Download the latest CBSE Class 12 Accountancy Redemption Of Debenture Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures

To secure a higher rank, students should use these Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 2 Chapter 2 Issue and Redemption of Debentures Revision Notes for Class 12 Accountancy

CHAPTER 9

Redemption of Debenture

Meaning : Redemption of debentures means repayment of the due amount of debentures to the debenture holders. It may be at par or at premium.

Time of redemption : (a) At maturity : when repayment is made at the date of maturity of debentures which is determined at the time of issue of debentures.

(b) Before maturity : If articles of association and terms of issue mentioned in prospectus allows, then a company can redeem its debentures before maturity date. Redemption methods : (1) Redemption is Lumpsum :When redemption is made at the expiry of a specific period, as per the terms of issue.

(2) Redemtion by draw of lots :In this method a certain proportion of debentures are redeem each year, the debenture for which repayment is to be made is selected by draw.

(3) Redemtion by purchase in open market :if articles of association of a company authorize, it may purchase its own debentures from open market i.e. stock exchange. Advantage of this method :

1. When market price of own debentures is low than the redeemable value.

2. Decrease the amount of interest payable to outsiders.

3. if term of issue is provided that debentures are to be redeemed at premium then such premium can be decrease Sometimes company can purchase the debentures at more than the redeemable value

due to the following reasons :

1. To maintain the solvency ratio.

2. To utlize the surplus money or funds which are lying idle with the company.

3. When rate of interest on debentures is more than the current market rate of interest on debentures in the industry.

4. Redemption by conversion : As per the terms of issue, convertible debentures may be covert into shares or new debentures at the option of debenture holders. This option of conversion is given to the debentureholder within specific period. In this case no need to transfer profit to Debenture Redemption Reserve Account.

Sources of Redemption of debentures.

1. Proceeds from fresh issue of share capital or debenture holders.

2. From accumulated profits.

3. Proceeds from sale of fixed assets.

4. A company may purchases its own debentures out of its surplus funds.

Two terms which are used in the redemption of debentures :

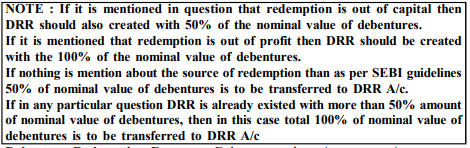

1. Redemption out of capital : when a company not used its reserve or accumulated profit for redemption of its debentures. It is called redemption out of capital. So company using this method are not transfer it profit to DRR A/c. But as per SEBI guidelines it is necessary for a company to transfer 50% amount of nominal value of debentures to be redeemed in DRR A/c before redemption of debentures commence.

2. Redemption out of profit : Redemption out of profit means that adequate amount of profits are transferred to DRR A/c from P&L Appropriation A/c before the redemption of debenture commences. This reduce the amount available for dividends to shareholders.

Debenture Redemption Reserve : Debenture redemption reserve is a reserve representing retentions out of profit made for the purpose of redemption of debentures. Amount of DRR to be created : Section 117 (c) of the Indian Companies Act 1956 requires that, an adequate amount of profit should be transferred to DRR before redemption commences. However the adequate amount is not specified by the companies Act.

SEBI has issued guidlines for the redemption of debentures whereby :

1. An amount equivalent to 50% of the amount of debentures issue must be transferred to DRR before redemption of debentures commences. This provision is applicable for nonconvertible debentures or nonconvertible part of party convertible debentures. After all the debentures are redeemed, this account is closed by transferring to general reserve account.

Exception to the creation of DRR as per SEBI guidlines :

1. All infrastructure companies, wholly engaged in the business related to development maintenance and operation of infrastructure facilities.

2. A company issuing debentures maturity period of not more than 18 months.

3. Debentures issued by Banking Companies.

4. Companies issuing privately placed debentures.

The above types of companies are exempted by SEBI from creating DRR. However the above types of companies can create DRR(at it option) for the redemption of debentures.

(B) Redemption At Premium : Illustration 2. Z Ltd. Redeemed its 1,00,000 10% Debentures of Rs.10 each at 5% premium on 31st March, 2011.

Illust. 3 : Rajesh Export Ltd. has 2,000, 9% Debentures of Rs.100 each due on redemption on 31st March 2011. Debentures redemption reserve has a balance of Rs.30,000 on that date. Record the necessary journal entries at the time of redemption of debentures

Illust. 4 : Rahul Ltd. has 50,000, 9% Debentures of Rs.50 each due on redemption on

31st March 2011. Debentures redemption reserve has a balance of Rs.15,00,000 on that date. Record the necessary journal entries at the time of redemption of debentures.

Note : In this case DRR is Already more than 50% of nominal value of debentures, then it is created upto the 100% of the nominal value of debenture

Illust.5 : Saket Ltd.(an infrastructure co.) has outstanding 10,000, 9% Debentues of Rs.50 each due on redemption on 31st March, 2011. Record the necessary journal entries at the time of redemption of debentures.

(Note : The infrastructure Companies are exempted from creating DRR as per SEBI guidlines. However these companies may create DRR at its option.)

Redemption Method : 2 Draw of lots

Illustration 6 : S Ltd. redeemed its Rs.10,000, 8% Debentures out of capital by drawing a Lot on 30 Nov.2011 Journalise.

Please click the link below to download pdf file for CBSE Class 12 Redemption of Debenture.

Free study material for Accountancy

CBSE Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures Notes

Students can use these Revision Notes for Part 2 Chapter 2 Issue and Redemption of Debentures to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 2 Chapter 2 Issue and Redemption of Debentures Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 2 Chapter 2 Issue and Redemption of Debentures Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 2 Chapter 2 Issue and Redemption of Debentures. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Redemption Of Debenture Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Redemption Of Debenture Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Redemption Of Debenture Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Redemption Of Debenture Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Redemption Of Debenture Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.