Access free DK Goel Solutions Class 12 Accountancy Chapter 7 Company Accounts Issue of Share 2026 below. Students can now access free DK Goel Solutions for Class 12 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 12 Math Chapter 7 Company Accounts Issue of Share DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 7 Company Accounts Issue of Share Class 12 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 7 Company Accounts Issue of Share DK Goel Class 12 Solved Exercises

Short Answer Questions

Question 1.

Solution 1

Question 2.

Solution 2 At least 5% of share application money of the nominal value of shares. The Application money must be deposited by the Company in a ‘Scheduled Bank’. Application money is a part of the share capital of the company, and as such, when the directors allot the shares the application money is transferred to share capital account. Application money received by the company when it shares are issues to the public.

Question 3.

Solution 3 In the absence of the Articles of Association, the provisions of Table ‘F’ of Schedule I of the companies Act, 2013 shall apply. The amount to be called up either on application, or on allotment, or on any one call shall not exceed 25% of the total quantum of the issue.

Question 4.

Solution 4 In the absence of the Articles of Association, the provisions of Table ‘F’ of Schedule I of the companies Act, 2013 shall apply. There must be an interval of at least one month between the makings of two calls.

Question 5.

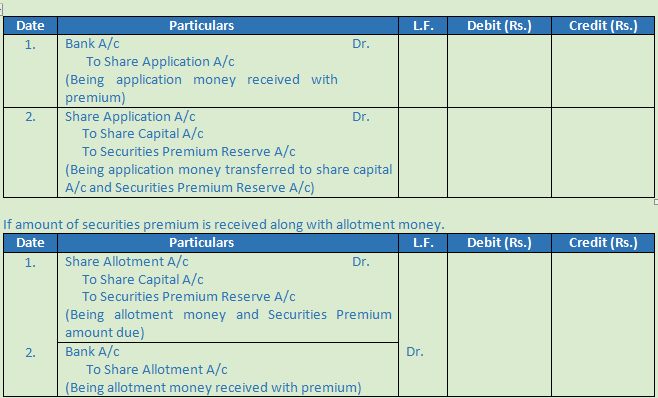

Solution 5 The amount of securities premium may be charged by the Company on application or on allotment or even with the calls.

Entries will be passed, if the amount of premium is received along with application money:

Question 6.

Solution 6 No, securities premium cannot be utilised for the purchases of fixed assets. According to section 52 (2) of the companies Act, 2014 the amount of Securities premium can be utilised only for the following purpose:

1.) In writing off the preliminary expenses of the company.

2.) For writing off the expenses, commission or discount allowed on issue of share or debentures of the company.

3.) For providing for the premium payable on redemption of redeemable preference shares or debentures of the company.

4.) For issuing fully paid bonus shares.

5.) For Buy back of its own shares and other securities as per section 68.

Question 7.

Solution 7 Securities Premium can utilized:-

1.) In writing off the preliminary expenses of the company.

2.) For writing off the expenses, commission or discount allowed on issue of share or debentures of the company.

3.) For providing for the premium payable on redemption of redeemable preference shares or debentures of the company.

Numerical Questions

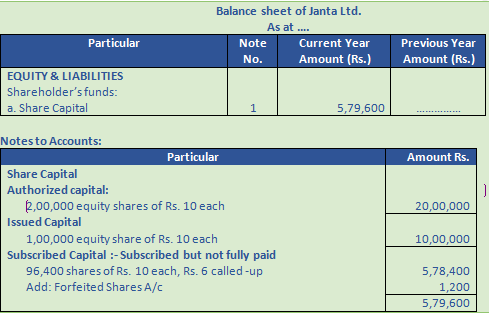

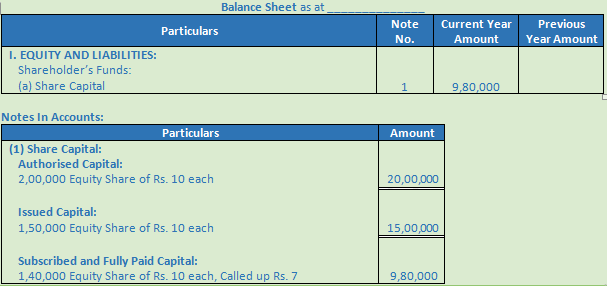

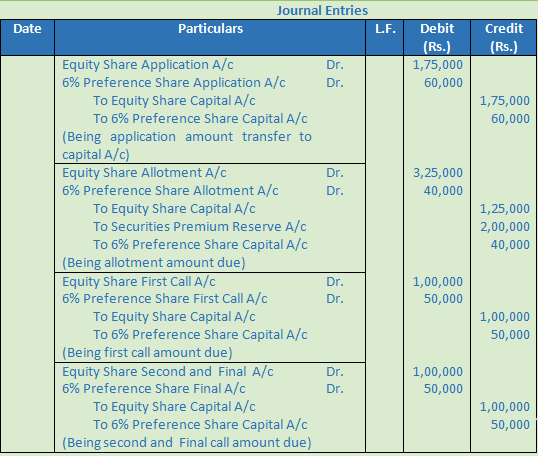

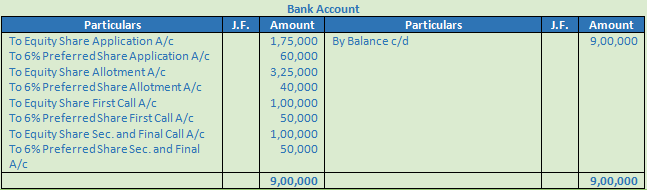

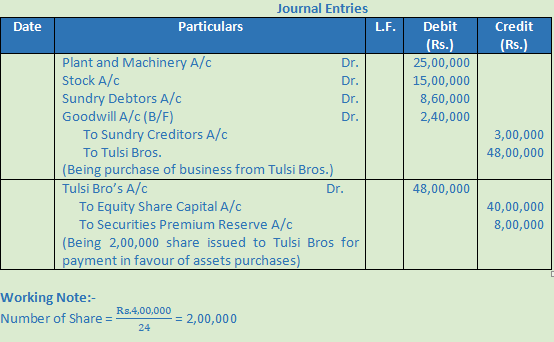

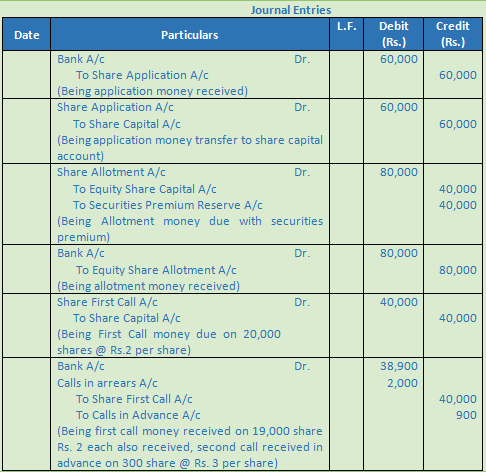

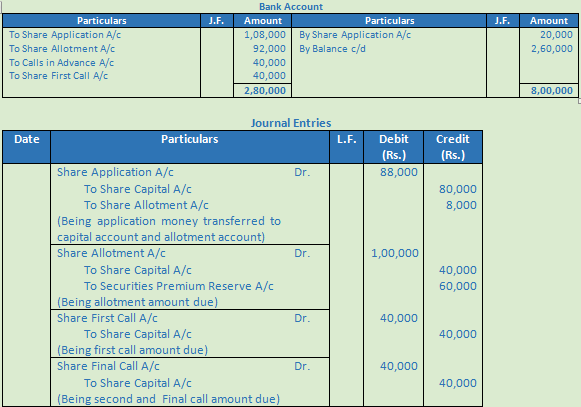

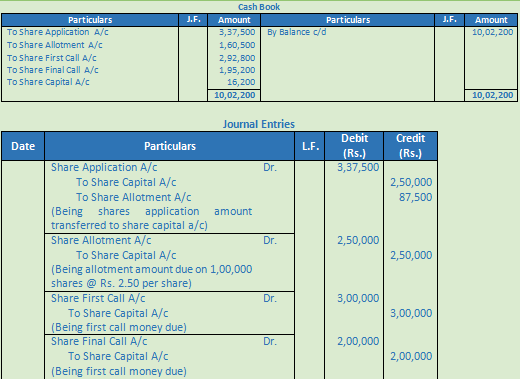

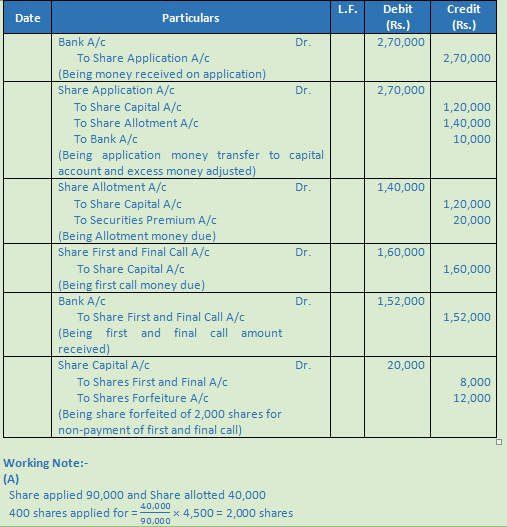

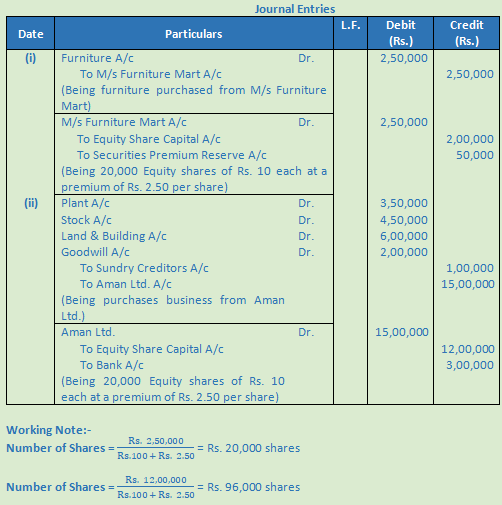

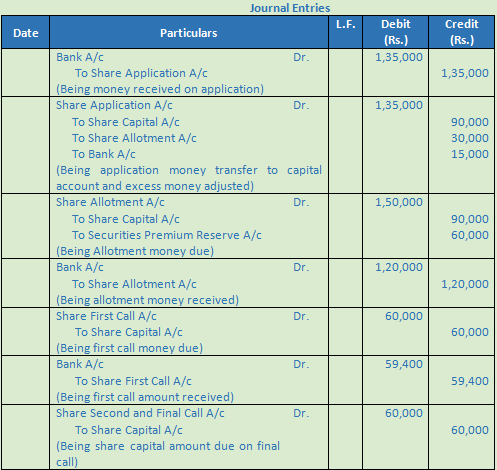

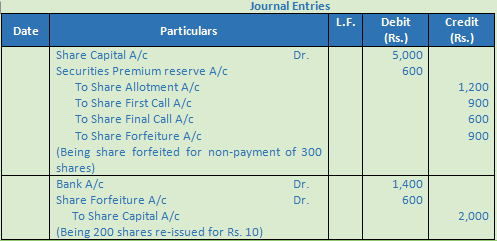

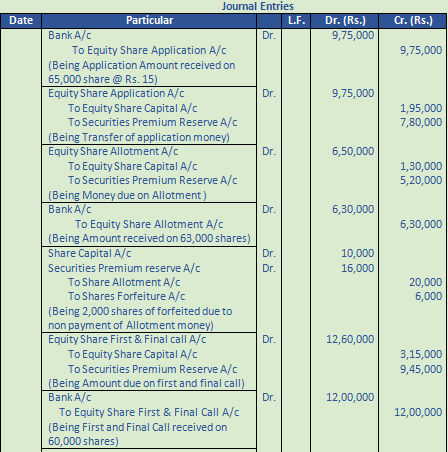

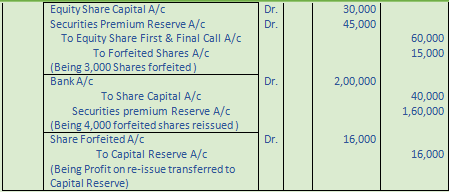

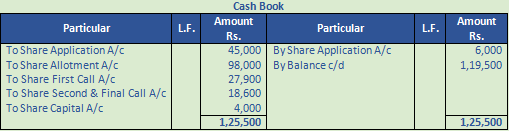

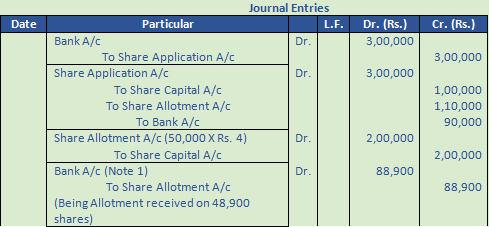

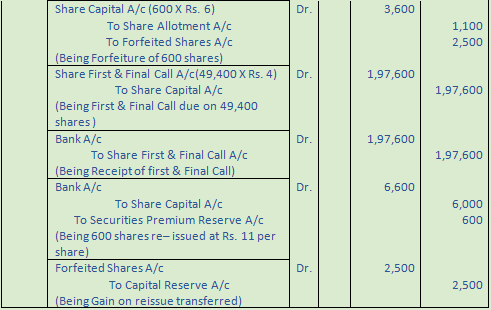

Question 1.

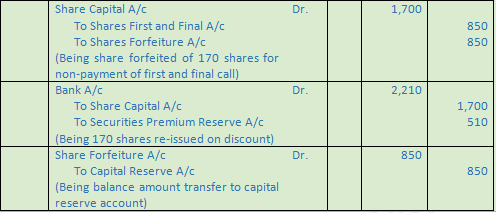

Solution 1

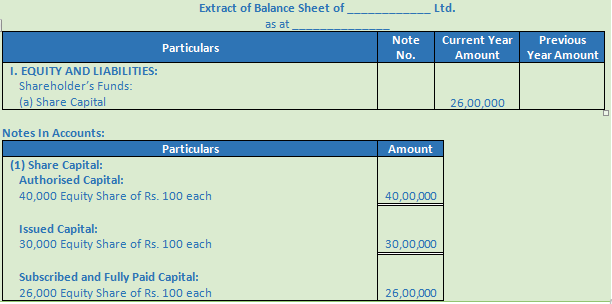

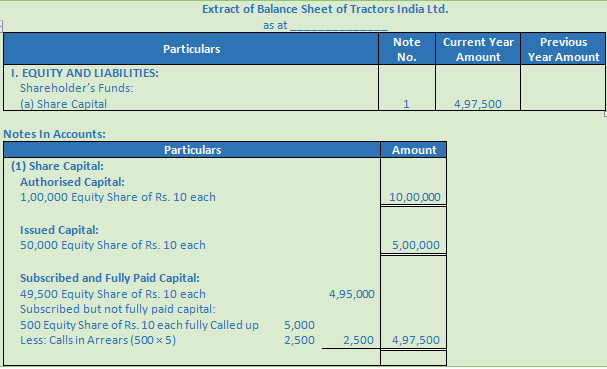

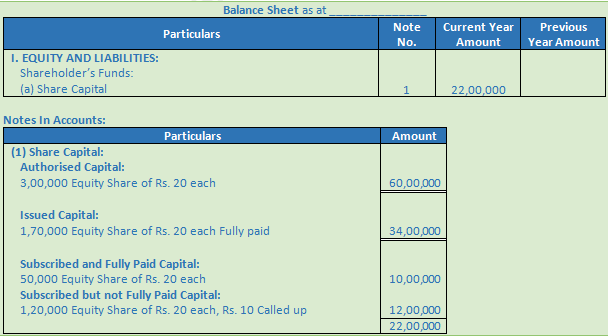

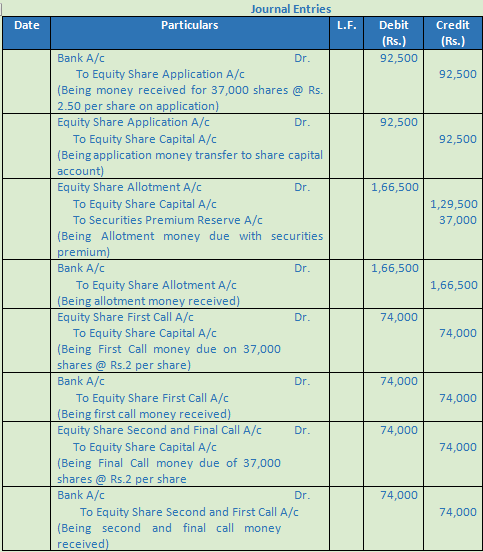

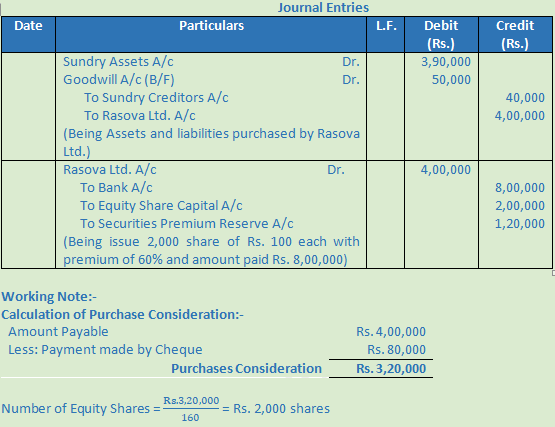

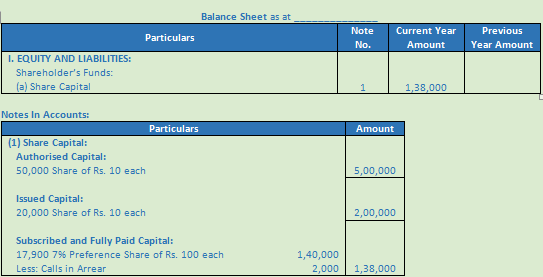

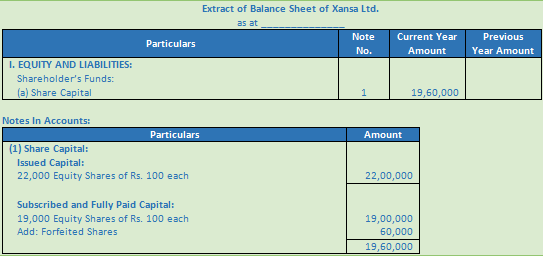

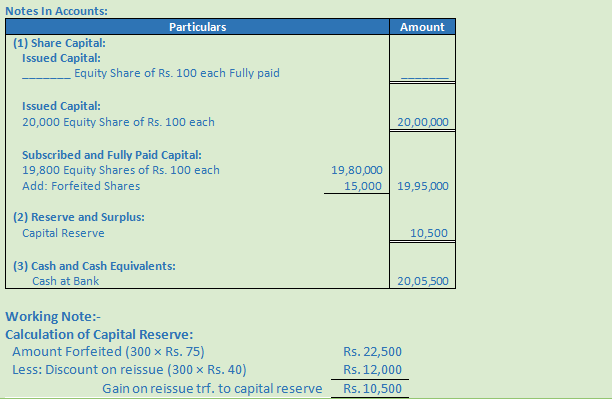

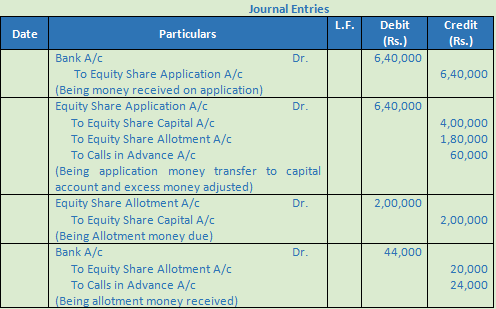

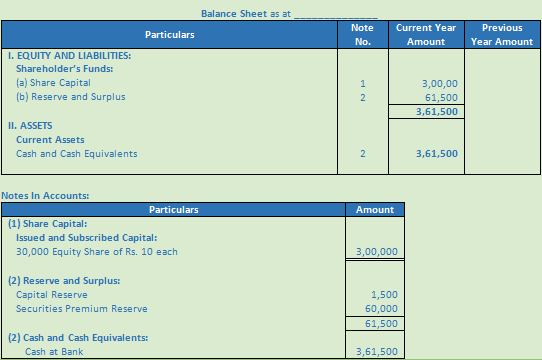

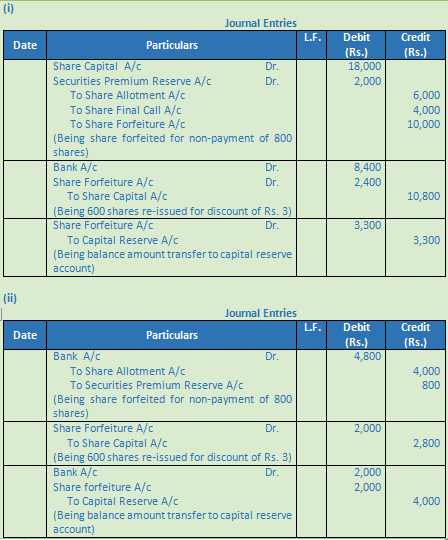

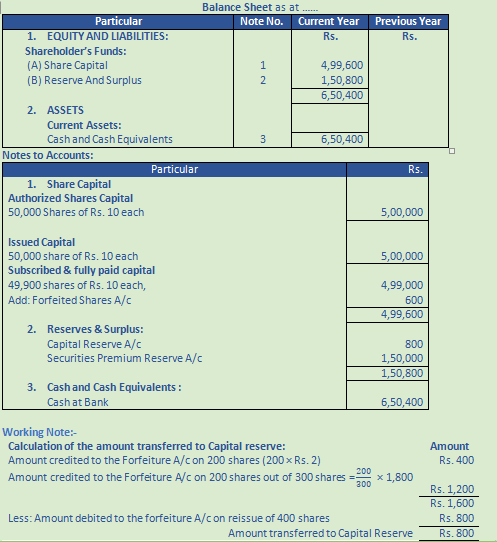

Question 2.

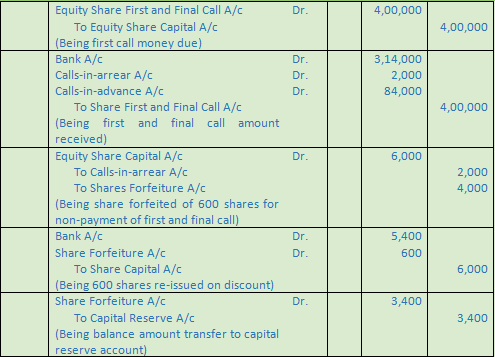

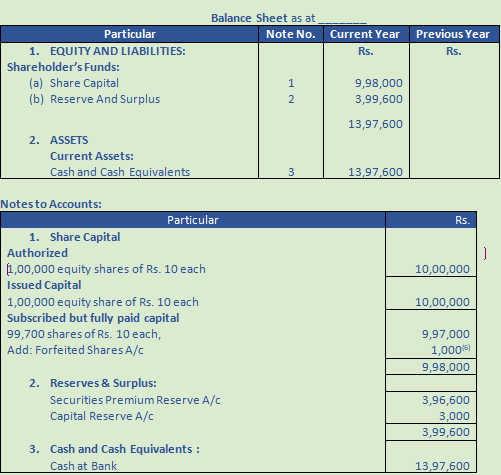

Solution 2 Extract of Balance Sheet of Tractors India Ltd.

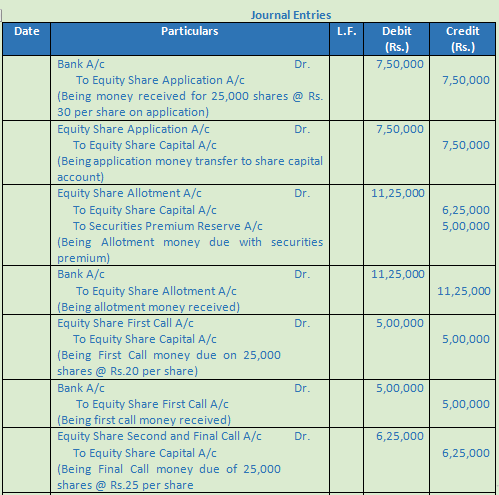

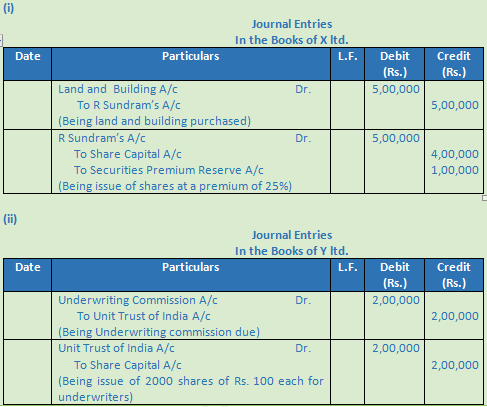

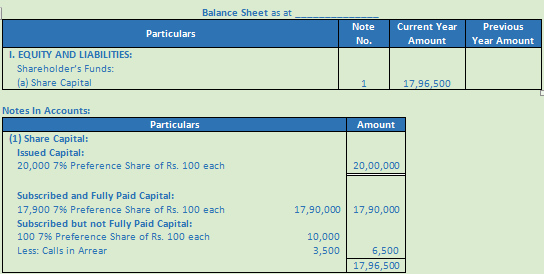

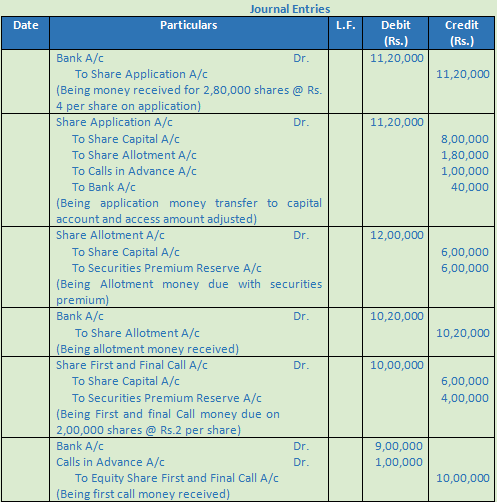

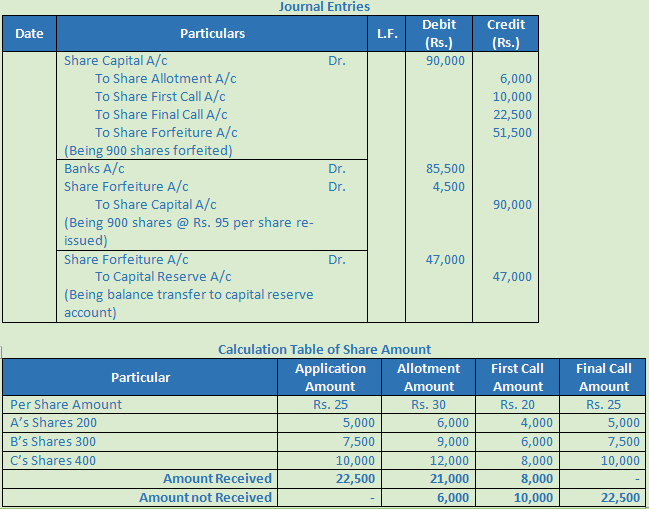

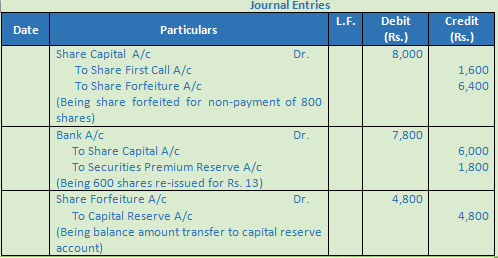

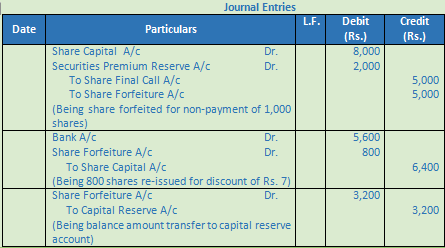

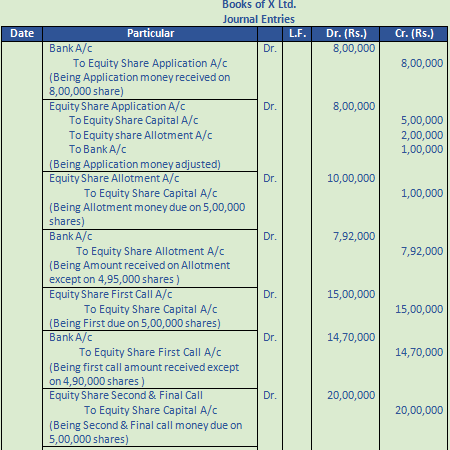

Question 3.

Solution 3

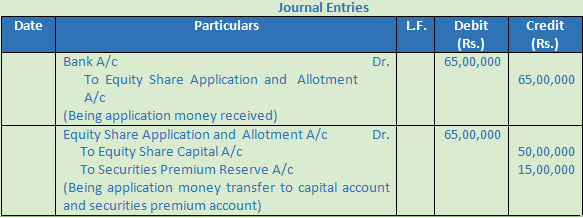

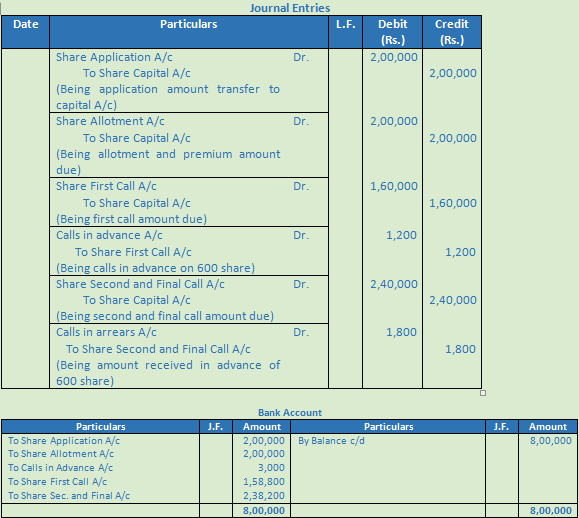

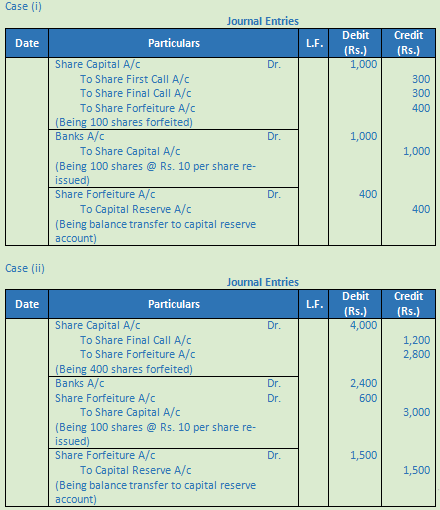

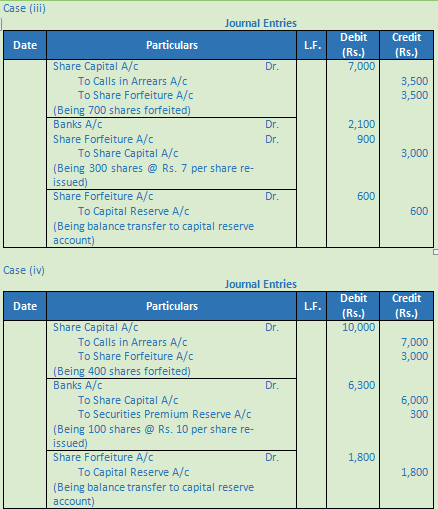

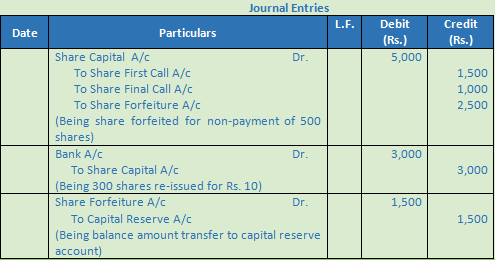

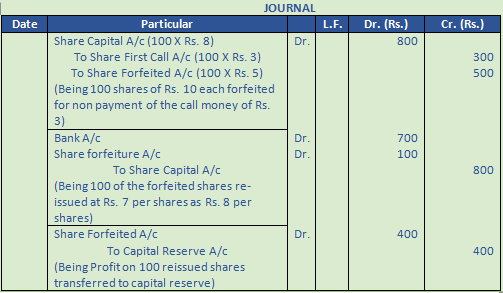

Question 4.

Solution 4

Question 5.

Solution 5

Question 6.

Solution 6

Question 7.

Solution 7

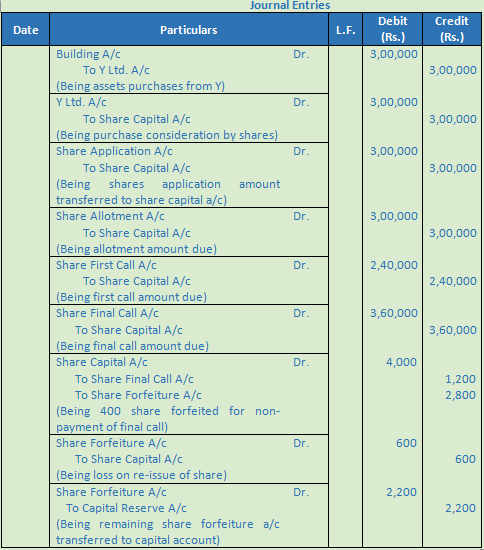

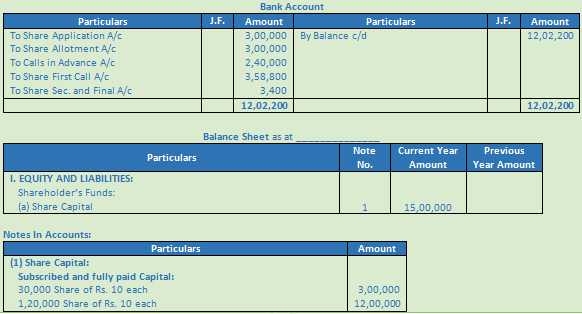

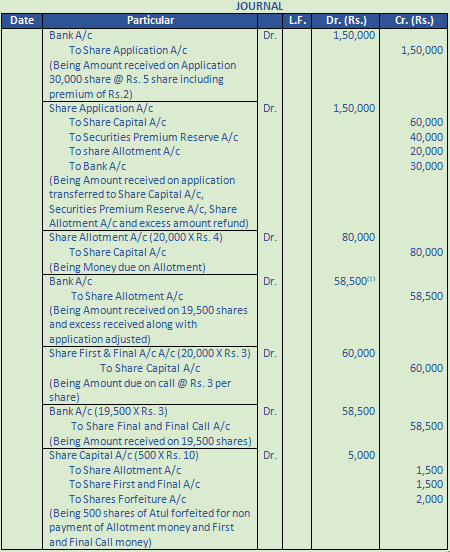

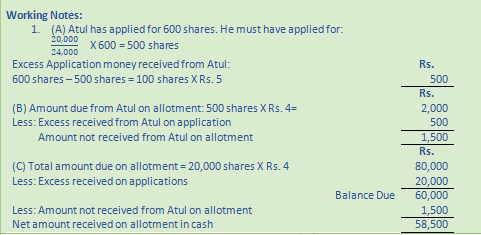

Question 8.

Solution 8

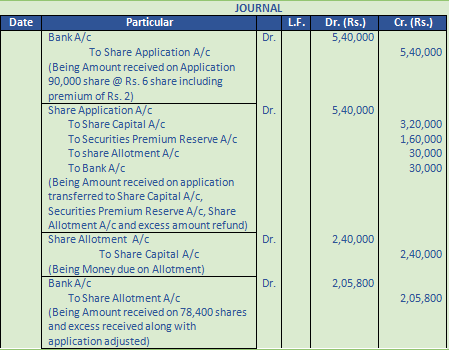

Question 9.

Solution 9

Question 10.

Solution 10

Question 11.

Solution 11

Question 12.

Solution 12

Question 13.

Solution 13

Question 14.

Solution 14

Question 15.

Solution 15

Question 16.

Solution 16

Question 17.

Solution 17

Question 18.

Solution 18

Question 19.

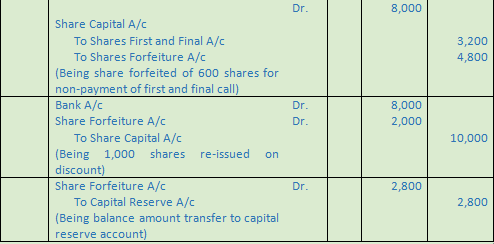

Solution 19

Question 20.

Solution 20

Question 21.

Solution 21

Question 22.

Solution 22

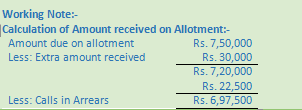

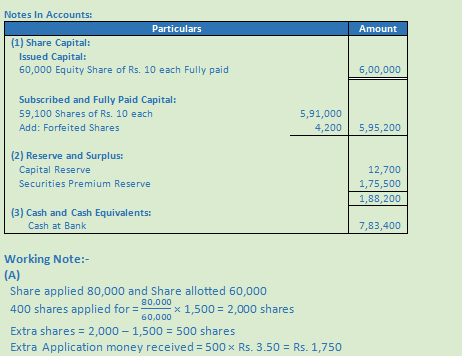

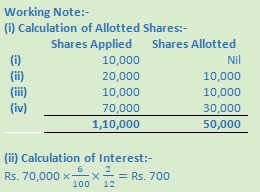

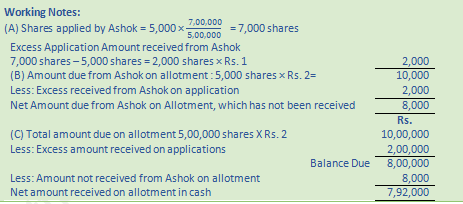

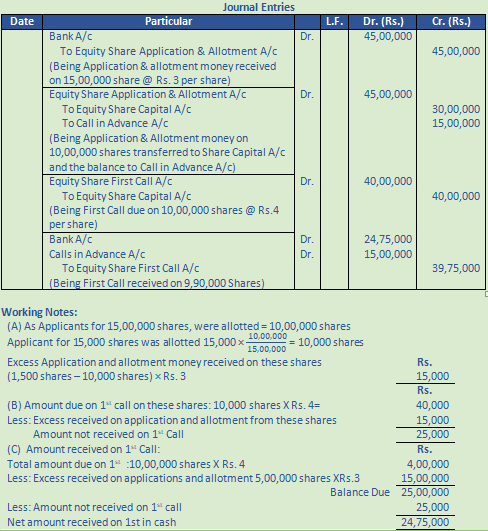

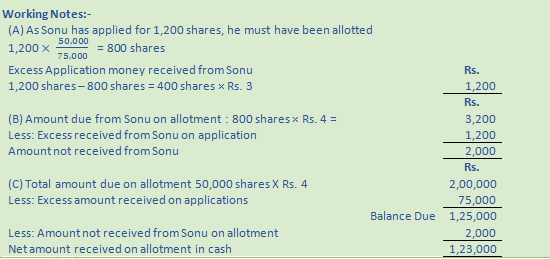

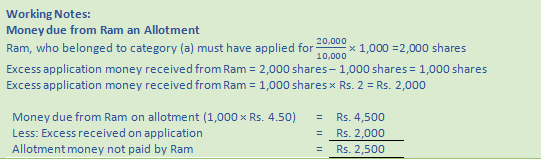

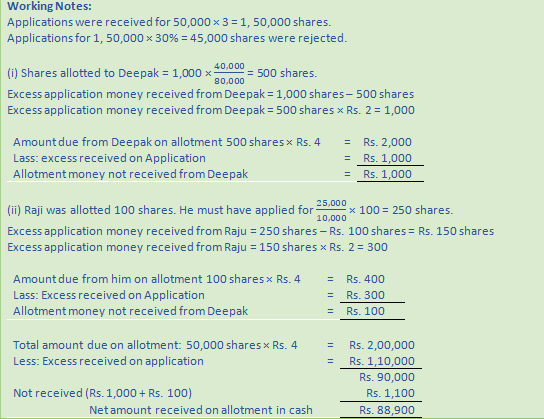

Working Note:-

Calculation of Access Money:-

70,000 Share @ Rs. 4 per share = Rs. 2,80,000

Less: Adjustment in Allotment 30,000 @ Rs. 6 = Rs. 1,80,000

Amount transferred to Call in advance = Rs. 1,00,000

Question 23.

Solution 23

Question 24.

Solution 24

Question 25.

Solution 25

Question 26.

Solution 26

Question 27.

Solution 27

Question 28.

Solution 28

Question 29.

Solution 29

Question 30.

Solution 30

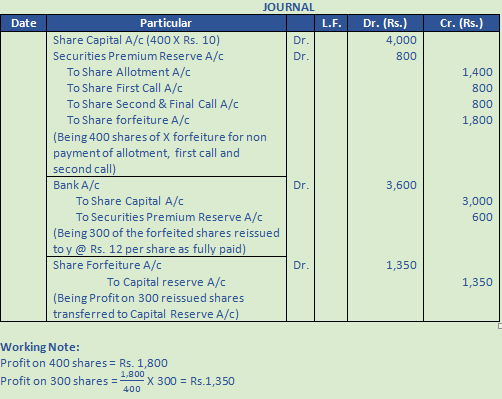

Question 31.

Solution 31

Question 32.

Solution 32

Question 33.

Solution 33

Question 34.

Solution 34

Question 35.

Solution 35

Question 36.

Solution 36

Question 37.

Solution 37

Question 38.

Solution 38

Question 39.

Solution 39

Question 40.

Solution 40

Question 41.

Solution 41

Question 42.

Solution 42

Question 43.

Solution 43

Question 44.

Solution 44

Question 45.

Solution 45

Question 46.

Solution 46

Question 47.

Solution 47

Question 48.

Solution 48

Question 49.

Solution 49

Question 50.

Solution 50

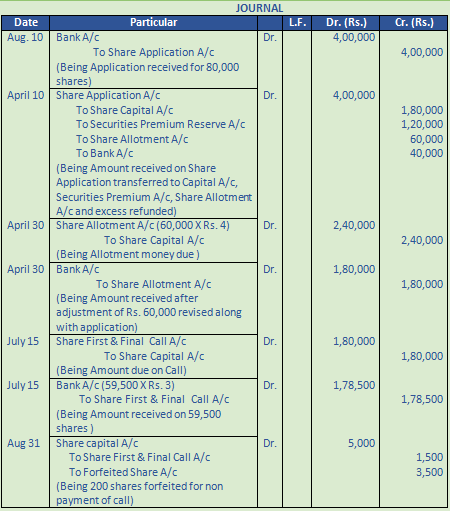

Extra money received from application:-

A applicant demand 2,00,000 shares allotted 1,00,000 shares = 1,00,000 × 3 = Rs. 3,00,000

Question 51.

Solution 51

Question 52.

Solution 52

Question 53.

Solution 53

Question 54.

Solution 54

Question 55.

Solution 55

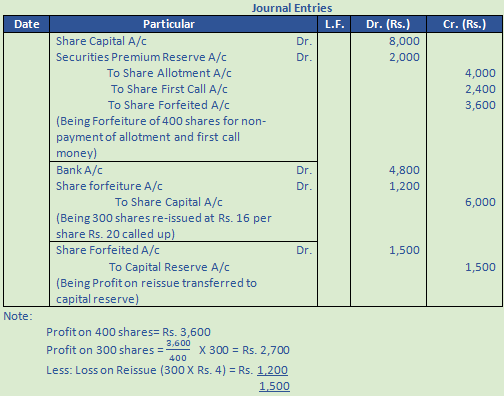

(B)

Allotment amount due = 500 shares × Rs. 20 = Rs. 10,000

Less: Extra amount received = Rs. 5,000

Amount not due on allotment = Rs. 5,000

Question 56.

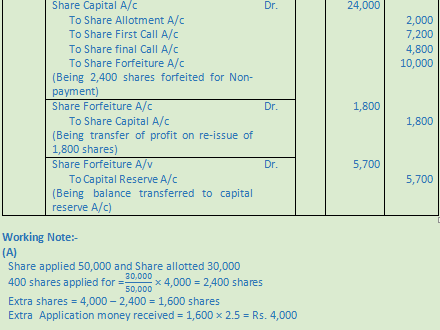

Solution 56

Question 57.

Solution 57

(B)

Allotment Amount due on 2,400 shares = 2,400 × Rs. 2.50 = Rs. 6,000

Less: Extra received on application from shares = Rs. 4,000

Amount not received on allotment = Rs. 2,000

(C)

Allotment Amount due on 1,00,000 shares = 1,00,000 × Rs. 2.50 = Rs. 2,50,000

Less: Extra received on application from shares = 35,000 × Rs. 2.50 = Rs. 87,500

Amount due on allotment = Rs. 1,62,500

Less: Amount not received on allotment = Rs. 2,000

Net Amount received = Rs. 1,60,500

Question 58.

Solution 58

Question 59.

Solution 59

(B)

Allotment Amount due on 400 shares = 400 × Rs. 4 = Rs. 1,600

Less: Extra received on application from shares = Rs. 600

Amount not received on allotment = Rs. 1,000

(C)

Allotment Amount due on 1,00,000 shares = 10,000 × Rs. 4 = Rs. 40,000

Less: Extra received on application from shares = Rs. 15,000

Amount due on allotment = Rs. 25,000

Less: Amount not received on allotment = Rs. 1,000

Net Amount received = Rs. 24,000

Question 60.

Solution 60

(B)

Allotment Amount due on 1,200 shares = 1,200 × Rs. 5 = Rs. 6,000

Less: Extra received on application from shares = Rs. 800

Amount not received on allotment = Rs. 5,200

(C)

Allotment Amount due on 60,000 shares = 60,000 × Rs. 5 = Rs. 3,00,000

Less: Extra received on application from shares = Rs. 40,000

Amount due on allotment = Rs. 2,60,000

Less: Amount not received on allotment = Rs. 5,200

Net Amount received = Rs. 2,54,800

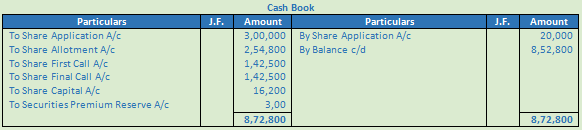

Question 61.

Solution 61

(B)

Allotment Amount due on 1,500 shares = 1,500 × Rs. 5.50 = Rs. 8,250

Less: Extra received on application from shares = Rs. 1,750

Amount not received on allotment = Rs. 6,500

(C)

Allotment Amount due on 60,000 shares = 60,000 × Rs. 5.50 = Rs. 3,30,000

Less: Extra received on application from shares = Rs. 70,000

Amount due on allotment = Rs. 2,60,000

Less: Amount not received on allotment = Rs. 6,500

Net Amount received = Rs. 2,53,500

Question 62.

Solution 62

Question 63.

Solution 63

(B)

Allotment Amount due on 800 shares = 800 × Rs. 5 = Rs. 4,000

Less: Extra received on application from shares = Rs. 300

Amount not received on allotment = Rs. 3,700

(C)

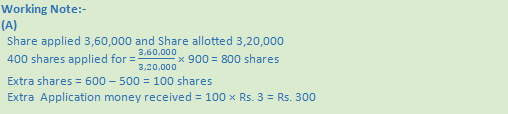

Allotment Amount due on 3,20,000 shares = 3,20,000 × Rs. 5 = Rs. 16,00,000

Less: Extra received on application from shares = Rs. 1,20,000

Amount due on allotment = Rs. 14,80,000

Less: Amount not received on allotment = Rs. 3,700

Net Amount received = Rs. 14,76,300

Question 64.

Solution 64

(B)

Allotment Amount due on 800 shares = 800 × Rs. 5 = Rs. 4,000

Less: Extra received on application from shares = Rs. 1,000

Amount not received on allotment = Rs. 3,000

(C)

Allotment Amount due on 2,00,000 shares = 2,00,000 × Rs. 5 = Rs. 10,00,000

Less: Extra received on application from shares = Rs. 2,50,000

Amount due on allotment = Rs. 7,50,000

Less: Amount not received on allotment = Rs. 3,000

Net Amount received = Rs. 7,47,000

Question 65.

Solution 65

(B)

Allotment Amount due on 1,125 shares = 1,125 × Rs. 6 = Rs. 6,750

Less: Extra received on application from shares = Rs. 3,375

Amount not received on allotment = Rs. 3,370

(C)

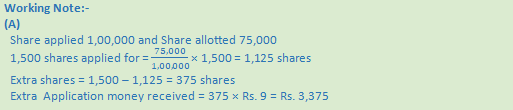

Allotment Amount due on 75,000 shares = 75,000 × Rs. 6 = Rs. 4,50,000

Less: Extra received on application from shares = Rs. 2,25,000

Amount due on allotment = Rs. 2,25,000

Less: Amount not received on allotment = Rs. 3,375

Net Amount received = Rs. 2,21,625

Question 66.

Solution 66

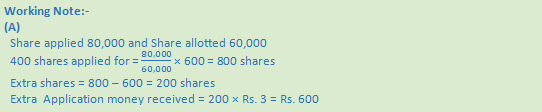

Working Note:-

(A)

Extra shares = 600 – 400 = 200 shares

Extra Application money received = 200 × Rs. 4 = Rs. 800

Allotment Amount due on 400 shares = 400 × Rs. 5.50 = Rs. 2,200

Less: Extra received on application from shares = Rs. 800

Amount not received on allotment = Rs. 1,400

Question 67.

Solution 67

Working Note:-

(A)

Extra shares = 2,250 – 1,500 = 750 shares

Extra Application money received = 750 × Rs. 5 = Rs. 3,750

Allotment Amount due on 1,500 shares = 1,500 × Rs. 3 = Rs. 4,500

Less: Extra received on application from shares = Rs. 3,750

Amount not received on allotment = Rs. 750

Question 68.

Solution 68

(B)

Allotment Amount due on 600 shares = 600 × Rs. 3 = Rs. 1,800

Less: Extra received on application from shares = Rs. 600

Amount not received on allotment = Rs. 1,200

(C)

Allotment Amount due on 1,00,000 shares = 1,00,000 × Rs. 3 = Rs. 3,00,000

Less: Extra received on application from shares = Rs. 1,50,000

Amount due on allotment = Rs. 1,50,000

Less: Amount not received on allotment = Rs. 1,200

Net Amount received = Rs. 1,48,800

Question 69.

Solution 69

(B)

First and Final Amount due on 800 shares = 800 × Rs. 8 = Rs. 6,400

Less: Extra received on application from shares = Rs. 2,700

Amount not received on First and Final call = Rs. 3,700

(C)

First and Final Amount due on 4,00,000 shares = 4,00,000 × Rs. 8 = Rs. 32,00,000

Less: Extra received on application from shares = Rs. 13,50,000

Amount due on allotment = Rs. 18,50,000

Less: Amount not received on allotment = Rs. 3,700

Net Amount received = Rs. 18,46,300

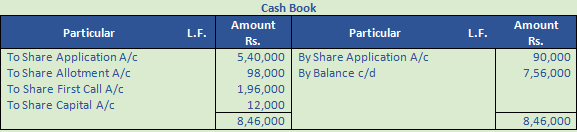

Question 70.

Solution 70

Allotment amount due = 2,000 × Rs. 5 = Rs. 10,000

Less: Actual Amount for Application = = Rs. 3,000

Amount not received from Ganesh Rs. 7,000

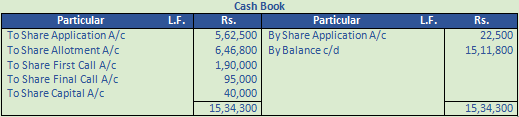

Net Amount received on Allotment = Rs. 1,50,000 – Rs. 30,000 – Rs. 30,000 – Rs. 4,000 – Rs. 6,000

Net Amount received on Allotment = Rs. 79,000

Question 71.

Solution 71

Question 72.

Solution 72

Question 73.

Solution 73

Question 74.

Solution 74

(B)

Allotment Amount due on 1,000 shares = 1,000 × Rs. 5 = Rs. 5,000

Less: Extra received on application from shares = Rs. 2,400

Amount not received on allotment = Rs. 2,600

(C)

Allotment Amount due on 50,000 shares = 50,000 × Rs. 5 = Rs. 2,50,000

Less: Extra received on application from shares = Rs. 1,20,000

Amount due on allotment = Rs. 1,30,000

Less: Amount not received on allotment = Rs. 2,600

Net Amount received = Rs. 1,27,400

Question 75.

Solution 75

(B)

Allotment Amount due on 1,200 shares = 1,200 × Rs. 6 = Rs. 7,200

Less: Extra received on application from shares = Rs. 5,400

Amount not received on allotment = Rs. 1,800

(C)

Allotment Amount due on 40,000 shares = 40,000 × Rs. 6 = Rs. 2,40,000

Less: Extra received on application from shares = Rs. 1,80,000

Amount due on allotment = Rs. 60,000

Less: Amount not received on allotment = Rs. 1,800

Net Amount received = Rs. 58,200

Question 76.

Solution 76

Working Note:-

Excess application money received from Vinita:

Extra shares = 700 – 400 = 300 shares

Extra Application money received = 300 × Rs. 50 = Rs. 15,000

(ii) Amount Due from Vinita:-

Allotment Amount due on 400 shares = 400 × Rs. 70 = Rs. 28,000

Less: Extra received on application from shares = Rs. 15,000

Amount not received on allotment = Rs. 13,000

Question 77.

Solution 77

Question 78.

Solution 78

Question 79.

Solution 79

Question 80.

Solution 80

Question 81.

Solution 81

Question 82.

Solution 82

Question 83.

Solution 83

Question 84.

Solution 84

Question 85.

Solution 85

Question 86.

Solution 86

Question 87.

Solution 87

Question 88.

Solution 88

Question 89.

Solution 89

Question 90.

Solution 90

Question 91.

Solution 91

Question 92.

Solution 92

Question 93.

Solution 93

Question 94.

Solution 94

Question 95.

Solution 95

Question 96.

Solution 96

Question 97.

Solution 97

Question 98.

Solution 98

Question 99.

Solution 99

Question 100.

Solution 100

Question 101.

Solution 101

Question 102.

Solution 102

Question 103.

Solution 103

Question 104.

Solution 104

Question 105.

Solution 105

Question 106.

Solution 106

Question 107.

Solution 107

Question 108.

Solution 108

Question 109.

Solution 109

Question 110.

Solution 110

Question 111.

Solution 111

Question 112.

Solution 112

Question 113.

Solution 113

Question 114.

Solution 114

Question 115.

Solution 115

Question 116.

Solution 116

Question 117.

Solution 117

Question 118.

Solution 118

Question 119.

Solution 119

Question 120.

Solution 120

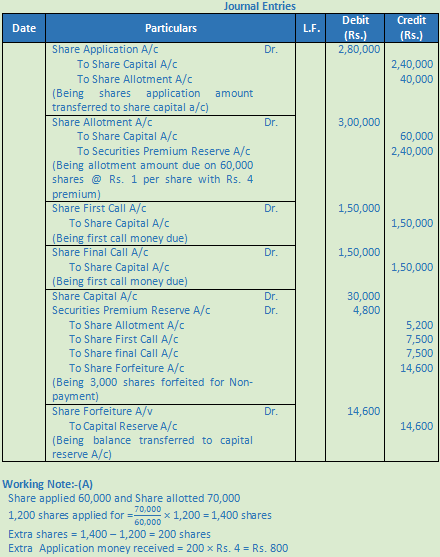

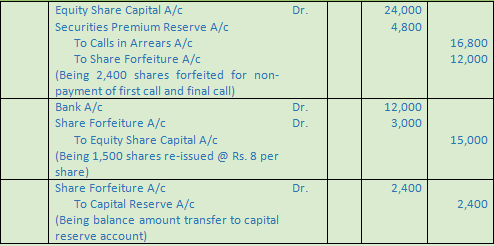

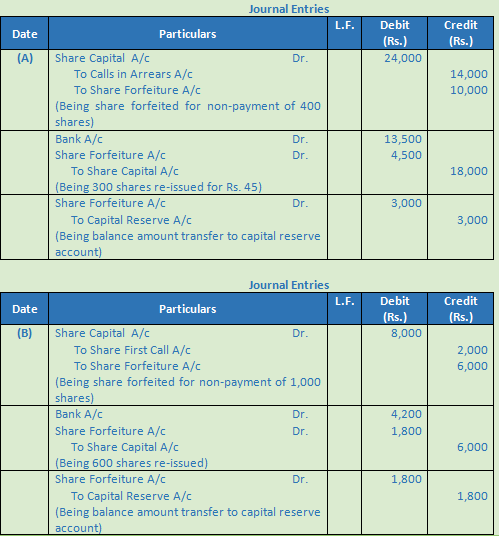

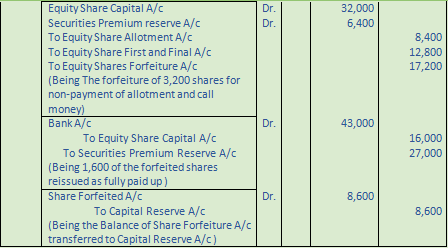

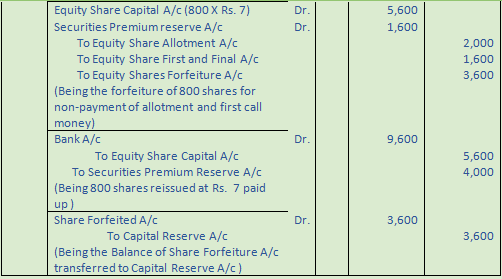

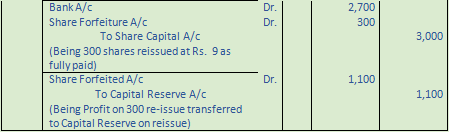

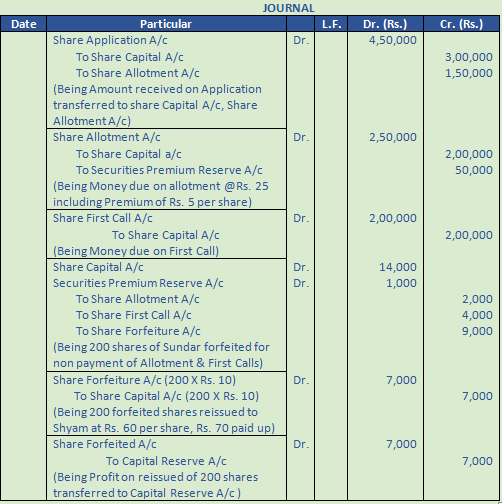

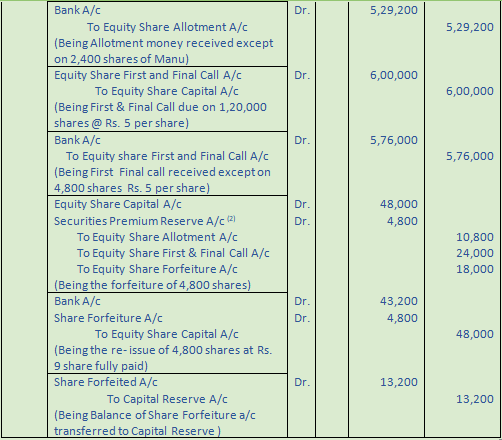

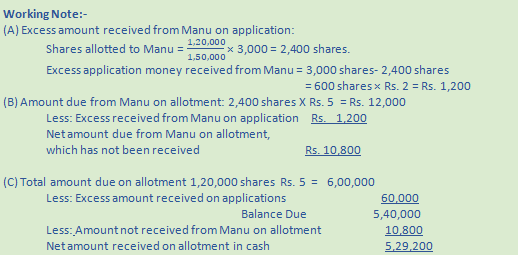

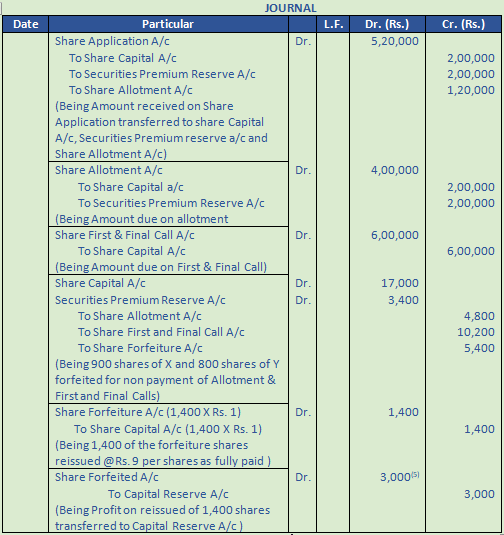

Premium is due with allotment and only Manu has not paid the amount of allotment. Therefore, Securities Premium Reserve account has been debited from the amount of premium due from Manu only i.e., 2,400 shares × Rs. 2= Rs. 4,800.

Question 121.

Solution 121

Question 122. .

Solution 122

Question 123.

Solution 123

Question 124.

Solution 124

Question 125.

Solution 125

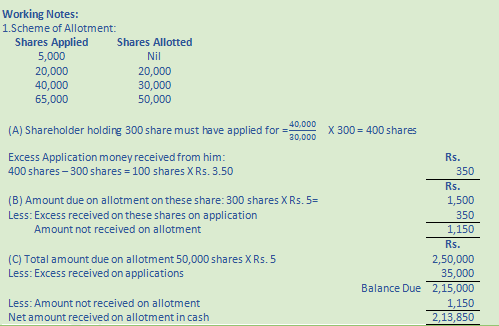

Rs.

Total amount due on Allotment (including premium): 60,000 X Rs. 5 3,00,000

Less: (i) Excess money received in Application in Category A:

30,000 Shares- 20,000 Shares= 10,000 Shares X Rs. 3 30,000

(ii) Excess money received on Application in Category B:

50,000 Shares – 40,000 Shares = 10,000 Shares X Rs. 3 30,000

Question 126.

Solution 126

Question 127.

Solution 127

Question 128.

Solution 128

Question 129.

Solution 129

Question 130.

Solution 130

Working note:

Excess Shares applied from Dev = 2,500 shares – 1,000 shares = 1,500 Shares

Excess application money received from Dev = 1,500 shares × Rs. 15 = Rs. 22,500

Question 131.

Solution 131

Question 132.

Solution 132