Read and download free pdf of CBSE Class 12 Accountancy Accounting For Partnership Firms Worksheet Set B. Students and teachers of Class 12 Accountancy can get free printable Worksheets for Class 12 Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts in PDF format prepared as per the latest syllabus and examination pattern in your schools. Class 12 students should practice questions and answers given here for Accountancy in Class 12 which will help them to improve your knowledge of all important chapters and its topics. Students should also download free pdf of Class 12 Accountancy Worksheets prepared by teachers as per the latest Accountancy books and syllabus issued this academic year and solve important problems with solutions on daily basis to get more score in school exams and tests

Worksheet for Class 12 Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts

Class 12 Accountancy students should download to the following Part 1 Chapter 2 Accounting for Partnership Basic Concepts Class 12 worksheet in PDF. This test paper with questions and answers for Class 12 will be very useful for exams and help you to score good marks

Class 12 Accountancy Worksheet for Part 1 Chapter 2 Accounting for Partnership Basic Concepts

MCQ Questions for NCERT Class 12 Accountancy Accounting For Partnership Firms

Question. Seeta and Geeta are partners sharing profits and losses in the ratio 4 : 1. Meeta was manager who received the salary of ₹4,000 p.m. in addition to a commission of 5% on net profits after charging such commission. Profit for the year is ₹6,78,000 before charging salary. Find the total remuneration of Meeta.

(a) ₹78,000

(b) ₹88,000

(c) ₹87,000

(d) ₹76,000

Answer: A

Question. If the Partners’ Capital Accounts are fixed ‘salary payable to partner’ will be recorded :

(a) On the debit side of Partners’ Current Account

(b) On the debit side of Partners’ Capital Account

(c) On the credit side of Partners’ Current Account

(d) None of the above

Answer: C

Question. For the firm interest on drawings is

(a) Capital Payment

(b) Expenses

(c) Capital Receipt

(d) Income

Answer: D

Question. Interest on Partner’s drawings will be debited to :

(a) Profit and Loss Account

(b) Profit and Loss Appropriation Account

(c) Partner’s Current Account

(d) Interest Account

Answer: C

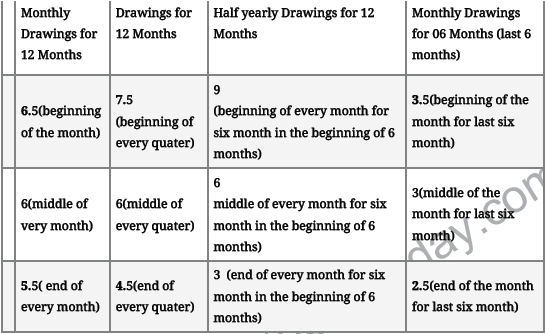

Question. If a fixed amount is withdrawn by a partner in each quarter, interest on the total amount is charged for ……………….. months

(a) 3

(b) 6

(c) 4.5

(d) 7.5

Answer: B

Question. A and B contribute ₹1,00,000 and RS₹60,000 respectively in a partnership firm by way of capital on which they agree to allow interest @ 8% p.a. Their profit or loss sharing ratio is 3 : 2. The profit at the end of the year was ₹2,800 before allowing interest on capital. If there is a clear agreement that interest on capital will be paid even in case of loss, then S’s share will be:

(a) Profit ₹6,000

(b) Profit ₹4,000

(c) Loss ₹6,000

(d) Loss ₹4,000

Answer: D

Question. Which of the following statement is true

(a) Fixed capital account will always have a credit balance

(b) Current account can have a positive or a negative balance

(c) Fluctuating capital account can have a positive or a negative balance

(d) All of the above

Answer: D

Question. When partners’ capital accounts are fixed, which one of the following items will be written in the partner’s capital account :

(a) Partner’s Drawings

(b) Additional capital introduced by the partner in the firm

(c) Loan taken by partner from the firm

(d) Loan Advanced by partner to the firm

Answer: B

Question. A, B and C are partners. A’s capital is ₹3,00,000 and B’s capital is ₹1,00,000. C has not invested any amount as capital but he alone manages the whole business. C wants RS30,000 p.a. as salary. Firm earned a profit of ₹1,50,000. How much will be each partner’s share of profit:

(a) A ₹60,000; B ₹60,000; C ₹Nil

(b) A ₹90,000; B ₹30,000; C ₹Nil

(c) A ₹40,000; B ₹40,000 and C ₹40,000

(d) A ₹50,000; B ₹50,000 and C ₹50,000.

Answer: D

Question. It the Partner’s Capital Accounts are fixed, interest on capital will be recorded:

(a) On the credit side of Current Account

(b) On the credit side of Capital Account

(c) On the debit side of Current Account

(d) On the debit side of Capital Account

Answer: A

Question. If a fixed amount is withdrawn by a partner in the middle of every month, interest on the total amount is charged for …………… months

(a) 6

(b) 6 1/2

(c) 5 1/2

(d) 12

Answer: A

Question. Sushil is a partner in a firm. He withdrew ₹4,000 per month in the middle of every month during the year ended 31st March, 2019. If interest on drawings is charged @ 8% p.a. the interest charged will be :

(a) ₹2,080

(b) ₹1,760

(c) ₹3,840

(d) ₹1,920

Answer: D

Question. On 1st April 2018, 2fs Capital was ₹2,00,000. On 1st October 2018, he introduces additional capital of ₹1,00,000. Interest on capital @ 6% p.a. on 31st March, 2019 will be :

(a) ₹9,000

(b) ₹18,000

(c) ₹10,500

(d) ₹15,000

Answer: D

Question. X and Y are partners in the ratio of 3 : 2. Their capitals are RS2,00,000 and ₹1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm earned a profit of RS60,000 for the year ended 31st March 2019. Interest on Capital will be :

(a) X ₹16,000; Y ₹8,000

(b) V ₹8.000; Y ₹4,000

(c) X ₹14,400; Y ₹9,600

(d) No Interest will be allowed

Answer: A

Question. X and Y are partners in the ratio of 3:2. Their capitals are ₹2,00,000 and ₹1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm earned a profit of ₹15,000 for the year ended 31st March 2019. As per partnership agreement, interest on capital is treated a charge on profits. Interest on Capital will be :

(a) X ₹16,000; Y ₹8,000

(b) X ₹9,000; Y ₹6,000

(c) X ₹10,000; Y ₹5,000

(d) No Interest will be allowed

Answer: A

Question. Bipasa is a partner in a firm. She withdrew ₹6,000 at the end of each quarter during the year ended 31st March, 2019. Interest on her drawings @ 10% p.a. will be :

(a) ₹900

(b) ₹600

(c) ₹1,500

(d) ₹1,200

Answer: A

Question. Partners are suppose to pay interest on drawing only when by the

(a) Provided, Agreement

(b) Permitted, Investors

(c) Agreed, Partners

(d) ‘A’ & ‘C’ above

Answer: D

Question. Where will you record interest on drawings :

(a) Debit Side of Profit & Loss Appropriation Account

(b) Credit Side of Profit & Loss Appropriation Account

(c) Credit Side of Profit & Loss Account

(d) Debit Side of Capital/Current Account only

Answer: B

Question. Vikas is a partner in a firm. His drawings during the year ended 31st March, 2019 were RS72,000. If interest on drawings is charged @ 9% p.a. the interest charged will be :

(a) ₹324

(b) ₹6,480

(c) ₹3,240

(d) ₹648

Answer: C

Question. X and Y are partners in the ratio of 3:2. Their capitals are RS2,00,000 and ₹1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm incurred a loss of ₹60,000 for the year ended 31st March 2019. Interest on Capital will be :

(a) X ₹16,000; Y ₹8,000

(b) A ₹8,000; Y ₹4,000

(c) X ₹14,400; Y ₹9,600

(d) No Interest will be allowed

Answer: D

Question. If a fixed amount is withdrawn by a partner on the last day of every month, interest on the total amount is charged for …………… months :

(a) 12

(b) 6 1/2

(c) 5 1/2

(d) 6

Answer: C

Question. X and Y are partners in the ratio of 3:2. Their capitals are ₹2,00,000 and ₹1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm earned a profit of ₹15,000 for the year ended 31st March 2019. Interest on Capital will be :

(a) X ₹16,000; Y ₹8,000

(b) X ₹9,000; Y ₹6,000

(c) X ₹10,000; Y ₹5,000

(d) No Interest will be allowed

Answer: C

Question. In a partnership firm, a partner withdrew ₹5,000 per month on the first day of every month during the year for personal expenses. If interest on drawings is charged @ 6% p.a. the interest charged will be :

(a) ₹3,600

(b) ₹1,950

(c) ₹1,800

(d) ₹1,650

Answer: B

Question. If fixed amount is withdrawn by a partner on the first day of each quarter, interest on the total amount is charged for …………….. months

(a) 4.5

(b) 6

(c) 7.5

(d) 3

Answer: C

Question. If a fixed amount is withdrawn by a partner on the last day of each quarter, interest on the total amount is charged for ……………… months

(a) 6

(b) 4.5

(c) 7.5

(d) 3

Answer: B

According to Section -4 of the Indian Partnership Act, 1932:

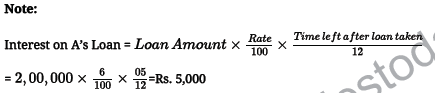

Q.1. A and B are partners. A gave a loan of ₹ 8,000 to the firm on 1.4.12. The Partnership Deed is silent upon interest on loan. How much interest on loan will be provided to him?

Accounting year is calendar year

(a) ₹ 480

(b) ₹360

(c) ₹ 200

(d) none of the above

Answer : B

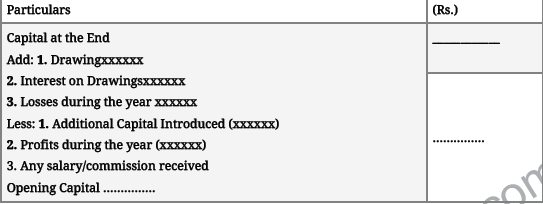

Q.2. On 31.3.12, after the close of books of accounts, the capital a/c of Ram, Shyam & Mohan showed a balance of ₹24,000, ₹ 18,000 and ₹ 12,000 respectively. The profits for the year ended 31.3.12 amounted to Rs. 36,000 and the partner’s drawings had been Ram-Rs. 3,600, Shyam-₹ 4,500 and Mohan-₹ 2,700. The Profit Sharing Ratio was 3:2:1. How much will be the opening capital?

(a) Ram-₹15,600, Shyam-₹10,500, Mohan-₹ 8,700

(b) Ram-₹15,650, Shyam-₹ 10,550, Mohan-₹ 2,750

(c) Ram-₹15,600, Shyam-₹10,500, Mohan-₹ 2,800

(d) None of the above

Answer : A

Q.3. If Partnership Deed is silent, how much salary will be provided to partners?

(a) Proportionate to capital contribution

(b) Proportionate to time spent

(c) Nil

(d) none of the above

Answer : C

Q.4. A, B and C are partners in a firm. They decided to share profits upto ₹ 10,000 in the ratio of 50%, 30% and 20% respectively. Above this amount, profits are shared equally. If the profits of the firm for the year was ₹25,600. Distribute the profits.

(a) A-₹10,000, B-₹8,500, C-₹7,500

(b) A-₹10,200, B-₹8,100, C-₹7,300

(c) A-₹10,200, B-₹8,200, C-₹7,200

(d) A-₹10,200, B-₹8,200, C-₹.7,500

Answer : C

Q.5. A, B and C are partners sharing profits and losses in the ratio of 2:1:2. Their capitals were ₹3,00,000, ₹1,00,000 and ₹2,00,000 respectively. Interest on capital for the year 2011 was credited to them @ 9% p.a. instead of 10% p.a. The profits for the year before charging interest was ₹ 2,50,000. Which of the following journal entry is correct?

(a) A’s Capital A/c Dr. 200

C’s Capital A/c Dr. 400

To B’s Capital A/c 600

(b) B’s Capital A/c Dr. 200

C’s Capital A/c Dr. 400

To A’s Capital A/c 600

(c) B’s Capital A/c Dr. 200

A’s Capital A/c Dr. 400

To C’s Capital A/c 600

(d) None of the above

Answer : B

Q.6. X and Y are partners. X drew regularly ₹400 at the beginning of every month for six months ending 30.6.12. Calculate interest on drawings @ 5% p.a.?

(a) ₹ 40

(b) ₹ 38

(c) ₹ 29

(d) ₹35

Answer : D

| CBSE Class 12 Accountancy Accounting for Not for Profit Organisation Worksheet |

| CBSE Class 12 Accountancy Accounting For Partnership Firms Worksheet Set A |

| CBSE Class 12 Accountancy Accounting For Partnership Firms Worksheet Set B |

| CBSE Class 12 Accountancy Admission Of Partner Worksheet Set A |

| CBSE Class 12 Accountancy Admission Of Partner Worksheet Set B |

| CBSE Class 12 Accountancy Retirement And Death Of Partner Worksheet Set A |

| CBSE Class 12 Accountancy Retirement And Death Of Partner Worksheet Set B |

| CBSE Class 12 Accountancy Retirement And Death Of Partner Worksheet Set C |

| CBSE Class 12 Accountancy Retirement And Death Of Partner Worksheet Set D |

| CBSE Class 12 Accountancy Dissolution Of Partnership Firm Worksheet Set A |

| CBSE Class 12 Accountancy Dissolution Of Partnership Firm Worksheet Set B |

| CBSE Class 12 Accountancy Share Capital Worksheet Set A |

| CBSE Class 12 Accountancy Share Capital Worksheet Set B |

| CBSE Class 12 Accountancy Debentures Worksheet |

| CBSE Class 12 Accountancy Financial Statements Of Company Worksheet |

| CBSE Class 12 Accountancy Financial Analysis And Tools For Financial Analysis Worksheet |

| CBSE Class 12 Accountancy Ratio Analysis Worksheet |

| CBSE Class 12 Accountancy Cash Flow Statement Worksheet Set A |

| CBSE Class 12 Accountancy Cash Flow Statement Worksheet Set B |

Worksheet for CBSE Accountancy Class 12 Part 1 Chapter 2 Accounting for Partnership Basic Concepts

We hope students liked the above worksheet for Part 1 Chapter 2 Accounting for Partnership Basic Concepts designed as per the latest syllabus for Class 12 Accountancy released by CBSE. Students of Class 12 should download in Pdf format and practice the questions and solutions given in the above worksheet for Class 12 Accountancy on a daily basis. All the latest worksheets with answers have been developed for Accountancy by referring to the most important and regularly asked topics that the students should learn and practice to get better scores in their class tests and examinations. Expert teachers of studiestoday have referred to the NCERT book for Class 12 Accountancy to develop the Accountancy Class 12 worksheet. After solving the questions given in the worksheet which have been developed as per the latest course books also refer to the NCERT solutions for Class 12 Accountancy designed by our teachers. We have also provided a lot of MCQ questions for Class 12 Accountancy in the worksheet so that you can solve questions relating to all topics given in each chapter.

You can download the CBSE Printable worksheets for Class 12 Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts for latest session from StudiesToday.com

There is no charge for the Printable worksheets for Class 12 CBSE Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts you can download everything free

Yes, studiestoday.com provides all latest NCERT Part 1 Chapter 2 Accounting for Partnership Basic Concepts Class 12 Accountancy test sheets with answers based on the latest books for the current academic session

CBSE Class 12 Accountancy Part 1 Chapter 2 Accounting for Partnership Basic Concepts worksheets cover all topics as per the latest syllabus for current academic year.

Regular practice with Class 12 Accountancy worksheets can help you understand all concepts better, you can identify weak areas, and improve your speed and accuracy.