Download the latest CBSE Class 12 Accountancy Accounting For Not For Profit Organisations Notes Set 01 in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 1 Chapter 1 Accounting for Not for Profit Organisation

To secure a higher rank, students should use these Class 12 Accountancy Part 1 Chapter 1 Accounting for Not for Profit Organisation notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 1 Chapter 1 Accounting for Not for Profit Organisation Revision Notes for Class 12 Accountancy

UNIT-09

ACCOUNTING FOR NOT FOR PROFIT ORGANISATIONS

1. Meaning of NPO :-

Non profit organizations are those organizations which are established for a Social/Charitable/Cultural purpose & not for earning profit. They render services for the promotion of Art, Culture, Sports, Education & Healthcare etc.

2. Features of NPO :-

a) They are registered distinct entities

b) They render services to the society at nominal charges

c) Their basic motive is not profit earning but social service.

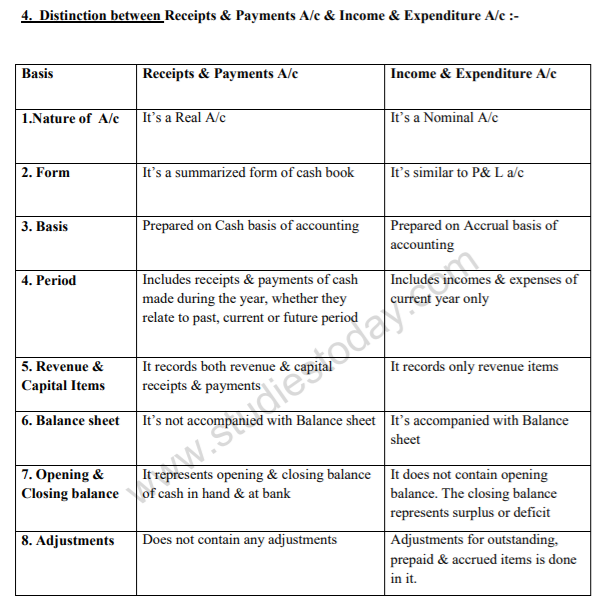

3. Final Accounts of NPO :-

They prepare the following financial statements at the end of the accounting period:-

1. Receipts & Payments A/c;

2. Income & Expenditure A/c;

3. Balance sheet.

4. Calculation of Subscription to be credited to Income & Exp. A/c.

Note : - Taking the figure of subscriptions received from the Receipts & Payments a/c as the base, additions for subscription of the current year though outstanding and subtraction of the subscription of the past & future period should be done to arrive at the figure to be credited to Income & Expenditure a/c. It should be clearly kept in mind that only the subscription of the current year should be considered even if it is outstanding and the subscription of the past & future period even if received in the current year should be excluded.

The following illustrations shall clarify the point:-

Illustration : - 1 Rs.

Subscription received during 2007-08 50,000

Subscription outstanding on 31-3-08 8,000

Subscription outstanding on 1-04-07 6,000

Calculate the amount of subscription to be credited to Income & Expenditure a/c for the yr. 2007-08.

Ans.1

Rs.

Subscription received during the yr. 50,000

Add: Subscription outstanding on 31-3-08 8,000

---------

58,000

Less: Subscription outstanding on 1-04-07 6,000

---------

Amount to be credited to Income & Expenditure A/c ==→ 52,000

---------

Illustration : - 2 Rs.

Mumbai Club received subscription during the yr. 2005-06 1,50,000

Subscription received on 31-3-05 4,500

Subscription received on 31-3-06 5,100

Subscription outstanding on 31-3-06for 2005-06 3,800

Subscription outstanding 2004-05 (of which Rs.4,000 received in 2005-06) 6,000

Calculate the subscription to be taken to Income & Exp. a/c for 2005-06.

Ans. 2 Rs.

Total Subscription Received during the yr. 2005-06 1,50,000

Add: Sub. Outstanding for 2005-06 3,800

Sub. Received in advance on 31-3-05 4,500

----------

1,58,300

Less: Sub received in advance on 31-3-06 5,100

Sub. Of 2004-05 received in 2005-06 4,000 9,100

---------- ------------

Sub for 2005-06 to be taken to Income & Exp. a/c. ==→ Rs.1,49,200

-----------

Calculation of expenses for the year for Income & Expenditure a/c.

Note : Here too, it is important to understand that - the guiding principle is - that the expenses of the current year whether paid or not should be considered. Similarly expenses of previous or future period though paid in the current year should be excluded. The following Illustration shall clarify the concept further.

Illustration :- 3 Ascertain the amount of salary chargeable to Income & Expenditure A/c for 2006-07

Rs.

Total salaries paid in 2006-07 10,200

Prepaid salaries on 31-3-2006 1,200

Prepaid salaries on 31-3-2007 600

Outstanding salaries on 31-3-2006 900

Outstanding salaries on 31-3-2007 750

Ans. 3 Rs.

Total Salaries paid in 2006-07 10,200

Add: - Outstanding salaries on 31-3-07 750

Prepaid salary on 31-3-06 1,200

---------------

12,150

Less:- Outstanding on 31-3-06 - 900

Prepaid on 31-3-07 - 600 1,500

------ ---------------

Salaries dr. to Income & Exp. A/c for 2006-07 10,650

Please refer to attached file CBSE Class 12 Accountancy Accounting For Not For Profit Organisations Notes Set A.

Free study material for Accountancy

CBSE Class 12 Accountancy Part 1 Chapter 1 Accounting for Not for Profit Organisation Notes

Students can use these Revision Notes for Part 1 Chapter 1 Accounting for Not for Profit Organisation to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 1 Chapter 1 Accounting for Not for Profit Organisation Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 1 Chapter 1 Accounting for Not for Profit Organisation Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 1 Chapter 1 Accounting for Not for Profit Organisation. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Accounting For Not For Profit Organisations Notes Set 01 from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Accounting For Not For Profit Organisations Notes Set 01 include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Accounting For Not For Profit Organisations Notes Set 01 provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Accounting For Not For Profit Organisations Notes Set 01, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Accounting For Not For Profit Organisations Notes Set 01, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.