Access free TS Grewal Accountancy Class 11 Solution Chapter 18 Financial Statements of Sole Proprietorship 2026 below. Students can now access free TS Grewal Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 18 Financial Statements of Sole Proprietorship TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 18 Financial Statements of Sole Proprietorship Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 18 Financial Statements of Sole Proprietorship TS Grewal Class 11 Solved Exercises

About this chapter: Chapter 18 of the TS Grewal Accountancy Class 11 textbook on Financial Statements of Sole Proprietorship is a very important topic from which many questions are regularly asked in exams. Students should understand how the books of accounts of sole proprietorships should be maintained. Students should understand how the trading and profit and loss account, balance sheet should be maintained for sole proprietorships. It is important to maintain accurate financial statements to be compliant with accounting standards and local laws. All these topics have been clearly explained in this chapter in TS Grewal. Students will also understand the adjustments which are allowed to be made in such books. All concepts are followed by theoretical and practical questions for which we have provided all answers below prepared by expert accountancy teachers.

Question.1. What is a Trading Account and why is it prepared?

Answer: 1 Trading Account is the account that reveals the gross profit or gross loss. It is credited with the amount of sales of goods and debited with the opening stock of goods along with the direct expenses related to the sales made. Trading Account is prepared to know gross profit or gross loss during the accounting period.

Question.2. Explain the object of preparing Profit and Loss Account.

Answer: 2 Profit and Loss Account is prepared to know net profit or net loss during the accounting period.

Question.3. How does Profit and Loss Account differ from Trading Account?

Answer: 3

Question.4. Give any three points of distinction between Capital Expenditure and Revenue Expenditure.

Answer: 4 Three points of distinction between Capital Expenditure and Revenue Expenditure are:

Question.5. What are Direct Expenses? Give two examples.

Answer: 5 Direct expenses are those expenses which are incurred on purchases of goods up to the point of bringing them to the place of business. In the case of manufacturing business, they are the expenses incurred to make then ready for sale.

The two examples of direct expenses are:

1. Octroi paid on purchases.

2. Power Expenses.

Question .5. Why is Balance Sheet prepared? (Old Question)

Answer: 6 Balance Sheet is prepared with a view to measure true financial position of a business at a particular point of time. It is a method to show the financial position of a business in a systematic and standard form. The financial position of the business can be understood at a glance. The debit and credit balances of related accounts are shown on the assets and liabilities side of the Balance Sheet.

Question.6. What are Indirect Expenses? Give two examples.

Answer: 7 Indirect expenses are those expenses which are incurred and are not directly associated with the purchases of goods or manufacture of goods.

The two examples of indirect expenses are:

1. Office salaries.

2. Warehouse expenses.

Question.7. Distinguish between Profit and Loss Account and Balance Sheet on any six basis.

Answer: 7 Distinguish between Profit and Loss Account and Balance Sheet on any six basis are:

Question.8. What is meant by marshaling of assets and liabilities? Name the way in which a Balance Sheet may be marshaled.

Answer: 8 Assets and Liabilities are shown in a certain order in the Balance Sheet. Therefore they should be arranged in certain group and in a particular order. This is called Grouping and Marshaling of the Balance Sheet.

‘Grouping’ means putting items of a similar nature under a common accounting head. The arrangement of assets and liabilities in a particular order in the Balance Sheet is called Marshaling.

Question.9. Briefly explain Current Liabilities.

Answer: 9 Current Liabilities are payable during or within the year. Creditors, Bills Payable, Outstanding Expenses, Bank Overdrafts, Short-term Loans etc., are the examples of Current Liabilities.

Question.10. Briefly explain Current Assets.

Answer: 10 Current Assets are those assets which are held for resale or for converting into cash. These are the assets which are likely to be realized within a period of one year or during the period of normal operating cycle. A business earns profit by selling these assets but not by keeping them as stock for a longer period. These assets are temporary in nature and may change from time to time. These are sometimes referred to as floating or circulating assets.

Question.11. Write a short note on Contingent Liability.

Answer: 11 Contingent Liability is a liability that becomes payable on the happening of an event. If the event does not happen, then no amount is payable. Such liabilities are not accounted for and not shown in the Balance Sheet. However they are shown as footnotes to the Balance Sheet. The contingent liabilities are:

1. Bills Discounted: If the firm discounts the Bills Receivable at bank then the primary liability is with the accepter of the bill. If the acceptor does not pay the bill then the firm is liable to the bank.

2. Guarantee for Loan: If the firm has stood surety for a loan, it will be liable to pay the amount if the borrower fails to repay the loan.

3. Disputed Claims: If some other party has lodged a claim against the firm and succeeds in fixing the claim then the firm has to pay the liability.

Question .12. Distinguish between Current Assets and Fixed Assets.

Answer 12.

Question .13. Distinguish between a Balance Sheet and Trial Balance. (Any five points)

Answer 13.

Question .14. Write short notes on any two: (Old Question)

(i) Contingent Liability

(ii) Capital expenditure

(iii) Operating profit

Answer 14.

(i) Contingent Liabilities: Contingent Liability is a liability that becomes payable on the happening of an event. If the event does not happen, then no amount is payable. Such liabilities are not accounted for and not shown in the Balance Sheet. However they are shown as footnotes to the Balance Sheet.

The contingent liabilities are:

1. Bills Discounted: If the firm discounts the Bills Receivable at bank then the primary liability is with the accepter of the bill. If the acceptor does not pay the bill then the firm is liable to the bank.

2. Guarantee for Loan: If the firm has stood surety for a loan, it will be liable to pay the amount if the borrower fails to repay the loan.

3. Disputed Claims: If some other party has lodged a claim against the firm and succeeds in fixing the claim then the firm has to pay the liability.

(ii) Capital Expenditure: Capital Expenditure is the amount incurred by an enterprise on purchase of fixed assets. Fixed assets are used in the business to generate income and held not for resale. Fixed assets purchased may be tangible or intangible. Capital Expenditure gives benefit to many periods even beyond the accounting period. The Capital Expenditure increases the earning capacity and reduces the operating expenses of a business.

(iii) Operating Profit: Operating Profit means profit from operating activities of the business. It is excess of gross profit over operating expenses. Gross profit is excess of revenue or net sales over cost of goods sold. Operating expenses include office and administrative expenses, selling and distribution expenses, finance expenses, bad debts, etc. Mathematically

Net Sales = Cash Sales + Credit sales — Sales Return.

Operating Profit = Net Sales — Operating Cost

= Net Sales — (Cost of Goods Sold + Office and Administrative Expenses + Selling Expenses + Finance Expenses

Or

Operating Profit = Net Profit + Non—Operating Expenses — Non-Operating Income.

Question .14. Calculate Gross Profit and Cost of Goods Sold from the following information:

Net Sales Rs. 1,00,000

Gross Profit is 25% on cost.

Answer 14.

Net Sales = Rs. 1,00,000

Question .15. Write a note on types of Assets with one example of each.

Answer: 15 Assets in the Balance Sheet are divided into two parts as follows:

1. Fixed Assets: Fixed Assets are those assets that are acquired for continued use and not for resale.

Fixed Assets are valued at cost less depreciation. They may be further divided into either tangible assets or intangible assets.

(a) Tangible Fixed Assets are those fixed assets which can be seen and touched for example Land and Building, Plant and Machinery, Furniture and Fixture, etc.

(b) Intangibles Fixed Assets are those fixed assets which are not in a physical form that is they can neither be seen nor touched for example goodwill, patents, trademarks, copyrights, technical knowhow, etc.

2. Current Assets: Current Assets are those assets which are held for resale or for converting into cash. These are the assets which are likely to be realised within a period of one year or during the period of normal operating cycle. A business earns profit by selling these assets but not by keeping them as stock for a longer period. These assets are temporary in nature and may change from time to time. These are sometimes referred to as floating or circulating assets. For example stock, debtors, cash, bank, bills receivable, etc.

3. Investments: Investments are capital expenditure incurred on purchase of shares, securities, debentures, bonds, etc. to earn interest dividend, etc. Investments are shown separately in the Balance sheet after fixed assets and before current assets. For example shares, securities, debentures, bonds, etc.

4. Fictitious Assets: Fictitious Assets in real scene are losses yet to be written off. For example, Advertisement Suspense Account, Discount on Issue of Debentures, Accumulated Losses, Profit and Loss Account Debit Balance, etc.

Question .16. List the following assets in order of liquidity:

Sundry Debtors, Stock, land and Building, Plant and Machinery, Furniture, Investments, Cash in Hand and Cash at Bank.

Answer: 16 List of the following assets in order of liquidity are:

1. Cash in Hand

2. Cash at Bank

3. Sundry Debtors

4. Stock

5. Investments

6. Furniture

7. Plant and Machinery

8. Land and Building

Question .17. List the assets in Question .16 in order of permanence.

Answer: 17 List of the following assets in order of permanence are:

1. Land and Building

2. Plant and Machinery

3. Furniture

4. Investments

5. Stock

6. Sundry Debtors

7. Cash at Bank

8. Cash in Hand

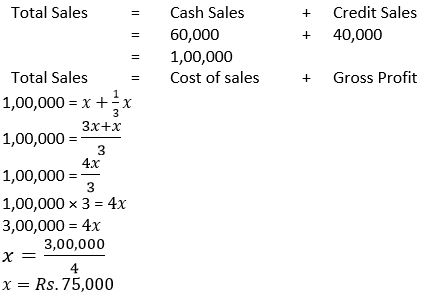

Question.18. Ascertain Cost of Goods Sold from the following:

Amount

Opening Stock 8,500

Purchases 30,700

Direct Expenses 4,800

Indirect Expenses 5,200

Closing Stock 9,000

Answer 18.

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

= Rs. 8,500 + Rs. 30,700 + Rs. 4,800 – Rs. 9,000

= Rs. 35,000

Question.19. Cash sales of a business in a year were Rs. 29,000 and credit sales Rs. 31,000. The cost of goods sold (including direct expenses) works out at Rs. 52,000. Find out the Gross Profit.

Answer 19.

Gross Profit = Cash Sales + Credit Sales – Cost of Goods Sold

= Rs. 29,000 + Rs. 31,000 – Rs. 52,000

= Rs. 8,000

Question .19. Following information was taken from an Income Statement: (Old Question)

Opening Stock Rs. 5,000; Sales Rs. 16,000; Carriage Inward Rs. 1,000; Sales Return Rs. 1,000; Gross Profit Rs. 6,000; Purchases Rs. 10,000; and Purchases Return Rs. 900.

Answer 19.

Question .20. Calculate Gross Profit and Cost of Goods Sold from the following information:

Net Sales Rs. 1,00,000

Gross Profit 33 1/3 %

Answer 20.

Question.21. Calculate Closing Stock from the following:

Opening Stock Rs. 36,000; Net Purchases Rs. 45,000; Salaries and Wages Rs. 7,000; Sales Rs. 60,000; Gross Loss Rs. 4,000; Freight Inwards Rs. 6,000.

Answer 21.

Closing Stock = Opening Stock + Net Purchases + Freight Inwards – Sales – Gross Loss

= Rs. 36,000 + Rs. 45,000 + Rs. 6,000 – Rs. 60,000 – Rs. 4,000

= Rs. 23,000

Class 11 Accounts Ch 18 Practical Problems Solutions

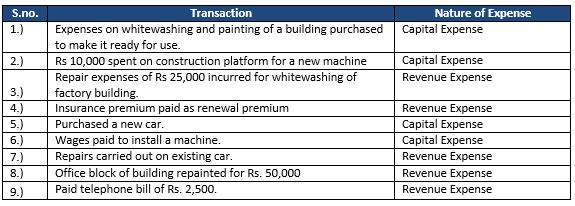

1.) Expenses on whitewashing and painting of a building purchased to make it ready for use.

2.) Rs. 10,000 spent on construction platform for a new machine.

3.) Repair expenses of Rs. 25,000 incurred for whitewashing of factory building.

4.) Insurance premium paid as renewal premium.

5.) Purchased a new car.

6.) Wages paid to install a machine.

7.) Repairs carried out on existing car.

8.) Office block of building repainted for Rs. 50,000

9.) Paid telephone bill of Rs. 2,500.

Answer: 1

Below are the bifurcation of Capital Expense and Revenue Expenses.

Point of Knowledge:-

Capital Expenditure: - Capital Expenditure is the amount spent by an enterprise on purchase of fixed assets that are used in the business to earn income and are not intended or resale. Fixed assets purchased may be tangible or intangible.

Revenue Expenditure: - Revenue Expenditure is the amount spent on running a business. An expenditure which is not capital can be considered as revenue expenditure.

Trading Account

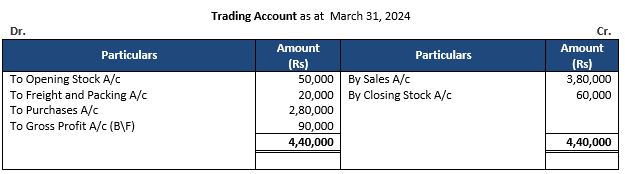

Question 2: From the following information determine Gross Profit for the year ended 31st March, 2024:-

Answer 2:

Statement Showing Calculation of Gross Profit: -

Point of knowledge:-

(i) Gross Profit = Sales + Closing Stock – (Opening Stock + Goods Purchased+ Freight and Packing)

= 3,80,000 + 60,000 – (50,000 + 2,80,000 + 20,000)

= 4,40,000 – 3,50,000

Gross Profit = 90,000

(ii) Packing Expenses on the sales is an indirect Expense, so we cannot include it in calculation of Gross Profit.

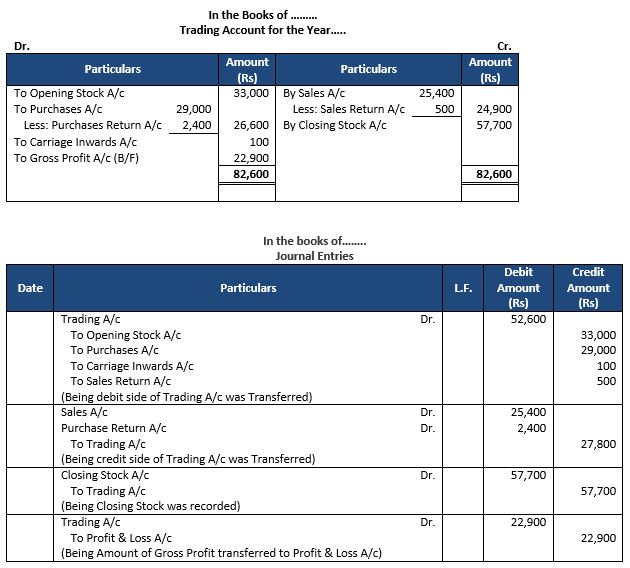

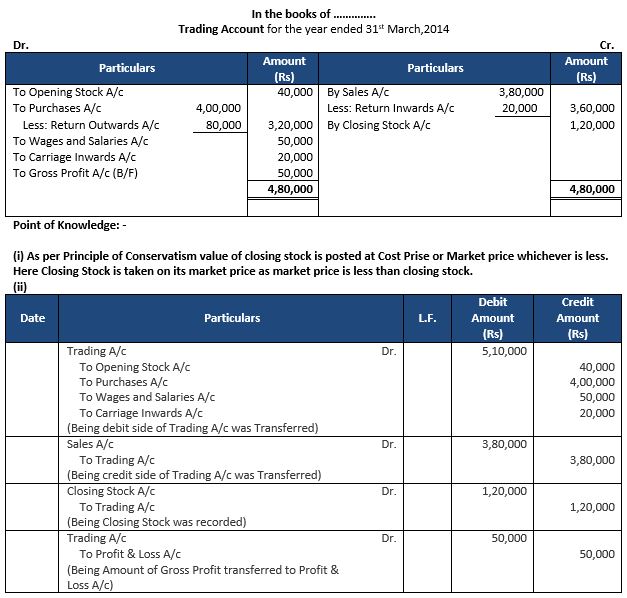

Question 3: Prepare Trading Account from the transactions given below:

Answer 3:

Statement Showing Calculation of Gross Profit: -

Point of Knowledge:-

(i) Depreciation in an Indirect Expense so we cannot include it in Trading Account.

(ii) Trading Account is prepared to know Gross Profit or Gross Loss during the accounting period. This account is based on marching the selling price of goods and services with the cost of goods sold and services rendered

Question 4: Calculate Closing Stock from the following details:

Answer 4:

Calculation of Gross Profit

Gross Profit = Total Sales - Cost of Sales

= 1,00,000 - 75,000

= 25,000

Calculation of Closing Stock

Closing Stock = Opening Stock + Purchases + Gross Profit - Total Sales

= 20,000 + 70,000 + 25,000 - 1,00,000

= 15,000

Question 5: Ascertain Gross Profit the following:

Answer 5:

Statement Showing Calculation of Gross Profit: -

Question 6: From the following information prepare Trading Account for the year ended 31st March, 2024:

Net Realizable Value (Market Value) of stock as on 31st March, 2018 was Rs 1,20,000.

Answer 6:

Statement Showing Calculation of Gross Profit: -

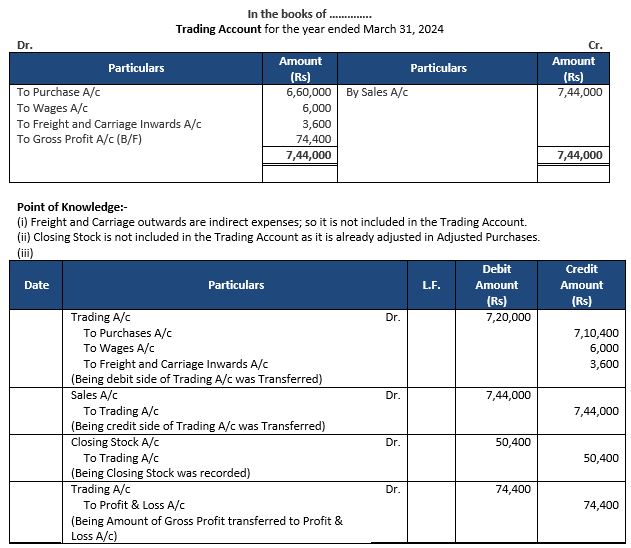

Question 7: From the following information, prepare Trading Account for the year ended 31st March, 2024: Adjusted Purchases Rs. 6,60,000; Sales Rs. 7,44,000; Closing Stock Rs. 50,400; Freight and Carriage Inwards Rs. 3,600; Wages Rs. 6,000; Freight and Cartage Outwards Rs. 2,000.

Answer 7:

Statement Showing Calculation of Gross Profit: -

Entry of Purchases account was pasted with without adjusted amount

Purchases = Purchases (After Adjustment) + Closing Stock

Purchases = Rs. 6.60,000 + Rs. 50,400

Purchases = Rs. 7,10,400

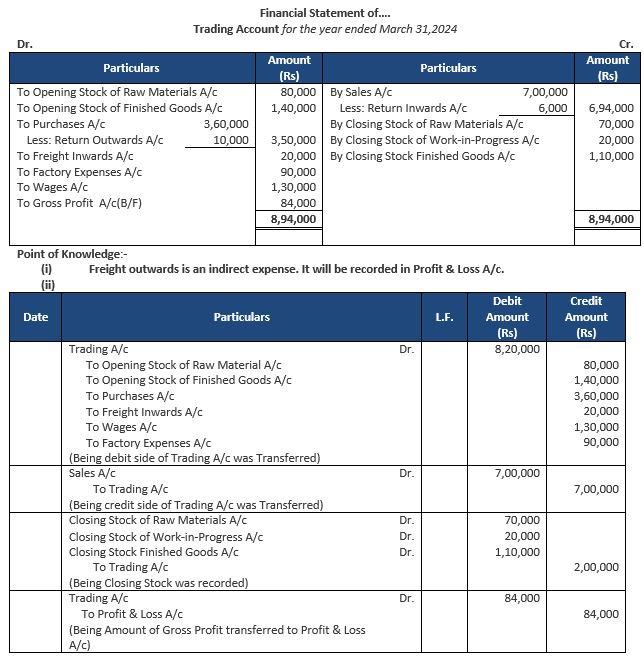

Question 8: Following balances appear in the Trail Balance of a firm as on 31st March, 2024:

Prepare Trading Account of the firm.

Answer 8:

Statement Showing Calculation of Gross Profit: -

Question 9: From the following information, prepare Trading account for the year ended 31st March, 2018: Adjusted Purchases Rs. 5,50,000; Sales Rs. 6,25,000; Freight and Carriage Inwards Rs. 3,000; Wages Rs. 7,000; Freight and Cartage Outwards Rs. 2,500; Closing Stock Rs. 50,000. (Old Question)

Answer 9:

Statement Showing Calculation of Gross Profit: -

Point of Knowledge:-

(i) Freight and Carriage Outwards are indirect expenses; so it is not included in the Trading Account.

(ii) Closing Stock is not included in the Trading Account as it is already adjusted in Adjusted Purchases.

Entry of Purchases account was pasted with without adjusted amount

Purchases = Purchases (After Adjustment) + Closing Stock

= Rs. 5.50,000 + Rs. 50,000

= Rs. 6,00,000

Question 9: From the following figures, calculate Operating Profit:

Answer 9:

Operating Profit = Net Profit – Rent Received – Gain on Sale of Machine+ Interest on loan - Donation

Operating Profit = 1, 00,000 – 10,000 – 15,000 + 20,000 – 2,000

Operating Profit = Rs. 93,000

Point of Knowledge:-

(i) Operating Expenses includes office and administrative expenses, selling and Distribution Expenses, Cash discount allowed, interest on bills payable and other short term debts, bad debts and so on.

Operating Profit = Net Sales – Operating Cost (Cost of goods sold + Administration and office expenses + Selling and distribution Expenses)

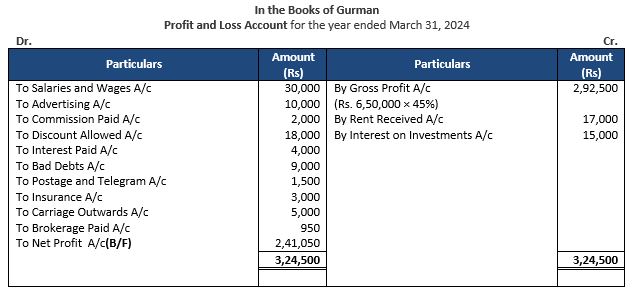

Question 10: From the following, prepare Profit and Loss Account of Gurman for the year ended 31st March, 2024:

The Gross Profit was 45% of sales, which amounted to Rs 6,50,000.

Answer 10:

Statement Showing Calculation of Gross Profit: -

Point of Knowledge:-

Calculation of Gross Profit: -

(i) Gross Profit = Sales × Percentage Given

= Rs. 6, 50,000 × 45%

= Rs. 2, 92,500

(ii) Amount Of Gross Profit Depends On The Valuation Of Stock. Increases In The Value Of Stock Will Increase The Gross Profit. Similarly, Reduction In The Value Of Closing Stock Will Reduce The Gross Profit.

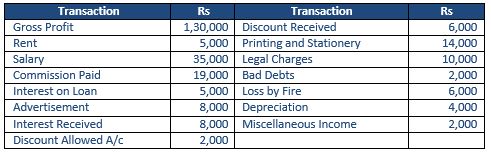

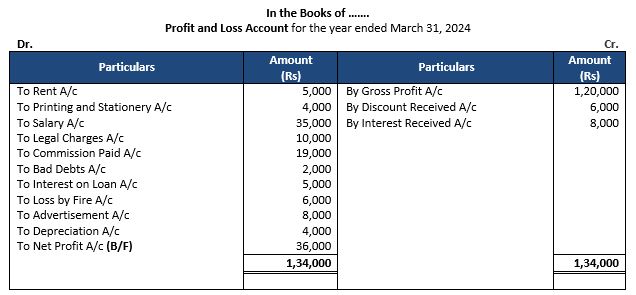

Question 11: From the following information, prepare Profit and Loss Account for the year ended 31st March, 2024:

Answer 11:

Statement Showing Calculation of Net Profit: -

Point of Knowledge:-

(i) The Profit and Loss account is prepared to ascertain the Net Profit or Net Loss of the Business.

(ii) The Balance of the Profit and loss account is transferred to the capital account of the Proprietor.

(iii) Item like indirect expenses related to sales, Distribution, administration, finance, etc. are shown in the Profit and loss account.

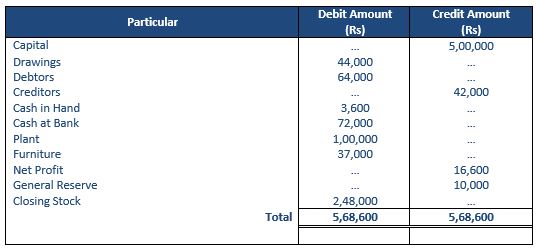

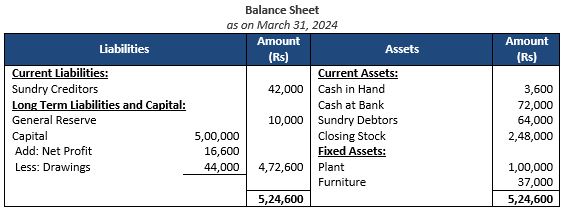

Question 12: From the following particular, prepare Balance Sheet as at 31st March, 2024:

Answer 12:

Statement Showing Liabilities and Assets: -

Point of Knowledge:-

(i) A balance sheet is prepared to show the financial position of a business concern; this financial statement shows the various types of assets and liabilities.

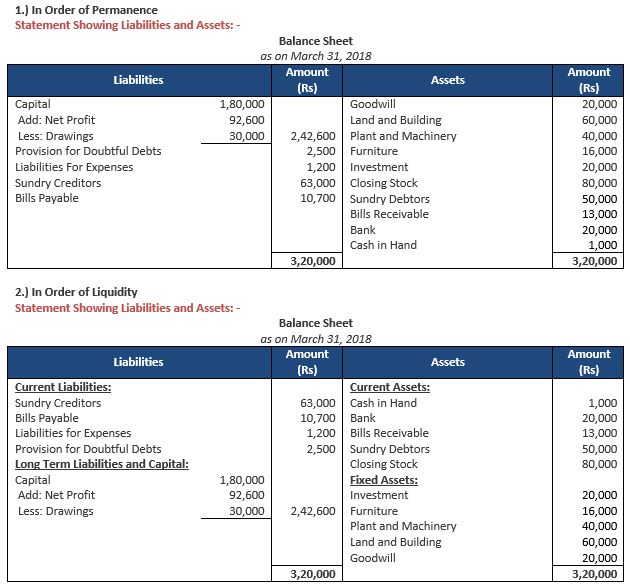

Question 13: From the following information, prepare Balance Sheet of a trader as at 31st March, 2024 arranging the assets and liabilities–(1) In order of permanence (2) in order of liquidity:

Answer 13:

Point of Knowledge:-

(i) It is desirable that in a balance sheet various types of assets and liabilities should be shown separately and prominently. This would give meaningful and logical information.

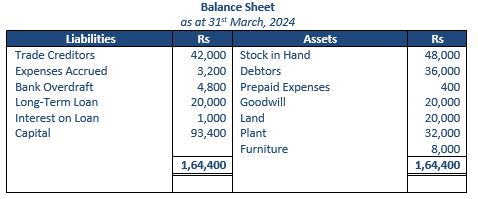

Question 14: From the Balance Sheet given below, calculate:

1.) Fixed Assets

2.) Current Assets

3.) Current Liabilities

4.) Working Capital

Answer 14:

(i) Fixed Assets = Good will + Land + Plant + Furniture

= 20,000 + 20,000 + 32,000 + 8,000

= Rs. 80,000

(ii) Current Assets = Stock in Hand + Debtors + Prepaid Expenses

= 48,000 + 36,000 + 400

= Rs. 84,400

(iii) Current Liabilities = Trade Creditors + Expenses Accrued + Bank Overdraft + Int. on loan

= 42,000 + 3,200 + 4,800 + 1,000

= Rs. 51,000

(iv) Working Capital = Current Assets - Current Liabilities

= 84,400 - 51,000

= Rs. 33,400

Point of knowledge: -

(i) Fixed assets are those assets that are acquired for continued use and are not meant for resale, through later it may be decided to sell a particular asset.

(ii) Current assets are those assets of the business which are kept temporarily for resale or for converting into cash.

(iii) Current Liabilities these liabilities are payable by the business within a year.

(iv) Working Capital is Current assets over current liabilities.

Final Accounts

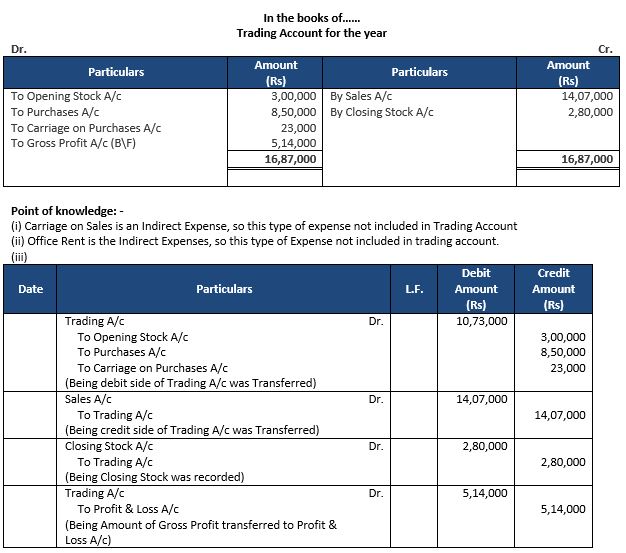

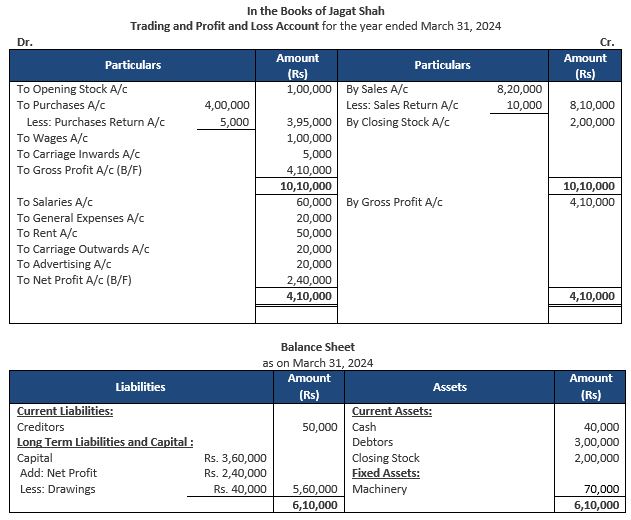

Question 15: Prepare Trading and Profit and Loss Account and Balance Sheet of Jagat Shah as at 31st March, 2024 from the following balances:

The Closing Stock was valued at Rs 2,00,000

Answer 15:

Below Are the Financial Statements of Jagat Shah:-

Point of Knowledge:-

(i) The balance sheet is prepared with a view to measure the true financial position of a business at a particular point of time. It is device to show the financial position of a business of a business in a systematic and standard form.

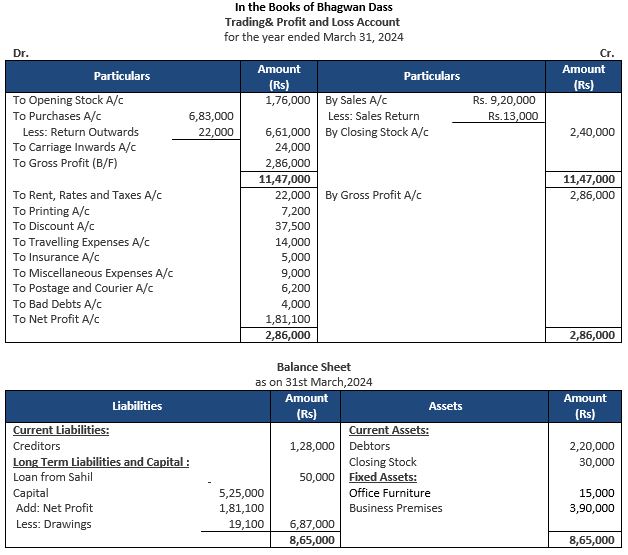

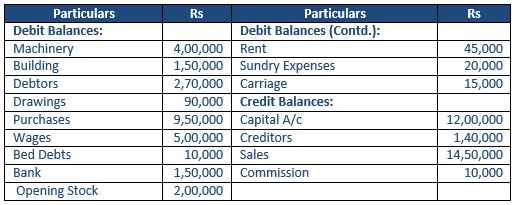

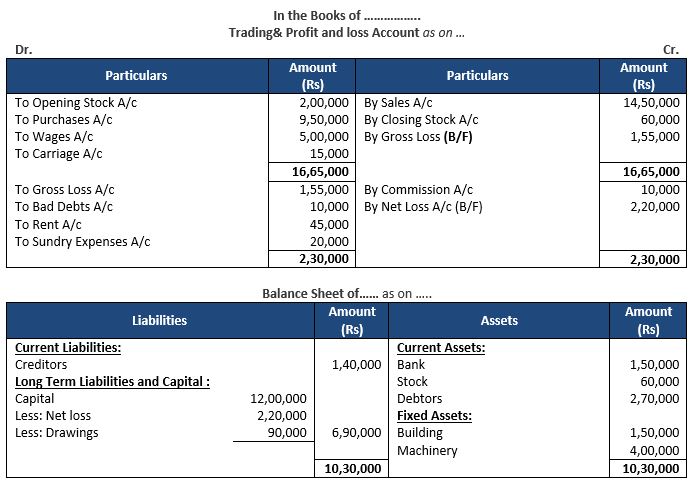

Question 16: The following are the balances as on 31st March, 2024 extracted from the books of Dass:

The stock on 31st March, 2018 was valued at Rs 2,40,000.

Prepare Trading Account, Profit and Loss Account and Balance Sheet as at 31st March, 2024

Answer 16:

Point Of Knowledge:-

(i) The Purpose of Trial Balance is to establish the Arithmetical Accuracy of the Books of Accounts, and the Purpose of making Balance sheet is to show the financial position of the business.

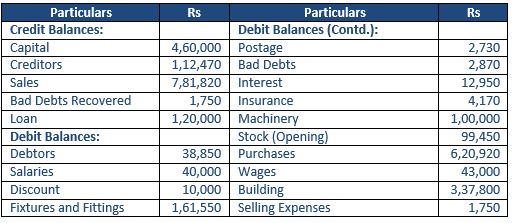

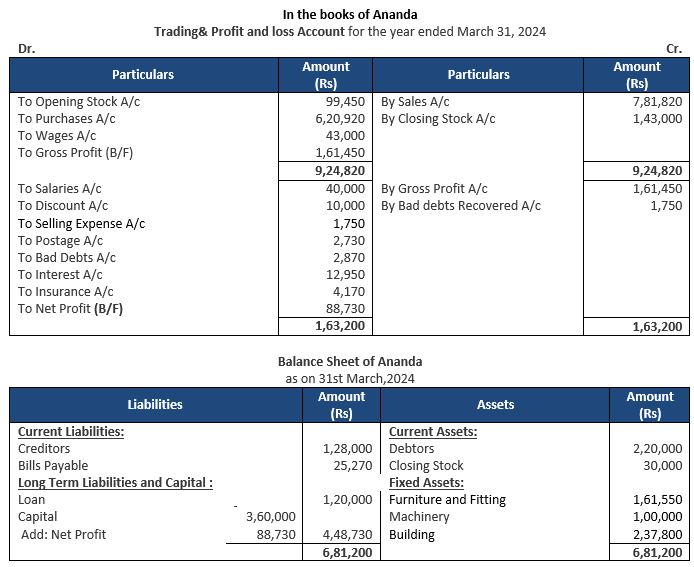

Question 17: From the following balances of Anand, prepare Trading Account, Profit and Loss Account and Balance Sheet as at 31st March, 2024:

Value of goods on hand (31st March, 2024) was Rs. 1,43,000.

Answer 17:

Point of Knowledge:-

(i) Balance sheet provides the information as to the profitability and financial position of the firm, but no such information provided by the Trail balance.

(ii) Only personal and real account appears in the balance sheet but in trail balance all accounts must be written no account can be left out.

Question 18: From the following balances, prepare Trading and Profit and Loss Account and the Balance Sheet:

Closing Stock was of Rs 70,000 but its net realizable value was estimated at Rs 60,000.

Answer 18:

Point of Knowledge:-

(i) Closing Stock is recorded at cost price or market price which is lower, So here we are taking Rs. 60,000.

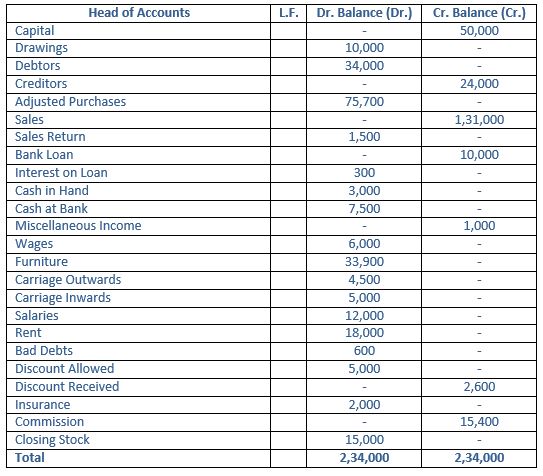

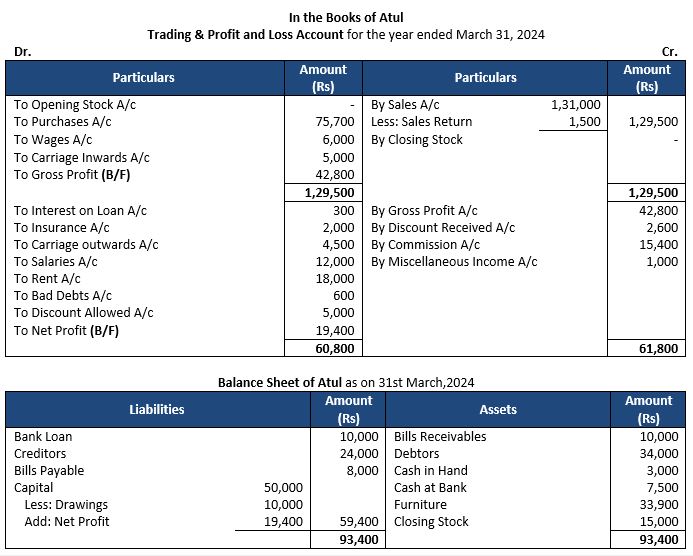

Question 19: The following is the Trail Balance of Atul as at 31st March, 2024:

Answer 19:

Point of Knowledge:-

As Closing Stock is given in the Trial Balance, it will be shown only in the Balance Sheet as an asset.

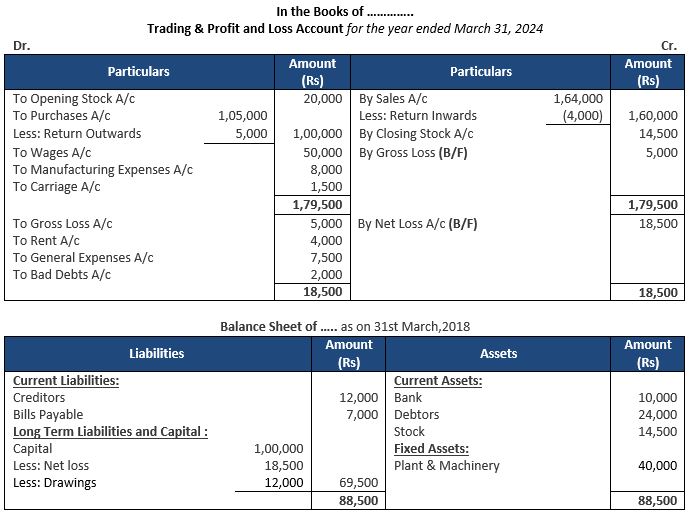

Question 20: From the following balances, as on 31st March, 2024, prepare Trading and Profit and Loss Account and Balance Sheet:

Closing Stock on 31st March, 2018 was valued at Rs 14,500.

Answer 20:

Point of Knowledge:-

(i) Return inwards are deducted from sales whereas Return Outwards are deducted from the purchases in the Trading Account.

(ii) Carriage inwards is debited to the trading account and carriage outward to the profit and loss account.

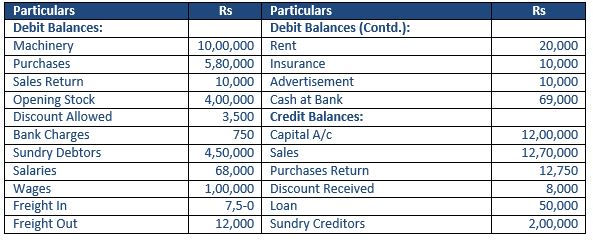

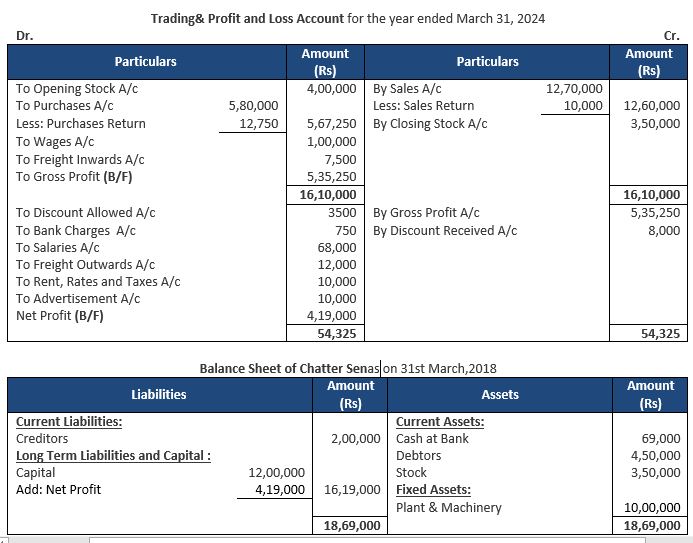

Question 21: Trial Balance of Chatter Sen on 31st March, 2024 revealed the following balances:

Stock on 31st March, 2024 was valued at Rs. 3,50,000 at cost and its net realizable value (market Value) was Rs. 4,00,000.

Prepare Trading and Profit and Loss Account for the year ended 31st March, 2024 and Balance Sheet as at the date

Answer 21:

Point of Knowledge:-

(i) Freight outward is not entered in the Trading Account; it will appear in the Profit & Loss Account.

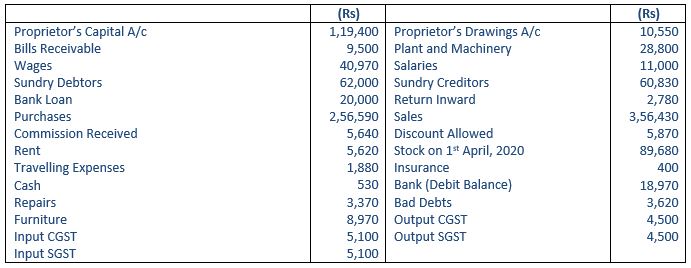

Question.22: Prepare Trail Balance, Trading and Profit and loss Account for the year ended 31st March, 2024 and Balance Sheet of the Premier Trading Company as at that date, from the following extracts of Ledger balances:

Stock in Hand on 31st March, 2024 was valued at Rs. 1,28,960.

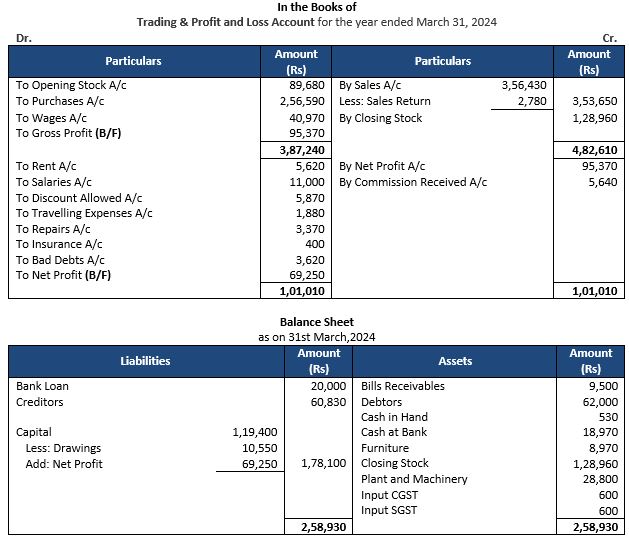

Answer 22:

Question 23: Following Trial Balance is extracted from the books of a merchant on 31st March, 2018: (Old Question)

Stock in Hand on 31st March, 2018 was valued at Rs 32,500.

From the above, prepare Trading and Profit and Loss Account for the year ended 31st March, 2018 and Balance Sheet as at that date.

Answer 23:

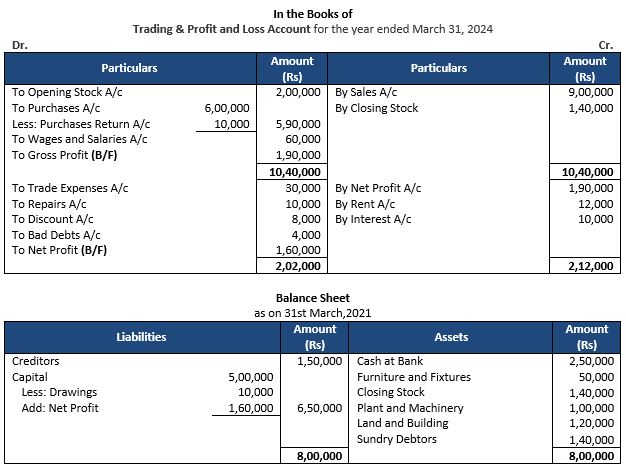

Question.23. From the following Trail Balance, prepare Trading and Profit and Loss Account for the year ended 31st March, 2021 and Balance Sheet as at that date:

The stock on 31st March, 2021 was valued at Rs. 1,40,000.

Answer 23: