Read and download the CBSE Class 12 Accountancy Admission Of Partner Worksheet Set 02 in PDF format. We have provided exhaustive and printable Class 12 Accountancy worksheets for Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner, designed by expert teachers. These resources align with the 2026-27 syllabus and examination patterns issued by NCERT, CBSE, and KVS, helping students master all important chapter topics.

Chapter-wise Worksheet for Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner

Students of Class 12 should use this Accountancy practice paper to check their understanding of Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner as it includes essential problems and detailed solutions. Regular self-testing with these will help you achieve higher marks in your school tests and final examinations.

Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Worksheet with Answers

MCQ Questions for NCERT Class 12 Accountancy Admission Of Partner

Question. The profit sharing ratio of Seeema and Ghosh was 5:3. They admitted Munmun as a new partner and the new profit sharing ratio of Seema, Gosh and Munmun was 4:3:3. The sacrificing ratio Seem and Gosh will be:

(a) 5:3

(b) 4:3

(c) 1:1

(d) 3:1

Answer: D

Question. As per ---------, only purchased goodwill can be shown in the Balance Sheet.

(a) AS 37

(b) AS 26

(c) Section 37

(d) AS 37

Answer: B

Question. On the admission of a new partner increase in the value of assets is debited to :

(a) Profit and loss adjustment account

(b) Assets account

(c) Old partners’ capital account

(d) None of the above

Answer: B

Question. At the time of admission of a partner, undistributed profits appearing in the balance sheet of the old firm is transferred to the capital accounts of :

(a) Old partners in old profit sharing ratio

(b) Old partners in new profit sharing ratio

(c) All the partner in the new profit sharing ratio

(d) None of the above

Answer: B

Question. The firm of P, Q and R with profit sharing ratio of 6:3:1, had the balance in General Reserve Account amounting Rs. 1,80,000. S joined as a new partner and the new profit sharing ratio was decided to be 3:3:3:1. Partners decide to keep the General Reserve unchanged in the books of accounts. The effect will be:

(a) P will be credited by Rs. 54,000

(b) P will be debited by Rs. 54,000

(c) P will be credited by Rs. 36.000

(d) P will be credited by Rs. 36,000

Answer: A

Question. Ramesh and Suresh are partners sharing profits in the ratio of 2:1 respectively. Ramesh’s capital is Rs.102000 and Suresh capital is Rs.73000. they admit Mahesh and agreed to give him 1/5th share in future profit. Mahesh brings Rs.14000 as his share of goodwill. He agrees to contribute capital in the new profits sharing ratio. How much capital will be brought by Mahesh?

(a) 43750

(b) 45000

(c) 47250

(d) 48000

Answer: C

Question. A and B are partners in a firm having capital of Rs.54000 and Rs.36000 respectively. They admitted C for 1/3rd share in the profits. C brought proportionate amount of capital. The capital brought in by C would be

(a) 90000

(b) 45000

(c) 5400

(d) 36000

Answer: B

Question. A and B are partners sharing profits in the ratio of 7:3. A surrenders 1/7th of his share and B surrenders 1/3rd of his share in favour C the new partner. The sacrificing ratio will be:

(a) 3:7

(b) 1:1

(c) 7:3

(d) 3:2

Answer: B

Question. Which of the following is not true with respect to Admission of a partner?

(a) A new partner can be admitted if it is agreed in the partnership deed.

(b) If all the partners agree, a new partner can be admitted.

(c) A new partner has to bring relatively higher capital as compared to the existing partners

(d) A new partner gets right in the assets of the firm

Answer: C

Question. A and B are partners sharing profit and losses in ratio of 5:3. C is admitted for 1/4th share. On the date of reconstitution, the debtors stood at Rs 40,000, bill receivable stood at Rs. 10,000 and the provision for doubtful debts appeared at Rs. 4000. A bill receivable, of Rs 10,000 which was discounted from the bank, earlier has been reported to be dishonored. The firm has sold, the debtor so arising to a debt collection agency at a loss of 40%. If bad debts now have arisen for Rs 6,000 and firm decides to maintain provisions at same rate as before then amount of Provision to be debited to Revaluation Account would be:

(a) Rs 4,400

(b) Rs 4,000

(c) Rs 3,400

(d) None of the above

Answer: C

Question. When new partner does not bring his share of goodwill in cash, the amount is debited to:

(a) Current account of the new partner

(b) Premium account

(c) Capital account of the old partners

(d) Cash account

Answer: C

Question. Sacrificing ratio is calculated because:

(a) Profit shown by Revaluation Account can be credited to sacrificing partners

(b) Goodwill brought in by the incoming partner can be credited to the new partner

(c) Goodwill brought in by the incoming partner can be credited to the sacrificing partners

(d) Both a and c

Answer: C

Question. Sacrificing ratio is used to distribute ------------------ in case of admission of a partner.

(a) Goodwill

(b) Revaluation Profit or Loss

(c) Profit and Loss Account (Credit Balance)

(d) Both b and c

Answer: A

Question. The need of revaluation of assets and liabilities on admission:

(a) Assets and liabilities should appear at revised value

(b) Any profit and loss on account of change in values belong to old partners

(c) All unrecorded assets and liabilities get recorded

(d) None of the above

Answer: B

Question. A and B are partners sharing profits in the ratio of 3:1. C is admitted to partnership firm for 1/4th share. The sacrificing ratio of A and B will be:

(a) Equal

(b) 2:1

(c) 3:2

(d) 3:1

Answer: D

Question. Which statement is true with respect to AS-26?

(a) Purchased goodwill can be shown in the Balance Sheet

(b) Revalued goodwill can be shown in the Balance Sheet

(c) Both purchased goodwill and revalued can be shown in the Balance Sheet

(d) None of the above

Answer: A

Question. The share of new partner and the sacrificing ratio of old partners is decided by:

(a) the new partner only

(b) the old partners only

(c) the old partners and the new partner

(d) the accountant of the firm

Answer: C

Question. A and B are partners in a firm sharing profits in 4:1. They admit Pal as a new partner for ¼ share in the profits, which he acquired wholly from A. New profit sharing ratio of the partners is:

(a) 4:1:1

(b) Equally

(c) 11:4:5

(d) none of the above

Answer: C

Question. On admission of a partner, which of the following items of the balance sheet is transferred to the credit of capital accounts of old partners in the old profit sharing ratio, if capital accounts are maintained on fluctuating capital accounts method:

(a) Deferred revenue expenditure

(b) Profit and loss account (debit balance)

(c) Profit and loss account (credit balance)

(d) Balance in drawing account of partners

Answer: C

Question. At the time of Admission of a new partner, the Goodwill already appears in the Balance Sheet of the firm is treated as -

(a) Debited in all partners’ Capital Accounts in new ratio .

(b) Debited in old partners ‘ Capital Accounts in old ratio .

(c) Credited in old partners’ Capital Accounts in old ratio .

(d) None of the Above .

Answer : B

Question. X & Y are partners in a firm. Z is admitted for 1/5th Share . If there in no Partnership Deed,the ratio in which X & Y sacrifice their share of profit in favour of new partner is _

(a) In the Ratio of capital

(b) Equally

(c) Either a or b

(d) None of the Above

Answer : B

Question. Hema & Seema were Partner in a firm sharing profits in the ratio of 3:1.Their Capitals Were Rs.4,00,000 and Rs.1,00,000/- respectively.They Admitted Dimple on 1st April 2021 for 1/5th share in future profits.Dimple Brought Rs.2,00,000/-as her capital.The Dimple’s share of goodwill is

(a) Rs.50,000/-

(b) Rs.60,000/-

(c) Rs.1,00,000/-

(d) None of the Above

Answer : B

Question. On the Admission of New partner, Increase in a Liability of the firm will be shown in _

(a) Credit Side of profit & loss appropriation A/c

(b) Debit Side of Profit & Loss Appropriation A/c

(c) Credit side of revaluation A/c

(d) Debit side of Revaluation A/c

Answer : D

Question. Amit and Sumit are partners in a firm sharing profits and losses equally .A new partner Lalit is admitted for 20 % share and Goodwill of the firm is valued at Rs 60,000 . What is the entry for Goodwill ,if Lalit does not bring his share of goodwill in cash .

(a) Premium for Goodwill A/c …..Dr. 15,000 To Amit’s Capital A/c 7,500 To Sumit’s Capital A/c 7,500

(b) Lalit’s Current A/c …..Dr. 15,000 To Amit ‘s Capital A/c 7,500 To Sumit’s Capital A/c 7,500

(c) Premium for Goodwill A/c …..Dr. 12,,000 To Amit’s Capital Alc 6,000 To Sumit’s Capital A/c 6,000

(d) Lalit’s Current A/c …..Dr. 12,000 To Amit ‘s Capital 6,000 To Sumit‘s Capital 6,000

Answer : D

Question. Arti & Amit Were Partners in a firm Sharing Profits & losses in the ratio of 2:1.Vipul was admitted as a new partner for 1/5th Share in profits.Vipul acquired 2/3rd of his share from Arti.The Share, which Vipul Acquired from Amit is _

(a) 2/15

(b) 1/15

(c) 1/9

(d) None of the above

Answers : B

Question. Match the following

(a) 1-iv , 2-ii , 3-i , 4-iii

(b) 1-ii , 2-iv , 3-i ,4-iii

(c) 1-ii , 2-i , 3-iii , 4-iv

(d) 1-ii , 2-iv , 3-iv , 4-iii

Answer : A

Question. Sun , Moon ,Star are partners in a partnership firm ,if Sky is admitted as a new partner -

(a) Old firm is dissolved .

(b) Old partnership and Old firm is dissolved .

(c) Old Partnership is reconstituted .

(d) None of these .

Answer : C

Question. In Case of Admission of a partner ,the entry for unrecorded Investment will be :-

(a) Debit Partners Capital A/c & Credit Investment A/c

(b) Debit Revaluation A/c & Credit Investment A/c

(c ) Debit Investment A/c & Credit Revaluation A/c

(d) None of the Above

Answer : C

Question. A, B ,C and D are Partners in a firm . A and B Share 2/3rd of profits Equally .C & D Share remaining Profits in the Ratio of 3:2.Find the profit sharing Ratio of A ,B ,C, and D.

(a) 7:7:6:4

(b)5:5:3:2

(c)3:3:3:2

(d) 3:3:6:4

Answer : B

Question. A and B are partners in a firm sharing profits and losses in the ratio of 3 : 2. They admitted C as a new partner . A sacrificed 1 / 5 th of his share and B sacrificed 1 / 5 th from his share in favour of C. C ‘s share in the profits of the firm will be -

(a) 5 / 25

(b) 8 / 25

(c) 6 / 25

(d) 2 / 5

Answer : B

Question. In Case of Fixed Capitals,Undistributed Losses are transferred to –

(a) Debit of Partners Capital A/c

(b) Credit of Partners Capital A/c

(c) Debit of Partners Current A/c

(d) Credit of Partners Current A/c

Answer : C

Assertion Reasoning Questions :

Question. Assertion : A minor can become a partner in a partnership firm .

Reason : The Indian Partnership Act ,1932 provides that minor can be admitted for the benefits in the partnership firm .

(a) Assertion and Reason both are correct and reason is the correct explanation of assertion .

(b) Assertion and Reason both are correct but reason is not the correct explanation of assertion .

(c) Assertion is true but reason is false .

(d) Assertion is false but Reason is true .

Answer : D

Question. Assertion : The ratio in which old partners sacrifice their share in favour of new partner at the time of his/ her admission is known as Sacrificing Ratio . Reason : The Sacrificing ratio is calculated by taking out difference between new share and old share .

(a) Assertion and Reason both are correct and reason is the correct explanation of assertion .

(b) Assertion and Reason both are correct but reason is not the correct explanation of assertion .

(c) Assertion is true but reason is false .

(d) Assertion is false but Reason is true .

Answer : C

Question. Assertion : In case of Admission of a partner , change in profit sharing ratio etc.The Valued Goodwill is not shown in the books of account . Reason : As per AS -26 , Goodwill should be recognized in the books of account only when consideration in money or money’s worth is paid for it .

(a) Assertion and Reason both are correct and reason is the correct explanation of assertion .

(b) Assertion and Reason both are correct but reason is not the correct explanation of assertion .

(c) Assertion is true but reason is false .

(d) Assertion is false but Reason is true .

Answer : A

Question. Assertion : In case of Admission of Partner , Change in Profit sharing ratio etc. old agreement is cancelled and new agreement is prepared . Reason : Profit and Loss Adjustment A/c (Revaluation A/c ) is prepared to Revalue the assets and Reassessment of liabilities .

(a) Assertion and Reason both are correct and reason is the correct explanation of assertion .

(b) Assertion and Reason both are correct but reason is not the correct explanation of assertion .

(c) Assertion is true but reason is false .

(d) Assertion is false but Reason is true .

Answer : B

Question. Himanshu and Naman share profits & losses equally. Their capitals were Rs.1,20,000 and Rs. 80,000 respectively. There was also a balance of Rs. 60,000 in General reserve and revaluation gain amounted to Rs. 15,000. They admit friend Ashish with 1/5 share. Ashish brings Rs.90,000 as capital. Calculate the amount of goodwill of the firm. B

(a) Rs.1,00,000

(b) Rs. 85,000

(c) Rs.20,000

(d) None of the above

Answer: B

PRACTICAL PROBLEMS:

1. A, B and C were partners in a firm sharing profits in 3:2:1. They admitted D for 10% profits. Calculate the new profit sharing ratio. ( Ans: 9:6:3:2).

2. X and Y are partners sharing profits in 5:3 ratio admitted Z for 1/10th share which he acquired equally for X and Y. Calculate new profit sharing ratio.(Ans. 23:13:4).

3. Radha and Rukmani are partners in a firm sharing profits in 3:2 ratio. They admitted Gopi as a new partner. Radha surrendered 1/3rd of her share in favour of Gopi and Rukmani surrendered 1/4th of her share in favour of Gopi. Calculate new profit sharing ratio.(Ans. 4:3:3)

4. A and B are partners in a firm sharing profits in the ratio of 3:2. They admit C into partnership for 1/5th share of profits in the firm. The goodwill of the firm is valued at Rs. 1,00,000. He is unable to bring in his share of goodwill. What will be the journal entries?

Solution: Goodwill of the firm = Rs 1,00,000

C’s share of goodwill = 1,00,000 X 1/5 = Rs. 20,000

Change in profit sharing ratio

Question. On the admission of a new partner, increase in the value of assets is debited to

(a) Revaluation A/c

(b) Profit & Loss Account

(c) Assets Account

(d) None of the options

Answer: C

Question. X and Y shares profits in the ratio of 2:3, how they decided to share profits equally in the future, Which partner will sacrifice and in which ratio

(a) Y Sacrifice 1/10

(b) X Sacrifice 1/10

(c) Both

(d) None of the options

Answer: A

Question. Change in partnership agreement

(a) Results in end of partnership business

(b) Changes in the relationship among the partner

(c) Dissolved the partnership firm

(d) None of the options

Answer: B

Question. If the incoming partner is to bring in premium for goodwill in cash and also a balance exists in the goodwill account, then this goodwill account is written of among the old partners in

(a) The old profit sharing ratio

(b) The new profit sharing ratio

(c) The sacrificing ratio

(d) None of the options

Answer: A

Question. Revaluation account or Profit & loss adjustment account is

(a) Real Account

(b) Personal Account

(c) Nominal Account

(d) None of the options

Answer: C

Question. The ratio in which the continuing partners acquire the outgoing partners share is called

(a) Gaining Ratio

(b) New Profit sharing ratio

(c) Old Profit sharing ratio

(d) None of the options

Answer: A

Question. In the event of death of a partner, the amount of general reserve is transferred to partners capital accounts in

(a) The new profit sharing ratio

(b) the capital ratio

(c) None of the options

(d) The old profit sharing ratio

Answer: D

Question. The partners whose share Increase as a result of change in profit sharing ratio are known as

(a) Sacrificing Partners

(b) Sleeping Partners

(c) Gaining Partners

(d) None of the options

Answer: C

Question. Z is admitted to a firm for 1/4 share in the profits for which he brings in Rs. 10000towards premium for goodwill, it will be taken by the old partners in

(a) The Sacrificing ratio

(b) The old Profit sharing ratio

(c) The new profit sharing ratio

(d) None of the options

Answer: A

Question. X and Y are partners sharing profits in the ratio of 2:1, they admit Z into the partnership for 1/4th share in profits for which brings in Rs. 20000 as his share of capital. Hence the adjusted capital of X and Y will be

(a) 32000 and 16000 respectively

(b) 40000 and 20000 Rs. Respectively

(c) 60000 and 30000 Rs. Respectively

(d) None of the options

Answer: B

Question. When goodwill is withdrawn by old partners ________________ a/c is credited.

(a) cash/bank

(b) capital

(c) revaluation

(d) Profit and Loss Adjustment

Answer: A

Question. Jay, Vijay and Ajay are three partners sharing profits in 3:2:1. They decided to admit Sanjay and give him 1/7th share, new profit sharing ratio of partners will be _____.

(a) equal

(b) 3:2:1:2

(c) 3:2:1:1

(d) 2:3:1:2

Answer: C

Question. If any asset is taken over by partner from the firm _________________ account will be debited.

(a) revaluation

(b) asset

(c) Profit and Loss Adjustment

(d) capital

Answer: D

Question. Excess of proportionate capital over actual capital represents.......................

(a) Equal capital

(b) Surplus Capital

(c) Deficit Capital

(d) Gain

Answer: C

Question. A firm is reconstituted , whenever there is a

(a) All of the options

(b) Retirement of Existing Partner

(c) Death of a partner

(d) Admission of a new partner

Answer: A

Question. The _________ ratio is useful for making adjustment for goodwill among the old partners.

(a) new

(b) sacrifice

(c) old

(d) Profit and Loss Adjustment

Answer: B

Question. Decrease in the value of Liabilities on reconstitution of the partnership firm results into

(a) Gain to the Existing Partner

(b) Loss to the Existing Partner

(c) Neither Gain of loss to Existing partner

(d) None of the options

Answer: A

Question. In case of admission of a partner, the profit or loss on revaluation of assets and liabilities is shared by _________partners.

(a) all

(b) old

(c) new

(d) none of these

Answer: B

Question. Profit & loss adjustment account, which

(a) Both

(b) Increase value of the assets

(c) Decrease Value of Liabilities

(d) None of the options

Answer: A

Question. Account is debited when unrecorded liability is brought into business.

(a) liability

(b) revaluation

(c) capital

(d) current

Answer: B

(i) it is an intangible asset having a definite value.

Answer: Rs. 45,000

Question. State the amount of goodwill, if goodwill is to be valued on the basis of 2 years’ purchase of last year’s profit. Profit of the last year was Rs.20, 000.

Answer: Rs. 40,000

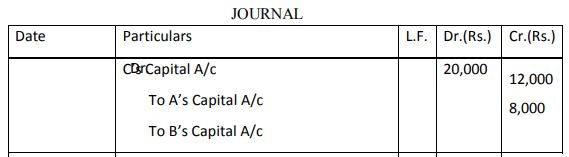

Question. P,Q and R are partners in a firm sharing profits in the ratio of 2:2:1 on 1.4.2007 the partners decided to share future profits in the ratio of 3:2:1 on that day balance sheet of the firm shows General Reserve of Rs. 50,000. Pass entry for distribution of reserve.

Answer: General Reserve A/c Dr. 50,000

To P’s Capital A/c 20,000

To Q’s Capital A/c 20,000

To R’s Capital A/c 10,000

(Being Reserve distributed)

THREE AND FOUR MARKS QUESTIONS.

Question. P, Q and R sharing profits and losses in the ratio of 3:2:1, decided to share future and losses in the ratio of 4:3:2 with effect from 1st April 2014. Following an extract of their balance sheet as at 31st March, 2014.

| Liabilities | Amount Rs. | Assets | Amount Rs. |

| Workmen compensation fund | 60000 |

Show the accounting treatment under the following cases.

i. If there is no other information.

ii. If a claim on account of workmen’s compensation is estimated at Rs. 24000.

iii. If a claim on account of workmen’s compensation is estimated at Rs.96000.

Answer: i. workmen compensation fund distributed in old ratio between all three partner.

ii. Rs. 36000 workmen compensation fund distributed in old ration between all three partner.

iii. 36,000 debited to revaluation account.

Question. kartik and Aroha are partners in a firm sharing profits in the ratio of 2:3. The balance sheet of the firm as on 31st March 2016 is given blow.Balance sheet as at 31st March 2016

| Liabilities | Amount | Assets | Amount |

| Creditors | 6200 | Bills receivable | 3600 |

| Bills payable | 1800 | Stock | 16000 |

| Capital A/cs | Machinery | 18400 | |

| Kartik | 16000 | Land and Building | 10000 |

| Aroha | 24000 | ||

| 48000 | 48000 |

The partners decided to share profits in equal ratio with effect from 1st April 2016. The following adjustments were agreed upon.

1. Land and building was valued at 16000 and machinery at 16400 and were appear at revalued amount in the balance sheet.

2. The goodwill of the firm was valued at 800 but was not to appear in the books.

Pass necessary journal entries to give effect the above.

Answer:

| S.N. | PARTICULAR | D R . AMT. | C R . AMT |

| 1 | Land and building ac dr | 6000 | |

| To revaluation ac | 6000 | ||

| 2 | Revaluation ac dr | 2000 | |

| To machinery ac | 2000 | ||

| 3 | Revaluation ac dr | 4000 | |

| To kartik’s capital ac | 1600 | ||

| To Aroha’s capital ac | 2400 | ||

| 4 | Kartik’s capital ac dr | 80 | |

| To Aroha’s capital ac | 80 | ||

| Sacrifice ratio= old ratio-new ratio Kartik=(1/10)Aroha=1/10 |

Q. 1. When there is a change in profit sharing ratio among the existing partners, which one is true?

(a) The sacrificing partner has to compensate the gaining partner

(b) The gaining partner has to compensate the sacrificing partner.

(c) One sacrificing partner has to compensate the other sacrificing partner

(d) One gaining partner has to compensate the other gaining partner.

Answer: A

Q.2. A, B and C share profits in the ratio of 3:2:1.They decided to change the profit sharing ratio to 2:2:1. Out the following which one will indicate each partner’s gain or sacrifice due to change in PSR?

(a) A sacrifices 3/30, B gains 2/30 and C gains 1/30

(b) A sacrifices 3/20, B gains 1/20 and C gains 2/20

(c) A sacrifices 3/30, B sacrifices 2/30 and C gains 5/30

(d) None of the above

Answer: A

Q.3. A and B share profits in the ratio of 5:4. They admit C for a 1/10th share of profits which he acquires in equal proportions from both. Calculate new ratio.

(a) 91:70:18

(b) 90:71:18

(c) 91:17:20

(d) 91:71:18

Answer: D

Q.4. K, L and M are partners sharing profits and losses in the ratio of 3:2:1. They admit N for 1/6th share. M would retain his original share. Find out the new profit sharing ratio.

(a) 12:8:5:5

(b) 10:8:5:4

(c) 15:8:4:5

(d) 12:8:4:5

Answer: A

Q.5. A and B share profits in the ratio of 7:3. C was admitted as a partner. A surrendered 1/7th of his share and B 1/3rd of his share in favour of C. The new profit sharing ratio of A, B and C will be:

(a) 3:2:1

(b) 3:1:1

(c) 2:1:1

(d) 3:2:2

Answer: B

1. What is meant by reconstitution of firm?

2. State the occasions on which reconstitution of partnership firm can take place.

3. What is meant by change in profit sharing ratio?

4. Define

(i) sacrificing ratio

(ii) gaining ratio

5. Enumerate the various matters that need adjustments at the time of change in profit sharing ratio.

6. Differentiate between sacrificing ratio and gaining ratio.

7. x, y and z are sharing P & L in the ratio of 5:3:2. They decide to share future profits and losses in the ratio of 2:3:5 with effect from 1st April 2002. They decide to record the effect of the following accumulated profits, losses and reserves without affecting their book figures, by passing a single adjusting entry.

Rs

General reserve 24000

Profit & Loss a/c 6000

Advertisement suspense A/c (Dr) 12000

[Ans z Dr 5400 to x 5400]

8. x, y and z are partners sharing P & L in ratio of 5: 3; 2, decide to share future P & L in the ratio of 2: 3: 5 with effect from 1st April 2002. an extract of their Balance Sheet as on 31-3-2002 is as

follows:

Liabilities Rs Assets Rs

Investment fluctuation

Reserve 1500 Investment 20000

(at cost )

Show the accounting treatment in each of the following cases:

(a) If no other information is given.

(b) If market value of investment is Rs 20000.

(c) If market value of investment is Rs 19000.if market value of investment is Rs 18000.

(d) If market value of investment is Rs 20500.

| Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Printable Worksheet Set 3 |

| Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Printable Worksheet Set 2 |

| Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Printable Worksheet Set 1 |

CBSE Accountancy Class 12 Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Worksheet

Students can use the practice questions and answers provided above for Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner to prepare for their upcoming school tests. This resource is designed by expert teachers as per the latest 2026 syllabus released by CBSE for Class 12. We suggest that Class 12 students solve these questions daily for a strong foundation in Accountancy.

Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Solutions & NCERT Alignment

Our expert teachers have referred to the latest NCERT book for Class 12 Accountancy to create these exercises. After solving the questions you should compare your answers with our detailed solutions as they have been designed by expert teachers. You will understand the correct way to write answers for the CBSE exams. You can also see above MCQ questions for Accountancy to cover every important topic in the chapter.

Class 12 Exam Preparation Strategy

Regular practice of this Class 12 Accountancy study material helps you to be familiar with the most regularly asked exam topics. If you find any topic in Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner difficult then you can refer to our NCERT solutions for Class 12 Accountancy. All revision sheets and printable assignments on studiestoday.com are free and updated to help students get better scores in their school examinations.

FAQs

You can download the latest chapter-wise printable worksheets for Class 12 Accountancy Chapter Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner for free from StudiesToday.com. These have been made as per the latest CBSE curriculum for this academic year.

Yes, Class 12 Accountancy worksheets for Chapter Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner focus on activity-based learning and also competency-style questions. This helps students to apply theoretical knowledge to practical scenarios.

Yes, we have provided solved worksheets for Class 12 Accountancy Chapter Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner to help students verify their answers instantly.

Yes, our Class 12 Accountancy test sheets are mobile-friendly PDFs and can be printed by teachers for classroom.

For Chapter Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner, regular practice with our worksheets will improve question-handling speed and help students understand all technical terms and diagrams.