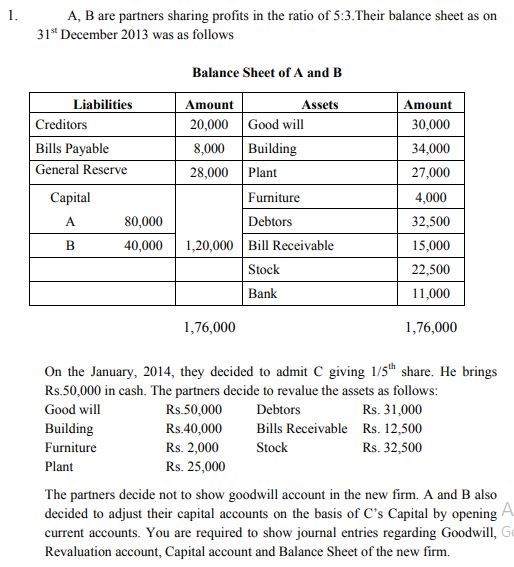

Read and download the CBSE Class 12 Accountancy Revision Worksheet in PDF format. We have provided exhaustive and printable Class 12 Accountancy worksheets for All Chapters, designed by expert teachers. These resources align with the 2026-27 syllabus and examination patterns issued by NCERT, CBSE, and KVS, helping students master all important chapter topics.

Chapter-wise Worksheet for Class 12 Accountancy All Chapters

Students of Class 12 should use this Accountancy practice paper to check their understanding of All Chapters as it includes essential problems and detailed solutions. Regular self-testing with these will help you achieve higher marks in your school tests and final examinations.

Class 12 Accountancy All Chapters Worksheet with Answers

Q. 1. Explain the meaning of the following terms with example:

a. Goods;

b. Expenses.

Q. 2. Show the accounting equation on the basis of the following transactions & Prepare Balance Sheet:

i. Sohan started business with cash Rs.40,000, goods Rs.20,000, furniture Rs.1,000 & Creditors of Rs. 6,000.

ii. Sold goods to Vikram costing Rs.4,000 @ 10% above cost.

iii. Purchase Building Worth Rs. 1,00,000 by taking Bank Loan.

iv. Bought Good Worth Rs. 5,000 from Ram and Received Cash Discount @ 5%.

v. Purchase Goods from Raju worth Rs. 10,000.

vi. Rent due to landlord for current month.

vii. Advance Salary paid to Mohan an Employee Rs. 2,000.

viii. Returned goods of Rs.2,000 purchased from Raju.

Q. 3. Give Journal entries in the books of Ram Dayal Furniture: 2009

Jan 1. Received Rs. 5,000 from B/R of Mahesh Chand.

Jan 2. Bought machinery Worth Rs. 9,800 & Paid cartage on it Rs. 200 & Paid wages Rs. 2,000 for the Installation of Machinery.

Jan 3. Bought Furniture from Shruti & Co. List Price Rs. 20,000 & Received TradeDiscount @ 10%. Half the Payment made at the time of Purchase & receivedCash Discount for the prompt payment @ 5%.

Jan 5. Furniture worth Rs. 2,000 transfer to Ram Dayal’s House for the Decoration.

Jan 8. Paid Rent Rs. 3,000 to Landlord up March 2009.

Jan 12. Sold to Surender Furniture Costing Rs. 8,000 at profit of 20% on Sale; andalso allowed him trade Discount of 10%.

Jan 23. Paid Outstanding Salaries for the December, 2008; Rs. 12,000.

Jan 29. Received Compensation from Ramu 70 paise in Rupee One from his total Debt of Rs. 2,300, on the Event of his insolvency.

Q. 4. Following are the transaction of Amar Ltd post them into the `T Shape’ ledger of Rakesh. (4)2009

Feb 1 Rakesh purchased goods of Rs.5000

Feb 3 Rakesh sold goods of Rs.30000 to Amar

Feb 8 Rakesh paid cash of Rs.2000

Feb 10 He returned goods of Rs.2000 purchased by him

Q. 5. Ram Started Business with the Capital of Rs. 2,50,000. During he Year 2008- 09 he withdrews for his Capital of Rs. 5,0000. His Assets & Liabilities are Rs. 5,00,000 & Rs. 2,25,000 respectively as 31st March 2009. Find out profit earned or Loss incurred by him during the financial year 2008-09

1. A Ltd. purchased machinery from B Ltd. amounting ₹95,000. Payment was to be made as follow:

20% of the cost of machinery in cash and balance by issue of preference shares of ₹20 each at a discount of 5%.

Pass the requisite Journal entries in the books of A Ltd.

What is the number of preference shares to be issued by A Ltd. A Ltd. purchased machinery from B Ltd. amounting ₹95,000. Payment was to be made as follow: 20% of the cost of machinery in cash and balance by issue of preference shares of ₹20 each at a discount of 5%.Pass the requisite Journal entries in the books of A Ltd.

2. Reliance Ltd. issued ₹1,00,000 shares of ₹10 each at a premium of ₹2 each as follows:

Application ₹2

Allotment ₹5 (including premium)

First call ₹2

Final call ₹3

All the shares were applied for and allotted. All the moneys were received except one shareholder holding ₹1,000 shares that could not pay allotment and first call money. His shares were forfeited after the first call was made. Final call was made afterwards and the money was duly received. ₹600 of the forfeited shares were reissued at ₹9 per share as fully paid-up.

Pass the requisite Journal entries in the books of Reliance Ltd.

3. Jain Ltd. offered ₹1,00,000 equity shares of ₹10 each at a premium of ₹2 each for Public subscription. The amount was payable, as follows:

Application ₹2

Allotment ₹5 (including premium)

First call ₹2

Final call ₹3

Applications were received for ₹1,95,000 shares. The allotment was made as follows:

Category-I: Applications for ₹10,000 shares were rejected

Category-II: Full allotment was made to the applicants for ₹15,000 shares

Category-III : Pro-rata allotment was made to the other applicants with the stipulation that the excess money shall be applied for at the time of allotment

All the moneys were received except in the case of :

(a) Ajay holding ₹1000 shares that could not pay allotment and first call money. His shares were forfeited after the first call was made. (Belongs to category-III)

(b) Another shareholder Vijay who has applied for ₹1,000, however, could not pay the two calls. His shares were forfeited after the Final call was made. (Belongs to category-III)

₹700 of the forfeited shares were reissued at ₹8 per share, as fully paid-up (whole of Vijay’s shares being included).

Pass the requisite Journal entries in the books of Jain Ltd.

4. Why Company is called an artificial person? 1

5. What do you mean by issuing shares at premium? State any three purposes for which the balance of share premium account can be utilized.

1. Give two circumstances in which sacrificing ratio may be applied?

2. How the factors of nature affecting the goodwill of the partnership firm?

3. What do you mean by partnership deed?

4. Give one difference between Revaluation Account & Realization Account?

5. What are super profits?

6. Where would you record interest on capital when capitals are fixed?

7. Distinguish between Sacrificing Ratio & Gaining Ratio.

8. The books of the business showed that the capital employed was10 Lakh and the profits for the last five years were ₹80,000, ₹1,00,000, ₹1,10,000,

₹1,40,000 and ₹1,70,000. You are required to find out the value of goodwill based on 3 years purchase of Super Profits of the business given that the normal rate of return is 10%.

9. A, B and C were partners in a firm. On 1st April 209 their fixed capitals stood at ₹50,000, ₹25,000 and ₹25,000 respectively.

As per the provisions of the partnership deed:

a) B was entitled for a salary of ₹5,000 p.a.

b) All the partners were entitled to interest on capital at 5% p.a.

c) Profits were to be shared in the ratio of capitals and C gets a guaranteed amount of profit ₹ 10,000 every year.

d) Any deficiency arises, it will be borne by A.

The net profit for the year ending 31.03.2010 of ₹45,000 was divided equally without providing for the above terms.

Pass an adjustment journal entry to rectify the above error.

10. A and B were partners sharing profits and losses in the ratio of 3:2. They admitted C into partnership for 1/5th share in profits. C brought ₹50,000 as capital and ₹10,000 as his share of goodwill. At the time of admission goodwill was appearing in the books at ₹3,000. A and B withdrew half of their share of goodwill from the firm. Partners decided to share future profits in the ratio of 5:3:2. Pass necessary journal entries.

11. Neena and Meena were partners. The partnership deed provided for:

a) Profits to be divided as Neena 2/5 and Meena 3/5

b) The accounts are closed on March 31st each year

c) In the event of death of a partner the executors will be entitled to:

I. Capital to credit on the date of death

II. Interest on capital at 12% p.a.

III. Interest on drawing 6% p.a.

IV. Proportion of profit to the date of death based on the average profits for the last three years.

V. Share of goodwill based on 3 years purchase of average profits of preceding 3 years.

The following information is provided to you:

Neena’s Capital ₹1,20,000, Meena’s Capital ₹80,000, Reserves ₹30,000, Cash ₹1,10,000 and Goodwill ₹70,000.

Prepare Neena’s Capital Account to be presented to her executors who died on 31-May-07. The profits for the three preceding years were ₹84,000, ₹90,000 and ₹99,000.

12. Following was the balance sheet of D, T and G as at 28-Feb-02.

| Liabilities | ₹ | Asset | ₹ |

Creditors | 50,000 10,000 8,000 12,000 20,000 2,50,000 | Bank Debtors Stock Furniture Land & building G’s Capital | 20,000 30,000 20,000 15,000 2,45,000 20,000 |

| 3,50,000 | 3,50,000 |

The firm was dissolved on the above date on the following terms.

I. Debtors realized ₹28,000, Creditors and bills payable were paid at a discount of 10%.

II. Stock was taken by T for ₹15,000 and furniture was sold to N for ₹12,000.

III. Land and building were sold for ₹2,80,000.

IV. R’s loan was paid by cheque for the same amount

V. Firm had a joint life policy of ₹5,00,000 with a surrender value of ₹1,00,000. The policy was surrendered at its surrender value.

Prepare the Realization Account, Bank Account and Partners Capital Account.

13. Ramesh, Suresh and Dinesh were partners in a firm sharing profit in the ratio of 3:3:4. Their capitals were ₹5,00,000, ₹4,00,000 and ₹5,00,000 respectively. The firm closes its books on 31st March every year. On 30-Sept-06 Ramesh died. The executor of a deceased partner, according to the agreement, was entitled for the following.

I. Interest on capital from the first day of the accounting year till the date of his death @9% p.a.

II. His share of goodwill – The goodwill of the firm was valued at ₹1,80,000.

III. His share of profits – The profit of the firm till his date of death was ₹1,20,000.

IV. His drawing was ₹60,000 and interest on drawing charged at 6%. Ramesh Executor was paid the sum due in two equal annual installments with interest @10% p.a. Pass necessary journal entries and prepare Ramesh’s capital account.

14. Pass the necessary journal entries for the following transactions of the dissolution of the firm of Geethu and Meethu after the various assets (other than cash) and outside liability have been transferred to realization account.

I. Creditors paid ₹18,500 in full settlement of their claims of ₹21,000

II. Geethu agreed to pay her hunband’s loan ₹17,000

III. Other assets realized ₹80,000

IV. Expenses of realization ₹25,000 were paid by Meethu

V. Stock ₹40,000 was taken over by Meethu for ₹40,000

VI. Profit on dissolution ₹9,000 was divided between Geethu & Meethu in the ratio of 2:1.

15. A, B and C are partners sharing profits and losses in the ratio of 2:3:5. On 31-Mar-10 their balance sheet was

| Liabilities | ₹ | Asset | ₹ |

| Capital Account A B C Creditors Bill Payable Profit & Loss Account | 36,000 44,000 52,000 64,000 32,000 14,000 | Cash Bills receivable Furniture Stock Debtors Investments Machinery Goodwill | 18,000 24,000 28,000 44,000 42,000 32,000 34,000 34,000 |

| 2,42,000 | 2,42,000 |

They admit D into partnership on the following terms:

I. Furniture, investments & machinery to be depreciated by 15%

II. Stock is revalued at ₹48,000

III. Outstanding rent amounted to ₹1,800,

IV. Prepaid salaries 800

V. D brings in ₹32,000 as his capital and ₹6,000 for goodwill in cash for 1/6th share of future profits of the firm.

VI. Adjustment of capitals to be made in cash

VII. Capital of the partner shall be proportionate to their profit sharing ratio taking D’s capital as basePrepare Revaluation Account, Partner’s Capital Account and the Balance Sheet of the new firm.

1. A, B and C are partners. Their capital accounts stood at Rs 30000, Rs 15000 and Rs 15000 respectively on 1st Jan 1996.As per the provisions of the deed.

i) C was to be allowed a remuneration of Rs 3000 per annum.

ii) Interest @ 5% p.a was to be provided on capital.

iii) Profits were to be divided in the ratio of 2:2:1.

Ignoring the above terms net profit of Rs 18000 for the year ended 1996 was divided among the three partners equally. Pass and adjustment entry to rectify the error.

2. X, Y and Z are partners sharing profits in the ratio of 3:2:1.Now the partners decide to share profits in the ratio of 2:2:1.They have also decided that the change shall be carried out with retrospective effect from1995.The profits and losses during the last few years have been 1994 – Rs 16000,1995- Rs 12000,1996 – Rs 14000 ,1997-Rs 19000,1998-Rs 15000 (Loss)

Pass and adjustment entry.

3. A and B are partners sharing profits in the ratio of 2:1.They admit ‘C’ for ¼ share in profits. ‘C’ brings Rs 30000 for his capital and Rs 8000 for his share of G/w .Before admission g/w appeared in the books at Rs 18000.Give journal entries.

4. A and C are partners sharing profits and losses in the ratio of 7:3. ‘A’ surrenders ¼ th of his share and ‘C’ surrenders 1/3rd of his share in favour of ‘Z’ ,a new partner.Calculate the new profit sharing ratio.

5. Asha,Deepa and lata are the partners in a firm sharing profits in the ratio of 3:2:1.Deepa retires after making all adjustments relating revaluation/w and accumulated profit etc.,the capital accounts of Asha and Lata showed a credit balance of Rs 1,60,000 and Rs 80,000 respectively. It was decided to adjust the capitals of Asha and Lata in their new profit sharing ratio .You are required to calculate the new capitals of the partners and record necessary new journal entries for bringing in or withdrawal of the necessary amounts involved.

6. A,B,C are partners in a firm sharing profits in the ratio of 4:3:1.A retires and his share is taken by B and C equally.Find the new profit sharing ratio and gain ratio. The g/w of the firm is valued at Rs 16000.Pass necessary journal entries for recording G/W.

7. Ali and Arib are partners in a firm sharing profits in the ratio of 4:1.They had insured their lives jointly for Rs 5,00,000.Ali dies 3 months after date of the last Balance Sheet. According to the partnership deed, legal representatives of the deceased partner were entitled for the following payments. (i)His capital Rs 1, 50,000 as per the last balance sheet.

(ii)Interest on capital @ 12% p.a. (iii)His share of profit to the date of death calculated on the basis of the average profits of last three years were Rs 1,00,000,Rs 1,50,000 and Rs 2,00,000. Prepare Ali’s capital account to by rendered to his representatives and the Executors account.

8. How will you deal with following items while preparing the final accounts of the club?

1-4-2007 (in Rs) 31-3-2008 (in Rs)

Stock of stationary 40000 30000

Creditors fro stationary 72000 54000

Amount paid for stationary during the year 2007 -2008- Rs 2,50,000.

9. From the following information calculate the amount of subscription to be credited to the income and Expenditure Account for the year 2007-08.

Subscription received during the year Rs 40000

Subscription outstanding on 31st March 2007 Rs 11000

Subscription outstanding on 31st March 2008 Rs 5000

Subscription received in advance on 31st March 2007 Rs 10000

10. The directors of a company forfeited 300 shares of Rs 10 each issued at a premium of Rs 3 per share,for the non-payment of the first call money of Rs 2 per share. The final call for Rs 2 per share has not been made.Half the forfeited share were reissued at Rs 1500 fully paid. Record journal entrie for the forfeiture and reissue of shares.

11. Vt Ltd.Forfieted 20 shares of Rs 10each (7 called up) issued at a discount of 10% to Meena on which she had paid Rs 2 per share .Out of these 18 shares were reissued to Neeta as Rs 8 called up for Rs 6 per share.Give journal entries to record forfeiture and reissue of shares./

12. JCM Ltd invited applications for issuing 20000 equity shares of Rs 20 each at a discount of 10 %.The whole amount was payable on application.The issue was fully subscribed .Pass necessary journal entries.

13. Write two items on credit side of partners current accounts.

14. A,B and C are partners sharing profits and losses in the ratio of 3:2:1. ‘B’ retires.What will be the new profit sharing ratio.

15. Why profit and loss appropriation is prepared?

| CBSE Class 12 Accountancy Accounting for Not for Profit Organisation Worksheet |

CBSE Accountancy Class 12 All Chapters Worksheet

Students can use the practice questions and answers provided above for All Chapters to prepare for their upcoming school tests. This resource is designed by expert teachers as per the latest 2026 syllabus released by CBSE for Class 12. We suggest that Class 12 students solve these questions daily for a strong foundation in Accountancy.

All Chapters Solutions & NCERT Alignment

Our expert teachers have referred to the latest NCERT book for Class 12 Accountancy to create these exercises. After solving the questions you should compare your answers with our detailed solutions as they have been designed by expert teachers. You will understand the correct way to write answers for the CBSE exams. You can also see above MCQ questions for Accountancy to cover every important topic in the chapter.

Class 12 Exam Preparation Strategy

Regular practice of this Class 12 Accountancy study material helps you to be familiar with the most regularly asked exam topics. If you find any topic in All Chapters difficult then you can refer to our NCERT solutions for Class 12 Accountancy. All revision sheets and printable assignments on studiestoday.com are free and updated to help students get better scores in their school examinations.

You can download the latest chapter-wise printable worksheets for Class 12 Accountancy Chapter All Chapters for free from StudiesToday.com. These have been made as per the latest CBSE curriculum for this academic year.

Yes, Class 12 Accountancy worksheets for Chapter All Chapters focus on activity-based learning and also competency-style questions. This helps students to apply theoretical knowledge to practical scenarios.

Yes, we have provided solved worksheets for Class 12 Accountancy Chapter All Chapters to help students verify their answers instantly.

Yes, our Class 12 Accountancy test sheets are mobile-friendly PDFs and can be printed by teachers for classroom.

For Chapter All Chapters, regular practice with our worksheets will improve question-handling speed and help students understand all technical terms and diagrams.