Read TS Grewal Solution Class 12 Chapter 6 Retirement of a Partner 2026. Students should study TS Grewal Solutions Class 12 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 12 Accountancy have been prepared by expert teachers. These TS Grewal Class 12 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 12 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 12 Accounts Chapter 6 Retirement of a Partner TS Grewal Solutions

TS Grewal Solutions for Chapter 6 Retirement of a Partner Class 12 Accounts have been provided below based on the latest TS Grewal Class 12 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 12 will help students to improve their concepts and easily solve accountancy questions for Class 12.

Chapter 6 Retirement of a Partner TS Grewal Class 12 Solutions

About this chapter: TS Grewal Class 12 Chapter 6 provides all details relating to the concept of the Retirement of a Partner from a partnership firm. It is very important topic for Class 12 commerce students. As explained in the chapter the Retirement of a partner from a partnership firm can happen due to various reasons, including personal reasons, health issues, or the desire to pursue other opportunities. There are detailed notes relating to legal and accounting provisions related to the retirement of a partner, such as the rights and liabilities of the retiring partner and the remaining partners. The accounting matters such as different methods of settling the accounts of the retiring partner, including the gaining ratio and the sacrificing ratio, treatment of accumulated profits and losses, goodwill, and revaluation of assets and liabilities have been explained in detail.

The chapter provides various practical examples and questions that can help students understand the concepts better. It is essential for students to practice these questions and understand the various scenarios that can arise during the retirement of a partner. Our teachers have provided detailed solutions to all the questions given in the chapter so that the students can solve the questions and then compare their answers with what we have provided below.

Partner’s Capital A/c………………………….Dr.

To Goodwill A/c

(Being the existing goodwill written off)

Question 10. Why the value of goodwill needs to be determined on retirement or death of a partner?

Answer:

At the time of retirement or death of a partner, adjustment is necessary for goodwill. When a partner retires of dies, his share in profit is taken by the continuing partners for which they should compensate the retiring or deceased partner.

Question 11. For which share of goodwill a partner is entitled at the time of retirement?

Answer:

The retiring or deceased partner is entitled to his share of goodwill at the time of retirement/death because goodwill has been earned by the firm at the time when he was a partner.

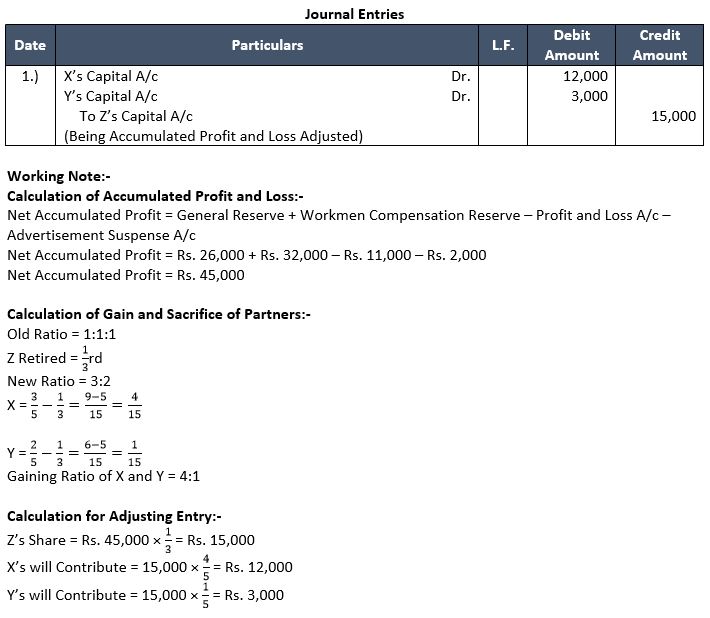

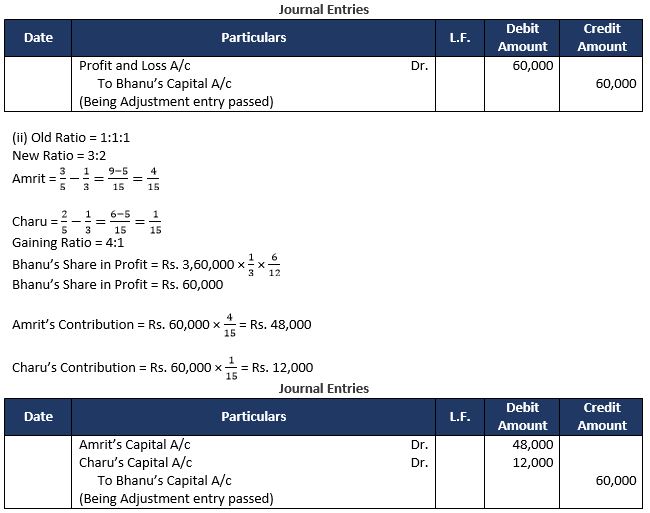

Question 12. Neetu, Meetu and Teetu were partners in a firm. On 1st January, 2018, Meetu retired. On Meetu’s retirement the goodwill of the firm was valued at Rs. 4,20,000.

Pass necessary Journal entry for the treatment of goodwill on Meetu's retirement.

Question 13. Give two circumstances in which the gaining ratio may be applied.

Calculation of Gaining Ratio under below circumstances:-

1.) When a partner retires or dies.

2.) When there is a change in the profit-sharing ratio.

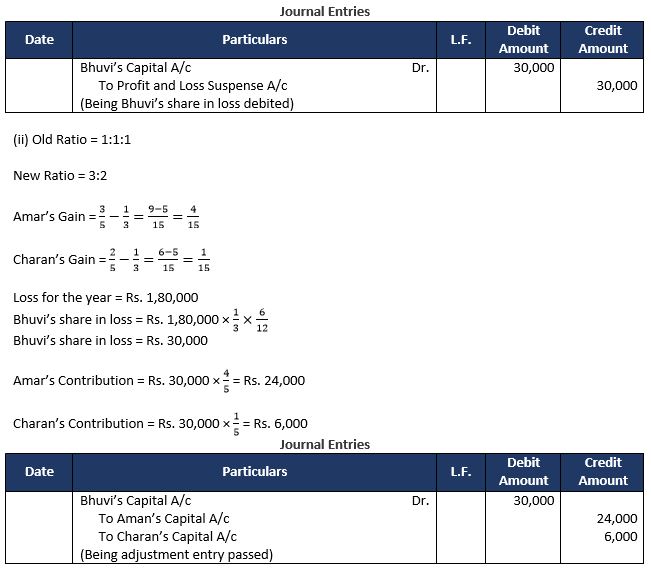

Question 14. Why the revaluation of assets and reassessment of liabilities are required at the time of retirement or death of a partner?

At the time of retirement or death of a partner, assets of the firm are revalued and liabilities are reassessed with a purpose that the retiring partner is not at an advantage of disadvantage because of the change in the value.

Question 15. Give the Journal entry to distribute ‘Workmen Compensation Reserve’ of Rs. 60,000 at the time of retirement of Sajjan, when there is no claim against it. The firm has three partners Rajat, Sajjan and Kavita.

Working Note:-

1.) Rajat’s Share in Workmen Compensation Reserve = 60,000 × 1/3 = 20,000

2.) Sajjan’s Share in Workmen Compensation Reserve = 60,000 × 1/3 = 20,000

3.) Kavita’s Share in Workmen Compensation Reserve = 60,000 × 1/3 = 20,000

Question 16. State any two deductions that may have to be made from the amount payable to a retiring partner.

Deduction that may have to be made from the amount payable to a retiring partner:-

1.) Loss on revaluation

2.) Goodwill to be written off

Question 17. How is share in profit of outgoing partner calculated when he retires during the accounting year?

Profit of outgoing partner calculated when he retires during the accounting year:-

1) Change in the Profit-sharing ratio, i.e. determining New Profit-sharing Ratio and Gaining Ratio.

2) Valuation and Adjustment of goodwill.

3) Revaluation of Assets and Reassessment of liabilities.

4) Reserves and Undistributed Profit.

Question 18. Jamuna, Ganga and Krishna are partners in a firm. Krishna retired from the firm. After making adjustments for Reserve and Revaluation of Assets and Liabilities the balance in krishna’s capital account was Rs. 1,20,000. Jamuna and Ganga paid Rs. 1,80,000 in full settlement to Krishna. Identify the item for which Jamuna and Ganga paid Rs. 60,000 more to Krishna.

Rs. (1,80,000- 1,20,000) = Rs. 60,000

Krishna’s Share of Goodwill which is paid by Jamuna and Ganaga.

Short Answer Type Questions

Question 1. Explain the Procedure of determining the amount payable to a retiring partner when he leaves the firm.

Amount payable to a retiring partner when he leaves the firm:-

1.) Change in the Profit-sharing ratio i.e. determining New Profit-sharing Ratio and Gaining ratio.

2.) Valuation and Adjustment of Goodwill.

3.) Revaluation of assets and Reassessment of Liabilities.

4.) Reserves and Undistributed Profit (Accumulated Profit/losses)

5.) Computation of retiring Partner’s Internet and Payments to the Retiring Partner.

6.) Adjustment of Capital.

Question 2. Explain the accounting treatment of goodwill on retirement of a partner.

For Accounting Treatment of Goodwill, guidelines of Accounting Standard-26 on Accounting for intangible Assets are followed.

When goodwill does not appear in the books:-

When Goodwill does not appear in the Balance Sheet, there are three ways in which the retiring or deceased partner can be given the credit for his share of goodwill as follows:

(a) Goodwill Account is not Raised in the books of Account: Retiring or deceased partner’s share of the current value of Goodwill is credited to his Capital Account by debiting Gaining Partner’s Capital in their gaining ratio.

Gaining Partners’ Capital A/c…………………..Dr.

To Retiring/Deceased Partner’s Capital A/c

(Being the share of goodwill credited to retiring/deceased partner debiting gaining partner’s Capital account in their gaining ratio)

(b) Goodwill is Raised at its Full Value and Written off: Goodwill Account is debited with the current value of goodwill, crediting Capital Accounts of all the partners, including retiring or deceased partner in their old profit-sharing ratio. Goodwill account so debited is immediately written off by debiting continuing partners capital account, in their new profit-sharing ratio and crediting goodwill account with its current value.

Goodwill A/c…………………..Dr.

To All Partner’s Capital A/c

(Being the goodwill raised at its current value)

Continuing Partner’s Capital A/c…………………..Dr.

To Goodwill A/c

(Being the goodwill Account written off in new profit-sharing ratio)

When goodwill appears in the books:-

Goodwill appearing in the books of account means it is purchase goodwill because self-generated goodwill is not recorded in the books of account following AS-26, Intangible Assets. Goodwill appearing in the books of account is written off by debiting all the partners’ Capital Accounts including retiring or deceased partner in their old profit-sharing ratio. The journal entry passed is:

All Partners’ Capital A/c………………..Dr.

To Goodwill A/c

(Being the existing goodwill written off)

Question 3. Why are assets and liabilities revalued on the retirement or death of a partner?

At the time of retirement or death of a partner, assets of the firm are revalued and liabilities are reassessed with a purpose that the retiring partner is not at an advantage or disadvantage because of the change in the values. To give effect to the change in value, a Profit and Loss Adjustment Account and Revaluation Account is prepared in the same manner is prepared at the time if admission of a partner. To recapitulate:

1.) Increase in the value of assets, unrecorded assets, decrease in amount of liabilities and excess provisions written back are credited to Revaluation Account.

2.) Decrease in value of assets, increase in amount of liabilities, liabilities provided and unrecorded liabilities are debited to it.

3.) Gain or loss from the revaluation is distributed among the partners in their old profit-sharing ratio. Gain on revaluation is credited to the Partners’ Capital Account or Partner’s Current Accounts.

4.) After revaluation, assets and liabilities are shown at their revised value in new balance sheet of the firm.

Question 4. Distinguish between the sacrificing ratio and the gaining ratio among partners.

EXERCISE................

Question 1: Gita, Radha and Garv were partners sharing profits in the ratio of 1/2, 2/5 and 1/10. Find the new ratio of the remaining partners if C retires.

Answer 1:

If Garv retires then the New Profit Sharing Ratio will be Gita:Radha = 5:4

About Solution:-

The ratio of remaining partners is known as New Profit Sharing Ratio, in which they will share the future profits. When a partner retires from the firm, the remaining partners acquired share of retiring partner either in their old ratio or in specified ratio.

Things to Remember:

All free reserves and profits given in the liabilities side should be credited to Partner's Capital Accounts or Current Account (If Capitals are fixed) and all fictitious assets/ accumulated losses should be debited to the Partner's Capital Account or Current Account (If Capitals are fixed) in their old ratios.

Important Notes:

Treatment of Revaluation of Assets and Re-assessment of liabilities and Preparation of Revaluation Account is same as we have done in case of Admission of a partner. In case of Retirement also we will distribute Revaluation Profits/Losses to all the partners in their old ratios.

Question 2: From the following particulars, calculate new profit-sharing ratio of the partners:

(a) Shiv, Mohan and Hari were partners in a firm sharing profits in the ratio of 5:5:4. Mohan retired and his share was divided equally between Shiv and Hari.

(b) P, Q and R were partners sharing profits in the ratio of 5:4:1. P retires from the firm.

Answer 2:

(a) Old Ratio of Shiv: Mohan: Hari = 5:5:4

(b) Old Ratio of P: Q: R = 5:4:1

Therefore New Ratio of Q : R = 4:1

About Solution:-

Change in Profit Sharing Ratio in the event of admission of a Partner: In the event of admission of a partner in the existing firm, the incoming partner becomes entitled to share future profits of the firm.

Things to Remember:

Such share is acquired by the incoming partner from old partners, therefore, it is necessary to determine new profit sharing ratio and also the gaining or sacrificing ratio. The new partner may acquire his share from old partner or partners in old ratio, in a particular ratio (sacrificing ratio) or in a particular fraction from old partners.

Important Notes:

Old partners will continue to share balance profits or losses in their old profit sharing ratio. It means that, in the absence of any information, profit sharing ratio among the existing partners remains unchanged.

Question 3: R, S and M are partners sharing profits in the ratio of 2/5,2/5 and 1/5. M decides to retire from the business and his share is taken by R and S in the ratio of 1:2. Calculate the new profit-sharing ratio.

Answer 3:

Old Ratio of R:S:M = 2:2:1

About Solution:-

In such situation, share of existing or old partners will change to the extent of share sacrificed on admission of the new or incoming partner.

Things to Remember:

New share of profits of the existing partners in the reconstituted firm is determined by deducting the sacrifice made by them from their existing share of profits.

Important Notes:

In such situation, share of new or incoming partner is to be determined by adding the shares surrendered by the old partners in favour of new or incoming partner.

Question 4: X, Y and Z are partners sharing profits in the ratio of 1/2, 3/10, and 1/5. Calculate the gaining ratio of remaining partners when Y retires from the firm.

Answer 4:

About Solution:-

Total of shares surrendered by all the partners in favour of new or incoming partner is considered as the share of new or incoming partner.

Things to Remember:

In the event of admission of a partner in a partnership firm, some partners sacrifice while some partners gain.

Important Notes:

Gain in profit share can be calculated from such shares sacrificed by the partners or where old and new share is given, by using the below mentioned formula:

Gaining Share = New Share - Old Share

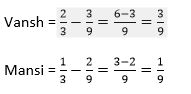

Question 5: Sarthak, Vansh and Mansi were partners sharing profits in the ratio of 4:3:2. Sarthak retires. Vansh and Mansi will share future profits in the ratio of 2:1. Determine the gaining ratio.

Answer 5:

Old Ratio of A:B:C = 4:3:2

New Ratio of B:C = 2:1

Gaining Ratio = New Ratio – Old Ratio

Question 6:

(a) W, X, Y and Z are partners sharing profits and losses in the ratio of 1/3, 1/6, 1/3 and 1/6 respectively. Y retires and W, X and Z decide to share the profits and losses equally in future. Calculate gaining ratio.

(b) A, B and C are partners sharing profits and losses in the ratio of 4:3:2. C retires from the business. A is acquiring 4/9 of C's share and balance is acquired by B. Calculate the new profit-sharing ratio and gaining ratio.

Answer 6:

About Solution:-

In case of change in profit sharing ratio among the partners or admission or retirement/death of a partner, goodwill is not to be raised in the books of the firm as no consideration in money or money's worth is paid for it. If goodwill is raised, it should be immediately written off.

Things to Remember:

Accounting Treatment of Goodwill at the time Of Admission Of a Partner: In the event of admission of a partner, new partner who acquires the share in future profits from the existing partners should compensate sacrificing partners by paying them an amount. This amount paid by the incoming partner is termed as Goodwill or Premium for Goodwill. Accounting treatment of such Goodwill has been explained with respect to 5 situations which may arise in the event of partner's admission.

Important Notes:

Goodwill (Premium on Goodwill) is paid privately;

Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is retained in business;

Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is withdrawn by Sacrificing Partners fully or partly;

Goodwill (Premium on Goodwill) is brought in kind;

Goodwill (Premium on Goodwill) is not brought in full or a part by the new or Incoming Partner.

Question 7: Kumar, Lakshya, Manoj and Naresh are partners sharing profits in the ratio of 3:2:1:4. Kumar retires and his share is acquired by Lakshya and Manoj in the ratio of 3:2. Calculate new profit-sharing ratio and gaining ratio of the remaining partners.

Answer 7:

Old Ratio of Kumar : Lakshya : Manoj : Naresh = 3:2:1:4

About Solution:-

Goodwill existing in the books of the firm is written off by debiting Old Partners' Capital Account/Current Account in their Old Profit Sharing Ratio and crediting Goodwill Account.

Old Partners' Capital/Current A/c Dr. (in Old Ratio)

To Goodwill A/c

Things to Remember:

Accounting Treatment when Goodwill (Premium on Goodwill) is paid privately: In this situation, Goodwill (Premium on Goodwill) is paid by the new or Incoming Partner privately to the sacrificing partners. In such situation, journal entry is not passed in the books of account of the firm.

Important Notes:

Accounting Treatment when Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is retained in business: In this situation, either of the 2 options are to be followed to record the accounting treatment of Goodwill:

Amount brought in by the new or Incoming Partner is transferred to Capital Accounts Of the sacrificing partners in their sacrificing ratio. Following entries are to be passed:

Brought in cash by the new or incoming partner:

1.) Cash/Bank A/c . Dr. [With share of Goodwill]

To Premium for Goodwill A/c

2.) Capital brought in cash by the new or Incoming Partner:

Cash/Bank A/c . Dr. [With Capital brought in Cash]

To New Partner's Capital A/c

Question 8: A, B, and C were partners in a firm sharing profits in 8:4:3. B retires and his share is taken up equally by A and C. Find the new profit-sharing ratio.

Answer 8:

Old Ratio of A:B:C = 8:4:3

About Solution:-

Amount of Goodwill is credited to the New Partner's Capital Account and thereafter, adjusted in favour of Old or existing partners in their sacrificing ratio for which following entries are passed:

i. Cash/Bank A/c Dr.

To New Partner's Capital

ii. New Partner's Capital A/ Dr.

To Sacrificing Partner's Capital/Current A/c (Individually)

(Being the goodwill brought by new partner distributed

among the sacrificing partners in their sacrificing ratio)

Things to Remember:

Accounting Treatment when Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is withdrawn by Sacrificing Partners fully or partly: Such amount of premium brought in by the new or incoming partner is shared by the sacrificing partners in the sacrificing ratio. These sacrificing partners may withdraw the premium amount fully or partly.

Important Notes:

Accounting Treatment when Goodwill (Premium on Goodwill) is brought in kind: In such situation, the assets brought in are debited individually with their values and Premium for Goodwill Account is credited with his share of goodwill and also new Partner's Capital Account with his capital. Such Premium for Goodwill is transferred to the Capital Accounts of the sacrificing partners in their sacrificing ratio.

About Solution:-

Accounting Treatment when Goodwill (Premium on Goodwill) is not brought in full or a part by the new or Incoming Partner: In such case, premium for goodwill account is credited with the amount of premium for goodwill brought by the new or incoming partner. Transfer entry is to be passed by debiting New or Incoming Partner's Capital/Current Account with the amount of premium on goodwill not brought by him besides debiting premium for Goodwill Account with the amount of premium paid by him. Where, Fixed Capital Accounts method is used for maintaining Capital Accounts, it is debited to his Current Account.

Things to Remember:

Revaluation of assets and reassessment of liabilities is to be done. The net increase or decrease is then adjusted in the existing partner's capital account in their old profit sharing ratio.

Important Notes:

Change in Profit Sharing Ratio in the event of admission of a Partner: In the event of admission of a partner in the existing firm, the incoming partner becomes entitled to share future profits of the firm. Such share is acquired by the incoming partner from old partners, therefore, it is necessary to determine new profit sharing ratio and also the gaining or sacrificing ratio. The new partner may acquire his share from old partner or partners in old ratio, in a particular ratio (sacrificing ratio) or in a particular fraction from old partners.

Question 10: Murli, Naveen and Omprakash are partners sharing profits in the ratio of 3/8, 1/2 and 1/8. Murli retires and surrenders 2/3rd of his share in favour of Naveen and remaining share in favour of Omprakash. Calculate new profit-sharing ratio and gaining ratio of the remaining partners.

Answer 10:

About Solution:-

When old ratio and new ratio of the old and existing partners is available, sacrificing ratio is to be calculated by deducting the new share from the old share.

Formula used is as follows:

Sacrificing Share = Old Share - New Share

Things to Remember:

The share surrendered by the partner is deducted from his old share of profit to determine his share in the reconstituted firm.

Total of shares surrendered by all the partners in favour of new or incoming partner is considered as the share of new or incoming partner.

Important Notes:

Like admission and changes in profit sharing ratio in case of retirement or death also the existing partnership deep comes to end and the new once comes into exist- tense among the remaining partner. There is not much difference in the accounting treatment at the time of retirement or in the event of death.

Question 11: P, Q and R are partners sharing profits in the ratio of 7:5:3. P retires and it is decided that profit sharing ratio between Q and R will be same as existing between P and Q. Calculate New Profit sharing ratio and Gaining Ratio.

Answer 11:

Old Ratio of P : Q : R = 7 : 5 : 3

New Ratio of Q : R = 7 : 5

Gaining Ratio = New Ratio – Old Ratio

Q’s Gain = New Share – Old Share = 7 / 12 - 5 / 15 = 35 - 20 / 60 = 15 / 60

R’s Gain = New Share – Old Share = 5 / 12 - 3/15 = 25 - 12 / 60 = 13 / 60

Gaining Ratio of Q : R = 15:13

Treatment of Goodwill

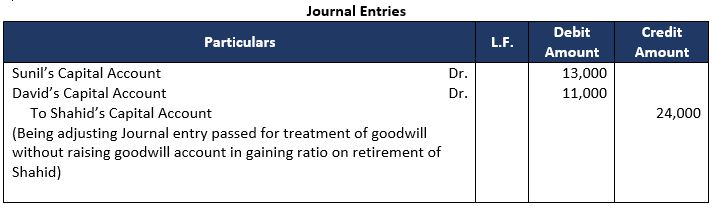

Question 12: Sunil, Shahid and David are partners sharing profits and losses in the ratio of 4:3:2. Shahid retires and the goodwill is valued at Rs. 72,000. Calculate Shahid's share of goodwill and pass the necessary Journal entry for Goodwill. Sunil and David decided to share the future profits and losses in the ratio of 5:3.

Answer 12:

Points of Knowledge:

Old Ratio of L:M:O = 4:3:2

New Ratio of L:O = 5:3

Gaining Ratio = New Ratio – Old Ratio

L’s Gain = 5/8 - 4 / 9 = 45-32 / 72 = 13 / 72

O’s Gain = 3/8 - 2 / 9 = 27-16 / 72 = 11 / 72

Therefore, Gaining Ratio of L:O = 13:11

Goodwill of the firm = 72,000

M’s Share of goodwill = 72,000 × 3/9 = 24,000

L will transfer for goodwill to M = 24,000 × 13 / 24 = 13,000

O will transfer for goodwill to M = 24,000 × 11 / 24 = 11,000

Condition for goodwill treatment: Remaining Partners to Retiring Partner

About Solution:-

Like admission and changes in profit sharing ratio in case of retirement or death also the existing partnership deep comes to end and the new once comes into exist- tense among the remaining partner.

Things to Remember:

Treatment at the time of retirement or in the event of death, Amount due to Retiring/Deceased Partner (To be credited to his capital account)

1. Credit Blanca of his capital.

2. Credit Balance of his current account (if any).

3. Share of Goodwill. (By gaining partners)

4. Share of Reserves of Undistributed profits.

5. His share in the profit on revaluation of assets and liabilities.

6. Share in profits up to the date of Retirement/Death. (By p & L suspense A/c)

7. Interest on capital if involved.

8. Salary if any

Important Notes:

Treatment at the time of retirement or in the event of death.

Deduction from the above sum (to be debited to capital account)

1. Debit balance of his current account (if any)

2. Share of existing Goodwill to be written off.

3. Share of accumulated loss.

4. Drawing and interest on drawings (if any)

5. Share of loss on account of Revaluation of assets and liabilities.

6. His share of business loss up to the date of Retirement/Death (Top & L) suspense A/C)

Question 13: P, Q, R and S were partners in a firm sharing profits in the ratio of 5:3:1:1. On 1st January, 2023, S retired from the firm. On S's retirement the goodwill of the firm was valued at Rs. 4,20,000. The new profit-sharing ratio between P, Q and R will be 4:3:3. Showing your working notes clearly, pass necessary journal entry for the treatment of goodwill in the books of the firm on S's retirement.

Answer 13:

Points of Knowledge:

Old Ratio of P:Q:R:S = 5:3:1:1

New Ratio of P:Q:R = 4:3:3

Gaining Ratio = New Ratio – Old Ratio

P’s Gain = 4/10 - 5/10 = 4-5 / 10 = - 1 / 10 (Sacrifice)

Q’s Gain = 3/10 - 3/10 = 3-3 / 10 = 0 / 10

R’s Gain = 3/10 - 1/10 = 3-1 / 10 = 2 / 10

S’s Sacrifice = 1/10

Therefore Sacrificing Ratio of P:S = 1:1

Goodwill treatment: Gaining partner to Sacrificing partner

Goodwill of the firm = 4,20,000

R’s Capital Account debited for goodwill = 4,20,000 × 2 / 10 = 84,000

P’s Capital Account credited for goodwill = 4,20,000 × 1 / 10 = 42,000

S’s Capital Account credited for goodwill = 4,20,000 × 1 / 10 = 42,000

About Solution:-

This outgoing partners A/c is settled as per the terms of partnership deed. Three cases may be there as given below-

When the retiring partner is paid full amount either in cash or by cheque:-

Retiring Partner’s Capital A/c Dr.

To Cash Bank A/c

Things to Remember:

When the retiring partner is paid nothing in cash then the whole amount due is transferred to his loan A/c.

Retiring Partner’s Capital A/c Dr.

To retiring partner’s Loan A/c

Important Notes:

When Retiring Partner is partly paid in cash and the remaining amount in treated Loan.

Retiring Partner’s Capital A/c Dr. (Total Amount due)

To Cash Bank A/c (Amount Paid)

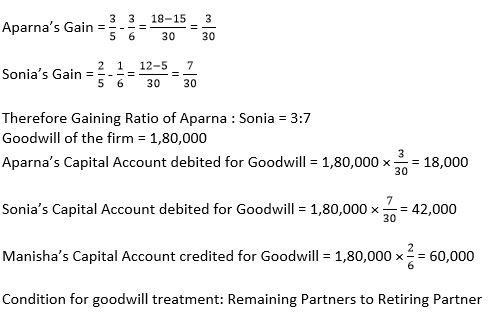

Question 14: Aparna, Manisha and Sonia are partners sharing profits in the ratio of 3:2:1. Manisha retires and goodwill of the firm is valued at Rs 1,80,000. Aparna and Sonia decided to share future profits in the ratio of 3:2. Pass necessary journal entries.

Answer 14:

Old Ratio of Aparna : Manisha : Sonia = 3:2:1

New Ratio of Aparna : Sonia = 3:2

Gaining Ratio = New Ratio – Old Rati

About Solution:-

Loan of the retiring partner is disposed of accordingly of the pre decided term and conditions among the partners. Normally the Principal amount is paid in few equal instalments. In such cases interest is credited to the Loan A/c on the basic of the amount outstanding at the beginning of each year and the amount paid it debited to loan A/c.

Things to Remember:

Journal entries are done

For interest on Loan.

Interest A/c Dr.

To Retiring partner’s Loan A/c

Important Notes:

Accounting treatment in the case of death is same as in the case of return except theFollowing:-

The deceased partners claim is transferred to his executer’s account. Normally the retirement takes place at the end of the Accounting pried but the death may occur at any time. Hence the claim of deceased part shall also include his share or profit or loss, interest on capital drawings if any from the date of the last balance sheet to the date his death.

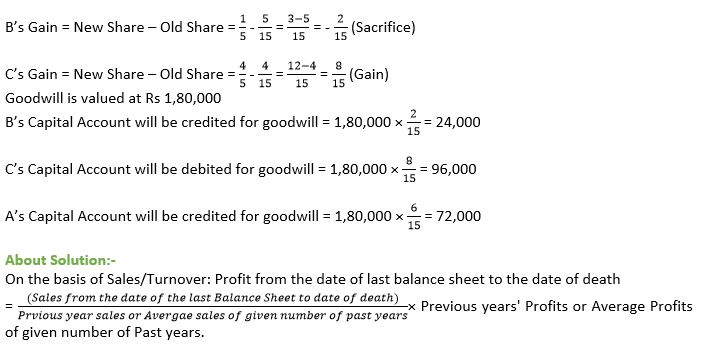

Question 15: A, B and C are partners sharing profits in the ratio of 3 : 2 : 1 . B retired and the new profit-sharing ratio between A and C was 2 : 1 . On B's retirement, the goodwill of the firm was valued at Rs. 90,000. Pass necessary journal entry for the treatment of goodwill on B's retirement.

Answer 15:

About Solution:-

Calculation of profit/Loss for the intervening Period:-

It is calculated by any one of the two methods given below:

1. On Time Basis: In this method proportionally profit for the time period is calculated either on the basis of last year’s profit or on basis of average profits of last few years and then deceased profit share is calculated based on his share of profits.

2. On Turnover or Sales Basis: In this method the profits upto the date of death for the

Things to Remember:

Current year are calculated on the basis of current year’s sales upto the date of death by using the formula.

Profits for the current year upto the date of death

= Sales of the current year upto the date of death / Total sales of last year × Profit for the last year

Important Notes:

When the retiring partner is paid nothing in cash then the whole amount due is transferred to his loan A/c

Retiring Partner’s Capital A/c Dr.

To Retiring partner’s Loon A/c

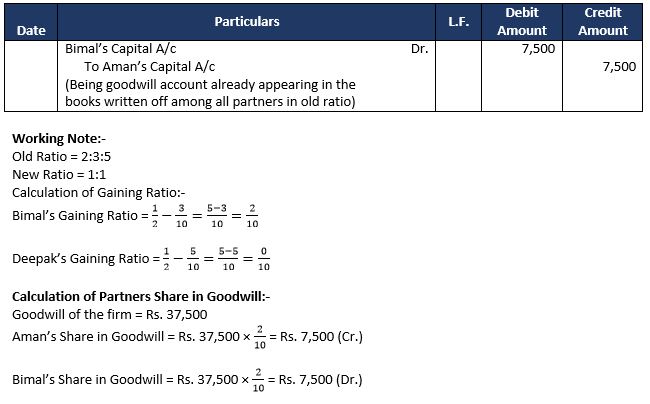

Question 16: Aman, Bimal and Deepak are partners sharing profits in the ratio of 2:3:5. The goodwill of the firm has been valued at Rs. 37,500. Aman retired, Bimal and Deepak decided to share profits equally in future. Calculate gain/sacrifice of Bimal and Deepak on Aman’s retirement and also pass necessary Journal entry for the treatment of goodwill.

Question 16:

Question 17: A, B and C are partners sharing profits in the ratio of 4/9 : 3/9 : 2/9. B retires and his capital after making adjustments for reserves and gain (profit) on revaluation stands at Rs 1,39,200. A and C agreed to pay him Rs 1,50,000 in full settlement of his claim. Record necessary journal entry for adjustment of goodwill if the new profit-sharing ratio is decided at 5 : 3.

Answer 17:

About Solution:-

Goodwill given in the Balance Sheet of the firm should be debited all old partners in their old ratio. (Same treatment as in case of change in profit sharing ratio and admission of a partner).

Things to Remember:

Treatment of Hidden goodwill, All free reserves and profits given in the liabilities side should be credited to Partner's Capital Accounts or Current Account (If Capitals are fixed) and all fictitious assets/ accumulated losses should be debited to the Partner's Capital Account or Current Account (If Capitals are fixed) in their old ratios.

Important Notes:

Treatment of Revaluation of Assets and Re-assessment of liabilities and Preparation of Revaluation Account is same as we have done in case of Admission of a partner.

In case of Retirement also we will distribute Revaluation Profits/Losses to all the partners in their old ratios.

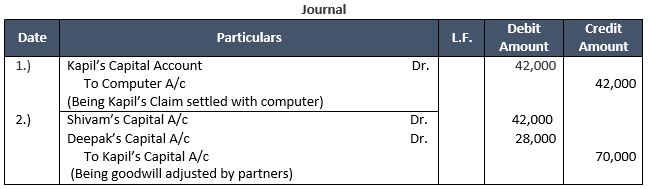

Question 18: Shivam, Kapil and Deepak are partners sharing profits in the ratio of 3:1:2. On 31st March, 2024, Kapil retired and his capital account after adjustments of reserve and profit on revaluation was Rs. 3,50,000. Shivam and Deepak paid him Rs. 4,20,000 in settlement of his claim. To settle his account, a computer of Rs. 4,20,000 was given to Kapil. Pass the necessary Journal entries in the books of the firm.

Answer 18:

Working Note:-

Old Ratio = 3:1:2

New Ratio = 3:2

Gaining Ratio = 3:2

Calculation of Hidden Goodwill:-

Goodwill of Kapil = Rs. 4,20,000 – Rs. 3,50,000

Goodwill of Kapil = Rs. 70,000

Contribution of Shivam and Deepak in Gaining Ratio:-

Shivam’s Contribution = Rs. 70,000 × 3/5 = Rs. 42,000

Deepak’s Contribution = Rs. 70,000 × 2/5 = Rs. 28,000

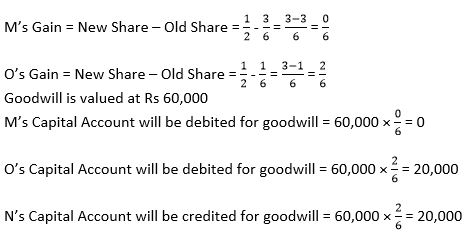

Question 19: M, N and O are partners in a firm sharing profits in the ratio of 3 : 2 : 1 . Goodwill has been valued at Rs 60,000. On N's retirement, M and O agree to share profits equally. Pass the necessary journal entry for treatment of N's share of goodwill.

Answer 19:

Old Ratio of M : N : O = 3:2:1

New Ratio of M:O = 1:1

Gaining Ratio = New Ratio – Old Ratio

About Solution:-

In case of death of the partner, partnership will come to an end immediately. In such a case remaining partners may continue the business. All amounts due to the deceased partner will be paid to his legal representative/Executor.Executor is the person named in a Will or appointed by a court to wind up the deceased partner's financial affairs after death. He is entitled to all the amounts due to the deceased partner.

Things to Remember:

On the Basis of Time: When share of profit is calculated on the basis of time, it may be on the basis of previous years' profit or average profit of the last year.Profit from the date of last balance sheet to the date of death = (Number of days or month from the date of last balance sheet to the date of death/ 365 or 12) x Previous years' profit or Average profits of given number of past years.

Important Notes:

When goodwill is not given (in adjustment), in such a case following steps to be used to calculate the Hidden Goodwill.

Step 1.Calculation of actual amount due to the retiring partner.

Step 2.Calculation of total amount to be paid to retiring partner.

Step 3. Hidden Goodwill = Step 2 — Step 1

Question 20: A, B, C and D are partners in a firm sharing profits in the ratio of 2:1:2:1. On the retirement of C, Goodwill was valued Rs 1,80,000. A, B and D decide to share future profits equally. Pass the necessary Journal entry for the treatment of goodwill.

Answer 20:

Old Ratio of A:B:C:D = 2:1:2:1

New Ratio of A:B:D = 1:1:1

Gaining Ratio = New Ratio – Old Ratio

About Solution:-

If goodwill already appears in the old balance sheet of the firm (if mentioned in the question), then first of all, this goodwill should be written off and should be distributed among all the partners of the firm including the retiring or the deceased partner in their old profit sharing ratio. The following Journal entry is passed to write off the old/existing

Things to Remember:

After writing off the old goodwill, the goodwill need to be adjusted through the partner's capital account with the share of the goodwill of the retiring or the deceased partner. The following Journal entry is passed.

Remaining Partner's Capital A/c Dr.

To Retiring/Deceased Partner's Capital A/c

(Gaining Partner's Capital A/c is debited in their

gaining share and retiring/deceased partner's capital

account in credited for their share of goodwill)

Important Notes:

At the time of retirement or at the event of death of a partner, the goodwill is adjusted among the partners in gaining ratio with the share of goodwill of the retiring or the deceased partner. As per Para 16 of Accounting Standard 10, it is mandatory to record goodwill in the books only when consideration in money or money's worth has been paid for it.

In case of retirement and death of a partner, goodwill account cannot be raised. There are namely two probable situations on which the treatment of goodwill rests.

1. If goodwill already appears in the books of the firm.

2. If no goodwill appears in the books of the firm.

Question 21: A, B and C were partners in a firm sharing profits in the ratio of 6:5:4. Their capitals were A—Rs. 1,00,000; B—Rs. 80,000 and C—Rs. 60,000 respectively. On 1st April, 2009, A retired from the firm and the new profit sharing ratio between B and C was decided as 1 : 4 . On A's retirement, the goodwill of the firm was valued at Rs 1,80,000. Showing your calculations clearly, pass the necessary journal entry for the treatment of goodwill on A's retirement.

Answer 21:

Old Ratio of A:B:C = 6:5:4

New Ratio of B:C = 1:4

Gaining Ratio = New Ratio – Old Ratio

Things to Remember:

Accounting treatment/ Adjustments to be made at the time of Retirement of a partner:

1. Calculation of New Profit-Sharing Ratio and Gaining Ratio.

2. Treatment of Goodwill.

3. Treatment of Accumulated Profit/ Losses and Reserves.

4. Revaluation of Assets and Reassessment of Liabilities.

5. Preparation of Balance Sheet.

Important Notes:

Calculation of New Profit Sharing Ratio:

The ratio of remaining partners is known as New Profit Sharing Ratio, in which they will share the future profits. When a partner retires from the firm, the remaining partners acquired share of retiring partner either in their old ratio or in specified ratio.

New Profit Sharing Ratio = Old Ratio + Gaining Ratio

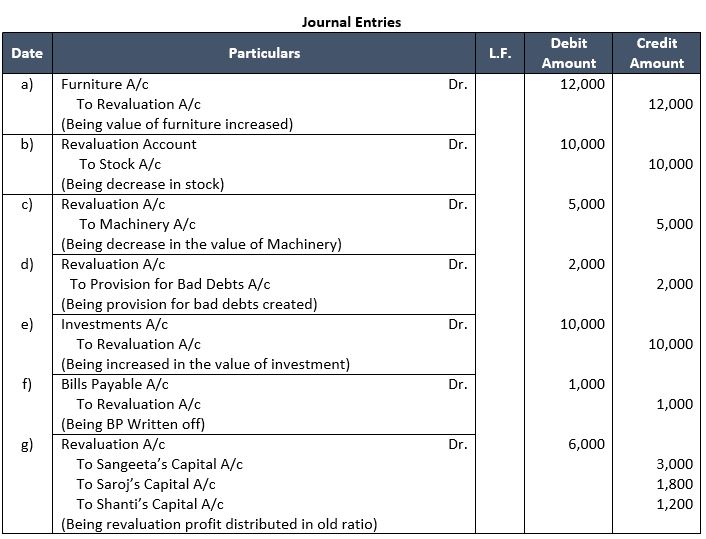

Q22: Sangeeta, Saroj and Shanti are partners sharing profits and losses in the ratio of 5:3:2. Shanit retired and on the date of her retirement, following adjustments was agreed:

a) The value of furniture is to be increased by ₹ 12,000

b) The value of stock to be decreased by ₹ 10,000.

c) Machinery of the books value of ₹ 50,000 is to be reduced by 10%.

d) @ 5% is to be created on debtors of book value of ₹ 40,000.

e) Unrecorded investment worth ₹ 10,000.

f) A creditor of ₹ 1,000 is not likely to be claimed, hence, is to be written back.

Pass necessary Journal entries.

Answer 22:

Question 23: A, B and C were partners, sharing profits and losses in the ratio of 2:2:1. B retire on 31st March, 2024. On the date of his retirement , some of the assets and liabilities appeared in the books as follows: Creditors Rs. 70,000; Building Rs. 1,00,000; Plant and Machinery Rs. 40,000; Stock of Raw Material’s Rs. 20,000; Stock of Finished Goods Rs. 30,000 and Debtors Rs. 20,000.

The following was agreed among the partners on B's retirement:

(a) Building to be appreciated by 20%.

(b) Plant and Machinery to be depreciated by 10%.

(c) A Provision of 5% on Debtors to be created for Doubtful Debts.

(d) Stock of Raw Materials to be valued at Rs. 18,000 and Finished Goods at Rs. 35,000.

(e) An Old Computer previously written off was sold for Rs. 2,000 as scrap.

(f) Firm had to pay Rs 5,000 to an injured employee.

Pass necessary journal entries to record the above adjustments and prepare the Revaluation Account

Answer 23:

About Solution:-

Treatment of Accumulated Profits/Losses and Reserves:

At the time of retirement of a partner, all the accumulated profits/Losses and Reserves are to be distributed to the old partners in their old profit-sharing Ratio.

Things to Remember:

All free reserves and profits given in the liabilities side should be credited to Partner's Capital Accounts or Current Account (If Capitals are fixed) and all fictitious assets/ accumulated losses should be debited to the Partner's Capital Account or Current Account (If Capitals are fixed) in their old ratios.

Important Notes:

Amount Payable to Retiring Partner:Amount to be credited to the Retiring Partner's Capital Account/Amount to be paid

1. Balance of his/her capital account

2. Balance of his/her current account

3. Share of goodwill

4. Share in Revaluation profits

5. Share in Accumulated profits and Reserves

6. Interest on Capital

7. Salary/Commission etc.

8. Share in the profit of current year.

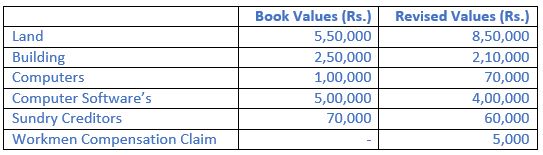

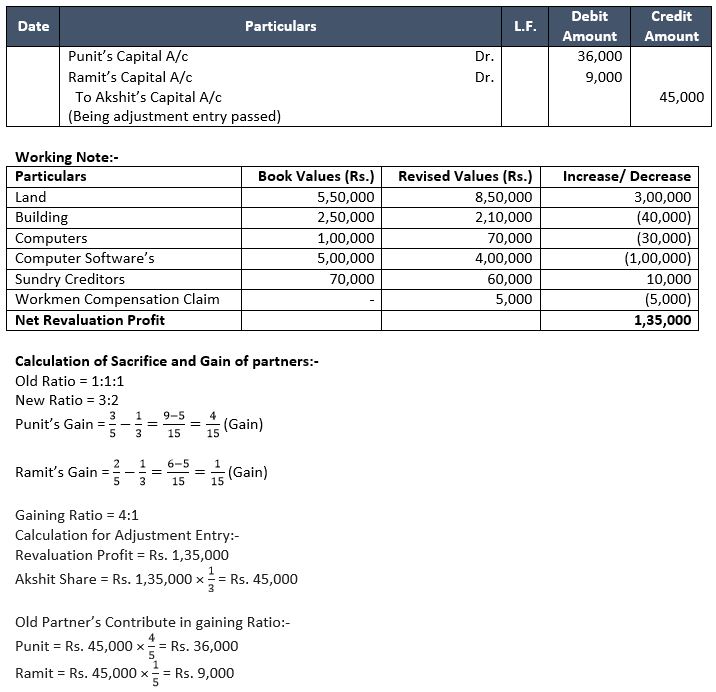

Question 24: Punit, Ramit and Akshit were partners sharing profits equally. Akshit retired on 1st April, 2023. Punit and Ramit decided to continue the business and share profits in the ratio of 3 : 2. They also decided to give effect to the change in values of assets and liabilities without changing their book values.

The book values and their revised values were as follows:

Pass an adjustment entry.

Answer 24:

Question 25: X, Y and Z are partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1 . Z retires from the firm on 31st March, 2018. On the date of Z's retirement, the following balances appeared in the books of the firm:

General Reserve Rs 1,80,000

Profit and Loss Account (Dr.) Rs 30,000

Workmen Compensation Reserve Rs 24,000 which was no more required

Employees' Provident Fund Rs 20,000.

Pass necessary journal entries for the adjustment of these items on Z's retirement.

Answer 25:

About Solution:-

In case of death of the partner, partnership will come to an end immediately. In such a case remaining partners may continue the business. All amounts due to the deceased partner will be paid to his legal representative/Executor.

Things to Remember:

Executor is the person named in a Will or appointed by a court to wind up the deceased partner's financial affairs after death. He is entitled to all the amounts due to the deceased partner.

Important Notes:

Amount to be debited to the Retiring Partner's Capital Account/Amount to be recovered

1. Drawings

2. Interest on drawings Empowering Educators

3. Share in Revaluation Loss

4. Written off portion of goodwill appearing in the books

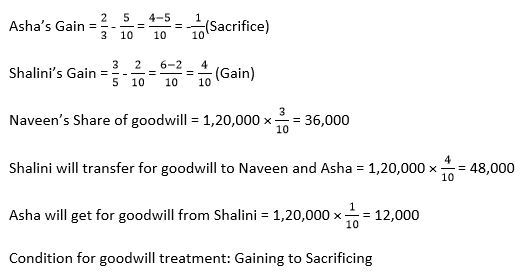

Question 26: Asha, Naveen and Shalini were partners in a firm sharing profits in the ratio of 5:3:2. Goodwill appeared in their books at a value of Rs. 80,000 and General Reserve at Rs. 40,000. Naveen decided to retire from the firm. On the date of his retirement, goodwill of the firm was valued at Rs. 1,20,000. The new profit ratio decided among Asha and Shalini is 2:3.

Record necessary journal entries on Naveen's retirement

Answer 26:

Points of Knowledge:

Old Ratio of Asha : Naveen : Shalini = 5 : 3 : 2

New Ratio of Asha :Shalini = 2 : 3

Gaining Ratio = New Ratio – Old Ratio

About Solution:-

On the Basis of Time: When share of profit is calculated on the basis of time, it may be on the basis of previous years' profit or average profit of the last year.

Profit from the date of last balance sheet to the date of death = (Number of days or month from the date of last balance sheet to the date of death/365 or 12) x Previous years' profit or Average profits of given number of past years.

Important Notes:

In case of profit,

Profit and Loss Suspense Account Dr

To Deceased Partner's / Current A/c

In case of Loss,

Deceased Partner's / Current Account Dr

To Profit and Loss Suspense A/c

Question 27: X, Y and Z were equal partners in a firm. On 31st March, 2023, their Balances Sheet was as follows:

On the above date, Z retires from the firm and X and Y decided to share future profits in the ratio of 3:2. Partners decide to show accumulated profits, losses and reserves in the Balance Sheet of the reconstituted firm at their original values.

Pass an ‘Adjustment Entry’ for the treatment of accumulated profits, losses and reserves.

Answer 27:

Question 28: Partnership Deed of C and D, who are equal partners, has a clause that any partner may retire from the firm on the following terms by giving a six-month notice in writing:

The retiring partner shall be paid—

(a) The amount standing to the credit of his Capital Account and Current Account.

(b) His share of profits to the date of retirement, calculated on the basis of the average profit of the three preceding completed years.

(c) Half the amount of the goodwill of the firm calculated at 1 1/2 times the average profit of the three preceding completed years.

C gave a notice on 31st March, 2023 to retire on 30th September, 2023, when the balance of his Capital Account was Rs. 6,000 and his Current Account (DR.) Rs 500. The profits for the three preceding completed years were; year ended 31st March, 2021 Rs 2,800; year ended 31st March, 2022 Rs 2,200 and year ended 31st March, 2023 Rs 1,600.

Determine the amount due to C as per the partnership agreement.

Answer 28:

About Solution:-

1. When old good will appears in the books then first of all this is writer in the old ratio. Remember Old Good will old Ratio

All Partner’s capital a/c Dr.

To Goodwill A/c

Things to Remember:

After written off of goodwill adjustment of retiring partner’s share goodwill will be made through the following journal entry.

Remaining Partner’s Capital, a/c Dr.

To Retiring/Deceased Partner’s Capital A/c

Important Notes:

According to accounting standards -10, Good will account can’t be raised as only purchased goodwill is recorded in books. Therefore only adjustment entry is done for goodwill.

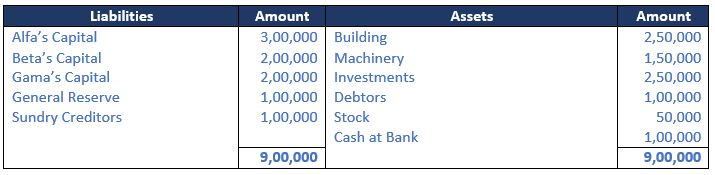

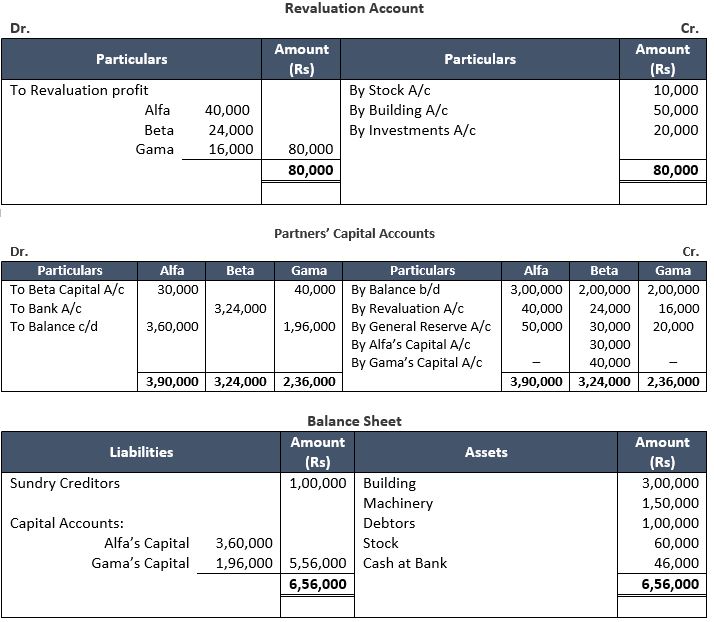

Question 29: Alfa, Beta and Gama are in partnership sharing profits in the ratio of 5:3:2. Their Balance Sheet on 1st April, 2022, the day Beta decided to retire from firm, was as follows:

(i) Beta takes goodwill from Alfa for ₹ 30,000 and from Gama for ₹ 40,000 for foregoing his share of profits.

(ii) Stock to be appreciated by 20% and building by ₹ 50,000.

(iii) Investments were sold for ₹ 2,70,000.

(iv) Beta is paid by bank draft.

Prepare Revaluation Account, Partner’s Capital Accounts and Balance Sheet of the new firm.

Answer 29:

Question 30: Kanika, Disha and Kabir were partners sharing profits in the ratio of 2 : 1 : 1 . On 31st March, 2016, their Balance Sheet was as under:

Kanika retired on 1st April, 2016. For this purpose, the following adjustments were agreed upon:

(a) Goodwill of the firm was valued at 2 years' purchase of average profits of three completed years preceding the date of retirement. The profits for the year:

2013-14 were Rs 1,00,000 and for 2014-15 were Rs 1,30,000.

(b) Fixed Assets were to be increased to Rs 3,00,000.

(c) Stock was to be valued at 120%.

(d) The amount payable to Kanika was transferred to her Loan Account .

Prepare Revaluation Account, Capital Accounts of the partners and the Balance Sheet of the reconstituted firm.

Answer 30:

About Solution:-

Disposal of the Amount Due to the Retiring Partner.This outgoing partners A/c is settled as per the terms of partnership deed. Three cases may be there as given below-

When the retiring partner is paid full amount either in cash or by cheque.

Retiring Partner’s Capital A/c Dr.

To Cash Bank A/c

Things to Remember:

When the retiring partner is paid nothing in cash then the whole amount due is transferred to his loan A/c

Retiring Partner’s Capital A/c Dr.

To retiring partner’s Loon A/c

Important Notes:

When Retiring Partner is partly paid in cash and the remaining amount in treated Loan.

Retiring Partner’s Capital A/c Dr. (Total Amount due)

To Cash Bank A/c (Amount Paid)

To Retiring Partner’s Loan A/c (Amount of Loan)

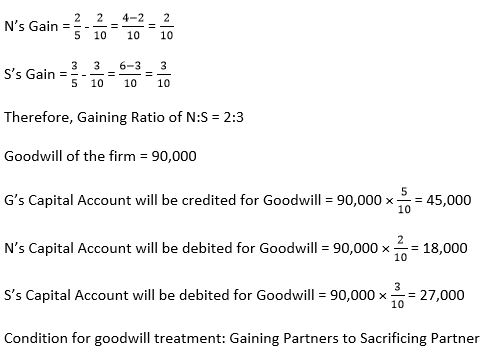

Question 31: N, S and G were partners in a firm sharing profits and losses in the ratio of 2:3:5. On 31st March, 2016 their Balance Sheet was as under:

G retired on the above ate and it was agreed that:

(a) Debtors of Rs 6,000 will be written off as bad debts and a provision of 5% on debtors for bad and doubtful debts will be maintained.

(b) Patents will be completely written off and stock, machinery and building will be depreciated by 5%.

(c) An unrecorded creditor of Rs 30,000 will be taken into account.

(d) N and S will share the future profits in 2:3 ratios.

(e) Goodwill of the firm on G's retirement was valued at Rs 90,000.

Pass necessary journal entries for the above transactions in the books of the firm on G's retirement.

Answer 31:

Old Ratio of N:S:G = 2:3:5

New Ratio of N:S = 2:3

Gaining Ratio = New Ratio – Old Ratio

About Solution:-

Excess of Deficiency of capital in the individual capital A/c is calculated. Such excess or shortage is adjusted by withdrawal or contribution in case or transferring to their current A/cs.

Journal Entries:-

(a) For excess Capital withdrawn by the Partners

Partner’s capital A/c Dr.

To Cash/Bank A/c

(b) For deficiency, cash will be brought in by the partner

Cash/Bank A/c Dr.

To Partner’s capital A/c

Things to Remember:

At the time of retirement/death, the remaining partners may decide to adjust their capitals in their new profit sharing Ratio. Then the sum of their capitals will be treated as the total capital of the new firm which will be divided in their New Profit Sharing Ratio.

Important Notes:

Accounting treatment in the case of death is same as in the case of return except the Following:

1. The deceased partners claim is transferred to his executer’s account.

2. Normally the retirement takes place at the end of the Accounting pried but the death may occur at any time. Hence the claim of deceased part shall also include his share or profit or loss, interest on capital drawings if any from the date of the last balance sheet to the date his death.

3. Calculation of profit/Loss for the intervening Period.

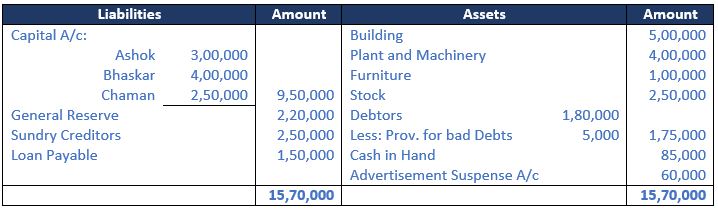

Question 32: Ashok, Bhaskar and Chaman are partners in a firm, sharing profits and losses as Ashok 1/3, Bhaskar 1/2 and Chaman 1/6 respectively. The Balance Sheet of the firm as at 31st March, 2023 was:

Chaman retires on 1st April, 2024 subject to the following adjustments:

(a) Goodwill of the firm be valued at Rs. 2,40,000. Chaman's share of goodwill is adjusted into the account of Ashok and Bhaskar who are going to share in future in the ratio of 3:2.

(b) Plant and Machinery to be depreciated by 10% and Furniture by 5%.

(c) Stock to be appreciated by 15% and Factory Building by 10%.

(d) Provision for Doubtful Debts to be raised to Rs. 20,000.

Prepare Revaluation Account, Capital Account of Chaman and the Balance Sheet of the firm after Chaman's retirement.

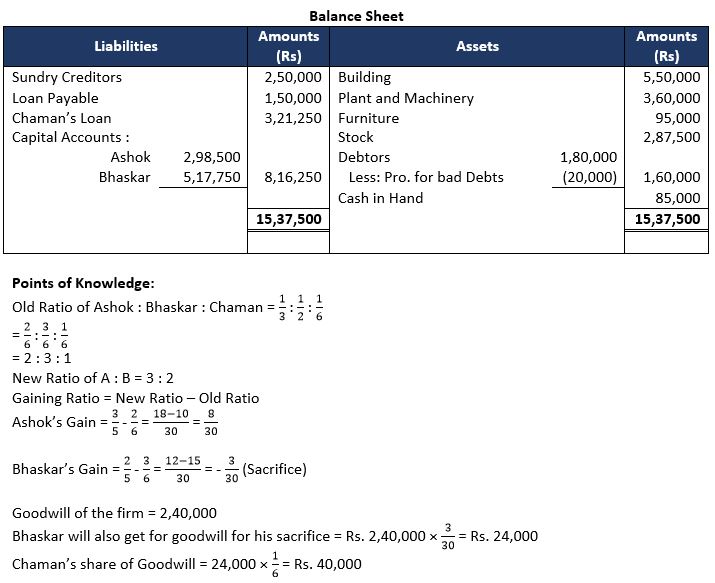

Answer 32:

Ashok will transfer for goodwill to Bhaskar = Rs. 24,000

Ashok will transfer for goodwill to Chaman = Rs. 40,000

Condition for goodwill treatment: Gaining to Sacrificing

About Solution:-

It is calculated by any one of the two methods given below:

a. On Time Basis: In this method proportionally profit for the time period is calculated either on the basis of last year’s profit or on basis of average profits of last few years and then deceased profit share is calculated based on his share of profits.

b. On Turnover or Sales Basis: In this method the profits upto the date of death for the Current year are calculated on the basis of current year’s sales upto the date of death by using the formula.

Things to Remember:

Profits for the current year upto the date of death = Sales of the current year upto the date of death / total sales of last year × Profit for the last year

Important Notes:

New profit Sharing Ratio & Gaining Ratio:-

New profit Sharing Ratio: it is the ratio in which the remaining partners share future profits after retirement/death.

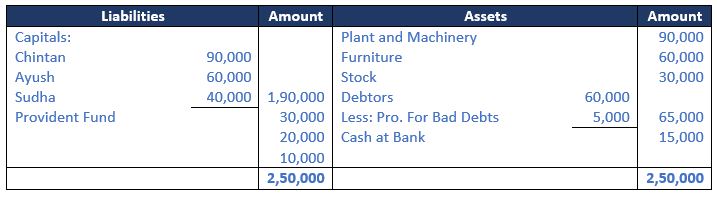

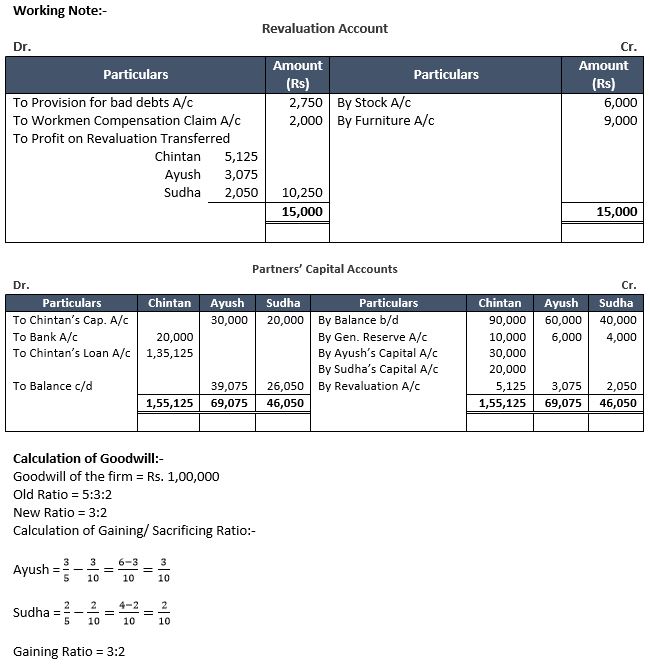

Question 33: Chintan, Ayush and Sudha were partners in a firm sharing profits and losses in the ratio of 5:3:2. On 31st March, 2019 their Balance Sheet was as follows:

Chintan retired on the above date and it was agreed that:

(a) Debtors of Rs. 5,000 were to be written off as bad debts and a provision of 5% on debtors for bad and doubtful debts was to be created.

(b) Goodwill of the firm on Chintan’s retirement was valued at Rs. 1,00,000 and Chintan’s share of the same will be adjusted by debiting the Capital Accounts of Ayush and Sudha.

(c) Stock was revalued at Rs. 36,000.

(d) Furniture was undervalued by Rs. 9,000.

(e) Liability for Workmen’s Compensation of Rs. 2,000 was to be created.

(f) Chintan was to be paid Rs. 20,000 by cheque and the balance was to be transferred to his loan account.

Pass the necessary Journal entries in the books of the firm’s on Chintan’s retirement.

Answer 33:

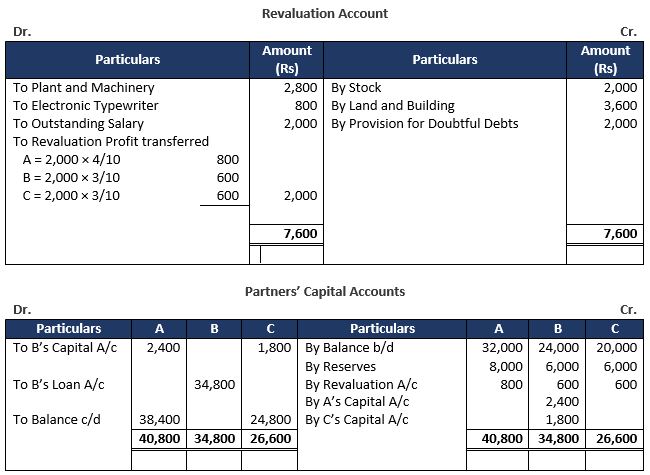

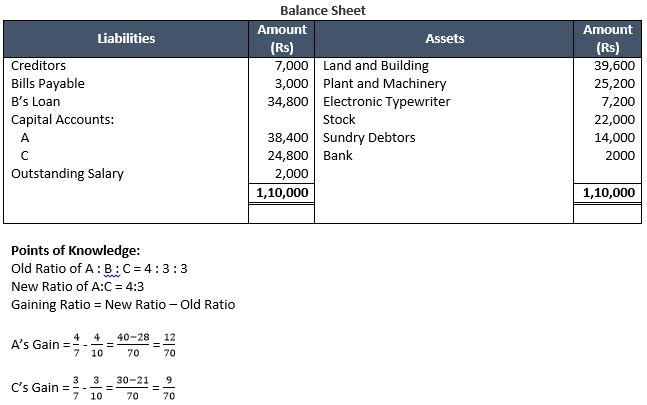

Question 34: A, B and C are partners sharing profits and losses in the ratio of 4:3:3 respectively. Their Balance Sheet as at 31st March, 2024 is:

On 1st April, 2024, B retires from the firm on the following terms:

(a) Goodwill of the firm is to be valued at Rs 14,000.

(b) Stock, Land and Building are to be appreciated by 10%.

(c) Plant and Machinery and Electronic Typewriter are to be depreciated by 10%.

(d) Sundry Debtors are considered to be good.

(e) There is a liability of Rs 2,000 for the payment of outstanding salary to the employee of the firm. This liability has not been shown in the above Balance Sheet but the same is to be recorded now.

(f) Amount payable to B is to be transferred to his Loan Account.

Prepare Revaluation Account, Partners' Capital Accounts and the Balance Sheet of A and C after B's retirement.

Answer 34:

Goodwill of the firm = 14,000

B will be compensated for goodwill = 14,000 × 3/10 = 4,200

A will transfer for goodwill to B = 4,200 × 4/7 = 2,400

C will transfer for goodwill to B = 4,200 × 3/7 = 1,800

Condition for goodwill treatment : Remaining partner to Retiring partner

About Solution:-

Excess of Deficiency of capital in the individual capital A/c is calculated. Such excess or shortage is adjusted by withdrawal or contribution in case or transferring to their current A/cs.

Journal Entries:-

(a) For excess Capital withdrawn by the Partners

Partner’s capital A/c Dr.

To Cash/Bank A/c

(b) For deficiency, cash will be brought in by the partner

Cash/Bank A/c Dr.

To Partner’s capital A/c

Things to Remember:

At the time of retirement/death, the remaining partners may decide to adjust their capitals in their new profit sharing Ratio. Then the sum of their capitals will be treated as the total capital of the new firm which will be divided in their New Profit Sharing Ratio.

Important Notes:

Accounting treatment in the case of death is same as in the case of return except the Following:

1. The deceased partners claim is transferred to his executer’s account.

2. Normally the retirement takes place at the end of the Accounting pried but the death may occur at any time. Hence the claim of deceased part shall also include his share or profit or loss, interest on capital drawings if any from the date of the last balance sheet to the date his death.

3. Calculation of profit/Loss for the intervening Period.

Question 35: X, Y and Z are partners sharing profits and losses in the ratio of 3:2:1. The Balance Sheet of the firm as at 31st March, 2018 stood as follows:

Z retired on the above date on the following terms:

(a) Goodwill of the firm is to be valued at Rs 34,800.

(b) Value of Patents is to be reduced by 20% and that of machinery to 90%.

(c) Provision for Doubtful Debts is to be created @ 6% on debtors.

(d) Z took over the investment at market value.

(e) Liability for Workmen Compensation to the extent of Rs 750 is to be created.

(f) A liability of Rs 4,000 included in creditors is not to be paid.

(g) Amount due to Z to be settled on the following basis:

Rs. 5,067 immediately, 50% of the balance within one year and the balance by a draft for 3 Months.

Give necessary Journal entries for the treatment of goodwill; prepare Revaluation Account, Capital Accounts and the Balance Sheet of the new firm

Answer 35:

Points of Knowledge:

Note 1: Calculation of Sacrificing Ratio

Old Ratio of X : Y : Z = 3 : 2 : 1

New Ratio of X : Y = 3 : 2

Gaining Ratio = New Ratio – Old Ratio

X’s Gain = 3/5 - 3/6 = (18-15)/30 = 3/30

Y’s Gain = 2/5 - 2/6 = (12-10)/30 = 2/30

Therefore Gaining Ratio of X : Y = 3 : 2

Note 2:

Goodwill of the firm = 34,800

Z’s share of goodwill = 34,800 × 1/6 = 5,800

X will transfer for goodwill to Z = 5,800 × 3/5 = 3,480

Y will transfer for goodwill to Z = 5,800 × 2/5 = 2,320

Condition for goodwill treatment: Remaining Partners to Retiring Partner

About Solution:-

Treatment of Accumulated Profits/Losses and Reserves:

At the time of retirement of a partner, all the accumulated profits/Losses and Reserves are to be distributed to the old partners in their old profit-sharing Ratio.

Things to Remember:

All free reserves and profits given in the liabilities side should be credited to Partner's Capital Accounts or Current Account (If Capitals are fixed) and all fictitious assets/ accumulated losses should be debited to the Partner's Capital Account or Current Account (If Capitals are fixed) in their old ratios.

Important Notes:

Amount Payable to Retiring Partner: Amount to be credited to the Retiring Partner's Capital Account/Amount to be paid

1. Balance of his/her capital account

2. Balance of his/her current account

3. Share of goodwill

4. Share in Revaluation profits

5. Share in Accumulated profits and Reserves

6. Interest on Capital

7. Salary/Commission etc.

8. Share in the profit of current year.

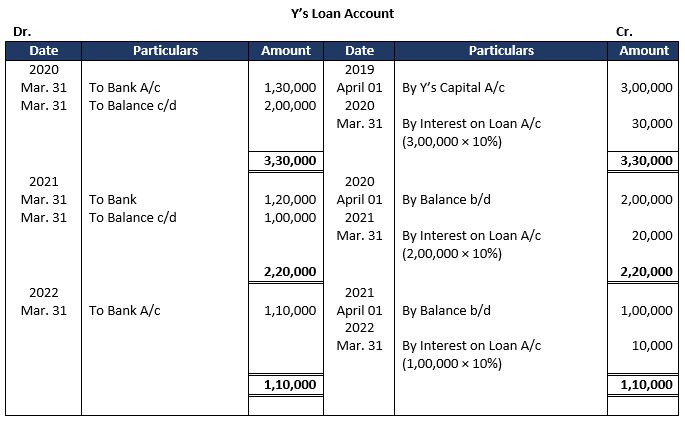

Question 36: Ashok, Bhaskar and Chaman were in partnership sharing profits and losses equally. 'Bhaskar' retires from the firm. After adjustments, his Capital Account shows a credit balance of Rs. 3,00,000 as on 1st April, 2019. Balance due to 'Bhaskar' is to be paid in three equal annual instalments along with interest @ 10% p.a. Prepare Bhaskar's Loan Account until he is paid the amount due to him. The firm closes its books on 31st March every year.

Answer 36:

Point of Knowledge:-

Amount to be paid per Instalment = Rs. 3,00,000 × 1/3

Amount to be paid per Instalment = Rs. 1,00,000

Question 37: Rakesh retired from the firm. The amount due to him was determined at Rs. 90,000. It was decided to pay the due amount as follows:

On the date of retirement – Rs. 30,000

Balance in three yearly instalments − First two instalments being of Rs. 26,000, including interest; and Balance amount as last instalment.

Interest was payable @ 10 p.a. Prepare retiring Partners' Loan Account.

Answer 37:

About Solution:-

The ratio of remaining partners is known as New Profit Sharing Ratio, in which they will share the future profits. When a partner retires from the firm, the remaining partners acquired share of retiring partner either in their old ratio or in specified ratio.

Things to Remember:

All free reserves and profits given in the liabilities side should be credited to Partner's Capital Accounts or Current Account (If Capitals are fixed) and all fictitious assets/ accumulated losses should be debited to the Partner's Capital Account or Current Account (If Capitals are fixed) in their old ratios.

Important Notes:

Treatment of Revaluation of Assets and Re-assessment of liabilities and Preparation of Revaluation Account is same as we have done in case of Admission of a partner. In case of Retirement also we will distribute Revaluation Profits/Losses to all the partners in their old ratios.

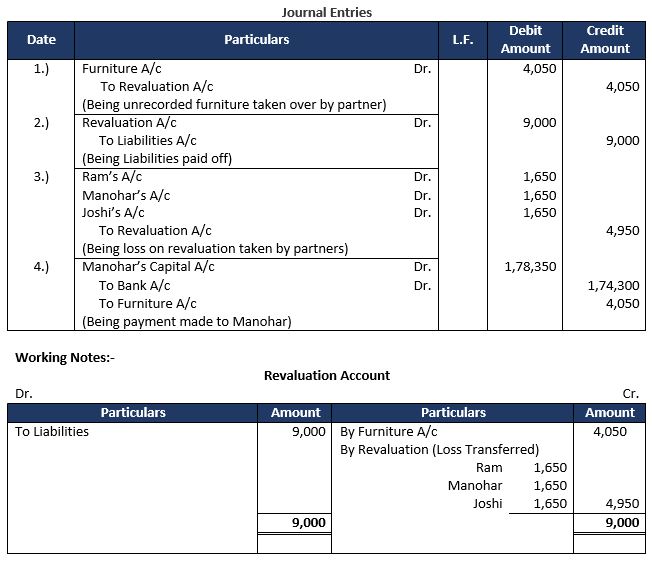

Question 38: Ram, Manohar and Joshi were partners in a firm. Monohar retired and his claim including his capital and share of goodwill was Rs. 1,80,000. There was unrecorded furniture estimated at Rs. 9,000 half of which was given for an unrecorded liability of Rs. 18,000 in settlement of claim of Rs. 9,000 and remaining half was taken by Manohar at a discount of 10% in part satisfaction of his claim. Balance of Monohar’s claim was discharged by bank draft. Pass necessary Journal entries to record the above transactions.

Answer 38:

Question 39: Harish, Paresh and Mahesh were three partners sharing profits and losses in the ratio of 5:4:1. Paresh retired on 31st March, 2022. His capital as on 1st April, 2021, was ₹ 80,000. During the year 2021-22, he withdrew ₹ 5,000. He was to be charged interest of ₹ 100 on drawings.

The Partnership Deed provides that on the retirement of a partner, he will be entitled to:

(i) His share of capital.

(ii) Interest on capital @ 10% per annum.

(iii) His share of profit in the year of retirement.

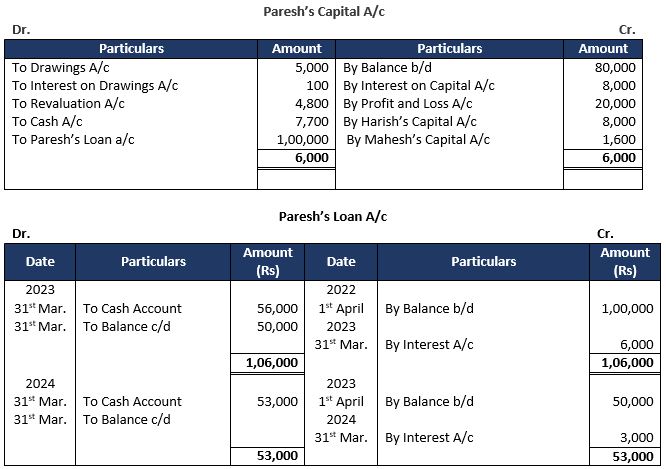

(iv) His share of goodwill of the firm.

(v) His share in the profit/loss on revaluation of assets and liabilities.

Additional Information:

(a) Paresh’s share in the profit of the firm for the year 2021-22 was ₹ 20,000.

(b) Goodwill of the firm was valued at ₹ 24,000.

(c) The firm incurred loss of ₹ 12,000 on the revaluation of assets and liabilities.

(d) Paresh was to be paid ₹ 7,700 in cash and the balance was to be transferred to his loan account bearing interest @ 6% p.a. Loan was to be repaid in two equal annual installments, the first installment to be paid on 31st March 2023.

You are required to prepare:

(i) Paresh’s Capital Account.

(ii) Paresh’s Loan Account till it is finally closed.

Answer 39:

Question 40: X, Y and Z are partners in a firm sharing profits in the ratio of 3 : 2 : 1 . On 1st April, 2009, Y retires from the firm. X and Z agree that the capital of the new firm shall be fixed at Rs 2,10,000 in the profit-sharing ratio. The Capital Accounts of X and Z after all adjustments on the date of retirement showed balance of Rs 1,45,000 and Rs 63,000 respectively. State the amount of actual cash to be brought in or to be paid to the partners.

Answer 40:

About Solution:-

On retirement of a partner, it is required to revalue assets and liabilities just as in the case of admission of a partner. If there is revaluation profit, then such profit should be distributed amongst the existing partners including the retiring partner at the existing profit sharing ratio. On the other hand, if there is loss on revaluation that is also to be distributed to all the partners including the retiring partner at the existing profit sharing ratio. To arrive at, profit or loss on revaluation of assets and liabilities, a Revaluation Account or Profit and Loss Adjustment Account is opened. Revaluation Account or Profit and Loss Adjustment Account is closed automatically by transfer of profit or loss balance to the Partners' Capital Accounts.

Things to Remember:

If it is decided that revalued figures of assets and liabilities will not appear in the balance sheet of the continuing partners, then a journal entry should be passed with the amount payable or chargeable to the retiring partner which the continuing partners will share at the ratio of gain.

Important Notes:

In the first instance, the journal entry for distribution of profit or loss on revaluation which will appear in the balance sheet also is as follows:

Revaluation A/c Dr.

To Partner’s Capital A/c

(for profit on revaluation)

Partner’s Capital A/c

To Revaluation A/c

(Being for loss on revaluation)

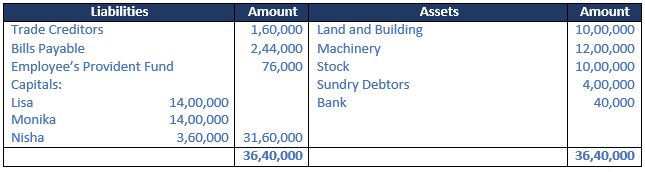

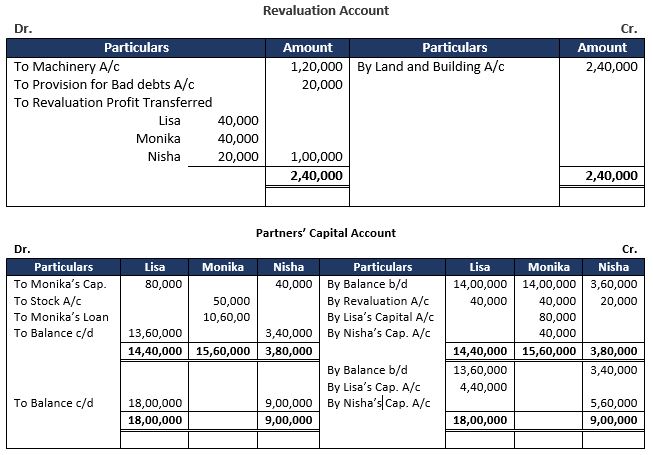

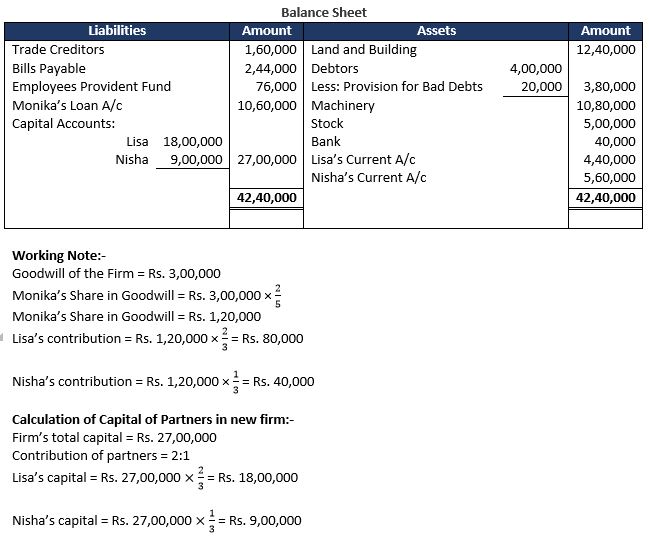

Question 41: Lisa, Monika and Nisha were partners in a firm sharing profits and losses in the ratio of 2:2:1. On 31st March, 2019, their Balance Sheet was as follows:

On 31st March, 2019, Monika retired from the firm and the remaining partners decided to carry o the business. It was agreed that:

(i) Land and Building be appreciated by Rs. 2,40,000 and machinery be depreciated by 10%.

(ii) 50% of the stock was taken over by the retiring partner at book value.

(iii) Provision for Doubtful debts was to be made at 5% on debtors.

(iv) Goodwill of the firm be valued at Rs. 3,00,000 and Monika’s share of goodwill be adjusted in the accounts of Lisa and Nisha.

(v) The total capital of the new firm be fixed at Rs. 27,00,000 which will be in the proportion of the new profit sharing ratio of Lisa and Nisha. For this purpose, Current Account of the partners were to be opened.

Prepare Revaluation Account, Partner’s Capital Account and the Balance Sheet of the reconstituted firm on Monika’s retirement.

Answer 41:

Question 42: On 31st March, 2018 , The Balance Sheet of A , B and C who were sharing profits and losses in proportion to their capitals stood as:

B retires and following readjustments of assets and liabilities have been agreed upon before ascertainment of the amount payable to B :

(a) Out of the amount of insurance premium which was debited to Profit and Loss Account, Rs 1,000 be carried forward for Unexpired insurance.

(b) Freehold Premises be appreciated by 10%.

(c) Provision for Doubtful Debts is brought up to 5% on Debtors.

(d) Machinery be depreciated by 5%.

(e) Liability for Workmen Compensation to the extent of Rs 1,500 would be created.

(f) That the goodwill of the entire firm be fixed at Rs 18,000 and B's share of the same be adjusted into the accounts of A and C who are going to share future profits in the proportion of 3/4th and 1/4th respectively.

(g) Total capital of the firm as newly constituted be fixed at Rs 60,000 between A and C in the proportion of 3/4th and 1/4th after passing entries in their accounts for adjustments , i.e., actual cash to be paid or to be brought in by continuing partners as the case may be .

(h) B be paid Rs 5,000 in cash and the balance be transferred to his Loan Account.

Prepare Capital Accounts of Partners and the Balance Sheet of the firm of A and C .

Answer 42:

Points of Knowledge:

Note 1: Calculation of New and Gaining Ratio

Old Ratio of A : B : C = 45,000 : 30,000 : 15,000: = 3:2:1

New Ratio of A:C = 3 :1

Gaining Ratio = New Ratio – Old Ratio

A’s Gain = 3/4 - 3/6 = (18-12)/24 = 6/24

C’s Gain = 1/4 - 1/6 = (6-4)/24 = 2/24

Therefore, Gaining Ratio of A:C = 6 : 2 = 3 :1

Treatment of goodwill:

Goodwill of the firm = 18,000

B will be compensated for goodwill = 18,000 × 2/6 = 6,000

A will transfer for goodwill to B = 6,000 × ¾ = 4,500

C will transfer for goodwill to B = 6,000 × ¼ = 1,500

Condition for goodwill treatment: Remaining partner to Retiring partner

Note 2:

Capital Adjustment:

A’s Capital = 60,000 × ¾ = 45,000

C’s Capital = 60,000 × ¼ = 15,000

Note 3:

Closing Bank Balance = 13,000 – 5,000 + 3,000 + 1,000 = 12,000

About Solution:-

The following adjustments are necessary in the capital A/c

(i) Transfer of reserve,

(ii) Transfer of goodwill,

(iii) Transfer of profit/loss on revaluation

Things to Remember:

The continuing partners may discharge the whole claim at the time of retirement. Then the journal entry will appear as follows:

Retiring partner’s capital A/c

To Bank A/c

Important Notes:

Sometimes the retiring partner agrees to retain some portion of his claim in the partnership as loan. The journal entry will be follows:

Retiring Partner’s Capital A/c

To Retiring Partner’s loan A/c

To Bank A/c

Question 43: X, Y and Z were in partnership sharing profits in proportion to their capitals. Their Balance Sheet as on 31st March, 2018 was as follows:

On the above date Y, retired owing to ill health. The following adjustments were agreed upon for calculation of amount due to Y:

(a) Provision for Doubtful Debts to be increased to 10% of Debtors.

(b) Goodwill of the firm be valued at Rs. 36,000 and be adjusted into the Capital Account of X and Z, who will share profits in future in the ratio of 3:1.

(c) Included in the value of Sundry Creditors was Rs. 2,500 for an outstanding legal claim, which will not arise.

(d) X and Z also decided that the total capital of the new firm will be Rs. 1,20,000 in their profit-sharing ratio. Actual cash to be brought in or to be paid off as the case may be.

(e) Y to be paid Rs. 9,000 immediately and balance to be transferred to his Loan Account.

Prepare Revaluation Account, Partners’ Capital Accounts and Balance Sheet of the new firm after Y’s retirement.

Answer 43:

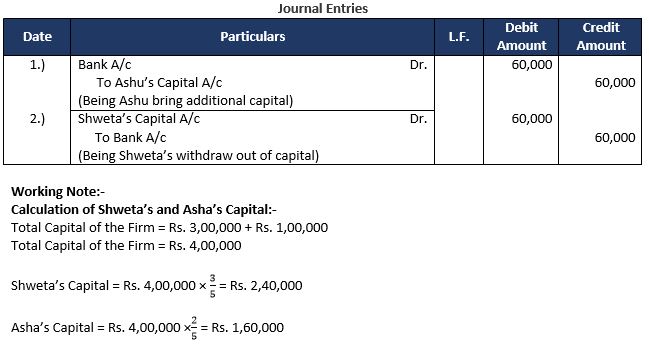

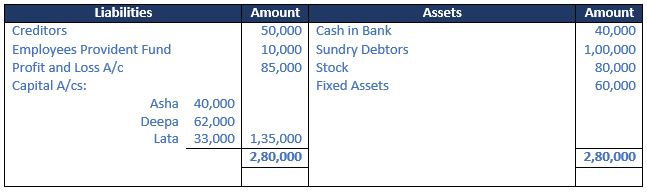

Question 44: Shweta, Meenu and Asha were partners in a firm sharing profits and losses in the ratio of 3:5:2. Meenu retired on 1st April, 2022. After making all adjustments relating to revaluation, goodwill and accumulated profits, etc., Capital Accounts of Shweta and Asha showed credit balance of ₹ 3,00,000 and ₹ 1,00,000 respectively. It was decided to adjust the capitals of Shweta and Asha in their new profit sharing ratio.

Pass necessary Journal entries for bringing in or withdrawal of the necessary amounts involved. Show your working clearly.

Answer 44:

Question 45: Amit, Balan and Chander were partners in a firm sharing profits in the proportion of 1/2, 1/3 and 1/6 respectively. Chander retired on 1st April, 2014. The Balance Sheet of the firm on the date of Chander's retirement was as follows:

(i) Goodwill be valued at Rs. 27,000.

(ii) Depreciation of 10% was to be provided on Machinery.

(iii) Patents were to be reduced by 20%.

(iv) Liability on account of Provident Fund was estimated at Rs. 2,400.

(v) Chander took over Investments for Rs. 15,800.

(vi) Amit and Balan decided to adjust their capitals in proportion of their profit-sharing ratio by opening Current Accounts.

Prepare Revaluation Account and Partners' Capital Accounts on Chander's retirement.

About Solution:-

Loan of the retiring partner is disposed off accordingly of the pre decided term and conditions among the partners. Normally the Principal amount is paid in few equal installments. In such cases interest is credited to the Loan A/c on the basic of the amount outstanding at the beginning of each year and the amount paid it debited to loan A/c. The following Journal entries are done:-

(1) For interest on Loan:-

Interest A/c Dr.

To Retiring partner’s Loan A/c

Things to Remember:

For the payment of instalment

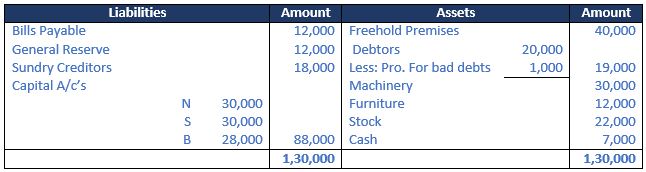

Retiring Partner’s Loan A/c Dr.

To Cash/Bank A/c (including interest)

Important Notes:

At the time of retirement/death, the remaining partners may decide to adjust their capitals in their new profit sharing Ratio. Then the sum of their capitals will be treated as the total capital of the new firm which will be divided in their New Profit Sharing Ratio.

Question 46: N, S and B were partners in a firm sharing profits and losses in proportion of 1/2, 1/6 and 1/3 respectively. The Balance Sheet of the firm as at 31st March, 2017 was as follows:

B retired from the business on the above date and the partners agreed to the following:

(i) Freehold premises and stock were to be appreciated by 20% and 15% respectively.

(ii) Machinery and furniture were to be depreciated by 10% and 7% respectively.

(iii) Provision for bad debts was to be increased by Rs. 1,500.

(iv) On B’s retirement goodwill of the firm was valued at Rs. 21,000.

(v) The continuing partners decided to adjust their capital in their new profit-sharing ratio after retirement of B. Surplus/deficit, if any, in their Capital Accounts was to be adjusted through their Current Accounts.

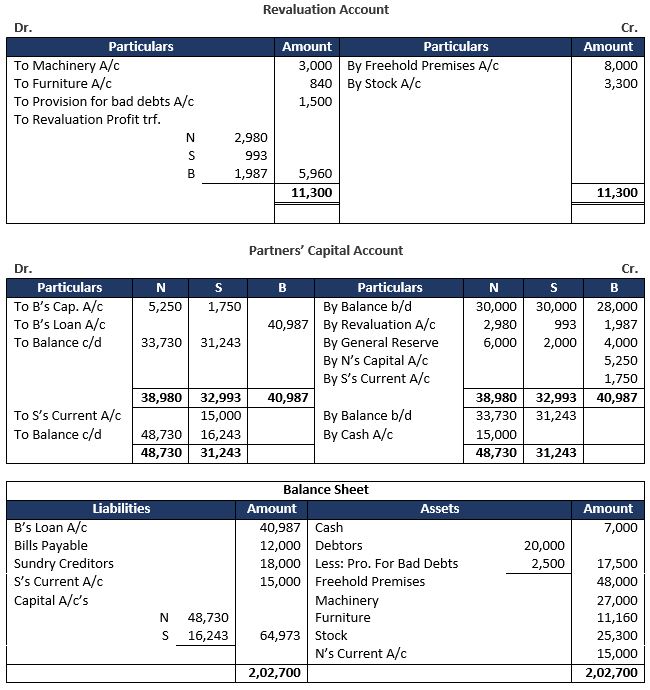

Prepare Revaluation Account, Partner’s Capital Accounts and the Balance Sheet of the reconstituted firm.

Answer 46:

Working Note:-

Total Capital = Rs. 33,730 + Rs. 31,243

Total Capital = Rs. 64,973

N’s Capital = Rs. 64,973 × 3/4 = Rs. 48,730

S’s Capital = Rs. 64,973 × 1/4 = Rs. 16,243

Calculation of Partners share in Goodwill:-

Goodwill = Rs. 21,000

B’s Share in Goodwill = Rs. 21,000 × 2/6 = Rs. 7,000

N and S contribute B’s Share in gaining Ratio 3:1.

N’s Contribution = Rs. 7,000 × 3/4 = Rs. 5,250

S’s Contribution = Rs. 7,000 × 1/4 = Rs. 1,750

(a) Land and Building be appreciated by 30%.

(b) Machinery be depreciated by 30%.

(c) There were Bad Debts of Rs 35,000.

(d) The claim against Workmen Compensation Reserve was estimated at Rs 15,000.

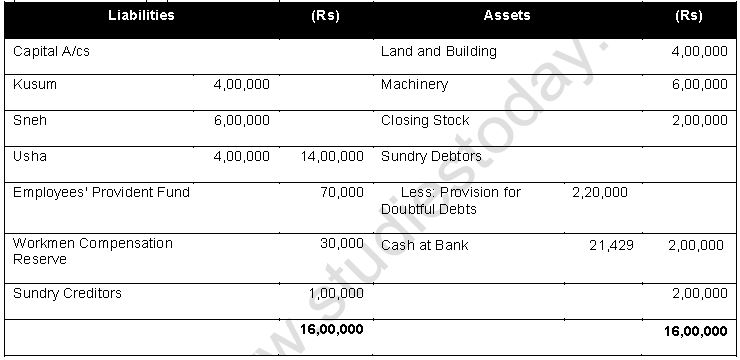

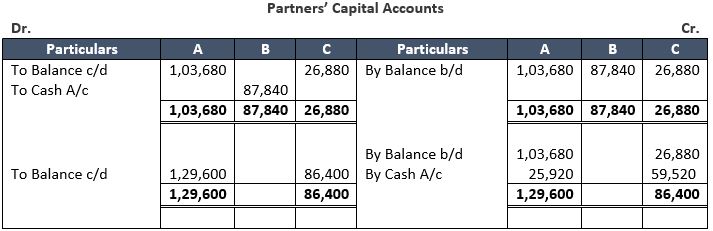

(e) Goodwill of the firm was valued at Rs. 2,80,000 and Kusum's share of goodwill was adjusted against the Capital Accounts of the continuing partners Sneh and Usha who have decided to share future profits in the ratio of 3 : 4 respectively.

(f) Capital of the new firm in total will be the same as before the retirement of Kusum and will be in the new profit-sharing ratio of the continuing partners.

(g) Amount due to Kusum be settled by paying Rs. 1,00,000 in cash and balance by transferring to her Loan Account which will be paid later on.

Prepare Revaluation Account, Capital Accounts of Partners and Balance Sheet of the new firm after Kusum's retirement.

Answer 47:

Therefore Gaining Ratio of Sneh : Usha = 0 : 2

Note 2: Treatment of goodwill:

Goodwill of the firm = 2,80,000

Kusum will be compensated for goodwill = 2,80,000 × 2/7 = 80,000 by usha only.

Condition for goodwill treatment: Gaining partner to Retiring partner.

Note 3: Capital Adjustment:

Total Capital of the new firm = 14,00,000

Sneh’s Capital = 14,00,000 × 3/7 = 6,00,000

Usha’s Capital = 14,00,000 × 4/7 = 8,00,000

Note 4 : Closing Bank Balance = 2,00,000 + 25,714 – 4,97,143 – 1,00,000 = 6,22,857

About Solution:-

Calculation of Gaining Ratio: It is the ratio in which retiring partner's share is acquired by the remaining partner.

Gaining Ratio = New Ratio — Old Ratio

Things to Remember:

Treatment of Goodwill:

1. At the time of retirement of a partner, he/she will get his/her capital, profit, reserves etc. and also goodwill.

2. The goodwill of retiring partner will be calculated and will be adjusted among remaining partners in gaining ratio.

3. Retiring Partner's share of goodwill = Total Goodwill of the firm x Retiring Partner's share.

Important Notes:

Journal Entries for Goodwill:

Gaining Partner's Capital A/c Dr.

To Retiring Partner's Capital A/c or Sacrificing Partner's Capital A/c

(Being retiring partners share of goodwill

is adjusted in the gaining ratio through the

Capital accounts of the partners)

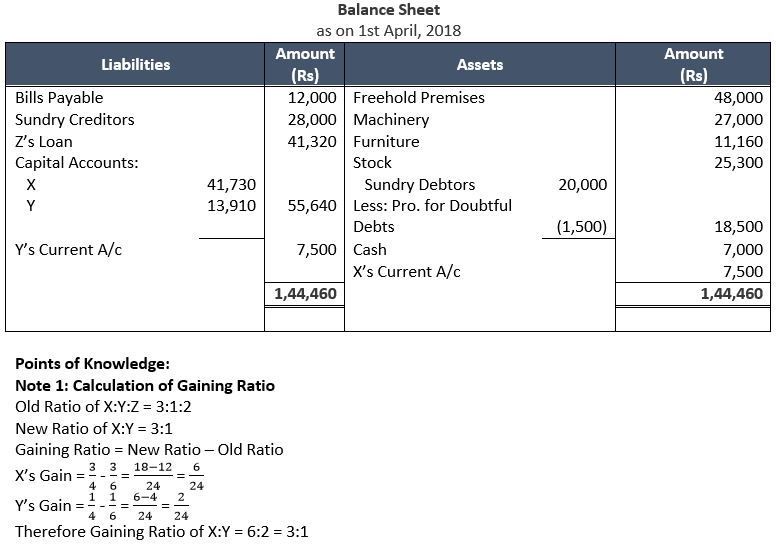

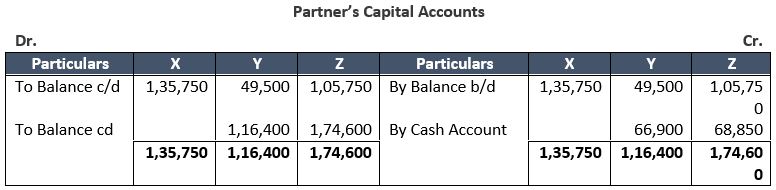

Question 48: Lal, Bal and Pal are partners sharing profits in the ratio of 5:3:7. Lal retired from the firm. Bal and Pal decided to share future profits in the ratio of 2:3. The adjusted Capital Accounts of Bal and Pal showed balances of ₹ 49,500 and ₹ 1,05,750 respectively. The total amount to be paid to Lal is ₹ 1,35,750. This amount is to be paid by Bal and Pal in a manner that their capitals become proportionate to their new profit-sharing ratio.

Calculate the amount to be brought or to be paid to partners.

Answer 48:

Total Capital of the firm = Rs. 49,500 + Rs. 1,05,750 + Rs. 1,35,750

Total Capital of the firm = Rs. 2,91,000

Bal’s Capital = Rs. 2,91,000 × 2/5 = Rs. 1,16,400

Pal’s Capital = Rs. 2,91,000 × 3/5 = Rs. 1,74,600

Bal’s Capital = Capital in firm - Adjusted Capital

Bal’s Capital = Rs. 1,16,400 - Rs. 49,500

Bal’s Capital = Rs. 66,900

Pal’s Capital = Capital in firm - Adjusted Capital

Pal’s Capital = Rs. 1,74,600 - Rs. 1,05,750

Pal’s Capital = Rs. 68,850

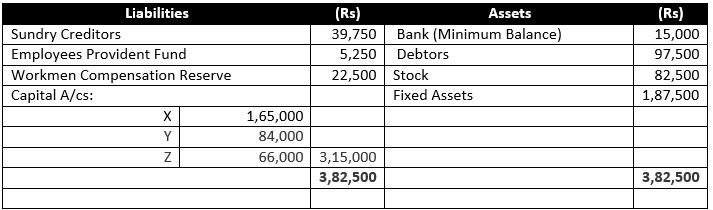

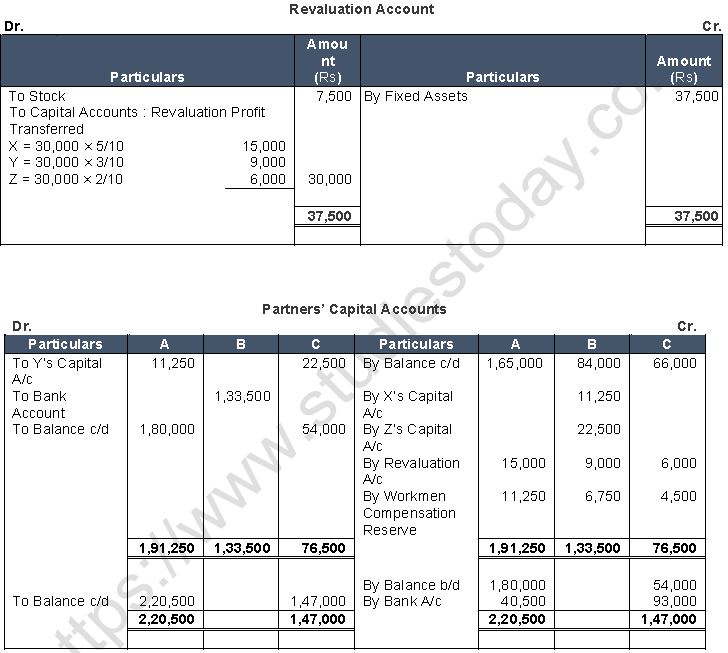

Question 49: The Balance Sheet of X, Y and Z who were sharing profits in the ratio of 5:3:2 as at 31st March, 2024 is as follows:

The other terms on retirement were:

(a) Goodwill of the firm is to be valued at Rs 80,000.

(b) Fixed Assets are to be depreciated to Rs 57,500.

(c) Make a Provision for Doubtful Debts at 5% on Debtors.

(d) A liability for claim, included in Creditors for Rs 10,000 is settled at Rs 8,000.

The amount to be paid to X by Y and Z in such a way that their Capitals are proportionate to their profit-sharing ratio and leave a balance of Rs 15,000 in the Bank Account. Prepare Profit and Loss Adjustment Account and Partners' Capital Accounts.

Answer 49:

Goodwill of the firm = 80,000

X will be compensated for goodwill = 80,000 × 5/10 = 40,000

Y will transfer for goodwill to X = 40,000 × 3/5 = 24,000

Z will transfer for goodwill to X = 40,000 × 2/5 = 16,000

Condition for goodwill treatment: Remaining partner to Retiring partner

Note 3: Capital Adjustment:

Total Capital of the new firm = 1,19,750 + 61,850 + 32,900 + (40,000-15,000) + 8000 = 1,97,500

Y’s Capital = 1,97,500 × 3/5 = 1,18,500

Z’s Capital = 1,97,500 × 2/5 = 79,000

About Solution:-

Loan of the retiring partner is disposed off accordingly of the pre decided term and conditions among the partners. Normally the Principal amount is paid in few equal installments. In such cases interest is credited to the Loan A/c on the basic of the amount outstanding at the beginning of each year and the amount paid it debited to loan A/c. The following Journal entries are done:-

(1) For interest on Loan:-

Interest A/c Dr.

To Retiring partner’s Loan A/c

Things to Remember:

For the payment of instalment

Retiring Partner’s Loan A/c Dr.

To Cash/Bank A/c (including interest)

Important Notes:

At the time of retirement/death, the remaining partners may decide to adjust their capitals in their new profit sharing Ratio. Then the sum of their capitals will be treated as the total capital of the new firm which will be divided in their New Profit Sharing Ratio.

Answer 50:

This outgoing partners A/c is settled as per the terms of partnership deed. Three cases may be there as given below-

When the retiring partner is paid full amount either in cash or by cheque:-

Retiring Partner’s Capital A/c Dr.

To Cash Bank A/c

Things to Remember:

When the retiring partner is paid nothing in cash then the whole amount due is transferred to his loan A/c.

Retiring Partner’s Capital A/c Dr.

To retiring partner’s Loan A/c

Important Notes:

When Retiring Partner is partly paid in cash and the remaining amount in treated Loan.

Retiring Partner’s Capital A/c Dr. (Total Amount due)

To Cash Bank A/c (Amount Paid

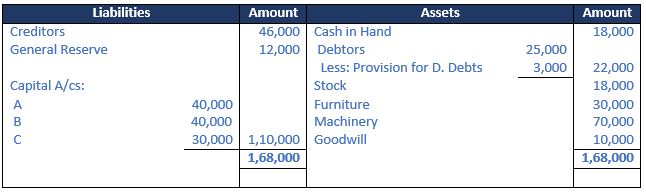

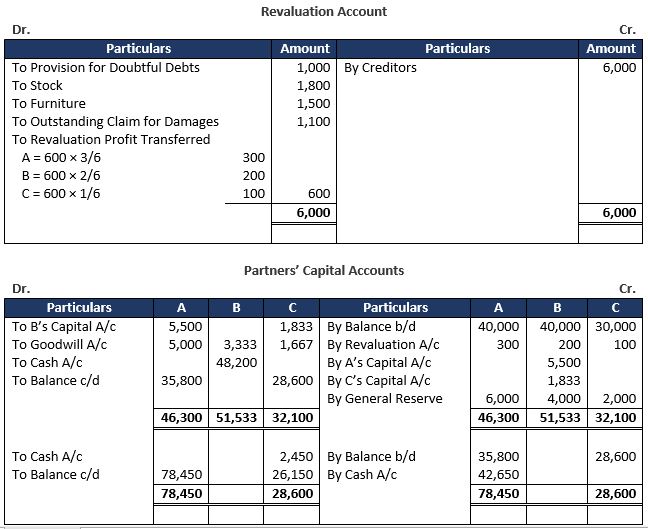

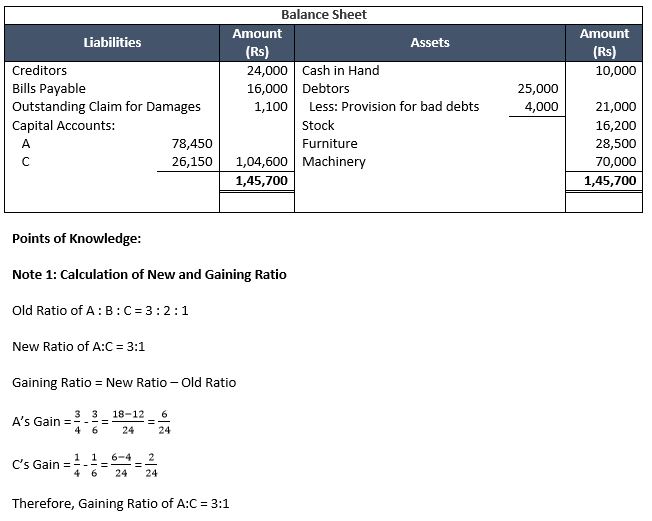

Question 51: Suraj, Pawan and Kamal are partners in a firm sharing profits and losses in the ratio of 3:2:1. Their Balance Sheet as at 31st March, 2024 is:

B retires on 1st April, 2024 on the following terms:

(a) Provision for Doubtful Debts be raised by Rs 1,000.

(b) Stock to be depreciated by 10% and Furniture by 5%.

(c) There is an outstanding claim of damages of Rs 1,100 and it is to be provided for.

(d) Creditors will be written back by Rs. 6,000.

(e) Goodwill of the firm is valued at Rs. 22,000.

(f) Bill paid in full with the cash brought in by A and C in such a manner that their capitals are in proportion to their profit-sharing ratio and Cash in Hand remains at Rs. 10,000.

Prepare Revaluation Account, Partners' Capital Accounts and the Balance Sheet of A and C.

Answer 51:

Note 2: Treatment of goodwill:

Goodwill of the firm = 22,000

B will be compensated for goodwill = 22,000 × 2/6 = 7,333

A will transfer for goodwill to B = 7,333 × ¾ = 5,500

C will transfer for goodwill to B = 7,333 × ¼ = 1,833

Condition for goodwill treatment: Remaining partner to Retiring partner