Read TS Grewal Accountancy Class 11 Solution Chapter 9 Ledger 2026. Students should study TS Grewal Solutions Class 11 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 11 Accountancy have been prepared by expert teachers. These TS Grewal Class 11 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 11 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 11 Accounts Chapter 9 Ledger TS Grewal Solutions

TS Grewal Solutions for Chapter 9 Ledger Class 11 Accounts have been provided below based on the latest TS Grewal Class 11 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 11 will help students to improve their concepts and easily solve accountancy questions for Class 11.

Chapter 9 Ledger TS Grewal Class 11 Solutions

Question.1. What is a Ledger?

Answer.1 Meaning of a Ledger:

Earlier, we discussed the term Account. In an account, transactions of one nature are posted or summarized. All the accounts put together constitute a 'Ledger'. A Ledger may be defined as a "book or register which contains, in a summarized and classified form, a permanent record of all transactions." It is the most important book of accounts, since, the Trial Balance is drawn from it and from the Trial Balance, and Financial Statements are prepared. Hence, the Ledger is called the Principal Book.

Question.2. What do you mean by posting?

Answer.2 Posting or posting the Entries means:

The process of transferring the information contained in a Journal to a Ledger is called Posting.

The following procedure is followed for posting the debit and credit aspects of the transaction recorded in a Journal:

A. Posting of Account debited in a Journal entry: The steps to be followed are:

1. Identify in the Ledger the account to be debited.

2. Enter the date of the transaction in the 'Date' column on the debit side of the account.

3. Write the name of the account which has been credited in the respective entry in the 'Particulars' column on the debit side of the amount as 'To (name of account credited)'.

4. Record the page number of the Journal where the entry exists in the Journal folio (J,F.) column.

5. Enter the relevant amount in the 'Amount' column on the debit side.

B. Posting an Account credited in a Journal entry: The steps to be followed are:

1. Identify in the Ledger the account to be credited.

2. Enter the date of the transaction in the 'Date' column on the credit side of the account.

3. Write the name of the account which has been debited in the respective entry in the 'Particulars' column on the credit side of the account as 'By (name of account debited)'.

4. Record the page number of the Journal where the entry exists in the Journal folio (J.F.) column.

5. Enter the relevant amount in the 'Amount' column on the credit side.

Question.3. What is an Account?

Answer.3 An account is a record of transaction, both cash and credit under a particular head of account like wages, rent, sales, etc., or a particular head like asset, liability, etc. It only shows the amount of transaction but also shows their effect and direction.

Question.4. What are the two sides of an account called?

Answer.4 The two sides of accounts are called debit side and credit side. The left hand side of the ledger account is debit side and the right hand side is credit side.

Question.5. Write a short note on ‘balancing an account’. Explain by balancing a Cash Account.

Answer.5 An Account is balanced like we have to add the bigger side either debit or credit whichever may be and write down the bigger one in the parallel column. The debit column if bigger than the credit column. The difference is written on the credit side as 'By Balance c/d'. The totals are then entered in the two columns opposite one another and then on the debit side, the balance is written as 'To Balance b/d' to show the debit balance in hand in the beginning of the next period or vice versa for the credit balance.

Balancing of Cash Account:

A Cash Account is balanced like any other account. The debit column is always bigger than the credit column. The difference is written on the credit side as 'By Balance c/d'. The totals are then entered in the two columns opposite one another and then on the debit side, the balance is written as 'To Balance b/d' to show the cash balance in hand in the beginning of the next period.

Cash Account cannot have a Credit Balance:

Cash Account cannot show a credit balance because cash payments cannot exceed cash receipts. At best, it can show nil balance when total cash receipts are equal to total payments.

Question.6. What is the object of preparing an account?

Answer.6 The objects of preparing an account are:

1.) To record transactions of a particular head.

2.) To record the amount of a particular transaction.

3.) The record the effect of a transaction.

4.) To record the direction of transaction.

Question.7 Give a specimen of an account.

Answer.7

Question.8 Distinguish between Journal and Ledger?

Answer.8

Question.9. What is a Trial Balance?

Answer.9 Meaning of Trial Balance:

After posting the transactions in the accounts and balancing them, a statement is prepared to show separately the debit and credit balances. Such a statement is known as Trial Balance. The total of the debit side of Trial Balance must be equal to that of its credit side. This is based on the principle that in double entry system, for every debit there must be a corresponding credit. The agreement of Trial Balance indicates arithmetic accuracy of the accounting work. If the two sides do not agree, there is definitely some error or errors. It must be remembered that equalizing the two sides of a Trial Balance is not the sole and conclusive proof of the complete correctness of accounting work.

Practical Problems :------->

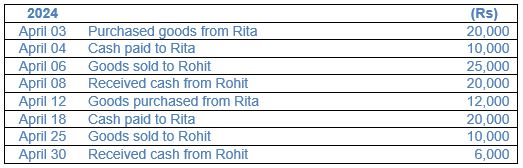

Question 1: On 1st April, 2024, Gopal started business with a capital of Rs. 50,000. He made the following transactions during the month of April:

Journalize the above transactions and show the respective Ledger accounts.

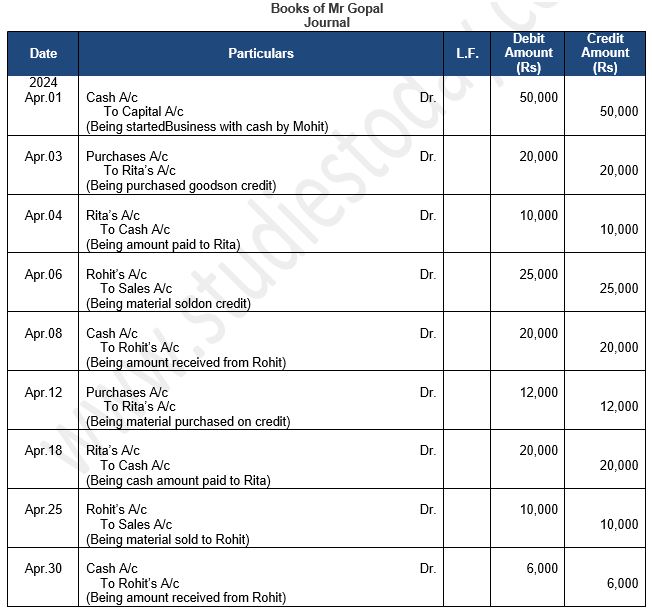

Answer 1:

Statement showing Journal of Gopal

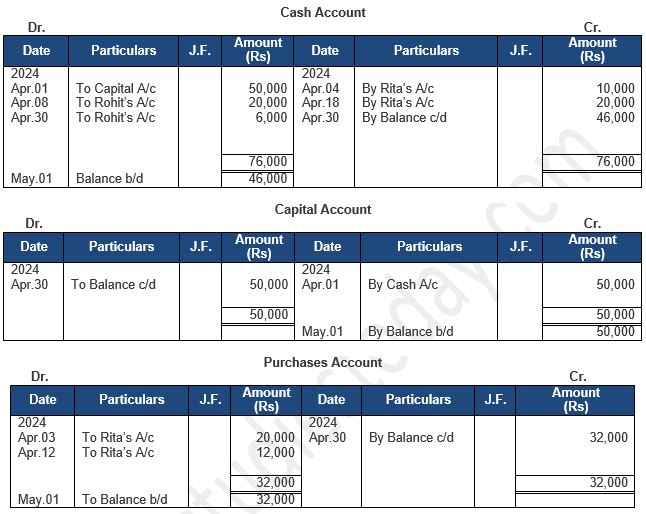

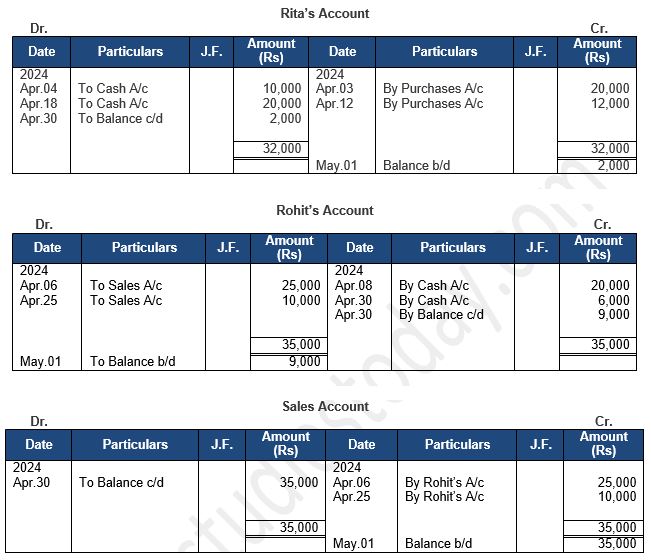

Following are the ledgers shown in the books of Gopal

Point of Knowledge:-

(1) If the debit side total is more than the credit side total write the difference on the credit side as “By Balance c/d”.

(2) If the credit side total is more than the debit side total write the difference on the credit side as “To Balance c/d”.

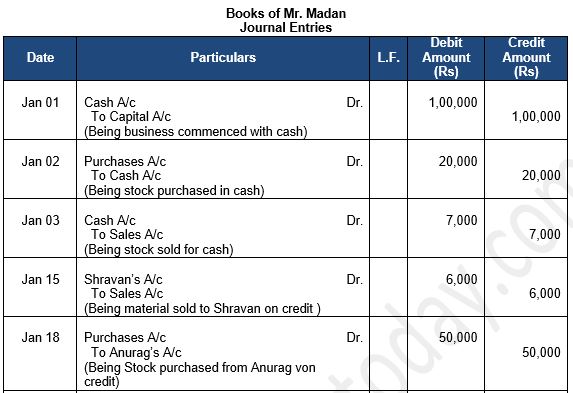

Question 2: Madan commenced business on 1st January, 2024 introducing capital in cash Rs. 1,00,000. His other transactions during the month were as follows:

Enter the above transactions in his books of account

Answer 2:

Statement showing Journal of Madan

Following are the ledgers shown in the books of Madan

Point of Knowledge:

(1) As Sales made on Jan. 15 is on credit so the Assets (debtors) will increases.

(2) As Purchases made on Jan. 18 is on credit so the liability (creditor) will increases.

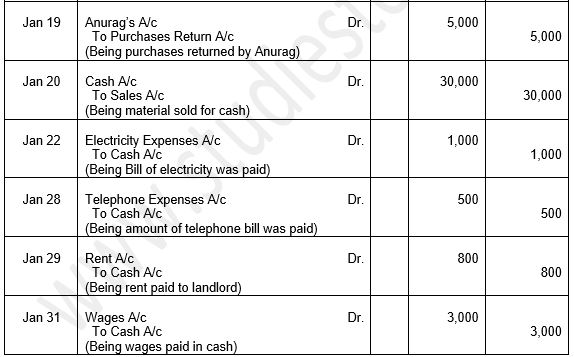

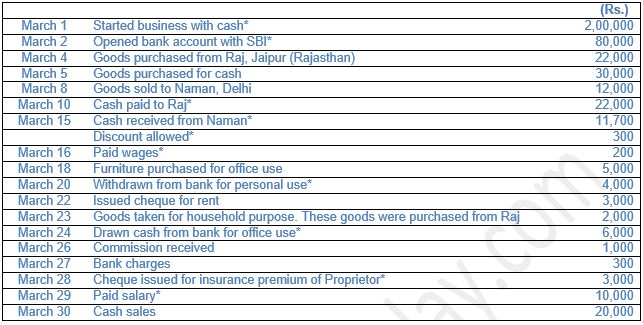

Question 3: Journalise the following transactions in the Journal of Rakesh, Delhi and post them to the Ledger:

Answer 3:

Statement showing Journal of Rakesh

Following are the ledgers shown in the books of Rakesh

Point of knowledge:-

(i) When we use goods for personal use it reduces the value of purchases with the value of goods use as personal. It is so because if goods are used for other purpose other than sale, the amount of such goods reduced.

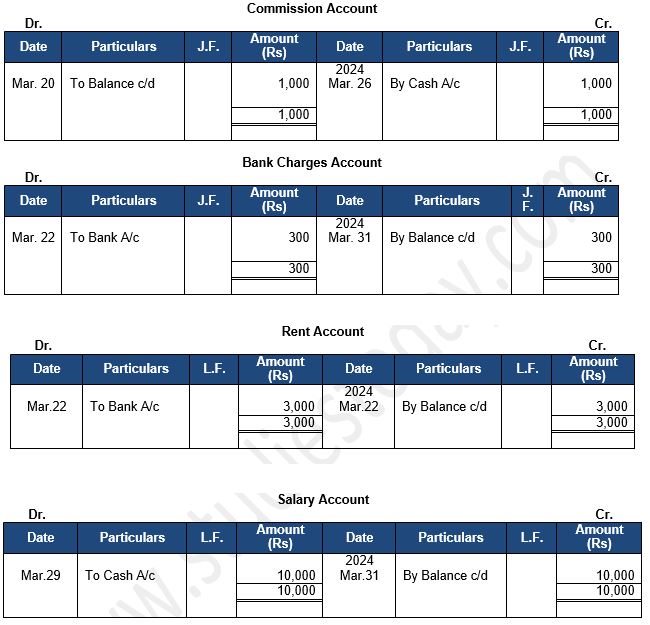

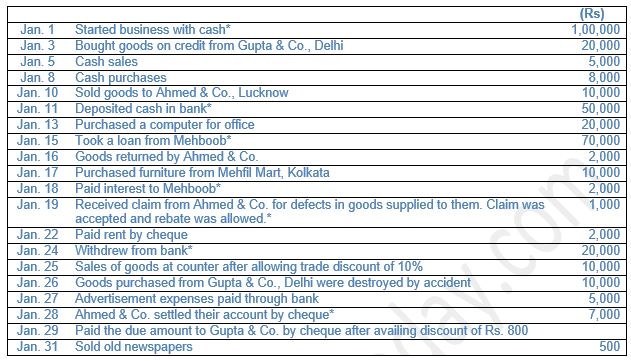

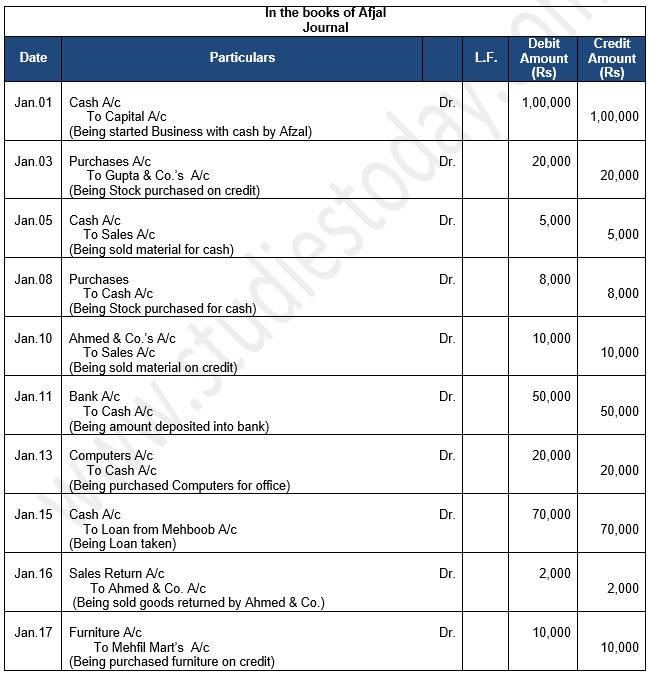

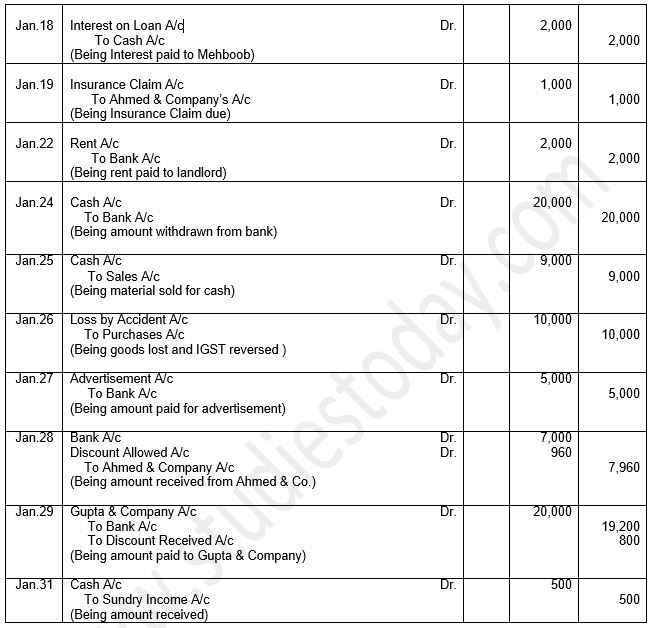

Question 4: Journalise the following transactions in the books of Afzal, Kolkata and post them to the Ledger:

Answer 4:

Statement showing Journal of Afzal, Kolkata

Following are the ledgers shown in the books of Afjal, Kolkata

Point Of Knowledge: -

Trade discount is the part of purchases & it should be deducted from the purchases. It is no shown in the books of accounts.

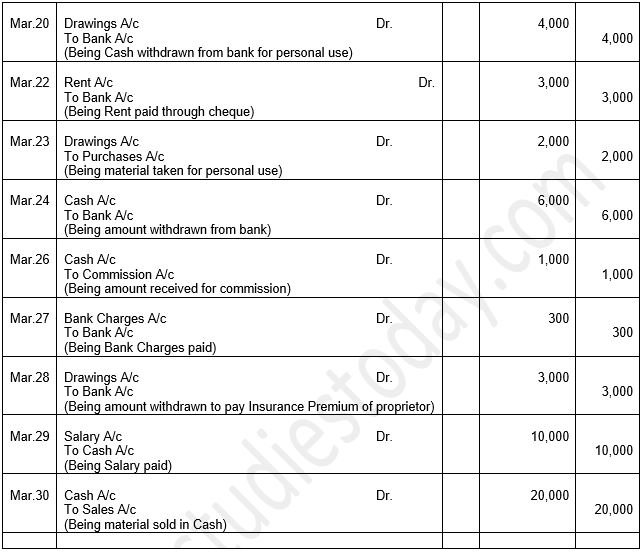

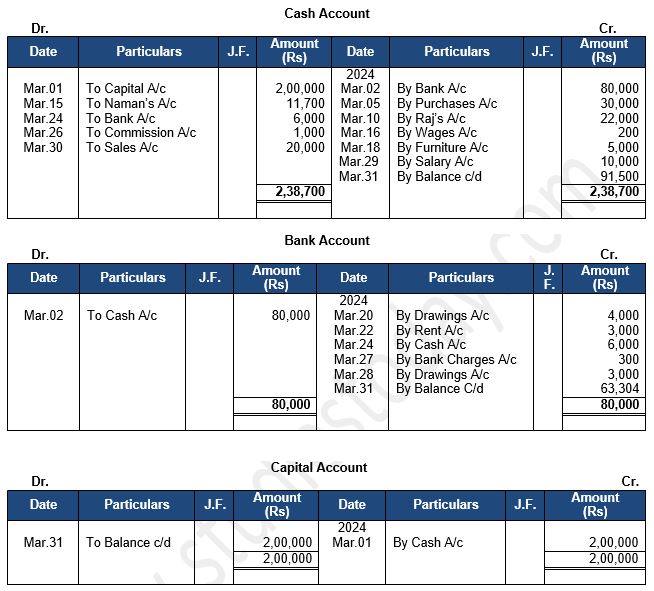

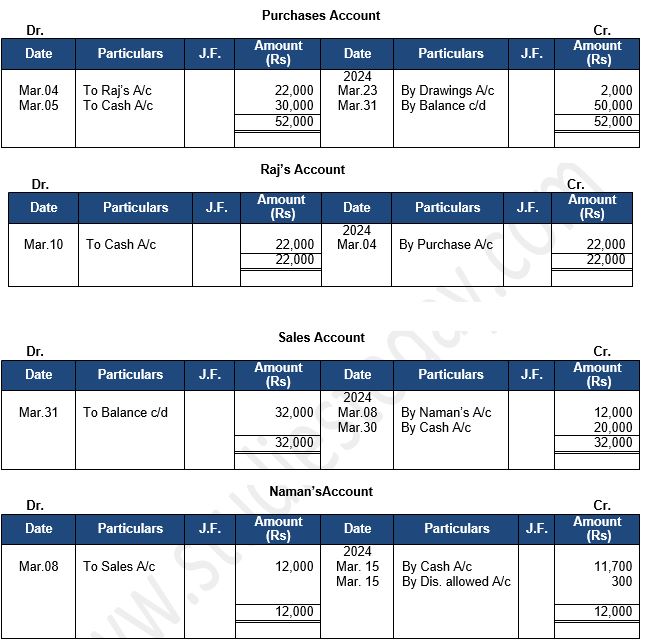

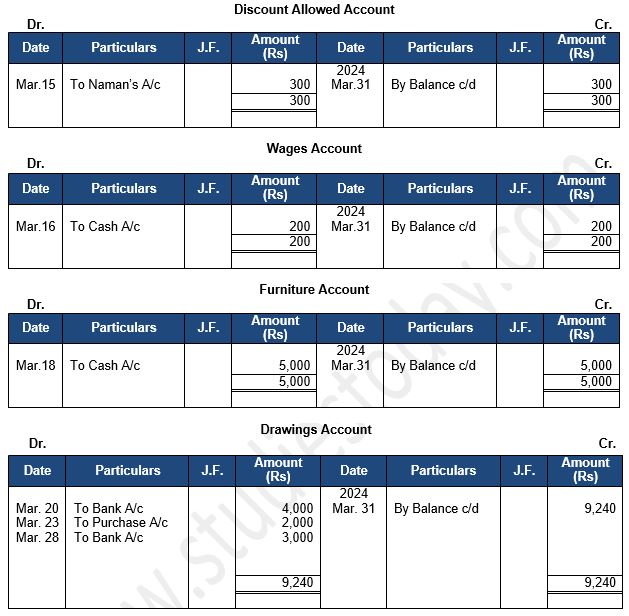

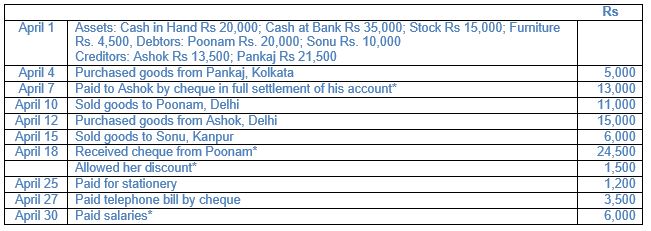

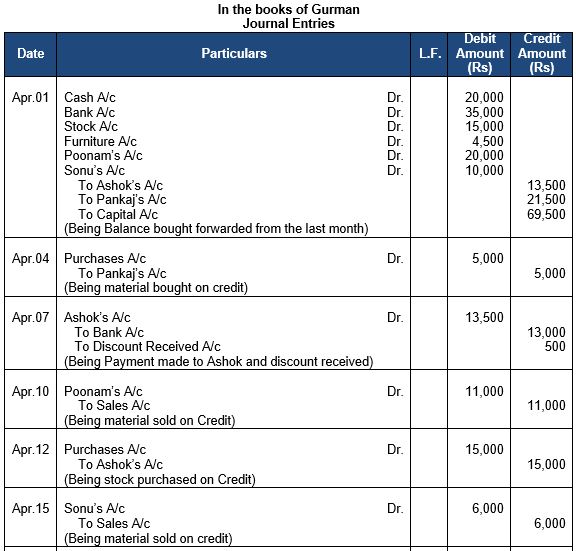

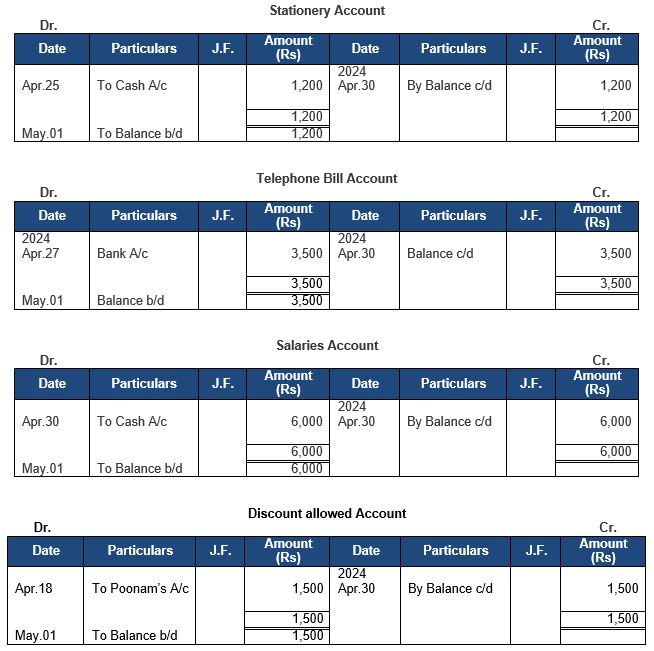

Question 5: Enter the following transactions in the Journal of Gurman and post them to the Ledger::

Answer 5:

Statement showing Journal of Gurman

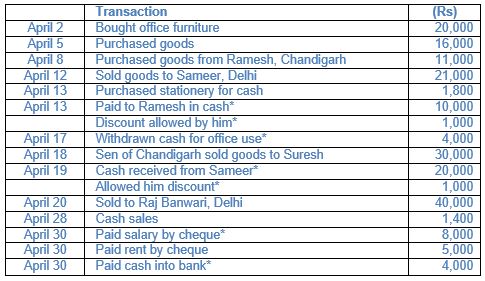

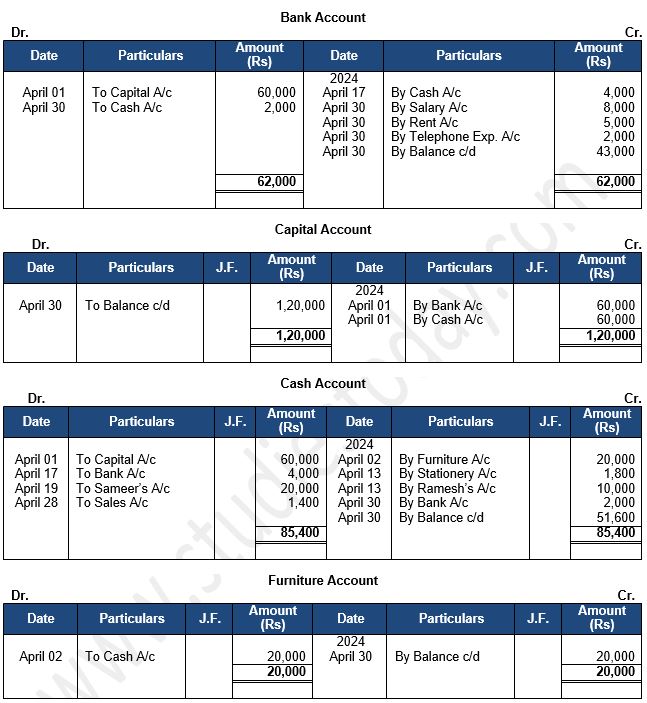

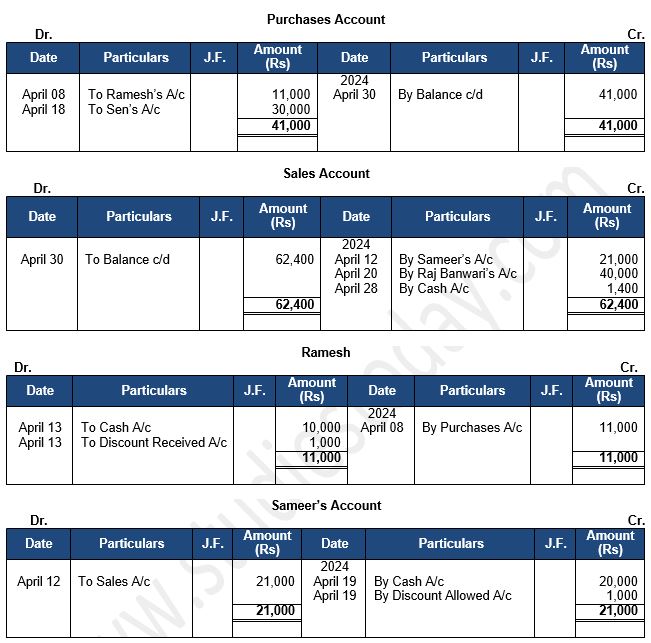

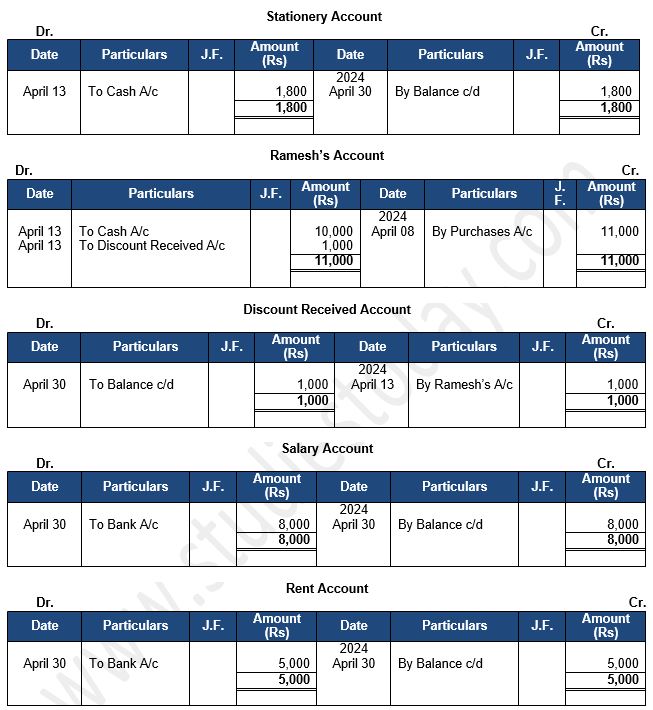

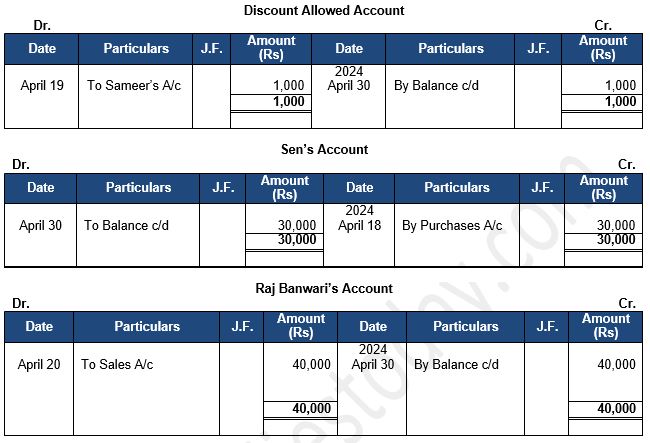

Question 6: Suresh commenced business on 1st April, 2024 with a capital of Rs. 1,20,000 of which Rs. 60,000 was paid into his Bank Account and balance retained as cash . His other transactions during the month were as follows:

Journalise the above transactions and post them to the Ledger

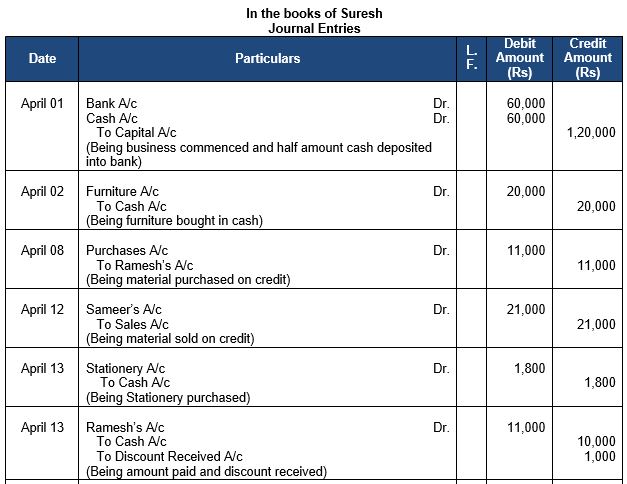

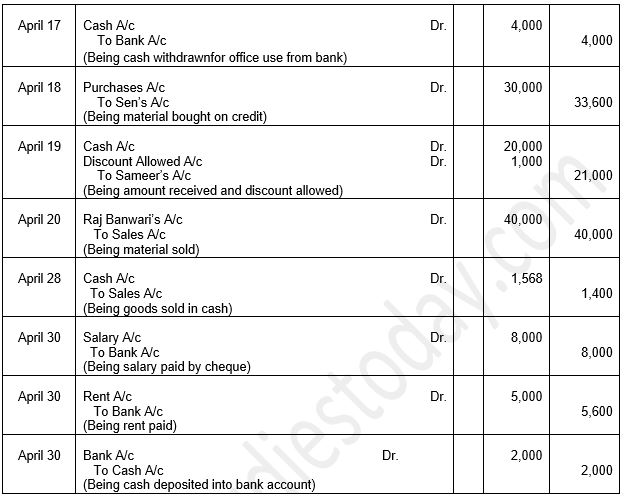

Answer 6:

Statement showing Journal of Suresh,

Following are the ledgers shown in the books of Suresh

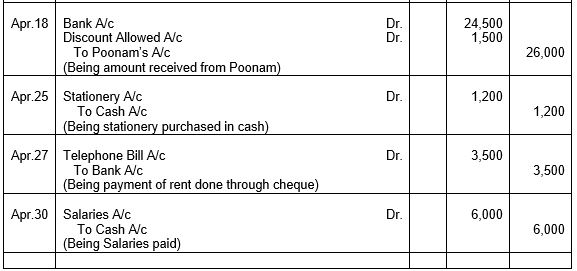

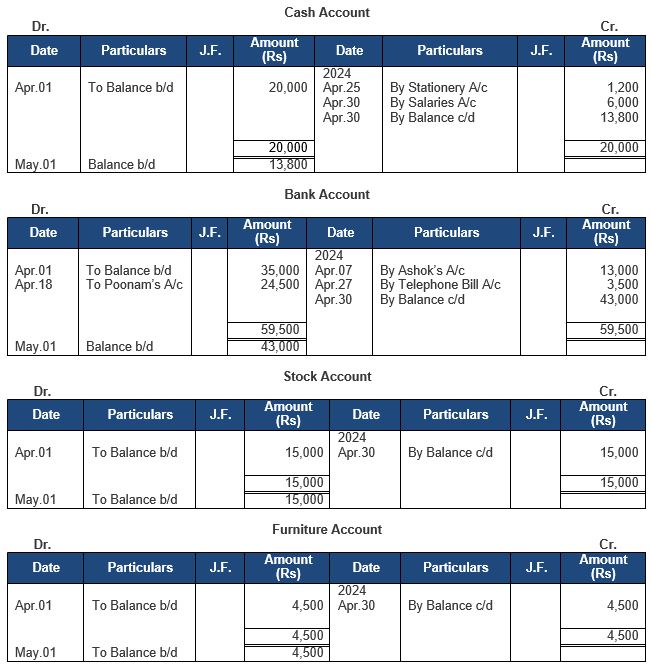

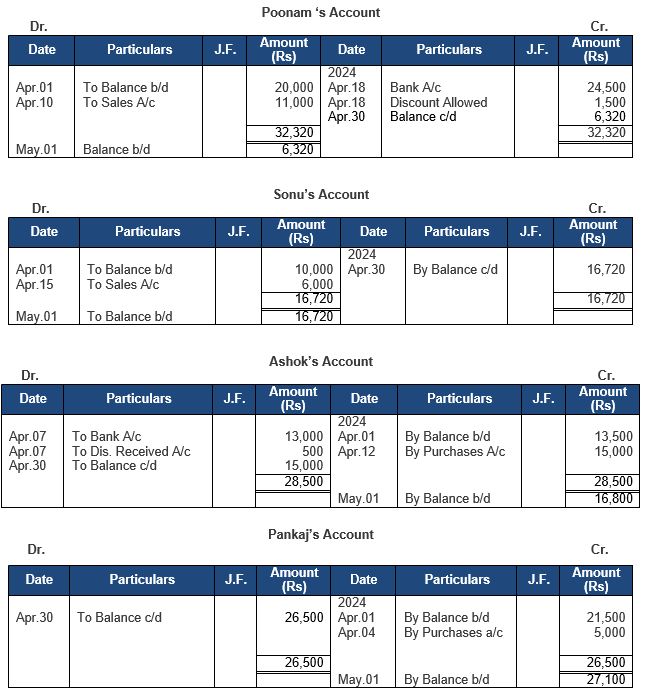

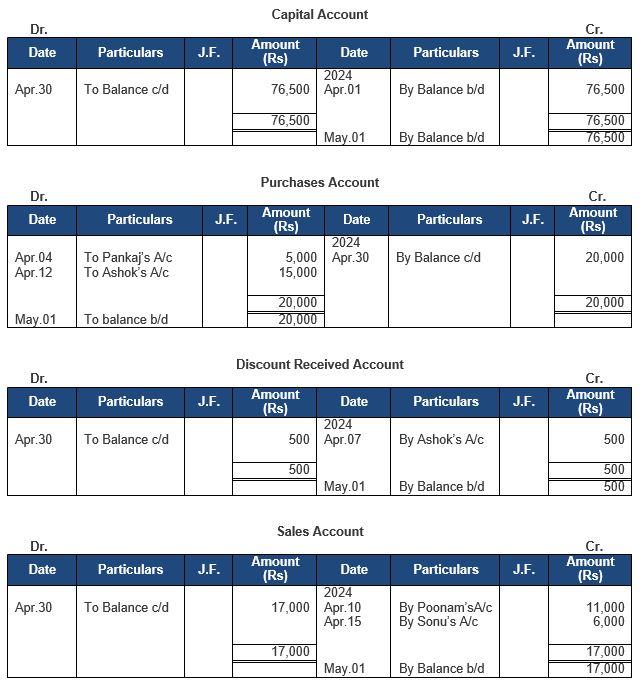

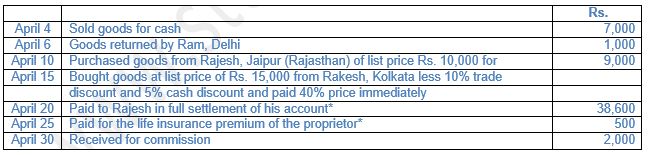

Question 7: Following balances appeared in the books of Ashok, Delhi on 1st April, 2024:

Assets: Cash Rs. 50,000; Stock Rs. 30,000; Debtors–Ram Rs. 50,000; Machinery Rs. 60,000.

Liabilities: Creditor – Rajesh Rs. 30,000.

The following transactions took place in April, 2024:

Pass Journal entries for the above transaction, post them into the Ledger and prepare the Trial Balance on 30th April, 2024.

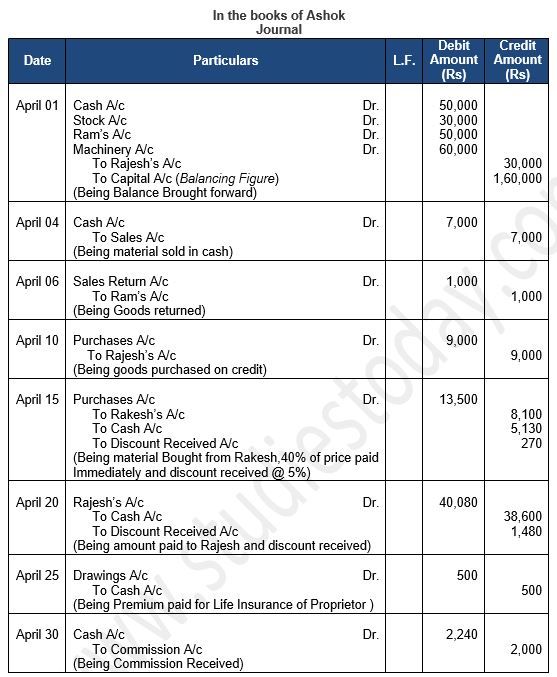

Answer 7:

Statement showing Journal of Ashok, Delhi

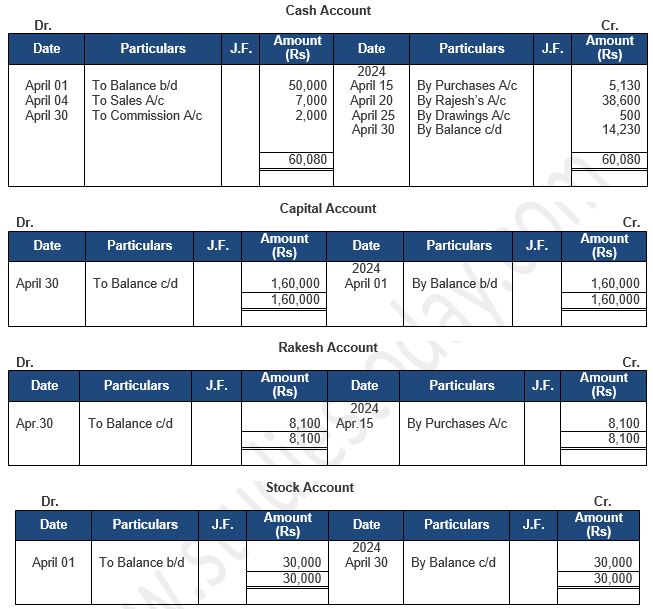

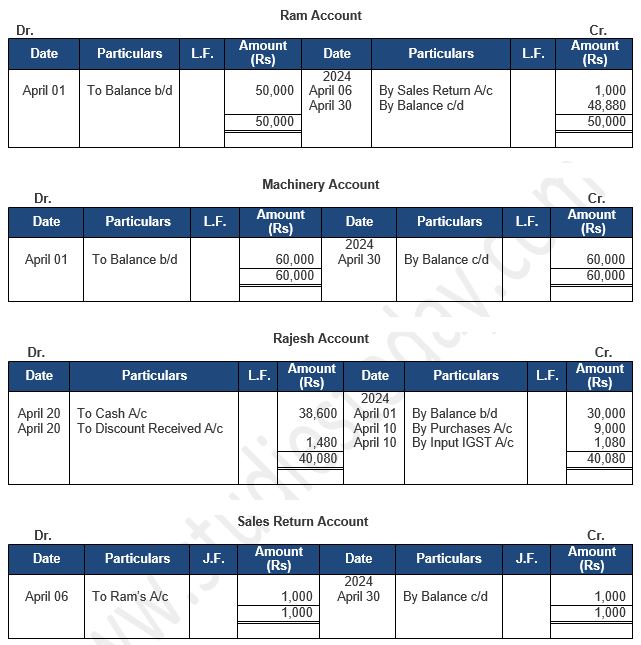

Following are the ledgers shown in the books of Ashok, Delhi

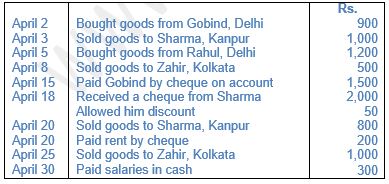

Question 8: On 1st April, 2024, the following were Ledger balances of M/s. Ram & Co., Delhi: Cash in Hand Rs. 300; Cash at Bank Rs. 7,000; Bills Payable Rs. 1,000; Zahir (Dr.) Rs. 800; Stock Rs. 4,000; Gobind (Cr.) Rs. 2,000; Sharma (Dr.) Rs. 1,500; Rahul (Cr.) Rs. 900; Capital Rs. 9,700. Transactions during the month of April, 2024 were:

Post the above transactions to the Ledger and prepare the Trial Balance on 30th April,2024.

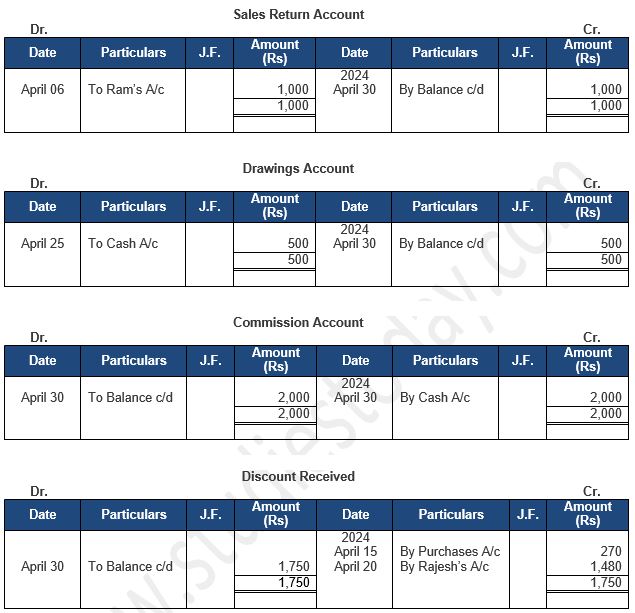

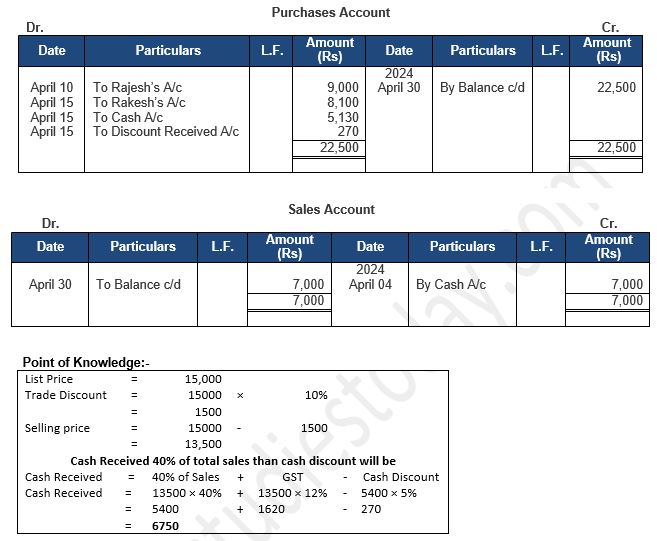

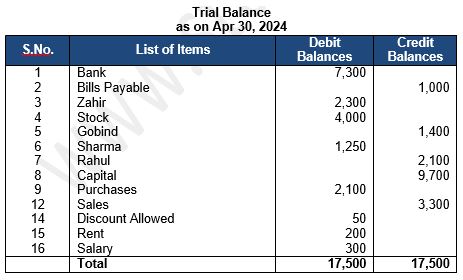

Answer 8:

Following are the ledgers shown in the books of M/s Ram & Co., Delhi

Statement of Trial Balance of M/s Ram & Co., Delhi as on April 30, 2024

Point of Knowledge:-

(i) If the two sides do not match of a Trail Balance it means there is definitely some error in Ledger or Trail balance.

Question 9: (Old Question from previous edition of TS Grewal)

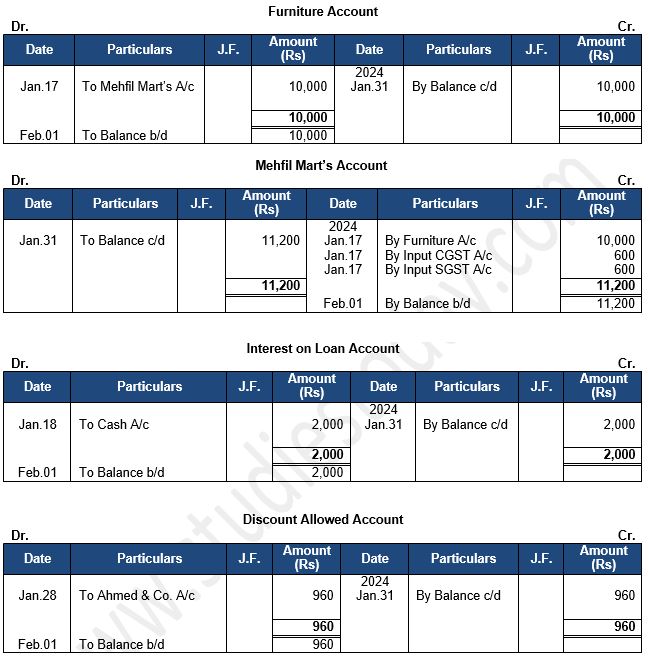

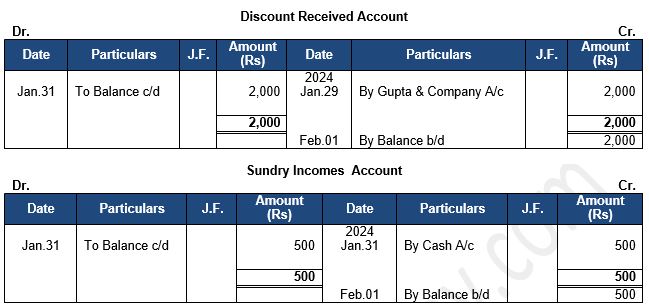

Question 9: Enter the following transactions in the Journal of M/s. Karim Bros., Prop. ShriKarim Khan, Kolkata, post to the Ledger and prepare the Trial Balance:

Inter-state transactions are subject to levy of IGST @ 12% and Intra-state transactions are subject to levy of CGST and SGST @ 6% each. GST is not levied on transactions marked with (*).

Answer 9:

Statement showing Journal of M/s. Karim Bros.

Question 10: (Old Question from previous edition of TS Grewal)

Inter-state transactions are subject to levy of IGST @ 12% and Intra-state transactions are subject to levy of CGST and SGST @ 6% each. GST is not levied on transactions marked with (*).

Journalise the above transactions and post them to the Ledger.

Answer 10:

Statement showing Journal of S. K. Gupta, Chandigarh

Point of Knowledge:-

(i) All Assets are showing a Debit Balance So Account will be opened and amount will written on the debit side as To Balance b/d.

Question 11: (Old Question from previous edition of TS Grewal)

Question 11: Journalise the following transactions in the books of Shri Manoj, Kolkata and prepare Ledger Accounts.

Opening Debit Balances:

Cash in Hand Rs15,000; Cash at Bank Rs 55,000; Stock Rs 28,000; Debtors Rs 25,000 (Sunil Rs 5,000; AbhayRs10,000 and Alok Rs 10,000); Fixed Assets : Computer and Printer Rs50,000; Furniture Rs 10,000; Delivery Van Rs 25,000.

Opening Credit Balances:

Bank Loan Rs 90,000; Salaries Outstanding Rs 15,000; Creditors Rs 20,000; Bills Payable Rs 10,000; Capital Rs 73,000.

Transactions for the month of April, 2019 were :

(i) Purchased goods from M/s Prabhat Electricals Rs 10,000 less 10% Trade Discount. Cheque was issued immediately and availed 2% Cash Discount on purchase price.

(ii) Cheque was received from Abhay for the balance allowing him discount of 2%*.

(iii) Cheque was received from Alok for the balance due* .

(iv) Sunil was unable to pay the full dues and offered to pay 75%, which was accepted. Cheque was duly received*.

(v) Gave goods costing Rs 1,000 as charity. These goods were purchased in Kolkata.

(vi) In a competition held by the RWA where the shop is located an electric iron costing Rs 500 was given as an award. It had been purchased from Prabhat Electricals, Delhi.

(vii) A debt of Rs 10,000 that was written off as bad debt in the past was received*.

(viii) Salaries amounting to Rs15,000 provided in the books for the month of March, 2019 were paid through cheque*.

(ix) Sales for the month were: Cash Sales Rs 15,00,000 (Intra-state) and Credit Sales Rs 3,00,000 (Inter-state).

(x) Purchases for the month were: Cash Purchases Rs 1,00,000 (Intra-state) and Credit Purchases (Inter-state) Rs 9,00,000.

Cheques Received from Debtors Rs2,00,000; Deposited Cash Rs 15,00,000.

(xi) Paid to creditors through cheques Rs 8,90,000*.

(xii) Bank Loan repaid during the month Rs 20,000*.

Inter-state transactions are subject to levy of IGST @ 12% and Intra-state transactions are subject to levy of CGST and SGST @ 6% each. GST is not levied on transactions marked with (*).

Answer 11:

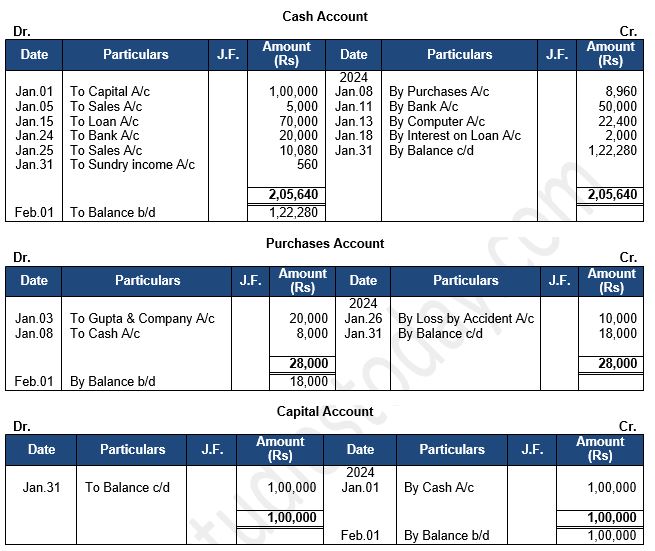

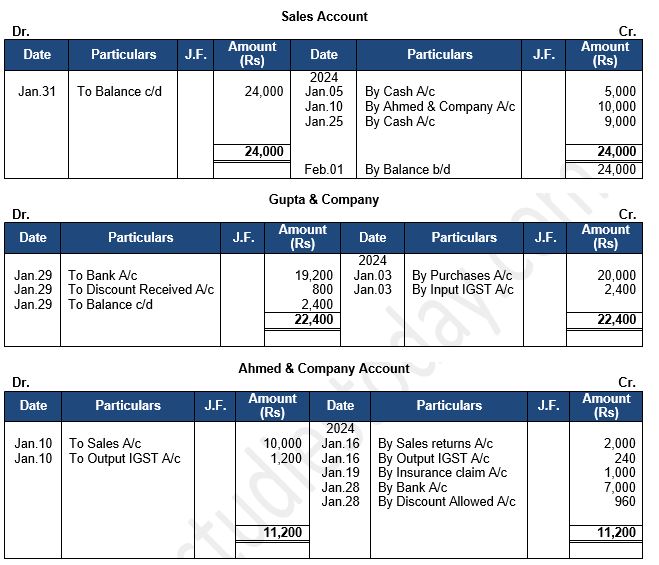

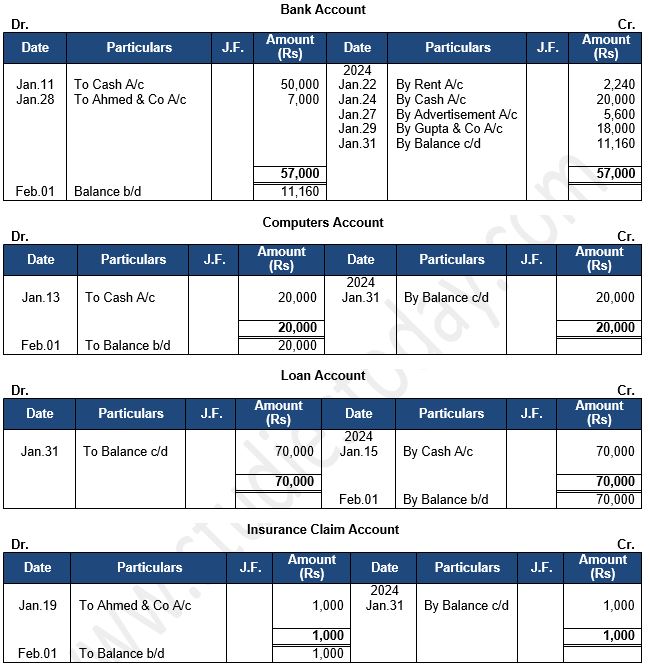

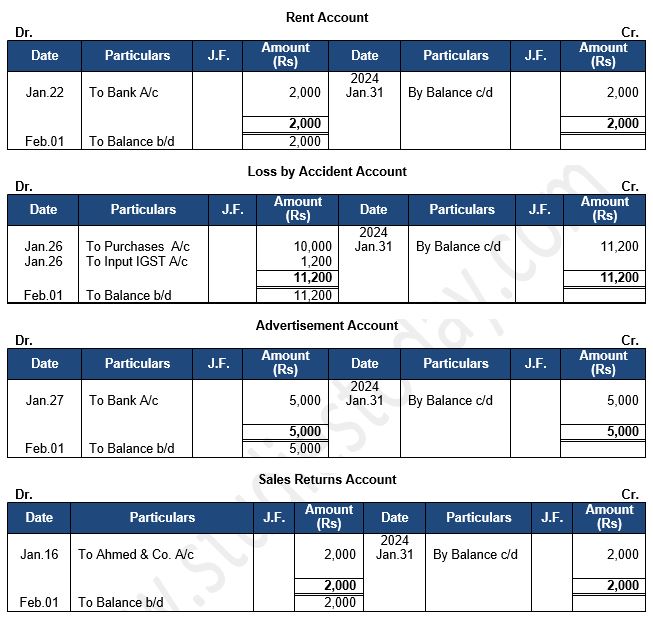

Statement showing Journal of Manoj, Kolkata

Point of Knowledge: -

When the goods given as charity the amount of purchases will decrease with the value of goods given as charity. It happen when goods are not sold, it used for other purposes like Charity, Free Sample, Loss by theft or fire & used for personal.