Read TS Grewal Accountancy Class 11 Solution Chapter 10 Special Purpose Books I Cash Book 2026. Students should study TS Grewal Solutions Class 11 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 11 Accountancy have been prepared by expert teachers. These TS Grewal Class 11 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 11 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 11 Accounts Chapter 10 Special Purpose Books I Cash Book TS Grewal Solutions

TS Grewal Solutions for Chapter 10 Special Purpose Books I Cash Book Class 11 Accounts have been provided below based on the latest TS Grewal Class 11 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 11 will help students to improve their concepts and easily solve accountancy questions for Class 11.

Chapter 10 Special Purpose Books I Cash Book TS Grewal Class 11 Solutions

Question.1. Why is it necessary to sub-divide a Journal? What are its advantages?

Answer 1. It is convenient to maintain a separate book for each such class of transactions-one to record cash transactions, another to record credit purchase of goods and yet another to record credit sale of goods. All of these books are called the books of original entry or primary entry or subsidiary books - it is a special form of Journal, a sub-division of Journal.

Advantages of Subsidiary Books:

(i) Division of Work: Since in the place of one Journal there are many subsidiary books, accounting work can be divided among a number of persons.

(ii) Specialization and Efficiency: When the same work is handled by a particular person for a considerable time, he acquires expertise in it and becomes efficient in handling it. Thus, accounting is done more efficiently.

(iii) Saving of Time: Various accounting processes can be undertaken simultaneously because of the use of number of books. Thus, it leads to saving of time.

(iv) Availability of Information: Since a separate book is maintained for each class of transactions, information relating to each class is available at one place.

(v) Facility in Checking: When the Trial Balance does not agree, location of error or errors is facilitated by the existence of separate books. Since the number of transaction will be considerably less as compared to only one Journal, it would become easy to locate the errors.

(vi) Responsibility: Division of work results in assigning a particular job to a particular person. If an error is committed in recording, responsibility can be easily fixed.

Question.2. What is a Cash Book? What are the types of Cash Book? How is it balanced?

Answer 2. Cash Book is a book of prime entry in which cash and bank transactions are recorded in a chronological order, i.e., as they occur. Cash receipts are recorded on the debit side of the Cash Book and cash payments on the credit side. A balance is struck by deducting the total cash payments from the total cash receipts to know the cash in hand necessary and useful information. The number of cash transactions in a firm is generally large; therefore, it is convenient to have a separate Cash Book to record such transactions.

The following are the types of Cash Books:-

(i) Simple Cash Book or Single Column Cash Book:For recording cash transactions only.

(ii) Two—Column Cash Book (Cash Book with cash and bank columns): For recording cash and bank transactions.

(iii) Three—Column Cash Book (Cash Book with cash, bank and discount columns): In this cash book there are three columns of amount of both the sides. The first for discount, the second for cash and the third for bank transactions. Discount allowed is recorded on the debit side, while discount received is recorded on the credit side.

(iv) Petty Cash Book: Petty Cash Book is the Book which is used for the purpose of recording expenses involving small amounts.

The cash books are balanced like ordinary ledger accounts.

Question.2. Name and describe the various books of original entries.(Old Question)

Answer 2. The following are the names and descriptions of the various books of original entries:

We had discussed earlier that it is practically difficult to record all the transactions in only one book of prime entry. For convenience, the Journal is divided into a number of Subsidiary Books. These are:

1. Cash Book: To record receipt and payments of cash, including receipts into and payments out of the bank.

2. Purchase Book: To record credit purchases of goods dealt in by the firm. All credit purchases of goods are recorded in this book.

3. Sales Book: To record the credit sales of goods dealt in by the firm.

4. Purchases Return Book: To record the return of goods previously purchased on credit.

5. Sales Return Book: To record the return of credit sales made by customers.

6. Bills Receivable Book: To record the receipt of promissory notes or bills drawn by firm and accepted by debtors.

7. Bills Payable Book: To record the issue of promissory notes and bills accepted by the firm.

8. Journal Proper: To record the transactions which cannot be recorded in any of the seven books mentioned above.

It may be noted that in all the above cases the word 'Journal' may be used for the word 'book'.

Question.3. “Cash Book always shows a debit balance.” How far is this statement true and why?

Answer 3. Cash book cannot have a Credit Balance or Cash Book always shows a debit balance. Cash Column in the Cash Book cannot show a credit balance because cash payments cannot exceed cash receipts. At best, it can show nil balance when total cash receipt are equal to total payment.

Question.4. What is a Contra Entry? How is it recorded? Give two examples of a Contra Entry.

Answer 4. Contra Entry: Some transactions are recorded in a Two-Column Cash Book which relate to both cash and bank, i.e., balance of one will decrease and the other will increase due to such transactions. Such transactions are entered on both sides of the Cash Book. Such entries are knows as Contra Entries. Let us take an example to understand it better.

(a) Cash deposited into the Bank 10,000: In this transaction, Bank Account is to be debited and Cash Account is to be credited. Debit aspect is recorded on the debit side of the Bank Column and credit aspect is recorded on the credit side of Cash Column.

(b) Cash withdrawn from Bank for Office Use 1,000: In this transaction Cash Account is to be debited and Bank Account is credited. Debit aspect is recorded on the debit side of the Double Column Cash Book in the Cash Column and credit aspect is recorded on the credit side of the Double Column Cash Book in the Bank Column.

Against such entries, the letter 'C' is written in the L.F. column to indicate that these are contra transactions and are not posted into the Ledger Account.

Question.5. State reasons for the following:

(i) The balance in the cash column of the Cash Book is always a debit balance whereas that in the bank column can sometimes is credit.

(ii) Contra entries in the Two-Column Cash Book are not posted into the ledger.

(iii) The Cash Account and the Bank Account are not posted in the Ledger.

Answer 5. The reasons for the following are:

(i) The balance in the cash column of the Cash Book is always a debit balance whereas that in th bank column can sometimes be credit. Cash Column in the Cash Book cannot show a credit balance because cash payments cannot exceed cash receipts. At best, it can show nil balance when total cash receipts are equal to total payments. Whereas in the bank column we can pay more than what we have in the bank due to overdraft arrangements with the bank and in that case the bank column will so a credit balance.

(ii) Contra entries in the Two-Column Cash Book are not posted into the Ledger. Some transactions are recorded in a Two-Column Cash Book which relate to both cash and bank, i.e., balance of one will decrease and the other will increase due to such transactions. Such transactions are entered on both sides of the Cash Book. Such entries are knows as Contra Entries. Against such entries, the letter 'C' is written in the L.F. column to indicate that these are contra transactions and are not posted into the Ledger Account as the Cash Book is a combination of Cash Ledger and Bank Ledger.

(iii) The Cash Account and the Bank Account are not posted in the ledger. Some transactions are recorded in Two-Column Cash Book which relate to both cash and bank, i.e., balance of one will decrease and the other will increase due to such transactions. Such transactions are entered on both sides of the Cash Book. Such entries are knows as Contra Entries. Against such entries, the letter 'C' is written in the L.F. column to indicate that these are contra transactions and are not posted into the Ledger Account as the Cash Book is a combination of Cash Ledger or Account and Bank Ledger or Account.

Question.6. What is a Petty Cash Book? Why is it maintained?

Answer 6. Petty Cash Book is the book which is used for the purpose of recording expenses involving petty amounts. Besides petty expenses, receipts from main cash are recorded. Petty Cash Book is prepared by Petty Cashier and acts as the Petty Cash Account. It is maintained as in a business besides large payments, number of small payments, such as for conveyance, stationary, cartage, etc., have to be made. If all these payments are recorded in the Cash Book, it will become unnecessarily large. Also, the main cashier will be overburdened with work. Therefore, it is usually for firms to appoint a person as 'Petty Cashier' and to entrust the task of making small payments, say, below 250, to him. Of course, he is reimbursed for the payments made. The respective accounts are debited.

Question.7. Explain the meaning of Imprest System of Petty Cash Book.

Answer 7. The imprest system of Petty Cash is explained below. Under this system, an estimate is made of amount required for petty expenses for a certain period (say for a week, a fortnight or a month). The amount so ascertained is given to the petty cashier in the beginning of a period and is reimbursed the amount paid by him during the period. Thus, he will again have the fixed amount in the beginning of the new period. This amount is called imprest money. This system of paying advance in the beginning and reimbursing the amount spent from time to time is called imprest system.

Question.8. Explain the method of posting a Petty Cash Book.(Old Question)

Answer 8. The expiation of the method of posting a Petty Cash Book is explained below as: Petty cash given to the Petty Cashier for small payments is recorded on the credit side of the Cash Book as 'By Petty Cash Account' and is posted to the debit side of the Petty Cash Account in the Ledger. All payments are recorded in the particulars column as 'By Particular Petty Expenses Account' and the amount is posted in the total column along with individual Petty Expenses column.

Practical Problems :---->

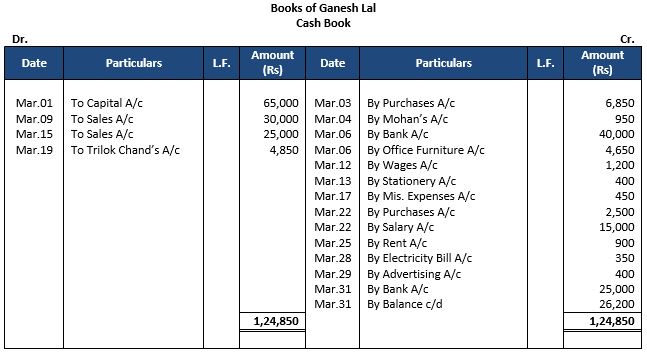

Question 1: Enter the following transactions of Mr. Ripinder, Delhi in a Single Column Cash Book and balance it:

Answer 1:

Format of Single Column Cash Book on the basis of given transactions

Point of Knowledge:-

(i) In the cash book only cash transaction are recorded. Credit transactions are not recorded.

(ii) The debit side is always greater than the credit as payments are never exceeds the cash available.

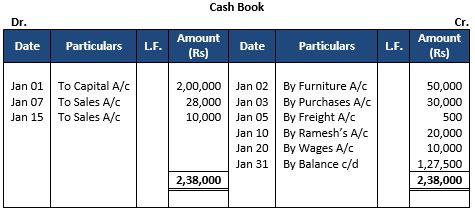

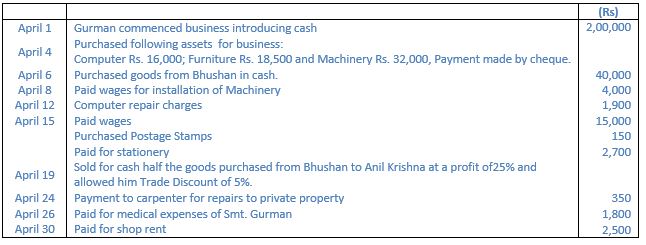

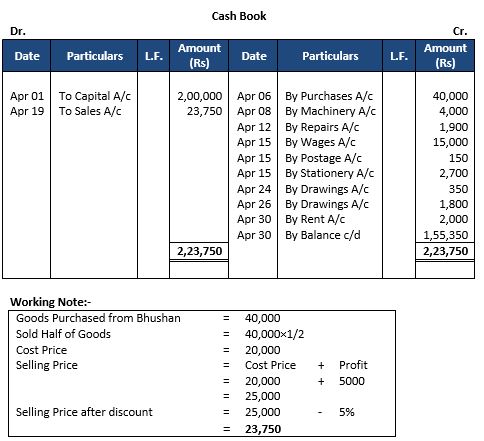

Question 2: Prepare Simple Cash book of Gurman of Amritsar from the following transactions:

Answer 2:

Format of Simple Cash Book on the basis of given transactions

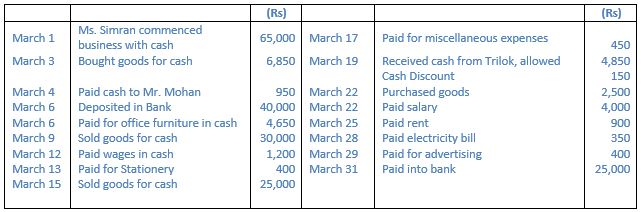

Question 3: Prepare Simple Cash Book from the following transactions of Simran, Delhi:

Answer 3:

Format of Simple Cash Book on the basis of given transactions

Point of Knowledge:-

(i) If a firm maintained Cash Book then it need not to make cash account separately.

Question 4: From the following prepare Single Column Cash Book of Suresh, Chennai and post them into ledger accounts:

Answer 4:

Format of Single Column Cash Book on the basis of given transactions

Point of Knowledge:-

(i) Cash book is maintained to record only cash transaction so, the credit purchases are not recorded in the cash book.

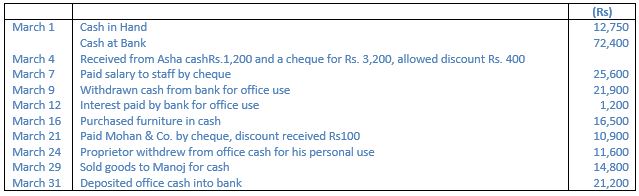

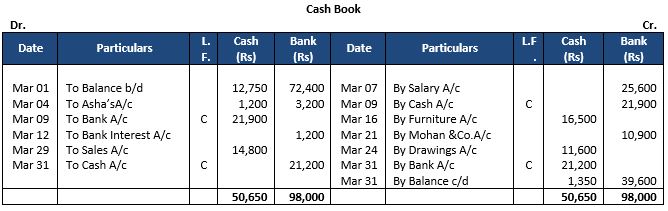

Question 5: Record the following transactions in Double Columns Cash Book and balance the book on 31st March, 2024:

Answer 5:

Format of Double Column Cash Book on the basis of given transactions

Point of Knowledge:-

(1) Contra Entry is an entry which includes both Cash & Bank Account and it is recorded in both debit & credit side of the double column cash book. When a contra entry posted in cash book there is a reference column, the letter “C” is written this denotes that the entry is a contra entry.

(2) This entry will not be posted to any ledger account.

Question 6: Prepare Two-column Cash Book of Bimal, Lucknow from the following transactions:

Answer 6:

Format of Two Column Cash Book on the basis of given transactions

Point of knowledge:-

(i) When a cheque is received and deposited into the bank on the same day the amount of the cheque is entered in the bank column on debit side.

(ii) When a cheque is received and does not represent on the same day, the amount of the cheque is entered in the cash column.

Question 7: Prepare Two-column Cash Book from the following transactions of Mani, Kochi;

Answer 7:

Format of Two Column Cash Book on the basis of given transactions

Question 8: Prepare Two-column Cash Book of Vinod, Delhi from the following transactions:

Answer 8:

Point of Knowledge:-

(i) The contra entry is done when the cash is withdrawn for business use. If cash is withdrawn for personal use, it will be entered in the bank column of credit side of the cash book.

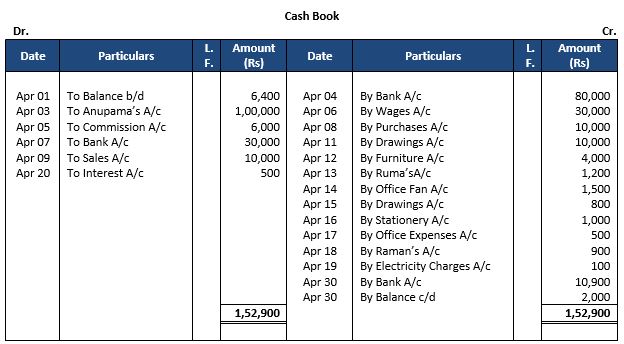

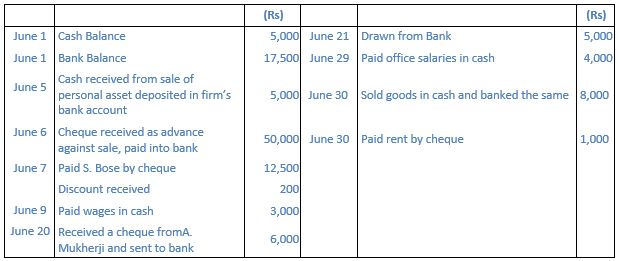

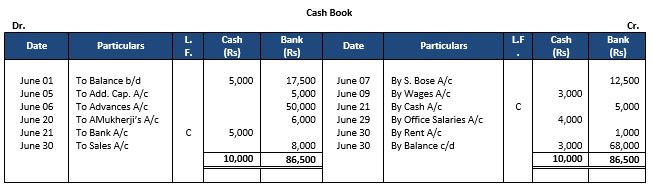

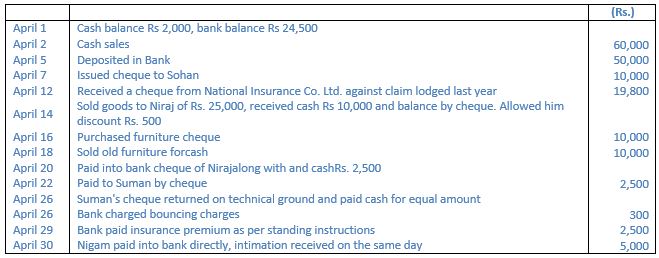

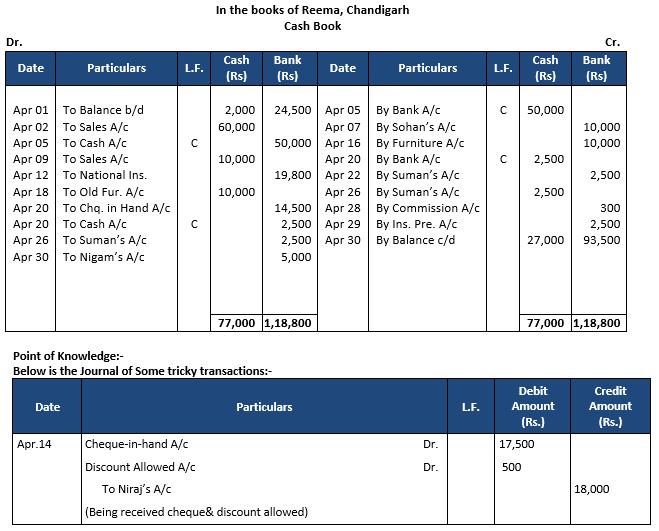

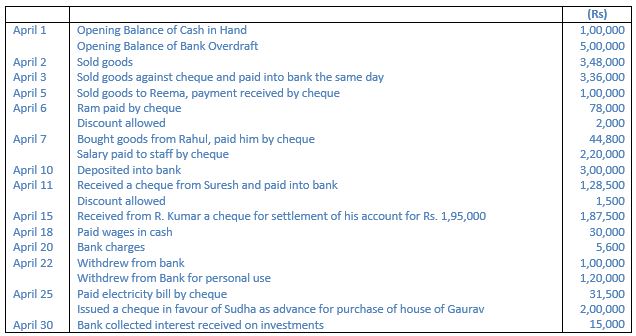

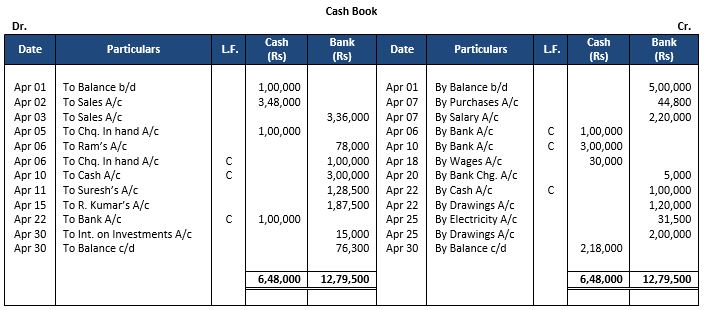

Question 9: Enter the following transactions in Two-column Cash Book of Reema, Chandigarh and find out cash and bank balances:

Answer 9:

Format of Two Column Cash Book on the basis of given transactions:

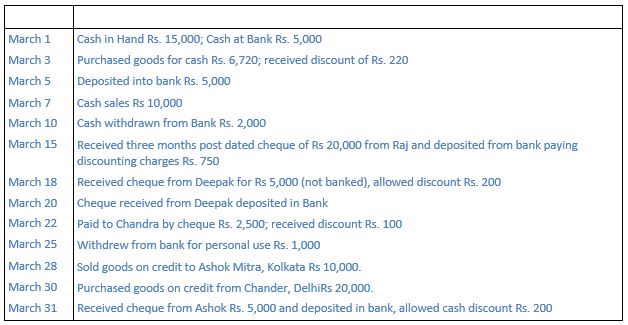

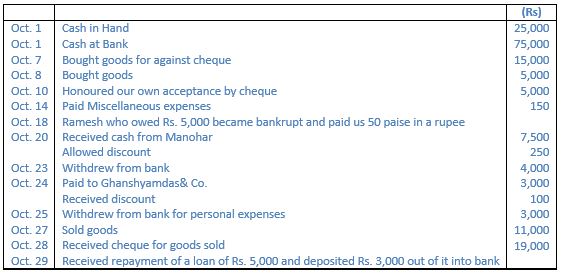

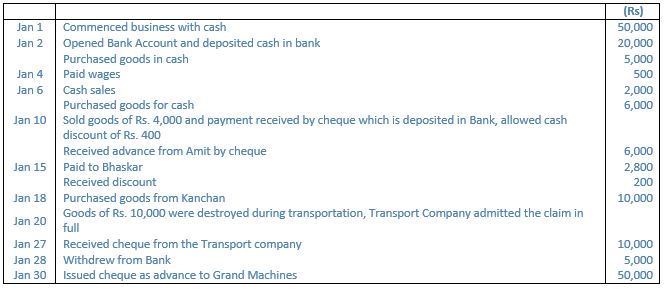

Question 10: Write the following transactions in the Cash Book of Premium Stores, Kolkata (Proprietor Amrit Kumar):

Answer 10:

Format of Two Column Cash Book on the basis of given transactions

Question 11: Enter the following transactions in Two-column Cash Book of Gaurav, Delhi:

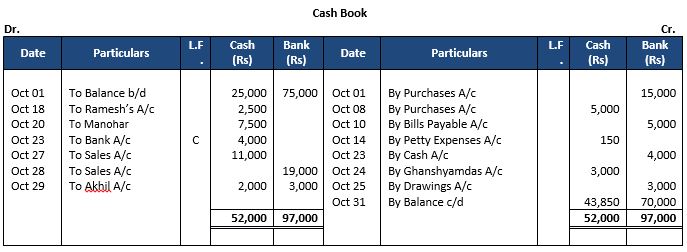

Answer 11:

Format of Two Column Cash Book on the basis of given transactions

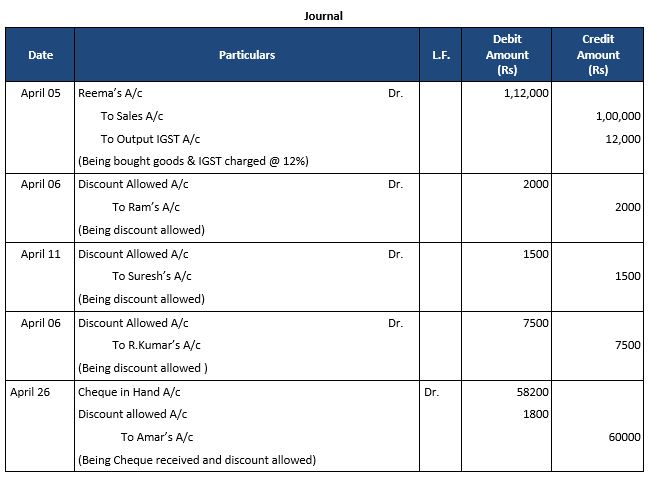

Point of Knowledge:-

(i) Below is the Journal of Some tricky transactions

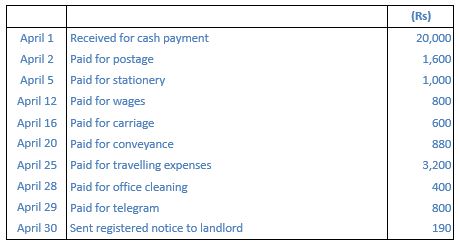

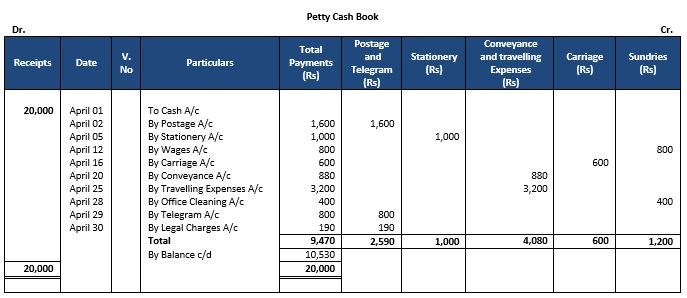

Question 12: From the following information, prepare an Analytical Petty Cash Book:

Answer 12:

Format of Analytical Petty Cash Book on the basis of given transactions

Question 13: Rajan maintains a Columnar Petty Cash Book on the Imprest System. The imprest amount is Rs 5,000. From the following information, show how his Petty Cash Book would appear for the week ended 12th September, 2023:

Answer 13:

Format of Columnar Petty Cash Book on the basis of given transactions

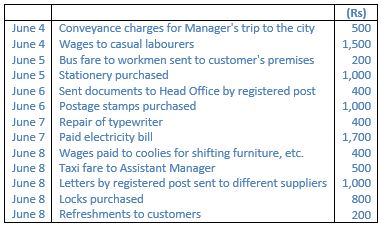

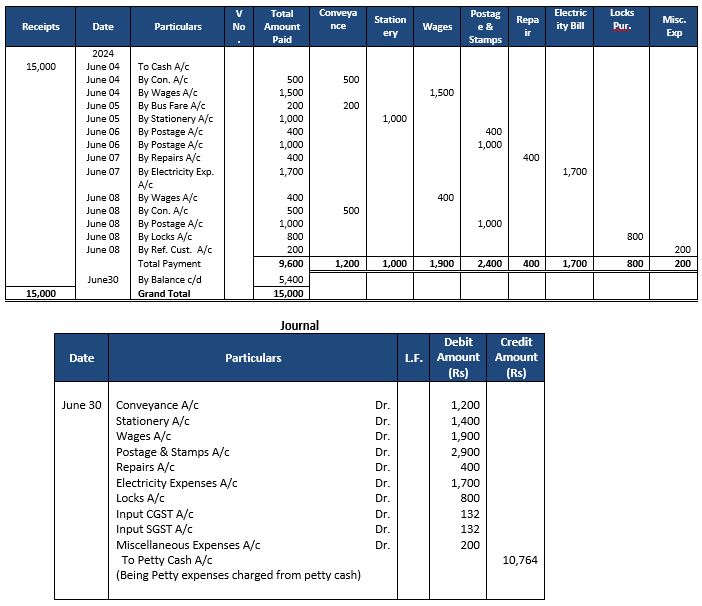

Question 14: A Petty Cashier in a firm received Rs.15,000 as the petty cash imprest on 4th June, 2024. During the week, his expenses were as follows:

Write up the Analytical Petty Cash Book and draft the necessary Journal entries for the payments made.

Answer 14:

Format of Analytical Petty Cash Book on the basis of given transactions:

Point of Knowledge:-

Advantages of Petty Cash Book:-

(i) Time Saving Activity.

(ii) Provides Control on Small payments.

(iii) Saving the labour to writing up the posting into the ledger.

Question 15: (Old Question from previous edition of TS Grewal)

Question 15: From the following information, prepare an Analytical Petty Cash Book:

Answer 15:

Question 16: (Old Question from previous edition of TS Grewal)

Question 16: The following transactions took place during the week ended 28th May, 2019. How will you record them in the Petty Cash Book which was maintained with a weekly 'float' of ₹ 3,000?

Answer 16:

Question 17: (Old Question from previous edition of TS Grewal)

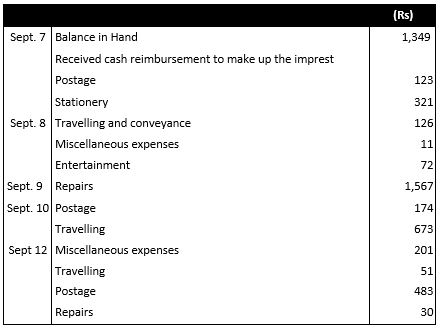

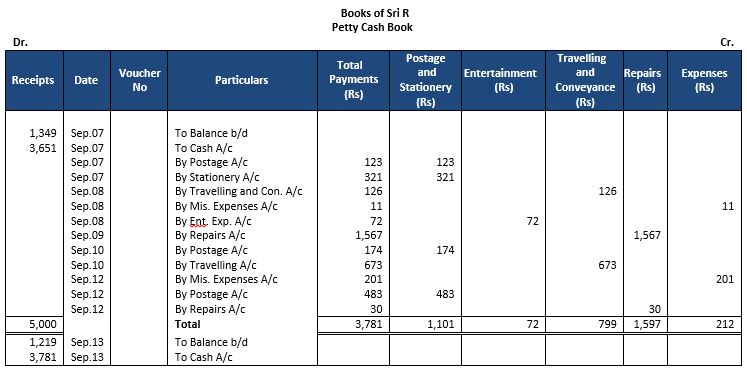

Question 17: Sri R maintains a Columnar Petty Cash Book on the Imprest System. The imprest amount is Rs 5,000. From the following information, show how his Petty Cash Book would appear for the week ended 12th September, 2017:

Answer 17:

Question 18: (Old Question from previous edition of TS Grewal)

Question 18: With Goods and Services Tax (GST)

A Petty Cashier in a firm received ₹15,000 as the petty cash imprest on 4th June, 2017. During the week, his expenses were as follows:

Write up the Analytical Petty Cash Book and draft the necessary Journal entries for the payments made.

Answer 18:

Format of Analytical Petty Cash Book on the basis of given transactions:

Point of Knowledge:- Advantages of Petty Cash Book.

(i) Time Saving Activity.

(ii) Provides Control on Small payments.

(iii) Saving the labour to writing up the posting into the ledger.