Read TS Grewal Accountancy Class 11 Solution Chapter 11 Special Purpose Books II Other Book 2026. Students should study TS Grewal Solutions Class 11 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 11 Accountancy have been prepared by expert teachers. These TS Grewal Class 11 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 11 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 11 Accounts Chapter 11 Special Purpose Books II Other Book TS Grewal Solutions

TS Grewal Solutions for Chapter 11 Special Purpose Books II Other Book Class 11 Accounts have been provided below based on the latest TS Grewal Class 11 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 11 will help students to improve their concepts and easily solve accountancy questions for Class 11.

Chapter 11 Special Purpose Books II Other Book TS Grewal Class 11 Solutions

Question.1 State most commonly used subsidiary books.

Answer 1.

Most common subsidiary books are:-

1. Cash book

2. Purchases book

3. Sales book

4. Purchases return or return outwards book

5. Sales return or return inwards book

6. Bills receivable book

7. Bills payable book

8. Journal proper

Question.1. What is a Purchases Book? (Old Question)

Answer 1. Purchases Book is a subsidiary book in which credit purchases of goods dealt in or stores and raw material used for production are recorded.

Question.2 Distinguish between Purchases Book and Purchases Account?

Answer 2.

Distinguish between Purchases Book and Purchases Account:-

Question.2. Define a Sales Book. (Old Question)

Answer 2. Sales Book is a subsidiary book in which credit sales of goods dealt in are recorded.

Question.3. Distinguish between Sales Book and Sales Account?

Answer 3. Distinguish between Sales Book and Sales Account:-

Question.4. What is a Purchases Return Book? Give its specimen.

Answer 4. Purchases Return Book is a subsidiary book in which the return of goods purchased is recorded.

Below is specimen of Purchases Return Book:-

Question.5. What is meant by a Journal Proper?

Answer 5. Journal Proper is a book of account in which those transactions and events are recorded which are not recorded in the subsidiary books.

Question.6. What is meant by a Sales Return Book? When is it opened?

Answer 6. Sales Return Book is a subsidiary book maintained to record the goods or materials returned by the purchaser that had been sold on credit.

This book is maintained if the return of goods is frequent otherwise it can be recorded in the journal.

Question.7. For what purposes is a Journal Proper used?

Answer 7. Journal Proper or General Journal is used for the purpose of recording the following Journal Entries.

1.) Opening Entry

2.) Closing Entries

3.) Rectification Entries

4.) Transfer Entries

5.) Adjusting Entries

6.) Outstanding expenses, i.e., expenses incurred but not yet paid

7.) Prepaid expenses, i.e., expense already paid in advance for some period in the future

8.) Income received in advance

9.) Accrued Income, i.e., income earned but not received

10.) Interest on capital, i.e., the interest which the proprietor thinks proper to allow on his investment

11.) Closing Stock.

Question.8. Give two examples of entries which appear in a ‘Journal Proper’.

Answer 8. Two examples of entries which appear in a Journal Proper of General Journal are:

(i) Interest receivable from Rajnish Rs. 3,500.

(ii) Wages due to laborers Rs. 20,000.

Question.9. What is Invoice?

Answer 9. An Invoice or Bill is prepared by the seller when the goods are sold on credit. It has details of the party to whom goods are sold, goods sold and the total sales amount. The original copy of the sales invoice is sent to the purchaser and a duplicate copy is retained as an evidence of the sales for recording it in the books of account and for future reference. From the purchaser's point of view, purchases are evidenced by credit bill received from the supplier. One prepares an invoice but receives a bill, though the two terms are interchangeable and mean the same thing.

Question.10. What is a Debit Note?

Answer 10. The purchaser prepares a 'Debit Note' and sends it to the supplier. A Debit Note is prepared w en goods are returned by the purchaser due to some reason. It is called a Debit Note because the party's account is debited with the amount written in this note. The 'Debit Note' is the basis for writing in the Purchases Return or Return Outward Book.

Question.11. What is a Credit Note?

Answer 11. A Credit Note is made out evidencing that credit has been granted to a debtor. For example, if a customer returns goods previously invoiced, or the customer is allowed further discount, a credit note is issued. The effect of a credit note is that the amount of the customer's indebtedness is reduced or, if it is already settled, to enable the customer to purchase goods to the value of credit without further payment.

Question.12. What are transfer entries?

Answer 12. Transfer entries are passed to transfer an account from one account to another account. This type of transfer is also made through a journal entry called transfer entry.

Non-Cash Vouchers or Transfer Vouchers refers to vouchers prepared for transactions not involving cash. Examples of these are Invoice or Bills, debit and Credit Notes, etc. Non-Cash Vouchers are prepared for the transactions of credit sales, credit purchases, goods returned, rectifying the mistake, etc. Non-Cash Vouchers or Transfer Vouchers gives the following information:

(i) Name and Address of the Organization.

Question.13. Why opening entries are passed?

Answer 13. Opening entry is the entry made in the beginning of a financial year to open the books of debiting assets and crediting liabilities and capital, appearing in the Balance Sheet of the previous year.

Question.14. What are Adjustment Entries?

Answer 14. Adjustment Entries are passed at the end of the year to adjust the amounts paid or received in advance or for amounts not yet settled in cash. Such an adjustment is also made through Journal entries. Usually the adjustment entries are made for outstanding expenses, prepaid expenses, interest on capital, depreciation, etc.

Question.15 Briefly explain the concept of GST?

Answer 15. Goods and Services Tax (GST) is a comprehensive indirect tax levied at the prescribed rate on every supply or sale of goods or services except on petroleum and alcohol for human consumption. Supply of goods means sale of goods whereas supply of services means rendering of services.

Question.16. What is the reason for maintaining accounts for CGST, SGST and IGST?

Answer 16. The reason for maintaining separate accounts for CGST, SGST and IGST are to setoff the GST Paid against the GST Collected in the prescribed order. GST paid or Input GST individually (Input CGST, SGST and IGST) is set off against GST Collected (Output GST) individually (Output CGST, SGST and IGST) in the prescribed order. Hence, it is necessary that separate accounts for Input GST and Output GST for each category of GST be maintained. It will enable the taxpayer to follow prescribed order of setting off the each category of GST.

Practical Problems :----->

Question 1: Record the following transactions in the Purchases Book of Krishna General Stores, Delhi:-

Answer 1:

Question 2: Verma Bros. carry on business as wholesale cloth dealer. From the following, write up their Purchases Book for January, 2024

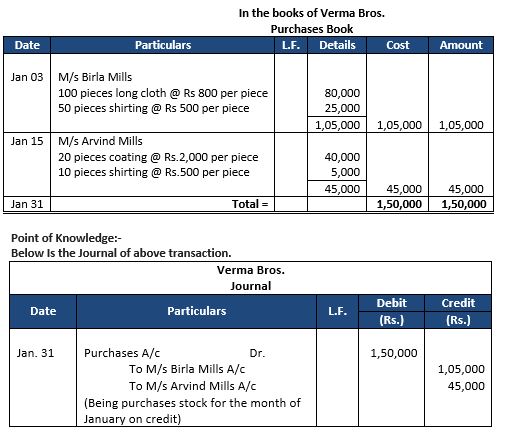

Answer 2:

(ii) Only credit purchases of goods are recorded in purchases book, Cash transaction are shown in cash book. Goods are purchased from M/s. Ambika Mills, Ahmadabad in cash mode. So this transaction not shown in purchases book.

(iii) Since Typewriter is an asset for a firm so it would not be recorded in the purchases book.

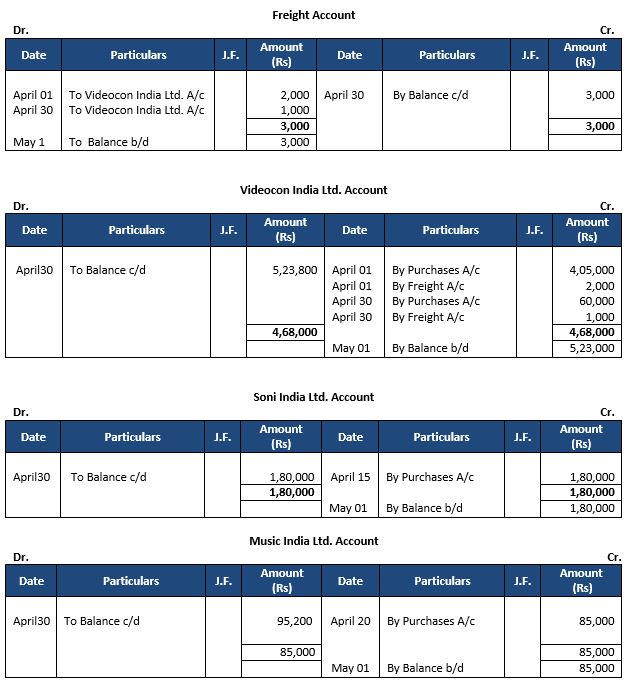

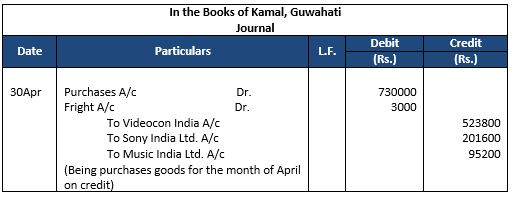

Question 3: From the following information of Kamal, Guwahati, prepare a Purchases Book and post them into Ledger:

Answer 3:

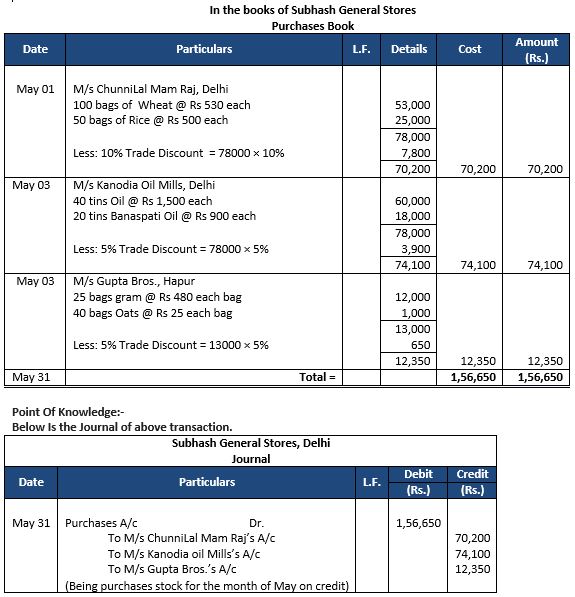

Point of Knowledge:-

Below Is the Journal of above transaction.

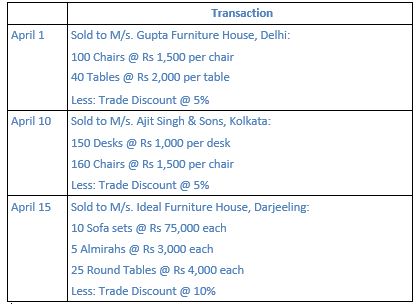

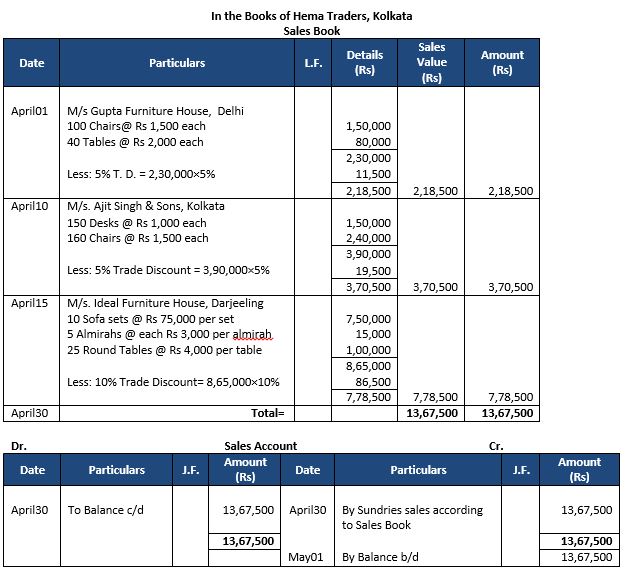

Question 4: Prepare a Sales Book from the following transactions of Mohan Traders dealing in furniture. Open the ledger Account also:

Answer 4:

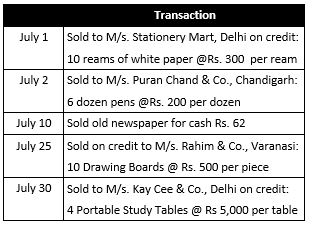

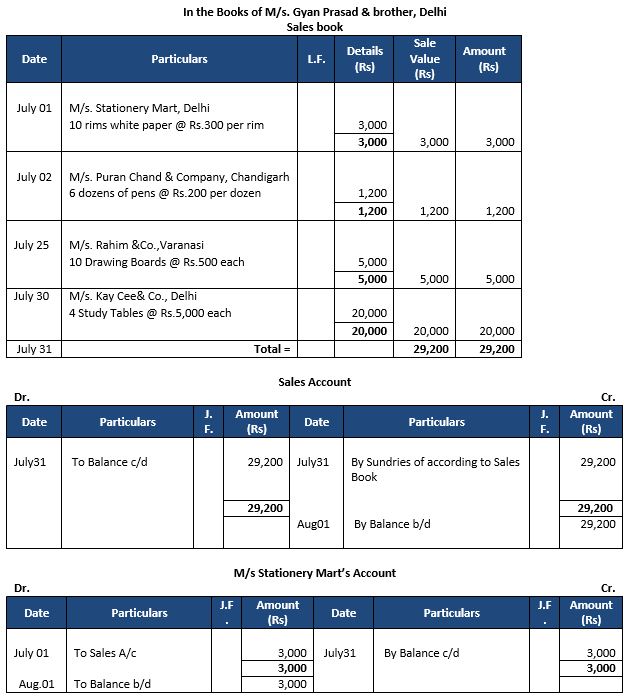

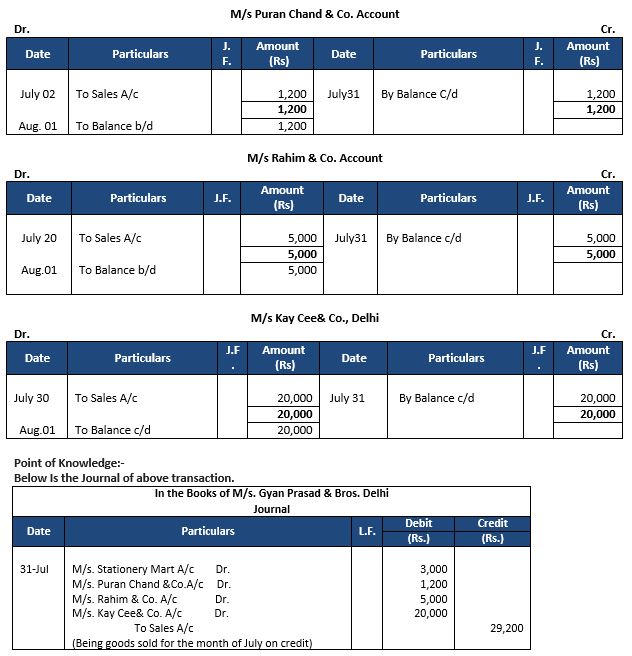

Question 5: From the following particulars, prepare a Sales Book of M/s. Gyan& Bros., Delhi, dealers of stationery and post inLedger Accounts:

Answer 5:

(ii) Since only credit sales of goods are recorded in sales book so sales of news paper was not shown in sales book.

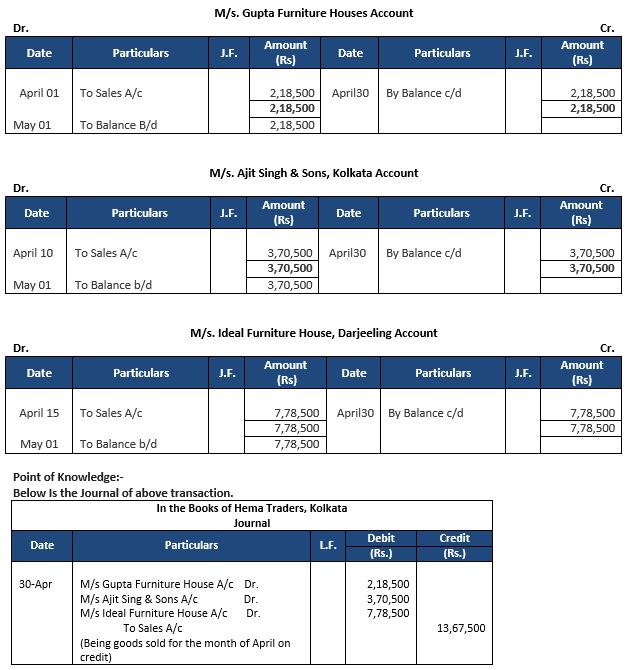

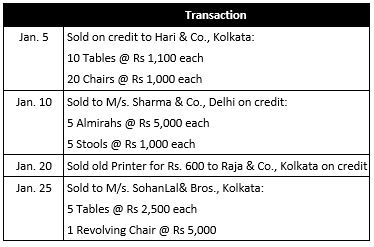

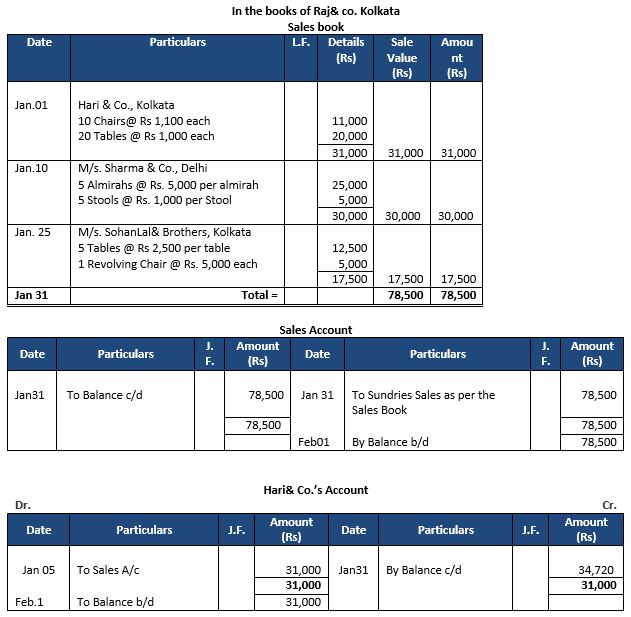

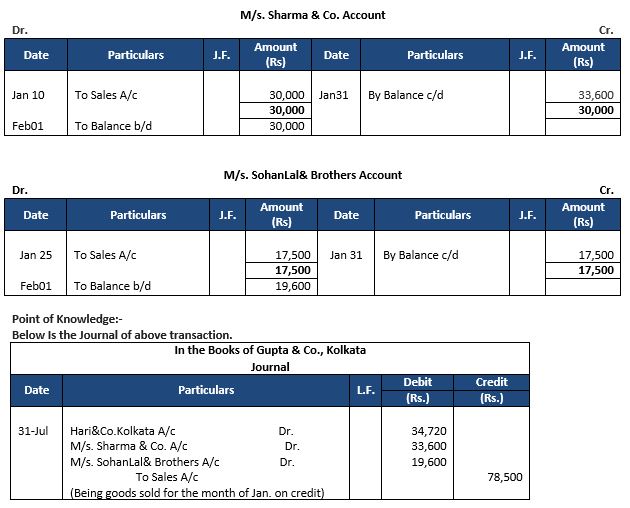

Question 6: From the following particulars, prepare Sales Book of Raj& Co., Kolkata who deals in furniture:

show the Posting from Sales Book to Ledger Accounts.

Answer 6:

(ii) Since only credit sales of goods are recorded in sales book so sales of old typewriter was not shown in sales book.

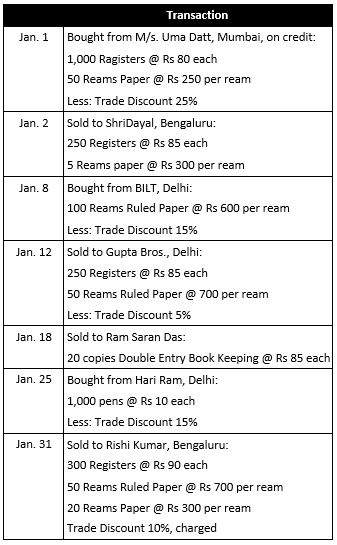

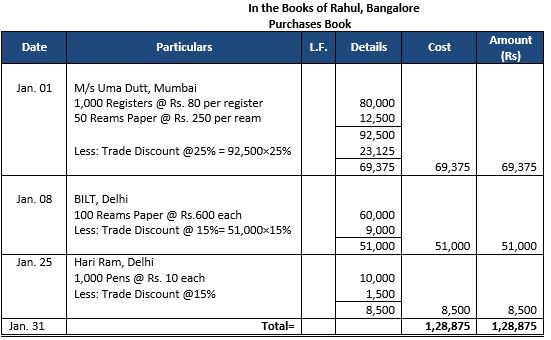

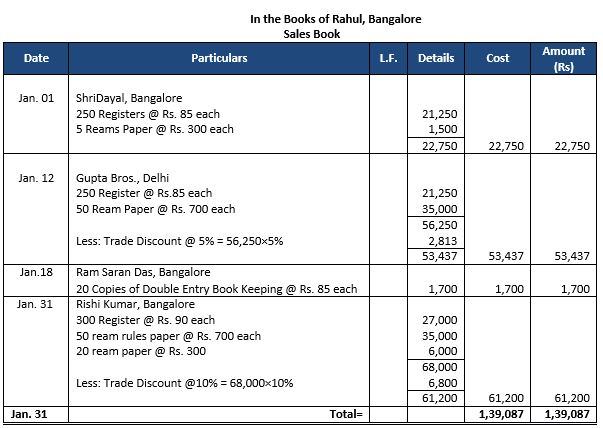

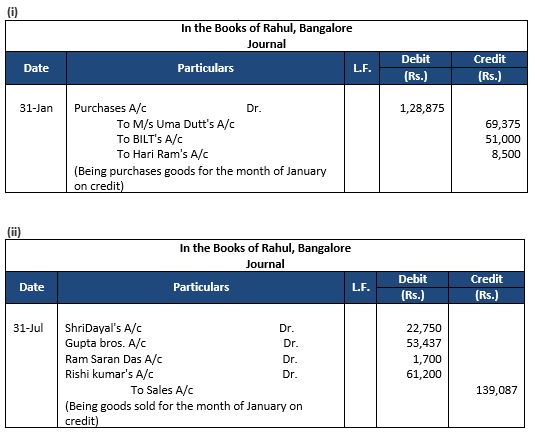

Question 7: Prepare the Purchase Book and Sales Book from the following transactions of Rahul, Bengluru:

Answer 7:

Point of Knowledge:-

Below Is the Journal of above transaction.

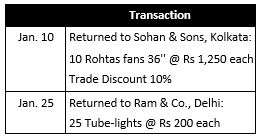

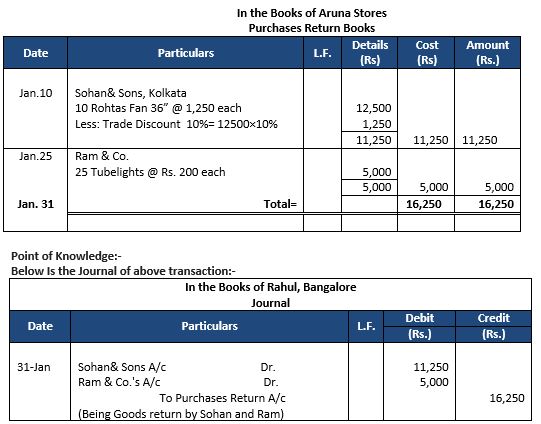

Question 8: Prepare Purchases Return Book of Aruna Stores, Kolkata from the following transactions and post them into Ledger:

Answer 8:

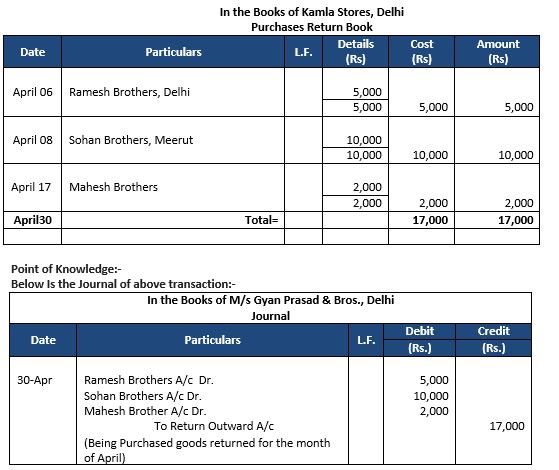

Question 9: Record following transactions in the Purchases Return Book of Kamla Stores for June 2024:

Answer 9:

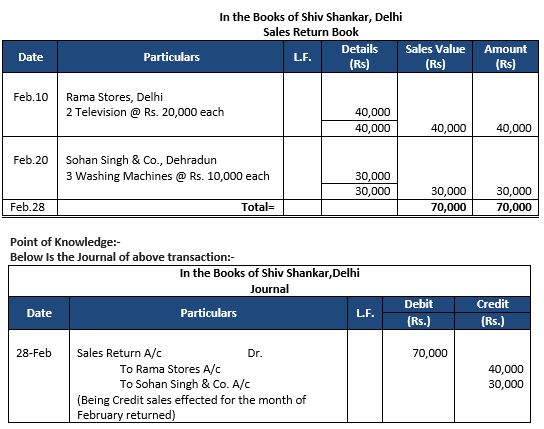

Question 10: Prepare Sales Return Book of Shiv Shankar, Delhi from the following transactions and post them into Ledger:

Answer 10:

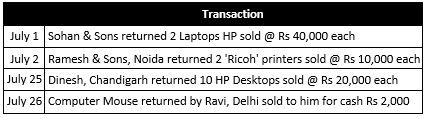

Question 11: Enter following transactions in the Sales Return Books of Raj Computers, Delhi:

Write up the ledger Accounts.

Answer 11:

(ii) Computer mouse are sold in cash mode then we are not considered sales return in sales return book.

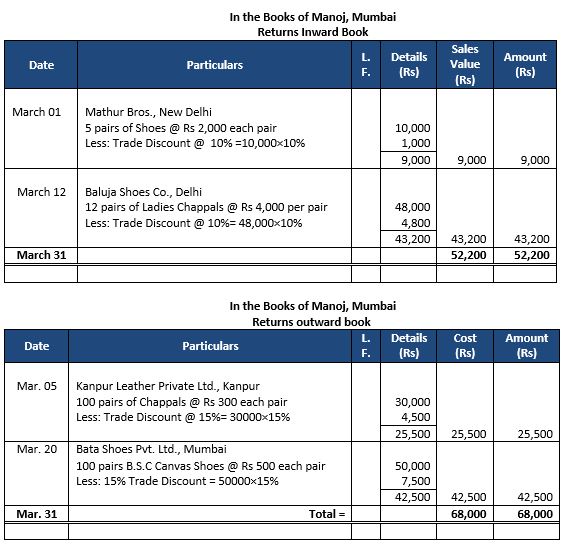

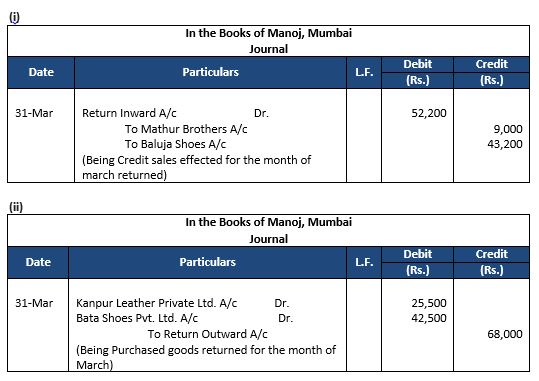

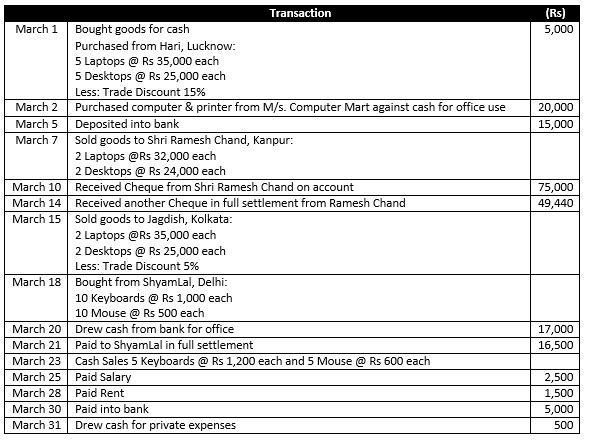

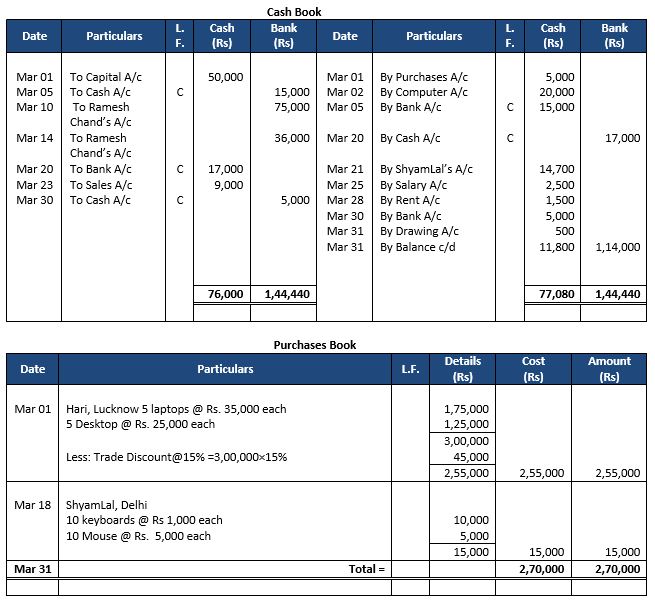

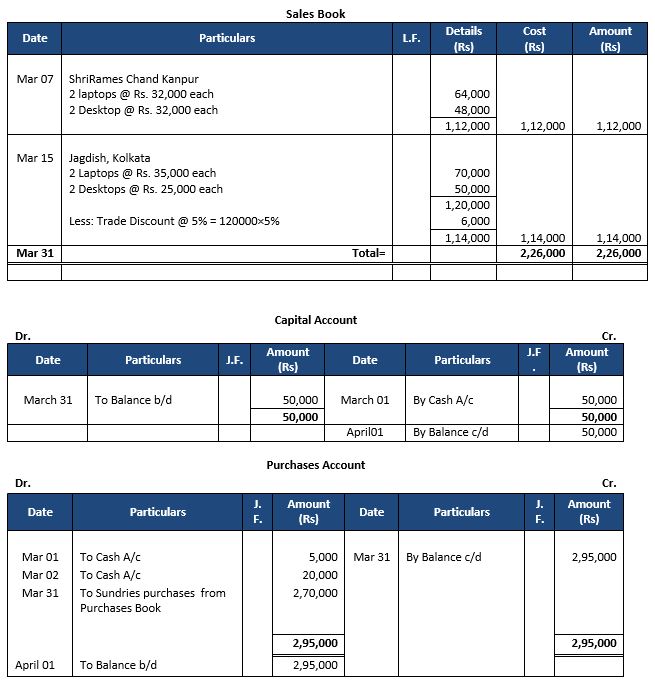

Question 12: Prepare Returns Inward and Return Outward Books of Manoj, Mumbai from the following transactions and post them into Ledger Accounts:

Answer 12:

Point of Knowledge:-

Below Is the Journal of above transaction.

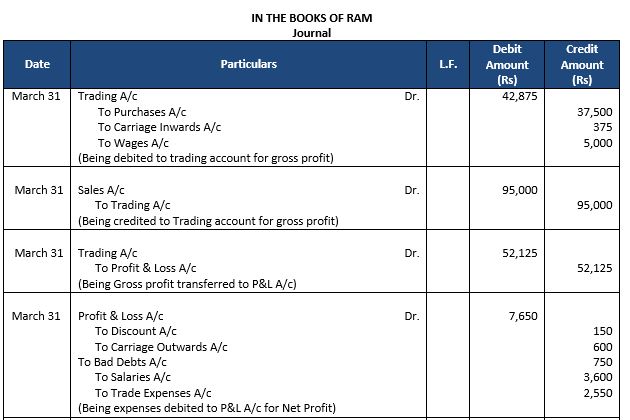

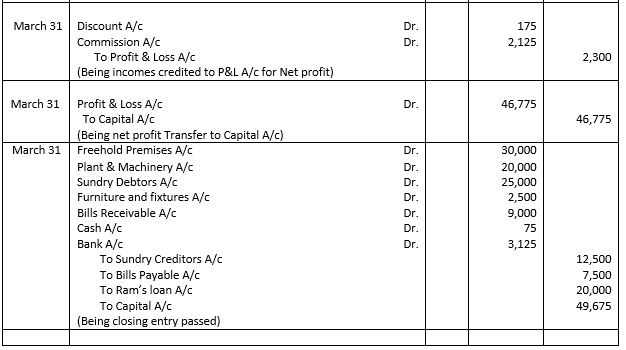

Question 13: (Closing Entries) Give the necessary entries in the Journal Proper of Ram on 31st March, 2024 to close their books:

Freehold Premises Rs 30,000; Plant and Machinery Rs. 20,000; Sundry Debtors Rs 25,000; Purchases Rs 37,500; Sales Rs 95,000; Discount (Dr.) Rs 150; Discount (Cr.)Rs 175; Sundry Creditors Rs. 12,500; Carriage Inwards Rs 375; Carriage Outwards Rs. 600; Furniture and Fixtures Rs. 2,500; Wages Rs 5,000; Bad debts Rs. 750; Salaries Rs. 3,600; Commission (Cr.)Rs 2,125; Capital Account−-Rs 25,000; Bills Payable Rs 7,500; Bills Receivable Rs 9,000; Trade Expenses Rs 2,550; Ram's Loan Account Rs 20,000; Cash in Hand Rs 75; Cash at Bank Rs 3,125.

Answer 13:

Point of Knowledge:-

• At the end of the year Closing entries are passed to close the accounts relating to expenses and revenue by transferring them to the Trading A/c & P&L A/c.

Question 14: (Old Question from previous edition of TS Grewal)

Question 14: (Transfer Entries). Give the Journal entries for the following:

(i) Gross Profit of Rs 32,000 from Trading Account to Profit and Loss Account.

(ii) Net Profit of Rs 14,500 to Capital Account of Sri Sankar Saha.

(iii) Sri Sankar Saha draws Rs 10,000 from his Capital Account.

(iv) Purchases Return of Rs 7,000.

(v) Sales Return of Rs 6,000.

Answer 14:

Point of Knowledge:-

- If an amount is to be Transferred from one account to another, such a transfer is also made through a journal entry only.

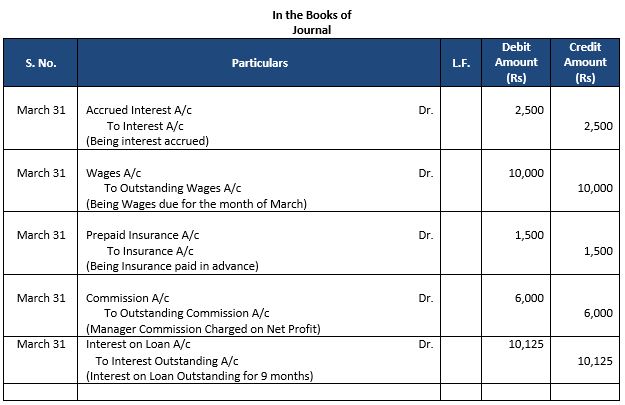

Question 14: (Adjustment Entries) From the following information available on 31st March, 2024, pass the necessary Adjustment Entries in the Journal for the year ending on that date:

(i) Interest accrued Rs 2,500.

(ii) Wages for March, 2024 outstanding Rs 10,000.

(iii) Insurance prepaid Rs 1,500.

(iv) Commission due to Manager 6% on net profit after charging such commission. The profit before charging such commission was Rs 1,06,000.

(v) Interest due on loan but not paid. Loan of Rs 1,50,000 was taken at 9% p.a. 9 months before end of the year.

Answer 14:

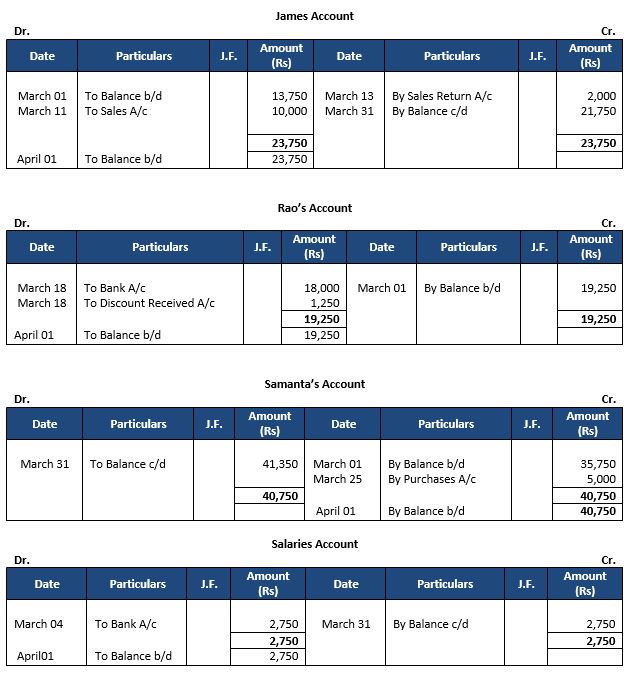

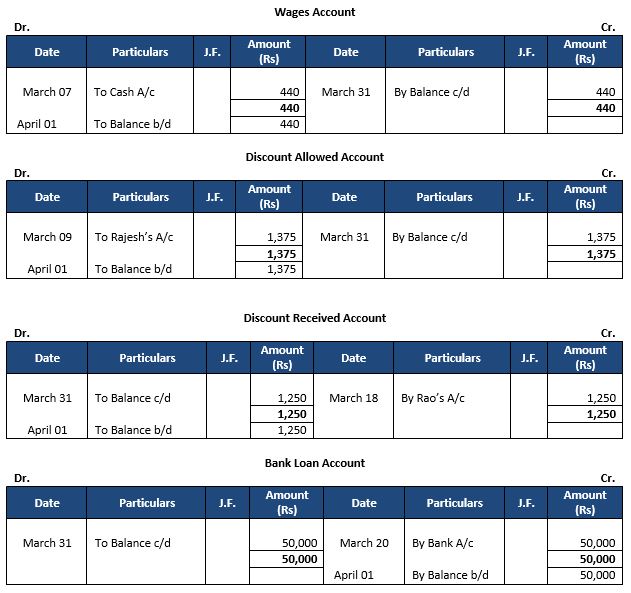

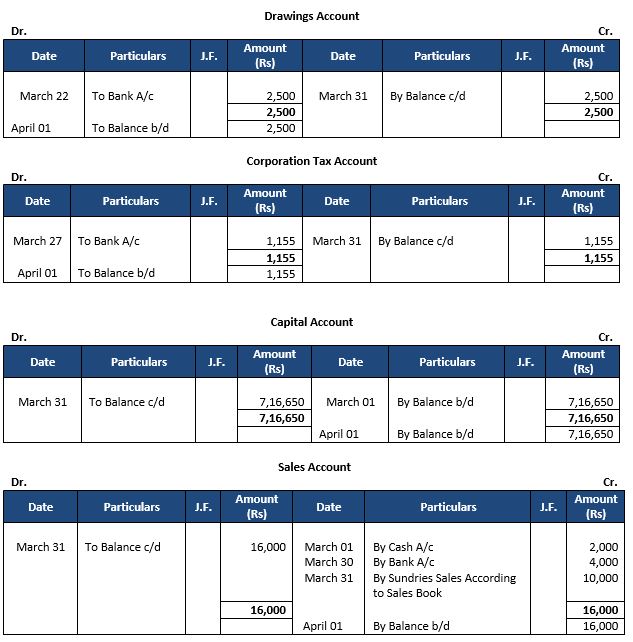

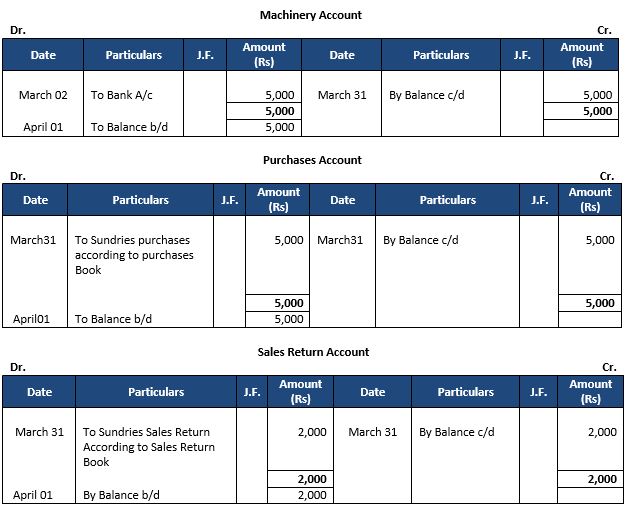

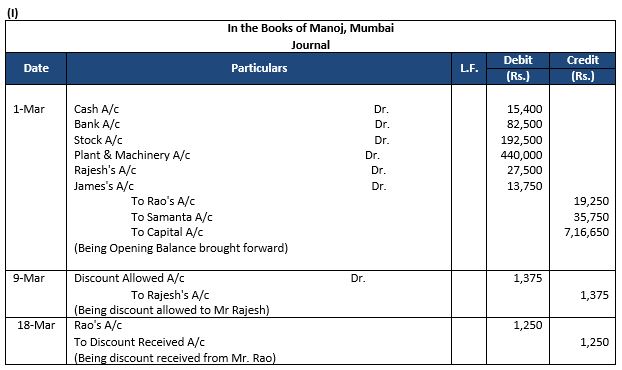

Question 15: R. Chetan has the following balances in his books on 1st March, 2024:

Cash Rs 15,400; Cash at Bank Rs 82,500; Stock Rs 1,92,500; Plant and Machinery Rs 4,40,000.

Sundry Debtors: Rajesh Rs 27,500; James Rs 13,750.

Sundry Creditors: Rao Rs 19,250, Samanta; Rs 35,750; CapitalRs 7,16,650.

The following are the transactions for the month of March 2024:

Record these transactions in his subsidiary books, post to the Ledger and prepare a Trail Balance as on 31st March, 2024.

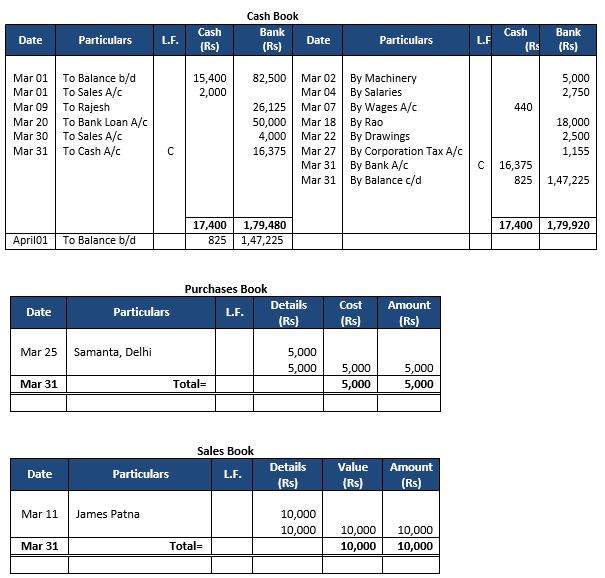

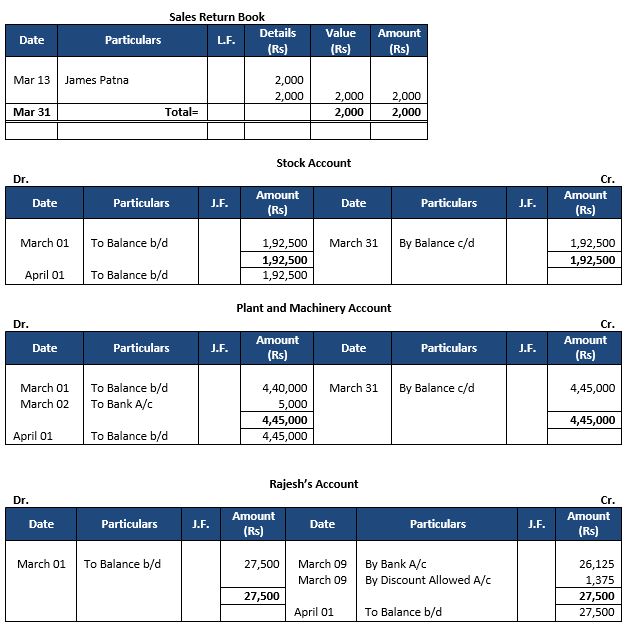

Answer 15:

Point of Knowledge:-

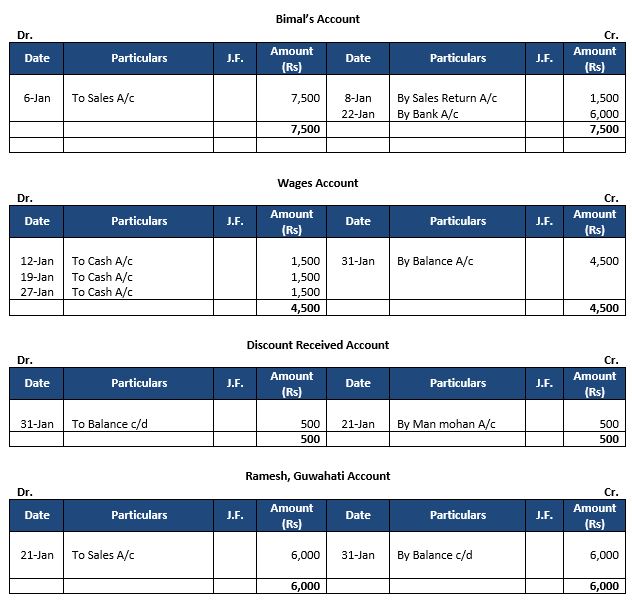

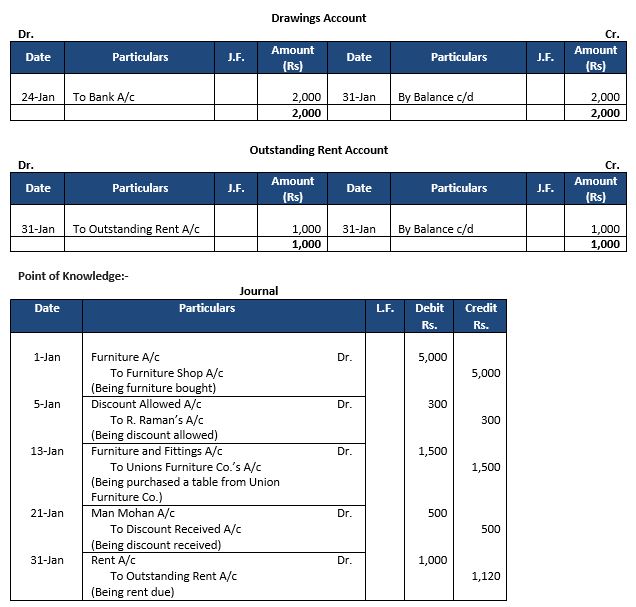

Question 16: Enter the following transactions in Proper Subsidiary Books of Ram, Lucknow (UP) for the month of January 2019: (Old Question)

Answer 16:

Point of Knowledge:-

- In Sales Book Only Credit Sales of Goods are recorded.

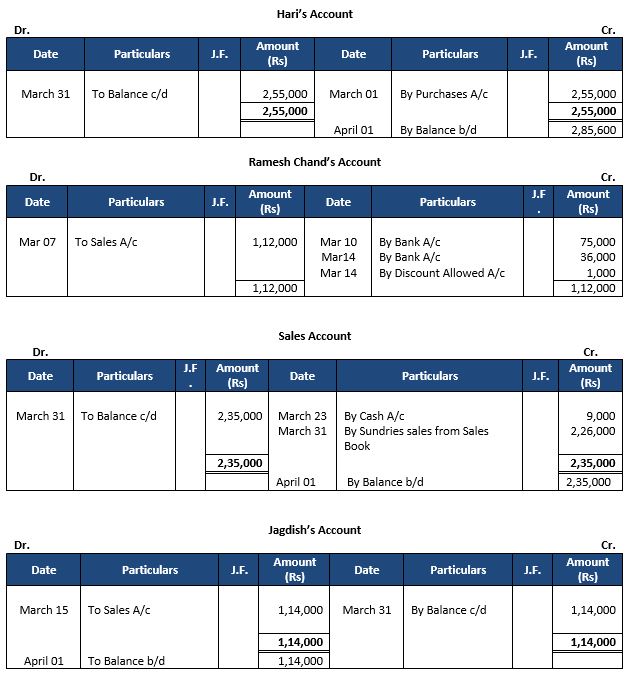

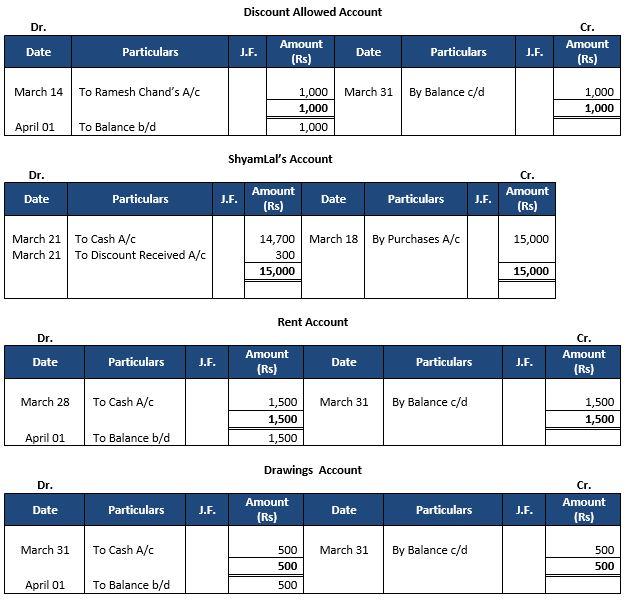

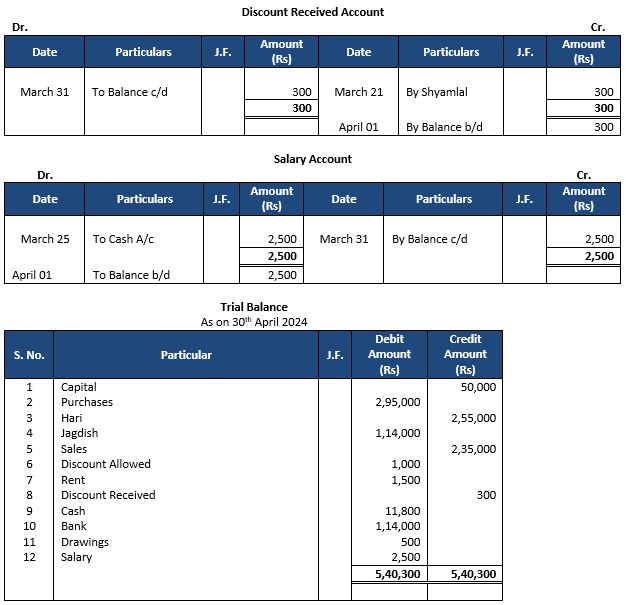

Question 17: On 1st March, 2024, ShriKailash Chand, Lucknow commenced business with cash Rs 50,000. The following are his transactions for the month of March, 2024. Record them in proper books post them to the Ledger and take out a Trial Balance:

Answer 17:

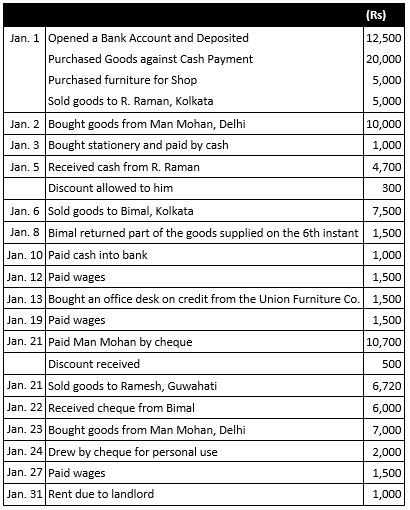

Question 18: On 1st January, 2024, Ram of Kolkata commenced business with a capital of Rs. 50,000 and entered into following transactions:

Pass the following transactions through proper books to the Ledger.

Answer 18:

Question 19: Write up Purchases and Sales Books from the following transactions of Kalyan Silks, Kochi, and Kerala given for April, 2019 and post the totals in the Ledger. (Old Question)

Answer 19:

Point of Knowledge:-

- Cash Purchases & Sales are recorded in Cash Book and Credit Purchases & Credit Sales are shown in Purchases & Sales book respectively.

Question 20: Record the following transactions of Prabhat Electric Co., Delhi in the proper subsidiary books:(Old Question)

Answer 20:

Point of Knowledge:-

- Sum of Purchases & Sales book are posted to the Purchases Account & Sales Account Respectively.

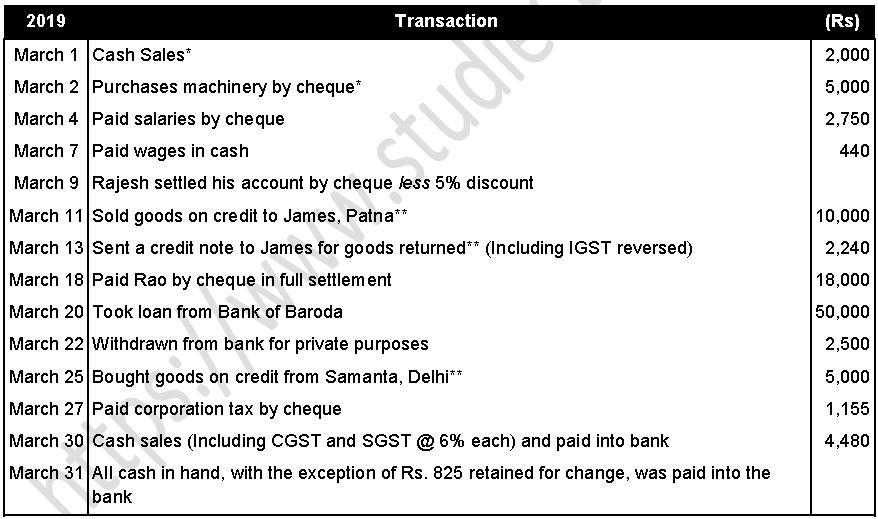

Question 21: R. Chetan has the following balances in his books on 1st March, 2019:

Cash Rs 15,400; Cash at Bank Rs 82,500; Stock Rs 1,92,500; Plant and Machinery Rs 4,40,000.

Sundry Debtors: Rajesh Rs 27,500; James Rs 13,750.

Sundry Creditors: Rao Rs 19,250, Samanta; Rs 35,750; Capital Rs 7,16,650.

The following are the transactions for the month of March 2019:

Transactions marked* are intra-state transactions subject to CGST and SGST @ 6% each. Transactions marked** are inter-state transactions subject to IGST @ 12%

Record these transactions in his subsidiary books, post to the Ledger and prepare a Trail Balance as on 31st March, 2019.

Answer 21:

Question 22: On 1st March, 2019, Shri Kailash Chand, Lucknow commenced business with cash Rs 50,000. The following are his transactions for the month of March, 2019. Record them in proper books post them to the Ledger and take out a Trial Balance:

Transactions marked* are intra-state transactions subject to CGST and SGST @ 6% each.

Transactions marked** are inter-state transactions subject to IGST @ 12%.

Answer 22:

Purchases Book

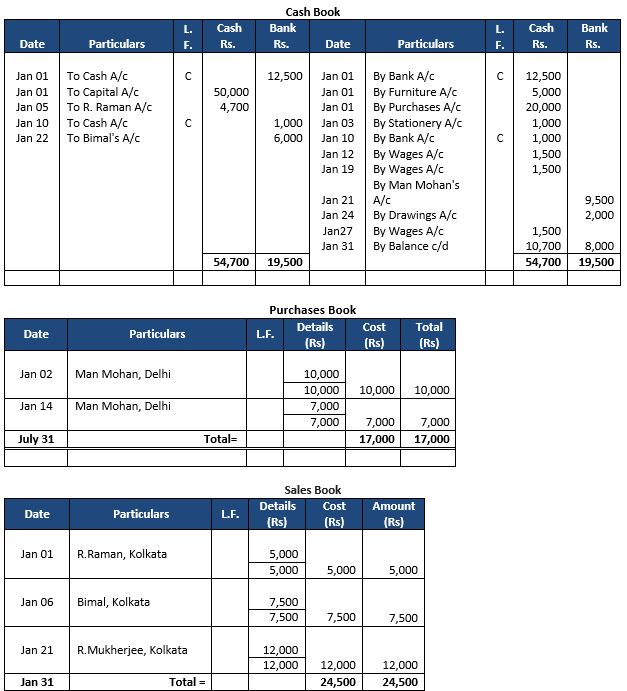

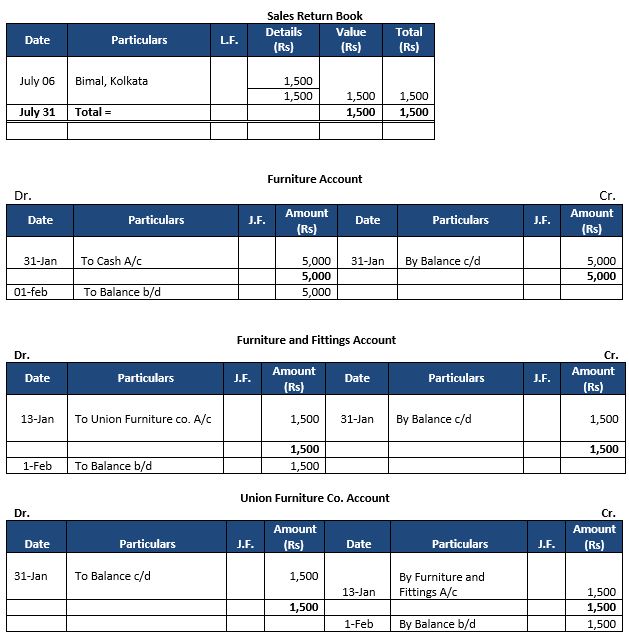

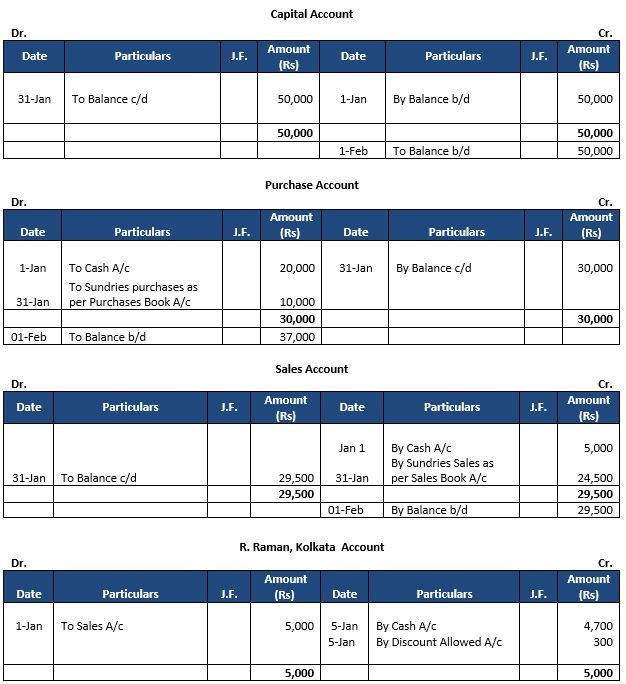

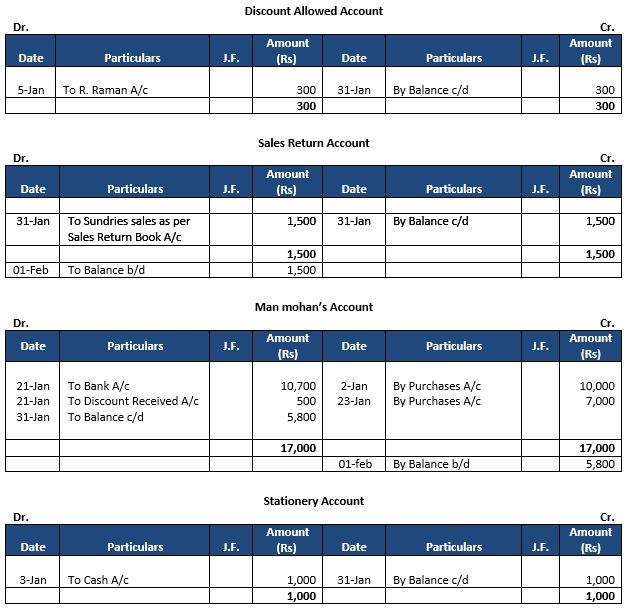

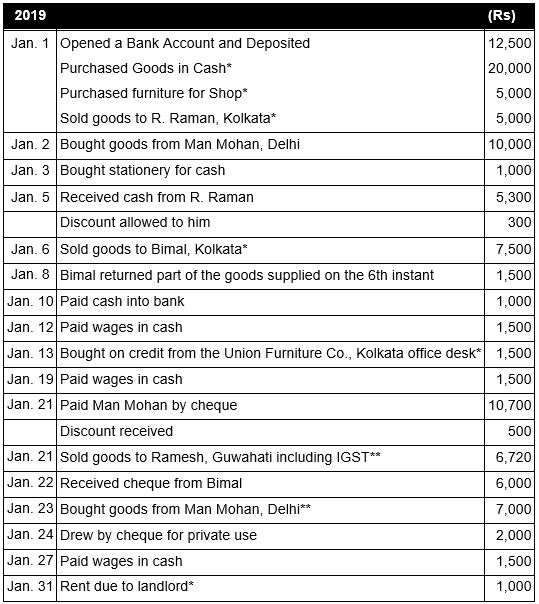

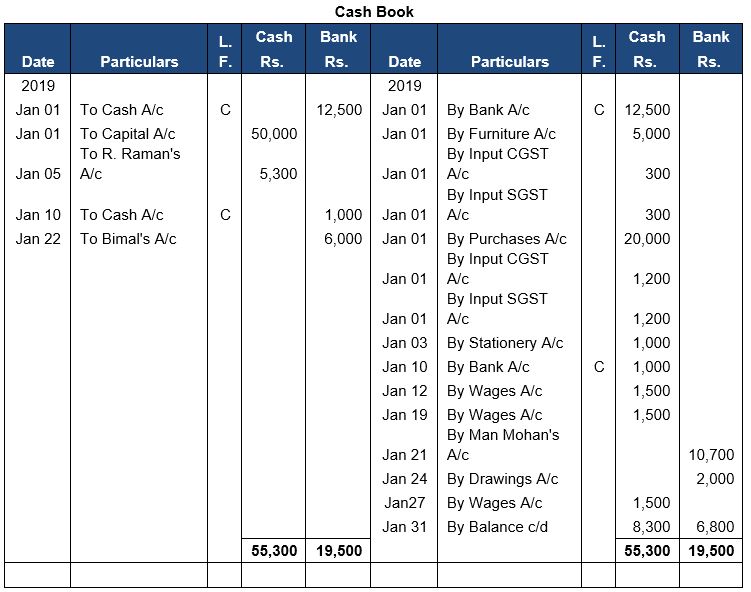

Question 23: On 1st January, 2019, Ram of Kolkata commenced business with a capital of Rs 50,000 and entered into following transactions:

Pass the following transactions through proper books to the Ledger. Take out a Trial Balance as on 31st January, 2019. The Cash Book must be balanced.

Transactions marked* are intra-state transactions subject to CGST and SGST @ 6% each.

Transactions marked** are inter-state transactions subject to IGST @ 12%.

Answer 23:

Point Of Knowledge:-