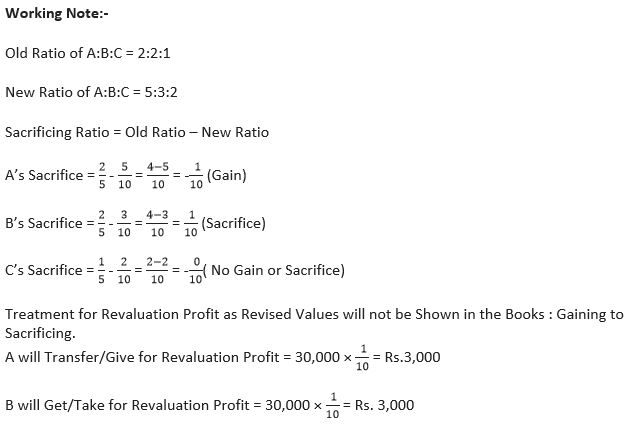

Question 23: A, B and C are partners sharing profits and losses in the ratio of 2 : 2 : 1 . They decided to share profit w.e.f. 1st April, 2024 in the ratio of 5 : 3 : 2 . They also decided not to change the values of assets and liabilities in the books of A/c. The book values and revised values of assets and liabilities as on the date of change were as follows:

Pass an adjustment entry.

Answer 23:

About Solution:-

Methods of Valuation of Goodwill: It is very difficult to assess the value of goodwill, as it is an intangible asset. In case of sale of a business, its value depends on the mutual agreement between the seller and the purchaser of the business. Usually, there are three methods of valuing goodwill:

1. Average Profit Method

2. Super Profit Method

3. Capitalisation Method

Things to Remember:

Goodwill can be classified into two categories:

(1) Purchased Goodwill, and

(2) Self-Generated Goodwill or Inherent Goodwill

Important Notes:

Purchased goodwill is the goodwill which is acquired by making a payment. For example, when a business is purchased, the excess of purchase consideration over its net assets (i.e., Assets - Liabilities) is referred to as purchased goodwill.

(i) It arises on purchase of a business.

(ii) It is recorded in the books of accounts because consideration is paid for it

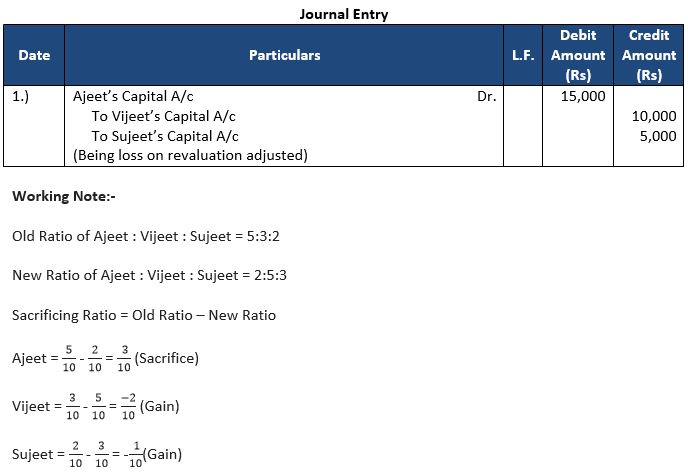

Question 24: Ajeet and Vijeet and Sujeet are partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. They decide to share profits and losses in the ratio of 2 : 5 : 3 with effect from 1st Apirl, 2023. Land (having book value of ₹ 1,00,000) was found undervalued by ₹ 2,50,000 and stock (having book value of ₹ 4,00,000) was found overvalued by ₹ 3,00,000.

Pass the necessary adjusting entry without affecting the existing book’s value.

Answer 24:

Question 25: Pinky and Rocky are partners in a firm sharing profit in the ratio of 3 : 2. Their Balance Sheet as at 31st March 2024 was as follows

Goodwill of the firm is valued at ₹ 36,000 and the building at ₹ 90,000 on 31st March, 2024. The partners decide to share profits equally with effect from 1st April, 2024.

Pass the necessary accounting entries without affecting the existing figure of building.

Answer 25:

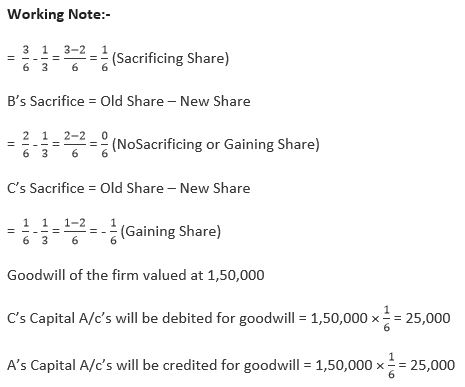

Question 26: A, B and C were partners in a firm sharing profits in the ratio of 3 : 2 : 1 . Their Balance Sheet as on 31st March, 2024 was as follows:

From 1st April, 2024, A, B and C decided to share profits equally. For this it was agreed that:

(i) Goodwill of the firm will be valued at Rs 1,50,000.

(ii) Land will be revalued at Rs 80,000 and building be depreciated by 6%.

(iii) Creditors of Rs 6,000 were not likely to be claimed and hence should be written off.

Prepare Revaluation A/c, Partners' Capital A/cs and Balance Sheet of the reconstituted firm.

Answer 26:

Working Note:-

Old Ratio of A:B:C = 3:2:1

New Ratio of A:B:C = 1:1:1

Sacrifice Ratio = Old Ratio-New Ratio

A’s Sacrifice = Old Share – New Share

About Solution:-

Goodwill is an intangible asset since it has no physical existence and cannot be seen or touched. But it is not a fictitious asset because fictitious assets do not have a value whereas goodwill has a value in case of profit making concerns. It can be sold, though a sale will be possible along with the sale of entire business.

Things to Remember:

Capitalisation Method: Under this method, goodwill can be calculated in two years

(i) By capitalising the average profits.

(ii) By capitalising the super profits.

Important Notes:

Capitalisation of Average Profits Method: Under this method first of all we calculate the average profits and then we assess the capital needed for earning such average profits on the basis of normal rate of return. Such capital is also called capitalised value of average profits. It is calculated as under:

Capitalised Value of Average Profits = Average Profit × 100 / Normal Rate of Return

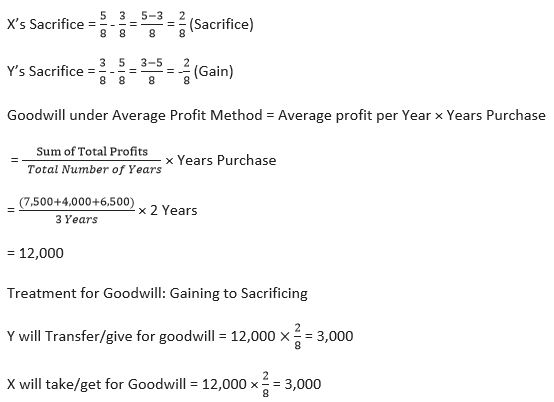

Question 27: Balance Sheet of X and Y , who share profits and losses as 5 : 3, as at 1st April, 2024 is :

On the above date, they decided to change their profit-sharing ratio to 3 : 5 and agreed upon the following :

(a) Goodwill be valued on the basis of two years' purchase of the average profit of the last three years. Profits for 2020-21——Rs. 7,500; 2021-22——Rs. 4,000; 2022-23——Rs. 6,500.

(b) Machinery and Stock be revalued at Rs. 45,000 and Rs. 8,000 respectively.

(c) Claim on A/c of workmen compensation is Rs. 6,000.

Prepare Revaluation A/c Partners' Capital A/c’s and the Balance Sheet of the new firm.

Answer 27:

Working Note:-

Old Ratio of X:Y = 5:3

New Ratio of X:Y = 3:5

Sacrificing Ratio = Old Ratio – New Ratio

About Solution:-

Super Profit Method of goodwill is calculated on the basis of surplus (excess) profits earned by a firm in comparison to average profits earned by other firms. If a business has no anticipated excess earnings, it will have no goodwill. Such excess profits are called super profits and the goodwill is calculated on the basis of super profits.

Things to Remember:

Goodwill is calculated by multiplying the Super Profits by a reasonable number of years, such as two years purchase or three years purchase etc.

Thus the Formula is:

(1) Normal Profit = Capital invested × Normal Rate of Return / 100

(2) Super Profit = Actual or Average Profit - Normal Profit

(3) Goodwill = Super Profit × No. of year purchase

Important Notes:

Capitalisation Method: Under this method, goodwill can be calculated in two years

(i) By capitalising the average profits

(ii) By capitalising the super profits

(iii) Capitalisation of Average Profits Method

(iv) Capitalisation of Super Profit Method

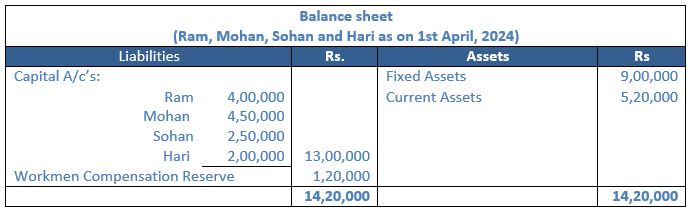

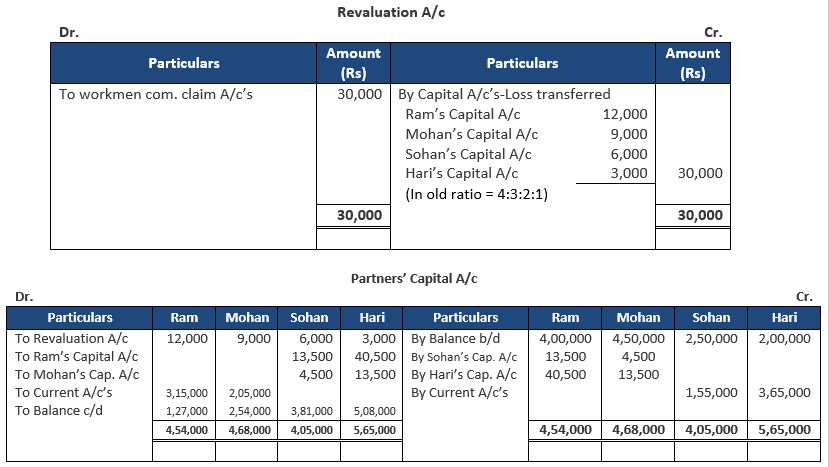

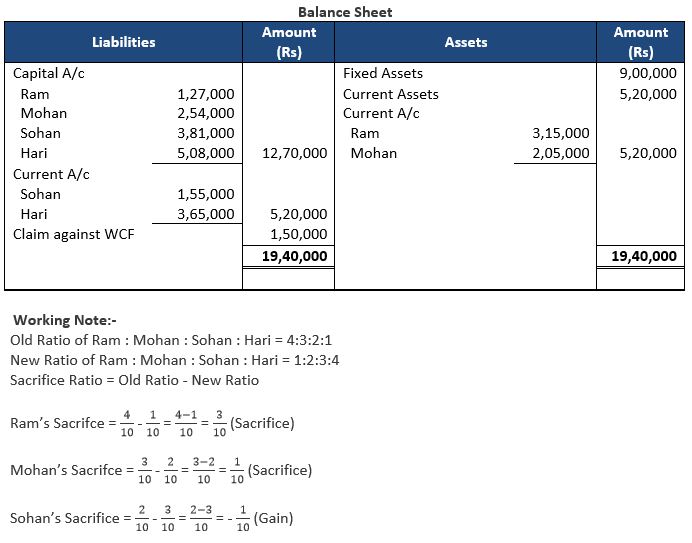

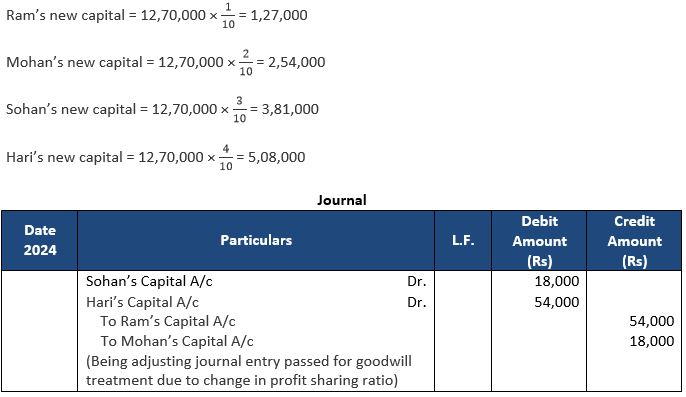

Question 28: Ram, Mohan, Sohan and Hari were partners in a firm sharing profits in the ratio of 4 : 3 : 2 : 1. On 1st April, 2024, their Balance Sheet was as follows:

From the above date, the partners decided to share the future profits in the ratio of 1 : 2 : 3 : 4 . For this purpose the goodwill of the firm was valued at Rs 1,80,000. The partners also agreed for the following:

(a) The Claim for Workmen Compensation has been estimated at Rs 1,50,000.

(b) Adjust the Capitals of the partners according to the new profit-sharing ratio by opening Partners' Current A/c’s.

Prepare Revaluation A/c , Partners' Capital A/cs and the Balance Sheet of the reconstituted firm.

Answer 28:

Total Capital of the reconstructed partnership= 4,42,000 + 4,59,000 + 2,26,000 + 1,43,000 Total Capital of the reconstructed partnership = 12,70,000

The total capital of the reconstituted firm will be in the new ratio of

Ram: Mohan: Sohan: Hari = 1:2:3:4

About Solution:-

Change in Profit Sharing Ratio among the Existing Partners: Sometimes the existing partners decide to change their profit sharing ratio. The change is necessitated due to the change in capital contribution or in active participation in management. As a result of change in profit sharing ratio, one or more of the existing partners may acquire extra share in profits at the cost of one or more of other partners. In such a case, in order to maintain equity among the partners, it is necessary to make adjustments for goodwill, revaluation of assets and liabilities, reserves, accumulated profits and losses etc. These adjustments are similar to those made at the time of admission or retirement of a partner.

Things to Remember:

Whenever there is a change in the profit sharing ratio, one or more of the existing partners have to surrender some of their old share in favour of one or more of other partners. The ratio of surrender of profit sharing ratio is called sacrificing ratio. It is calculated as follows:

Sacrificing Ratio = Old Ratio - New Ratio

Important Notes:

Adjustments required at the time of change in the profit sharing ratio: Various matters that need to be considered at the time of change in profit sharing ratio are:

(1) Determination of Sacrificing Ratio and Gaining Ratio

(2) Accounting for Goodwill

(3) Accounting Treatment of Reserves and Accumulated Profits

(4) Accounting for Revaluation of Assets and Liabilities

(5) Adjustment of Capitals

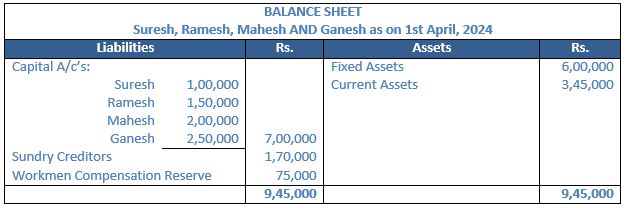

Question 29: Suresh, Ramesh, Mahesh and Ganesh were partners in a firm sharing profits in the ratio of 2:2:3:3. On 1st April, 2024, their Balance Sheet was as follows:

From the above date, the partners decided to share the future profits equally. For this purpose the goodwill of the firm was valued at Rs. 90,000. It was also agreed that:

(a) Claim against Workmen Compensation Reserve will be estimated at Rs. 1,00,000 and fixed assets will be depreciated by 10%.

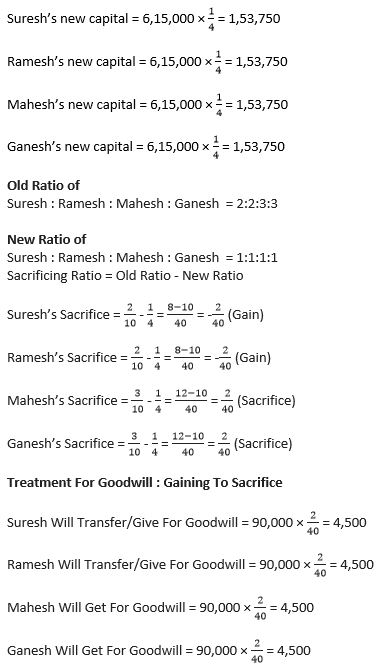

(b) The Capitals of the partners will be adjusted according to the new profit-sharing ratio. For this, necessary cash will be brought or paid by the partners as the case may be. Prepare Revaluation A/c, Partners' Capital A/c’s and the Balance Sheet of the reconstituted firm

Answer 29:

Capital Adjustment:-

Total Capital of the reconstructed partnership

= 78,500+1,28,500+1,79,000+2,29,000 = 6,15,000

The total capital of the reconstituted firm will be in the new ratio of

Suresh : Ramesh : Mahesh : Ganesh = 1:1:1:1

About Solution:-

Capital employed is not considered while calculating average profits. Average profits earned by two firms engaged in the same type of business may be the same whereas capital employed by the two firms may be different. Hence, average profits cannot be the proper base for calculation of goodwill.

Things to Remember:

Super Profits are Ignored if a firm is earning just the normal profits i.e., if it is earning the same profits as the other firms in the same business, then the firm enjoys no goodwill. The firm can claim some value of goodwill only on when it is earning super profit i.e., it is earning more than what the other firms in the same business are earning. Hence, it is desirable to value goodwill the basis of super profits and not the average profits.

Important Notes:

Number of Years of Purchase of Profits are Based on Estimates: In average profit method, average profits are multiplied by number of years (such as two or three) to find out the value of goodwill. However, the number of years of purchase used are based on estimation, hence, the value of goodwill cannot be stated as satisfactory. There should be some concrete or genuine basis for determining the number of years of purchase rather than based on estimates.

Old Questions

Question : Mandeep, Vinod and Abbas are partners sharing profits and losses in the ratio of 3 : 2 : 1 . From 1st April, 2018, they decided to share profits and losses equally. The Partnership Deed provides that in the event of any change in the profit-sharing ratio, the goodwill shall be valued at three years' purchase of the average profit of last five years. The profits and losses of the past five years are:

Profit— Year ended 31st March, 2015—Rs. 1,00,000; 2016—Rs. 1,50,000; 2018—Rs. 2,00,000; 2019—Rs. 2,00,000;

Loss — Year ended 31st March, 2017—Rs 50,000.

Pass the journal entries showing the working.

Answer:

Question : X, Y and Z are partners sharing profits and losses in the ratio of 5 : 3 : 2 , decided to share future profits and losses equally with effect from 1st April, 2018. On that date, the goodwill appeared in the books at Rs. 12,000. But it was revalue at Rs. 30,000. Pass journal entries assuming that goodwill will not appear in the books of A/c.

Answer:

Question : Jai and Raj are partners sharing profits in the ratio of 3 : 2 . With effect from 1st April, 2018, they decided to share profits equally. Goodwill appeared in the books at Rs. 25,000 . As on 1st April, 2018, it was valued at Rs. 1,00,000 . They decided to carry goodwill in the books of the firm.

Pass the journal entry giving effect to the above.

Answer:

Accounting Treatment of Reserve and Accumulated Profit

Question : X and Y are partners in a firm sharing profits and losses in the ratio of 3 : 2 . With effect from 1st April, 2018, they decided to share future profits equally. On the date of change in the profit-sharing ratio, the Profit and Loss A/c showed a credit balance of Rs 1,50,000. Record the necessary journal entry for the distribution of the balance in the Profit and Loss A/c immediately before the change in the profit-sharing ratio.

Answer:

Question : X, Y and Z share profits as 5 : 3 : 2 . They decide to share their future profits as 4 : 3 : 3 with effect from 1st April, 2018. On this date the following revaluations have taken place:

Pass necessary adjustment entry to be made because of the above changes in the values of assets and liabilities. However, old values will continue in the books.

Answer:

Question : Ashish ,Aakash and Amit are partners sharing profits and losses equally. The Balance Sheet as at 31st March, 2018 was as follows:

The partners decided to share profits in the ratio of 2 : 2 : 1 w.e.f . 1st April, 2018. They also decided that:

(i) Value of stock to be reduced to Rs 1,25,000.

(ii) Value of machinery to be decreased by 10%.

(iii) Land and Building to be appreciated by Rs 62,000.

(iv) Provision for Doubtful Debts to be made @ 5% on Sundry Debtors.

(v) Aakash was to carry out reconstitution of the firm at a remuneration of Rs 10,000.

Pass necessary journal entries to give effect to the above.

Answer:

Question : A, B and C are partners sharing profits and losses in the ratio of 5 : 3 : 2 . Their Balance Sheet as at 31st March, 2017 stood as follows:

They decided to share profits equally w.e.f. 1st April, 2017. They also agreed that:

(i) Value of Land and Building be decreased by 5% .

(ii) Value of Machinery is increased by 5%.

(iii) A Provision for Doubtful Debts be created @ 5% on Sundry Debtors.

(iv) A Motor Cycle valued at Rs 20,000 was unrecorded and is now to be recorded in the books.

(v) Out of Sundry Creditors, Rs 10,000 is not payable.

(vi) Goodwill is to be valued at 2 years' purchase of last 3 years profits. Profits being for 2016-17—Rs 50,000 (Loss); 2015-16—Rs 2,50,000 and 2014-15—Rs 2,50,000.

(vii) C was to carry out the work for reconstituting the firm at remuneration (including expenses) of Rs 5,000. Expenses came to Rs 3,000.

Pass Journal entries and prepare Revaluation A/c.

Answer:

Preparation of Balance Sheet:

Question : X, Y and Z are partners sharing profits and losses in the ratio of 7 : 5 : 4 . Their Balance Sheet as at 31st March, 2018 stood as:

Partners decided that with effect from 1st April, 2018 , they will share profits and losses in the ratio of 3 : 2 : 1 . For this purpose, goodwill of the firm was valued at Rs 1,50,000. The partners neither want to record the goodwill nor want to distribute the General Reserve and profits.

Answer:

Question : A and B are partners sharing profits in the ratio of 4 :3 . Their Balance Sheet as at 31st March, 2018 stood as:

They decided that with effect from 1st April, 2018, they will share profits and losses in the ratio of 2 : 1. For this purpose they decided that:

(i) Fixed Assets are to be depreciated by 10%.

(ii) A Provision for Doubtful Debts of 6% be made on Sundry Debtors.

(iii) Stock be valued at Rs. 1,90,000.

(iv) An amount of Rs. 3,700 included in Creditors is not likely to be claimed.

Partners decided to record the revised values in the books. However, they do not want to disturb the Reserve. You are required to pass journal entries, prepare Capital A/c’s of Partners and the revised Balance Sheet.

Answer:

Question : X, Y and Z are partners in a firm sharing profits and losses as 5 : 4 : 3 . Their Balance Sheet as at 31st March, 2018 was:

From 1st April, 2018, they agree to alter their profit-sharing ratio as 4 : 3 : 2 .It is also decided that :

(a) Furniture be taken at 80% of its value .

(b) Stock be appreciated by 20%.

(c) Plant and Machinery be valued at Rs. 4,00,000.

(d) Outstanding Expenses be increased by Rs. 13,000.

Partners agreed that altered values are not to be recorded in the books and they also do not want to distribute the General Reserve.

You are required to pass a single journal entry to give effect to the above. Also, prepare Balance Sheet of the new firm.

Answer:

Adjustment of Capital

Question : Following is the Balance Sheet of A and B , who shared Profits and Losses in the ratio of 2 : 1 , as at 1st April, 2019:

On the above date, the partners changed their profit-sharing ratio to 3 : 2 . For this purpose, the goodwill of the firm was valued at Rs 3,00,000 . The partners also agreed for the following:

(a) The value of Land and Building will be Rs 5,00,000;

(b) Reserve is to be maintained at Rs 3,00,000.

(c) The total capital of the partners in the new firm will be Rs 6,00,000 , which will be shared by the partners in their new profit-sharing ratio .

Prepare Revaluation A/c , Partners' Capital A/c’s and the Balance Sheet of the reconstituted firm.

Answer: