Download the latest CBSE Class 12 Accountancy Accounting For Partnership Firms Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts

To secure a higher rank, students should use these Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 1 Chapter 1 Accounting for Partnership Basic Concepts Revision Notes for Class 12 Accountancy

Meaning and Definition

According to Section 4 of the Partnership Act 1932 “Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all”

Features of partnership Firm

1) Association of two or more persons: There must be at least two persons and maximum of 50 persons to form a partnership and they must be competent to contract.

2) Partnership Agreement or Deed: There must be an agreement among partners to form a partnership. It can be written or oral.

3) Legal Business: The business of the partnership firm must be a legally allowed business.

4) Sharing of Profits or Losses: The partners must share profits or losses in a certain ratio.

5) Mutual Agency: The partners mutually take part in daily routine work or the work may be carried on by one or more partners on behalf of the other partners. Every partner is legally liable for the acts of all other partners, whether he is taking part in the activities of the firm or not.

6) Unlimited Liability: Partners' liability to the third parties is unlimited. If there are losses, and the firm is not able to pay its debts fully, then all the partners shall be jointly and severally liable to pay the debts of the firm to an unlimited extent.

Partnership Deed: The document, which contains terms of the agreement, is called' Partnership Deed'. It generally contains the details about all the aspects affecting the relationship between the partners including the objective of business, contribution of capital by each partner, ratio in which the profits and the losses will be shared by the partners and entitlement of partners to interest on capital, interest on loan, etc.

Provisions of Partnership Act, 1932 in the absence of Partnership Deed:

(a) Profit Sharing Ratio: If the partnership deed is silent about the profit sharing ratio, the profits and losses of the firm are to be shared equally by partners.

(b) Interest on Capital: No interest on capital is payable if the partnership deed is silent on the issue.

(c) Interest on Drawings: No interest is to be charged on the drawings made by the partners, if there is no mention in the Deed.

(d) Interest on Advances: If any partner has advanced some money to the firm beyond the amount of his capital for the purpose of business, he shall been titled to get an interest on the amount at the rate of 6 percent per annum.

(e) Remuneration for Firm's Work: No partner is entitled to get salary or other remuneration for taking part in the conduct of the business of the firm.

Fixed and Fluctuating Capital Accounts of Partners

There are two methods by which the capital accounts of partners can be maintained. These are:

(i) fixed capital method, and (ii) fluctuating capital method.

Fixed Capital Method: Under the fixed capital method, the capitals of the partners shall remain fixed unless additional capitalis introduced or a part of the capital is with drawn as per the agreement among the partners. All items likes hare of profit or loss, interest on capital, drawings,

Meaning and Definition

According to Section 4 of the Partnership Act 1932 “Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all”

Features of partnership Firm

1) Association of two or more persons: There must be at least two persons and maximum of 50 persons to form a partnership and they must be competent to contract.

2) Partnership Agreement or Deed: There must be an agreement among partners to form a partnership. It can be written or oral.

3) Legal Business: The business of the partnership firm must be a legally allowed business.

4) Sharing of Profits or Losses: The partners must share profits or losses in a certain ratio.

5) Mutual Agency: The partners mutually take part in daily routine work or the work may be carried on by one or more partners on behalf of the other partners. Every partner is legally liable for the acts of all other partners, whether he is taking part in the activities of the firm or not.

6) Unlimited Liability: Partners' liability to the third parties is unlimited. If there are losses, and the firm is not able to pay its debts fully, then all the partners shall be jointly and severally liable to pay the debts of the firm to an unlimited extent.

Partnership Deed: The document, which contains terms of the agreement, is called' Partnership Deed'. It generally contains the details about all the aspects affecting the relationship between the partners including the objective of business, contribution of capital by each partner, ratio in which the profits and the losses will be shared by the partners and entitlement of partners to interest on capital, interest on loan, etc.

Provisions of Partnership Act, 1932 in the absence of Partnership Deed:

(a) Profit Sharing Ratio: If the partnership deed is silent about the profit sharing ratio, the profits and losses of the firm are to be shared equally by partners.

(b) Interest on Capital: No interest on capital is payable if the partnership deed is silent on the issue.

(c) Interest on Drawings: No interest is to be charged on the drawings made by the partners, if there is no mention in the Deed.

(d) Interest on Advances: If any partner has advanced some money to the firm beyond the amount of his capital for the purpose of business, he shall been titled to get an interest on the amount at the rate of 6 percent per annum.

(e) Remuneration for Firm's Work: No partner is entitled to get salary or other remuneration for taking part in the conduct of the business of the firm.

Fixed and Fluctuating Capital Accounts of Partners

There are two methods by which the capital accounts of partners can be maintained. These are: (i) fixed capital method, and (ii) fluctuating capital method.

Fixed Capital Method: Under the fixed capital method, the capitals of the partners shall remain fixed unless additional capitalis introduced or a part of the capital is with drawn as per the agreement among the partners. All items likes hare of profit or loss, interest on capital, drawings, interest on drawings, etc. are recorded in separate accounts, called Partner's Current Account. The partners' capital accounts will always show a credit balance, which shall remain the same (fixed) year after year unless there is any addition or withdrawal of capital. The partners' current account on the other hand, may show a debit or a credit balance. Thus under this method, two accounts are maintained for each partner viz., capital account and current account, While the partners' capital accounts shall always appear on the liabilities side in the balance sheet, the partners' current account's balance shall be shown on the liabilities side, if they have credit balance and on the assets side, if they have debit balance.

The partner's capital account and the current account under the fixed capital method would appear as shown below:

Fluctuating Capital Method: Under the fluctuating capital method, only one account, i.e. capital account is maintained for each partner. All the adjustments such as share of profit and loss, interest on capital, drawings, interest on drawings, salary or commission to partners, etc. are recorded directly in the capital accounts of the partners. This makes the balance in the capital account to fluctuate from time to time. That's the reason why this method is called fluctuating capital method. In the absence of any instruction, the capital account should be prepared by this method. The proforma of capital accounts prepared under the fluctuating capital method is given below:

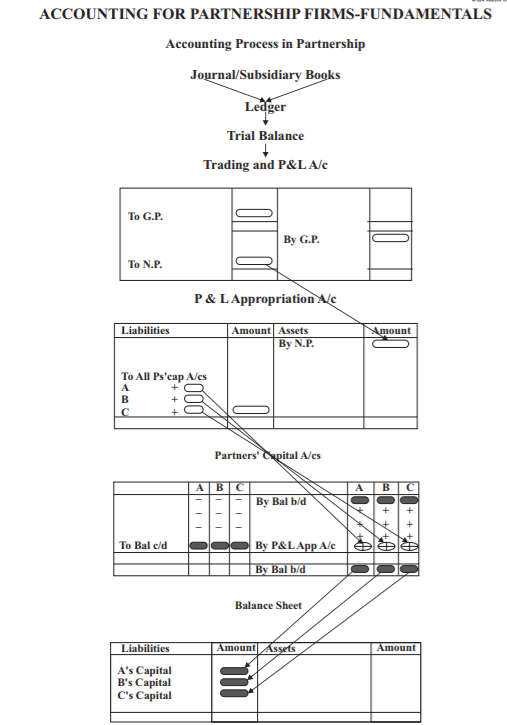

Distribution of Profit among Partners

The profits and losses of the firm are distributed among the partners in an agreed ratio. However, if the partnership deed is silent, the firm's profits and losses are to be shared equally by all the partners.

You know that in the case of sole partnership the profit or loss, as certained by the profit and loss account is transferred to the capital account of the proprietor. In case of partnership, however, certain adjustments such as interest on drawings, interest on capital, salary to partners, and commission to partners are required to be made. For this purpose, it is customary to prepare a Profit and Loss Appropriation Account of the firm and as certain the final figure of profit and loss to be distributed among the partners, in their profit sharing ratio.

The Proforma of Profit and Loss Appropriation Account is given as follows:

*Note: Interest on partner's loan is to be treated as a charge against profits.

Past Adjustments If after closing the accounts for the year it is the discovered that some errors have been committed, then these errors have to be rectified. Some adjustment entries have to be passed to rectify the error. The entries are made through Profit & Adjustment A/c. These entries are to rectify the errors committed in past, therefore, they are known as 'Past Adjustments'. Generally the following types of errors are committed:

Free study material for Accountancy

CBSE Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts Notes

Students can use these Revision Notes for Part 1 Chapter 1 Accounting for Partnership Basic Concepts to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 1 Chapter 1 Accounting for Partnership Basic Concepts Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 1 Chapter 1 Accounting for Partnership Basic Concepts Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 1 Chapter 1 Accounting for Partnership Basic Concepts. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Accounting For Partnership Firms Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Accounting For Partnership Firms Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Accounting For Partnership Firms Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Accounting For Partnership Firms Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Accounting For Partnership Firms Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.