Read and download the CBSE Class 12 Accountancy Retirement And Death Of Partner Worksheet Set 03 in PDF format. We have provided exhaustive and printable Class 12 Accountancy worksheets for Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner, designed by expert teachers. These resources align with the 2026-27 syllabus and examination patterns issued by NCERT, CBSE, and KVS, helping students master all important chapter topics.

Chapter-wise Worksheet for Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner

Students of Class 12 should use this Accountancy practice paper to check their understanding of Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner as it includes essential problems and detailed solutions. Regular self-testing with these will help you achieve higher marks in your school tests and final examinations.

Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner Worksheet with Answers

Very Answer Type Questions

Short Answer Type Questions

Question : On the retirement of a partner, profit on revaluation of assets and liabilities should the credited to the Capital Accounts of :

(b) 2 : 1

(c) 1 : 1

(d) 2 : 3

(a) Real Account

(b) Nominal Account

(c) Personal Account

(d) None of the options

Answer: B

Question. A, B and C are partners sharing profits in the ratio of 5 : 2 : 1. If the new ratio on the retirement of A is 3 :2, what will be the gaining ratio?

(a) 11: 14

(b) 3 : 2

(c) 2 : 3

(d) 14 : 11

Answer: D

Question. On retirement of a partner, goodwill will be credited to the Capital Account of:

(a) Retiring Partner

(b) Remaining Partners

(c) All Partners

(d) None of the Above

Answer: A

Question. A, B and C are partners sharing profits and losses in the ratio of 3 : 2 :1. On 1.3.2016 C died. The average profits of the firm for last four years were ₹ 72,000 Books are closed on 31st December. C’s share of profit till the date of his death will be:

(a) ₹ 2,000

(b) ₹ 12,000

(c) ₹ 1,400

(d) ₹ 24,000

Answer: A

Question. Revaluation Account is prepared at the time of …………

(a) Admission of a partner

(b) Retirement of a partner

(c) Death of a partner

(d) All of the above

Answer: D

Question. P, Q and R are partners sharing profits in the ratio of 5 : 4 : 3. Q retires and P and R decide to share future profits equally. Gaining Ratio will be :

(a) 5 : 3

(b) 1 : 1

(c) 1 : 3

(d) 3 : 1

Answer: C

Question. A, B and C are partners sharing profits in the ratio of 3 : 2 : 1. They had a Joint Life Policy of ₹ 3,00,000. Surrender value of JLP in Balance Sheet is ₹ 90,000. C dies what is share of each partner in JLP ?

(a) ₹ 1,05,000 ; ₹ 70,000; ₹ 35,000

(b) ₹ 45,000 ; ₹ 30,000; ₹ 15,000

(c) ₹ 1,50,000 ; ₹ 1,00,000 ; ₹ 50,000

(d) ₹ 1,95,000 ; ₹ 1,30,000 ; ₹ 65,000

Answer: C

Question. On death of a partner, his excutor is paid the profits of the deceased partner for the relevant period. This payment is recorded in Profit & Loss A/c :

(a) Adjustment

(b) Appropriation

(c) Suspense

(d) Reserve

Answer: C

Question. On the retirement of a partner, full amount of goodwill may be credited to the capital accounts of:

(a) Retiring partners

(b) Remaining partners

(c) All partners

(d) None of these

Answer: C

Question. How unrecorded assets are treated at the time of retriement of a partner ?

(a) Credited to Revaluation Account

(b) Credited to Capital Account of Retiring Partner

(c) Debited to Revaluation Account

(d) Credited to Partner’s Capital Accounts

Answer: A

Question. On retirement of a partner, his capital account will be credited with

(a) His/her share of goodwill.

(b) His share in reserves and surplus.

(c) His share of profit in revaluation

(d) All of the above

Answer: D

Question. According to the partnership Act, (Sec. 37) the interest payable to the deceased partner on the amount left by him will be:

(a) 6% p.a.

(b) 10% p.a.

(c) The Bank rate.

(d) None of the above.

Answer: A

Question. A, B are C are sharing profits in the ratio of \(\frac{1}{2}: \frac{1}{3} \div \frac{1}{6}\) C retired. Gaining ratio will be :

(a) 2 : 1

(b) 2 : 3

(c) 3 : 2

(d) 1 : 2

Answer: C

Question. The ratio in which the continuing partners acquire the outgoing partners share is called

(a) New Profit sharing ratio

(b) Old Profit sharing ratio

(c) None of the options

(d) Gaining Ratio

Answer: D

Question. At the time of retirement of a partner, if goodwill appears in the balance sheet, it must be written off, the capital accounts of all partners are debited in

(a) The old profit sharing ratio

(b) The new profit sharing ratio

(c) The capital ratio

(d) None of the options

Answer: A

(b) 3 : 2

(c) 1 : 1

(d) 2 : 1

(b) 21 : 11

(c) 4 : 3

(d) 4 : 2

(b) 3 : 1

(c) 4 : 1

(d) 5 : 1

Question : A, B, C are partners sharing profits in the ratio of 5:3:2.B retires and his share is taken over by A and C in the ratio of 2:1. The new PSR will be

a) 13:17

b) 2:1

c) 7:3

d) 2:4

Answer : C

Question : A, B, C are partners sharing profits in the ratio of 4:3:2. A retires and his share was taken by B and C in the ratio of 5:3.If A gets ₹ 12000 as goodwill then B and C will be debited with

a) ₹6500 and₹ 5500

b) ₹7500 and ₹4500

c) ₹2000 and ₹10000

d) ₹4000 and ₹8000

Answer : B

Question : A,B,C are partners sharing profits in the ratio of 4:3:2.B retires and remaining partners share profits in the ratio 5:3. Calculate gaining ratio.

a) 2: 3

b) 13:11

c) 2: 4

d) 5:3

Answer : D

Question : On the retirement of a partner, the amount of profit on revaluation of assets and liabilities is credited to the capital accounts of :

a) Only the retired partner

b) All partners in old PSR

c) Remaining partners in new PSR

d) Remaining partners in old PSR

Answer : B

Question : When is gaining ratio calculated

a) Admission

b) death

c) retirement

d) death and retirement

Answer : D

Very Short Answer Type Questions

Short Answer Type Questions – I

Short Answer Type Questions – II

RETIREMENT AND DEATH OF A PARTNER

Q 1 Define Gaining Ratio.

Q 2 Why is revaluation account prepared at the time of retirement of a partner?

Q 3 Calculate gaining ratio in the following cases:

(i) A, B & C are partners sharing profits & Losses in the ratio of 5:4:3. C retires from the firm.

(ii) X, Y & Z are partners sharing profits & losses in the ratio of 1/2, 3/10, & 1/5. Y decides to retire from the firm and X & Z decide to share future P&L in the ratio of 3:2.

Q 4 P, Q & R are partners sharing P&L in the ratio of 4:3:1. Q retires selling his share of profits to P & R for Rs 8100, Rs 3600 paid by P & Rs 4500 by R. The profits for the year after Q’s retirement were Rs 10500. Calculate the new profit sharing ratio & pass the necessary journal entries.

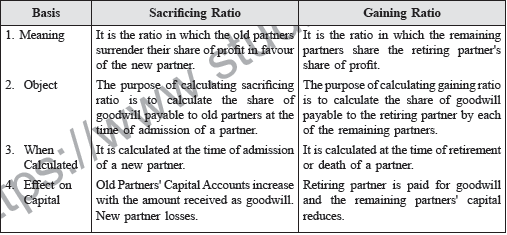

Q 5 Distinguish between gaining ratio & sacrificing ratio.

Q 6 A, B & C were partners in a firm sharing P&L in the ratio of 3:2:1. C retired and the new profit sharing ratio between A & B was 1:2. On C’s retirement goodwill was valued at Rs 30000. Pass the necessary journal entries without opening the goodwill account.

Q 7 When is “Memorandum Revaluation Account” prepared?

Q 8 A, B & C are partners sharing P & L in the ratio of 1/2, 1/3 &1/6 respectively. B retires

from the firm. A & C share future P & L equally. Their capitals after all necessary adjustment were A Rs 22400; B Rs 20200 & C Rs 11400. The cash balance as on that date was Rs 4000. Calculate the amount of cash to be brought in or to be withdrawn by the remaining partners in the following cases:

(i) The entire capital of the firm as newly constituted is fixed at Rs 40000.

(ii) The entire capital of the new firm will be readjusted so that the future capitals are in new profit sharing ratio.

(iii) B is to be paid through cash brought in by A & C in such a way as to make their capitals proportionate to their new profit sharing ratio.

(iv) B is to be paid through cash brought in by A & C in such a way as to make their capitals proportionate to their new profit sharing ratio. Minimum cash balance of Rs 3000 is to be maintained.

(v) Sufficient cash is to be brought in by A & C in such a way as to make their capitals proportionate to their new profit sharing ratio.

Q 9 What all items is the representative of the deceased partner entitled to?

Q 10 List the items that are debited to the deceased partners capital account.

Q 11 What are the two methods of calculation of profits of the deceased partner?

Explain with the help of examples.

Q 12 What is the difference between retirement of a partner & death of a partner?

Q 13 Why is outgoing partner entitled to a share of goodwill of the firm?

Q 14 Where is the payment recorded for the executors share of profit on the death of a partner when (i) remaining partners continue to share in old ratio (ii) the new profit sharing ratio is given .

Q 15 A ,B &C are partners in a firm sharing P & L in the ratio of 3:2:1. B died on 31/3/02.

The profits from 1/1/02 to 31/3/02 amounted to Rs 45000. Give the necessary Journal entries in the following cases:

(i) A & C agree to share future P&L in the ratio of 3:2

(ii) A & C continue to share P &L in the same ratio.

DISSOLUTION OF A PARTNERSHIP FIRM

Q 1 Distinguish between Realisation account & Revaluation account.

Q 2 Why is the balance of cash or bank not transferred to realisation account?

Q 3 Pass the necessary journal entries in the following cases:

(i) An unrecorded asset taken over by a partner

(ii) An unrecorded asset given to our creditor

(iii) Payment to creditors worth Rs 3000 if they accept stock of the same value

(iv) partner A takes over the liability of Mrs A’s loan of Rs 10000.

Q 4 Mention two internal liabilities whose payment does not require cash payment at the time of dissolution of the firm.

Q 5 Explain the provisions of sec 48 of partnership act.

Q 6 Distinguish between firms debts & private debts.

Q 7 Give the circumstances under which partnership firm can be dissolved.

Q 8 Are provisions against assets to be paid? Give reason.

Q 9 How do we deal with the following at the time of dissolution of the firm:

(i) Undistributed profits / losses

(ii) Fictitious assets

(iii) Partners loan account

(iv) If the question is silent regarding realisation of intangible asset

(v) If the question is silent regarding realisation of tangible asset

(vi) If the question is silent regarding payment of liability.

Q 10 Pass the journal entries in the following cases:

(i) Expenses of realisation Rs 7000 were to be borne by Ram, a partner. Ram used firms cash for paying these expenses.

(ii) Expenses of realisation Rs 8000 were to be borne by Ritu, a partner.

(iii) Realisation expenses paid by the firm amounted to Rs 3000. B had to bear these expenses.

(iv) An asset which had already been written off fetched Rs 8000.

(v) The firm had a JLP of Rs 50000 on which the premium paid was regarded as a business expense. The surrender value of the policy was Rs 15000. The Insurance co. Also paid a special bonus of Rs 6000.

(vi) Hari was to be given a commission of 3% on the net cash realised on dissolution & he was to meet all realisation expenses.The cash realised from sale of assets was Rs 76000& cash paid for liabilities amounted to Rs 16000. Actual expenses were Rs 7400.

(vii) L , a creditor to whom Rs 16000 were due to be paid took over machinery at Rs 20000. Balance was paid by him in cash.

(viii) Expenses of realisation were Rs 2000.

(ix) An unrecorded liability 0f Rs 5500 settled at a discount of 20%.

(x) Realisation expenses Rs 2000 were paid by Kishore.

(xi) Dissolution expenses were 9000. Out of the said expense Rs 4000 were to be borne by the firm and the balance by a partner.

(xii) Dissolution expenses were 9000. Out of the said expense Rs 4000 were to be borne by the firm and the balance by a partner. The expenses were paid by a partner.

(xiii) X agrees to do dissolution work for an agreed remuneration of Rs 5000 & the firm bears all realisation expenses which amounted to Rs 8000.

Question : A,B,C are three partners .B died on 31 st August .Calculate B ‘s share of profits when the annual profit was Rs 54000. Books are closed on 31st march every year

a) 2300

b) 7500

c) 3455

d) 5700

Answer : B

Question : A, B, C are three partners and C died .calculate new PSR .

a) 3:4

b)1:1

c) 4:2

d) 3:1

Answer : B

Question : A, B and C are sharing profits in the ratio of 2:2:1. B died on 31.3.12. Accounts are closed on 31st December. Sales for the year 2011 amounted to ₹ 3,00,000. Sales of ₹1,00,000 amounted between the period from 1st Jan 2012 to 31st March, 2012. The profits for the year 2011 amounted to ₹ 30,000. Calculate deceased partner’s share in the profits of the firm.

a) ₹5,000

b) ₹4,0000

c) ₹1,000

d) ₹6,000

Answer : B

Question : The legal representatives of a deceased partner is entitled , at his discretion, to interest on amount due from the date of death to the date of payment.

a)3%

b) 5%

c) 7%

d) 6%

Answer : D

Question : X,Y,Z are partners sharing profits in the ratio of 2:2:1.Y dies and his share is taken over by Z only. Calculate new PSR.

a) 4:5

b) 2:3

c) 5:6

d) 1:2

Answer : B

(b) Goodwill of the firm

(d) None of these.

Very Short Answer Type Questions

Short Answer Type Questions

Short Answer Type Questions -II

Free study material for Accountancy

CBSE Accountancy Class 12 Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner Worksheet

Students can use the practice questions and answers provided above for Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner to prepare for their upcoming school tests. This resource is designed by expert teachers as per the latest 2026 syllabus released by CBSE for Class 12. We suggest that Class 12 students solve these questions daily for a strong foundation in Accountancy.

Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner Solutions & NCERT Alignment

Our expert teachers have referred to the latest NCERT book for Class 12 Accountancy to create these exercises. After solving the questions you should compare your answers with our detailed solutions as they have been designed by expert teachers. You will understand the correct way to write answers for the CBSE exams. You can also see above MCQ questions for Accountancy to cover every important topic in the chapter.

Class 12 Exam Preparation Strategy

Regular practice of this Class 12 Accountancy study material helps you to be familiar with the most regularly asked exam topics. If you find any topic in Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner difficult then you can refer to our NCERT solutions for Class 12 Accountancy. All revision sheets and printable assignments on studiestoday.com are free and updated to help students get better scores in their school examinations.

FAQs

You can download the latest chapter-wise printable worksheets for Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner for free from StudiesToday.com. These have been made as per the latest CBSE curriculum for this academic year.

Yes, Class 12 Accountancy worksheets for Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner focus on activity-based learning and also competency-style questions. This helps students to apply theoretical knowledge to practical scenarios.

Yes, we have provided solved worksheets for Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner to help students verify their answers instantly.

Yes, our Class 12 Accountancy test sheets are mobile-friendly PDFs and can be printed by teachers for classroom.

For Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner, regular practice with our worksheets will improve question-handling speed and help students understand all technical terms and diagrams.