Download the latest CBSE Class 12 Accountancy Goodwill Nature And Valuation Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts

To secure a higher rank, students should use these Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 1 Chapter 1 Accounting for Partnership Basic Concepts Revision Notes for Class 12 Accountancy

CHAPTER 2

Goodwill : Nature and Valuation

Meaning of Goodwill:

Goodwill places the organization at a good position due to which the organization is able to earn higher profits without any extra efforts. Goodwill cannot be seen but felt. Therefore goodwill is called an Intangible asset.

Factors affecting the value of Goodwill :

1. Efficient management

2. Quality of products

3. Location of business

4. Availability of raw material

5. Favorable contracts

Need for valuing goodwill : Whenever the mutual rights of the partners changes then party which makes a sacrifice must be compensated. This basis of compensation is goodwill so we need to calculate goodwill. Mutual rights change under following circumstances

1) When profit sharing ratio changes

2) On admission of a partner

3) On Retirement or death of a partner

4) When amalganation of two firms taken place.

5) When partnership firm is sold.

Methods of valuation of goodwill :

1. Average profit method

2. Super profit method

3. Capitalization method

Average Profit Method

The profit earned by a Firm during previous accounting periods on an average basis is called average profit. Goodwill is calculated on the basis of average profit due to future expectations of earning capacity of the firm.

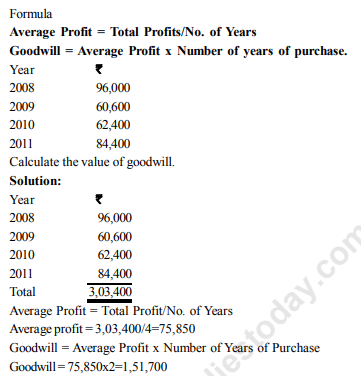

Illustration 1. (Average Profit Method)

Akanksha,Chetna and Dipanshu are partners in a firm sharing profits and losses in the ratio of 3:2:1. They decide to take Jatin into partnership from January 1,2012 for 1/5 share in the future profits. For this purpose , goodwill is to be valued at 2 times the average annual profits of the previous four years. The average profits for the past four years were:

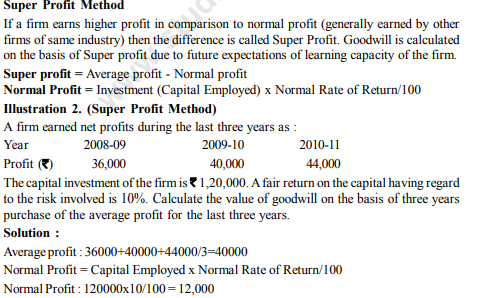

Super profit = Average profit Normal profit

= 40,00012,000=28,000

Goodwill = Super profit x number of years purchased

= 28,000 x 3 = 84,000

Capitalisation Method

In this method capitalized value of the firm is calculated on the basis of normal rate of return. Difference between teh capitalized value and actual capital employed is called goodwill.

Illustration 3 (Capitalisation Method)

A earns ` 1,20,000 as its annual profits, the rates of normal profit being 10% The assets of teh firm amounted to ` 14,40,000 and liabilities to ` 4,80,000. Find out the value of goodwill by capitalization method.

Solution :

Capitalized value of the firm = Average profit x 1000/ Rate of normal profit

= 1,20,000x10/100 = 12,00,0005

Capital employed = Total assets liabilities

= 14,40,000 4,80,000 = 9,60,000

Goodwill = capitalized value capital employeed

= 12,00,0009,60,000=2,40,000

Illustration 4 . (Average profit method)

A and B are partners in a firm. They admit C into the firm. The goodwill for the purpose is to be calculated at 2 year's purchase of the average normal profits of the last three years which were ` 10,000, ` 15,000 and ` 30,000 respectively. Second years profit included profit on sale of Machinery ` 10,000. Find the value of goodwill of the firm on C's Admission.

Solution

(1) Calculation of Average Profit :

Year ended `

Ist Year 10,000

2nd Year (`15,000`10,000) 5,000

3rd Year 30,000

Total Profits 45,000

Average profit = Total profit/No. of years

= ` 45,000/3=15,000

Illustration 5 (Super profit method)

The average net profits expected of a firm in future are ` 68,000 per year and capita invested in the business by the firm is ` 3,50,000. The rate of interest expected from capital invested in this class of business is 12%. The remuneration of the partners is estimated to be ` 8,000 for the year. You are required to find out the value of goodwill on the basis of two years' purchase of super profits.

Solution

Average Profit = Average Net Profit Partner's remuneration

(1) Average profit = ` 68,000` 8,000 = `60,000

(ii) Normal profit= Capital employed x Normal rate of return/100

= ` 3,50,000x12/100= ` 42,000

(iii) Super Profit = Average profit Normal profit

= ` 60,000 ` 42,000 = ` 18,000

(iv) Value of goodwill = Super profit x No. of years ' purchase

= ` 18,000x2 = ` 36,000

Illustration 6. (Super profit method)

On April 1st, 1998 an existing firm had assets of ` 75,000 including cash of ` 5,000. The partners' capital accounts showed a balance of ` 60,000 and reserves constituted the rest. If the normal rate of return is 20% and the goodwill of the firm is valued at ` 24,000 at 4 years purchase of super profits, find the averages profits of the firm

Solution :

(1) Calculation of Normal Profit : Capital employed x normal rate/100 =75,000x20/100 = ` 15,000

(2) Calculation of Super Profit :

Goodwill = Super profit x No. of years' purchase

` 24,000 = Super Profit x4

Super Profit = ` 24,000 = `6,000

(3) Calculating of Average Profit :

Super Profit = Average Profit Normal Profit

` 6,000 = Average Profit ` 15,000

Average Profit = ` 6,000+ ` 15,000 = ` 21,000

Please click the link below to download pdf file for CBSE Class 12 Goodwill-Nature and Valuation.

Free study material for Accountancy

CBSE Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts Notes

Students can use these Revision Notes for Part 1 Chapter 1 Accounting for Partnership Basic Concepts to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 1 Chapter 1 Accounting for Partnership Basic Concepts Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 1 Chapter 1 Accounting for Partnership Basic Concepts Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 1 Chapter 1 Accounting for Partnership Basic Concepts. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Goodwill Nature And Valuation Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Goodwill Nature And Valuation Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Goodwill Nature And Valuation Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Goodwill Nature And Valuation Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Goodwill Nature And Valuation Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.