Read and download the CBSE Class 12 Accountancy Accounting for Not for Profit Organisation Assignment for the 2025-26 academic session. We have provided comprehensive Class 12 Accountancy school assignments that have important solved questions and answers for Part 1 Chapter 1 Accounting For Not For Profit Organisation. These resources have been carefuly prepared by expert teachers as per the latest NCERT, CBSE, and KVS syllabus guidelines.

Solved Assignment for Class 12 Accountancy Part 1 Chapter 1 Accounting For Not For Profit Organisation

Practicing these Class 12 Accountancy problems daily is must to improve your conceptual understanding and score better marks in school examinations. These printable assignments are a perfect assessment tool for Part 1 Chapter 1 Accounting For Not For Profit Organisation, covering both basic and advanced level questions to help you get more marks in exams.

Part 1 Chapter 1 Accounting For Not For Profit Organisation Class 12 Solved Questions and Answers

Question. Which of the following is main source of income of non-profit organisation?

a) Sale of old books

b) Sale of old furniture

c) Received subscription

d) Business

Answer : C

Question. For the year ending 31st March, 2022, the following entries appeared related to subscription received

Amt (Rs)

2020-21 5,000

2021-22 96,000

2022-23 10,400

The club has 300 members, paying annual subscription of Rs 400 each. Subscription outstanding on 31st March, 2021 was Rs 8,000. Calculate the amount of subscription to be shown in the income and expenditure account?

a) Rs 96,000

b) Rs 1,11,400

c) Rs 1,20,000

d) Rs 91,000

Answer : C

Question. Which of the following will be recorded in credit side of receipts and payments account?

a) Rs 300 received from entrance fees

b) Cash purchases of books Rs 700

c) Donation received Rs 800

d) Outstanding Rs 300 for repair

Answer : B

Question. Donation can be

a) general donation

b) specific donation

c) Both (a) and (b)

d) None of these

Answer : C

Question. Item that should be debited in the income and expenditure account of a college is

a) tuition fees received from students

b) equipment purchased for science laboratory

c) amount of reward

d) fines collected from students

Answer : B

Question. Consider the following information

Sports fund investment Rs 70,000

Donation for sports fund Rs 15,000

Sports prizes awarded Rs 10,000

Expenses on sports events Rs 8,000

Income from sports fund investment Rs 5,000

Calculate amount of sport fund that will be shown in liability side of balance sheet.

a) Rs 40,000

b) Rs 38,000

c) Rs 45,000

d) Rs 72,000

Answer : D

Question. Consider the following statements

I. Income and expenditure records both capital and revenue items.

II. Receipt and payment account records only revenue items during the year.

Choose the correct option

a) Both are incorrect

b) Both are correct

c) Only (i) is correct

d) Only (ii) is correct

Answer : A

Question. Which of the following cannot be recorded in the receipt and payment account of a club?

a) Payment made to workers

b) Sale of old newspaper

c) Loss on sale of fixed asset

d) All of the above

Answer : C

Question. Capital fund in non-profit organisation will be

a) Total Assets − Total Liabilities

b) Total Assets − External Liabilities

c) Total Assets − Internal Liabilities

d) Total Fund − Total External Liabilities

Answer : A

Question. In the final account of non-profit organisation, closing balance of cash will be recorded in

a) receipt and payment account only

b) balance sheet only

c) income and expenditure account

d) receipt and payment account and balance sheet both

Answer : D

Question. Find the cost of medicines consumed, if Opening stock of medicines Rs 30,000 Purchases during the year Rs 50,000 Closing stock Rs 20,000

a) Rs 80,000

b) Rs 60,000

c) Rs 50,000

d) Rs 40,000

Answer : B

Question. What amount of rent will be transferred to debit side of income and expenditure account, if rent paid during the year was Rs 70,000, rent outstanding at the end of the year Rs 6,000 and rent outstanding at the beginning of the year Rs 8,000?

a) Rs 60,000

b) Rs 68,000

c) Rs 70,000

d) Rs 72,000

Answer : B

Question. A non-profit organisation normally prepares …… before preparing balance sheet.

a) income and expenditure account

b) real account

c) trading account

d) None of the above

Answer : A

Question. Receipt and payment account generally shows

a) a debit balance

b) a credit balance

c) surplus and deficit

d) capital fund

Answer : A

Question. On 15th April, 2021, assets of Ashish club was as follows

Assets : Land and building Rs 1,00,000, Cash in hand Rs 30,000, Furniture Rs 65,000, Subscription receivable Rs 30,000.

Liabilities: Bank overdraft Rs 1,25,000, Outstanding salaries Rs 15,000. Capital fund as on 1st April, 2021 will be

a) Rs 85,000

b) Rs 75,000

c) Rs 1,10,000

d) Rs 8,000

Answer : A

Question. Calculate the amount of locker rent to be transferred to income and expenditure account.

Particulars 31st March, 2021 (Rs) 31st March, 2022 (Rs)

Outstanding Locker Rent 9,200 12,600

Advance Locker Rent 6,000 8,000

Locker rent received during the year 2021-22,

Rs 64,000.

a) Rs 65,400

b) Rs 66,500

c) Rs 66,000

d) Rs 73,000

Answer : A

Question. Opening balance of prize fund was Rs 16,400. During the year, donations received towards this fund amounted to Rs 7,700, while amount spent on prizes was Rs 6,150 and interest received on prize fund investment was Rs 2,000. The closing balanceof prize fund will be

a) Rs 28,250

b) Rs 32,250

c) Rs 19,950

d) Rs 15,950

Answer : C

Question. Receipt and payment account shows

a) income and expenditure

b) profit and loss

c) saving and deficit

d) cash receipts and payments

Answer : D

Question. Receipt and payment account is the summary of

a) bank balance

b) capital account

c) cash book

d) income and expenditure account

Answer : C

Question. What is an accounting treatment of cash received for life membership fees?

a) Debit in income and expenditure account

b) Credit in income and expenditure account

c) To be shown in liabilities column of balance sheet

d) To be shown in assets column of balance sheet

Answer : C

Question. The amount of subscriptions received in advance is shown in

a) liabilities side

b) assets side of balance sheet

c) payments side of receipts and payments account

d) None of the above

Answer : A

Question. Pass the journal entry for Royal Dance Club, whose deficit is calculated Rs 91,000 during 2019-20.

a) Income and Expenditure A/c Dr 91,000 To Deficit A/c 91,000

b) Deficit A/c Dr 91,000 To Income and Expenditure A/c 91,000

c) Cash A/c Dr 91,000 To Income and Expenditure A/c 91,000

d) None of the above

Answer : B

Question. Funds raised by non-profit organisation for its operation are credited to

a) Capital Fund of NPO

b) General fund of NPO

c) Reserve Fund of Bank

d) Both (a) and (b)

Answer : D

Question. There are 500 members in Diamond Club, paying an annual subscription of Rs 50 each. Subscription received during the year Rs 20,000 including Rs 2,000 for next year. Calculate amount to be shown as outstanding subscription.

a) Rs 7,000

b) Rs 5,000

c) Rs 25,000

d) Rs 18,000

Answer : A

Question. Uttam Charitable gets surplus from his income and expenditure account of Rs 65,000 in 2018-19. It will be recorded in debit side of the ……… account.

a) receipts and payments

b) income and expenditure

c) Both (a) and (b)

d) None of these

Answer : B

Question. Pass journal entry for subscription recorded in the income and expenditure account.

a) Income and Expenditure A/c Dr —

To Subscription A/c —

b) Subscription A/c Dr —

To Income and Expenditure A/c —

c) Bank A/c Dr —

To Income and Expenditure A/c —

d) None of the above

Answer : B

Question. A non-profit organisation normally prepares …… before preparing balance sheet.

a) income and expenditure account

b) real account

c) trading account

d) None of the above

Answer : A

Question. In the absence of any specific information, entrance fees may be treated as

a) revenue receipt

b) capital receipt

c) non-cash receipt

d) deferred receipt

Answer : A

Question. Profit or loss on sale of any fixed asset is treated as ……… in concern of NPOs.

a) capital income or loss

b) revenue income or loss

c) not considered while preparing account

d) None of the above

Answer : B

Question. Debit balance in receipts and payments account was shown as Rs 80,000, subscription received amounted to Rs 9,600 out of which Rs 3,000 is related to next year. According to you, what amount will be shown in receipts and payments account?

a) Rs 80,000

b) Rs 89,600

c) Rs 9,600

d) Rs 86,600

Answer : B

Question. Which of the following is/are account(s) in NPO where outstanding expenses, prepaid expenses, etc. are not recorded?

a) Income and expenditure account

b) Balance sheet

c) Receipts and payments account

d) All of the above

Answer : C

Question. How would you account for ‘subscription received in advance’ in the current year in the books of a non trading organisation?

Answer : Subscription received in advance is subtracted from subscription received during the year in Income and Expenditure A/C and shown as a liability in the closing Balance sheet.

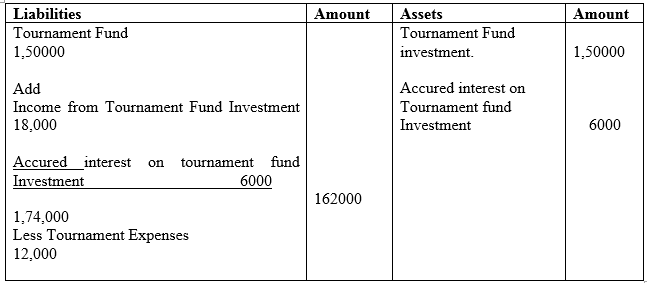

Question. Show the following information in the Balance Sheet of the Cosmos club as on 31st March 2007:-

Additional Information:-

Interest accrued on Tournament Fund Investment Rs. 6000.

Answer : Balance sheet of Cosmos Ltd.

As on 31st March, 2007

Question. How would you account for ‘subscription due to be received’ in the current year in the books of a non trading organisation?

Answer : Subscription due to be received is added with subscription received during the year in Income and Expenditure A/C and shown as an asset in the closing balance sheet.

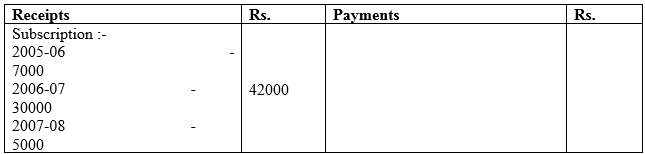

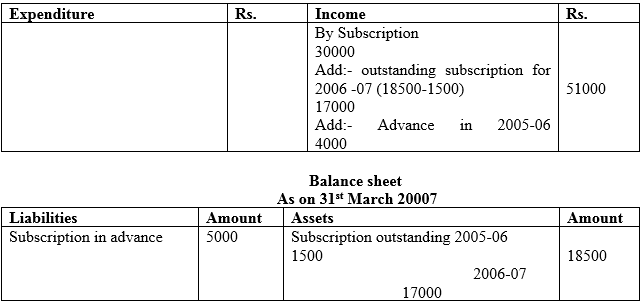

Question. From the following extracts of Receipts and Payments Account and the additional information given below, compute the amount of income from subscriptions and show us how they would appear in the Income and Expenditure Account for the year ending March 31, 2007and the Balance sheet on that date:-

Receipts and Payments A/C

For the year ending March 31, 2007

Additional information:-

(i) Subscription outstanding on March 31, 2006 Rs. 8500.

(ii) Total subscriptions outstanding on March 31, 2007 Rs. 18,500.

(iii) Subscriptions received in advance as on March 31, 2006 Rs. 4000.

Answer : Income and Expenditure A/C

For the year ending March 31, 2007

Question. Tournament fund appears in the books Rs. 15,000 and expenses on tournament during the year were Rs. 18000. How will you show this in format while preparing financial statement of a not-for-profit organisation?

Answer : Income and Expenditure A/C

For the year ended ………

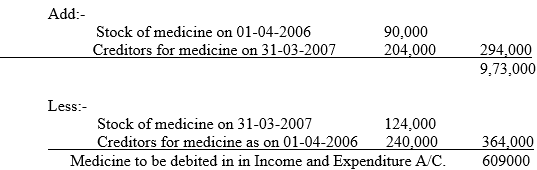

Question. Calculate the amount medicines to be debited in the Income and Expenditure Account of a Hospital on the basis of the following information:-

Amount paid for medicines during the year was Rs. 6,79000.

Answer : Amount paid for medicine during the year 6,79000

Question. What is meant by fund based accounting?

Answer : Fund based accounting is a book peeping technique where by separate self-balancing sets of assets, liability, income, expenses and fund balance accounts are maintained for each contribution for a specific purpose.

Question. State any two characteristics of Receipt and Payment Account.

Answer : (i) Receipts and Payments Account is a summary of Cash Book.

(ii) Non- cash expenses such as depreciation and outstanding expenses are not shown in Receipts and Payments Account.

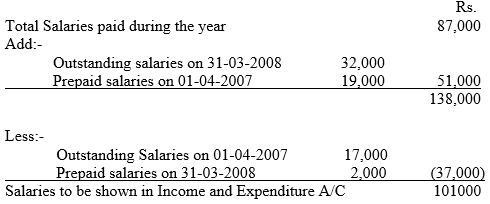

Question. From the following particulars of a club, calculate the amount of salaries to be shown in Income and expenditure account for the year ended 31 March, 2008:-

Total salaries paid during the year 2007-08 Rs. 87,000

Outstanding salaries on 01-04-2007 Rs. 17,000

Prepaid salaries on 01-04-2007 Rs. 19,000

Outstanding salaries on 31-03-2008 Rs. 32,000

Prepaid salaries on 31-03-2008 Rs 20,000

Answer :Calculation of salaries to be shown in Income and Expenditure A/C for the year ended March 31, 2008:-

Question. Distinguish between Receipts and Payments A/C and Income and expenditure A/C.

Answer : Difference between Receipts and Payments and Income and Expenditure.

![]()

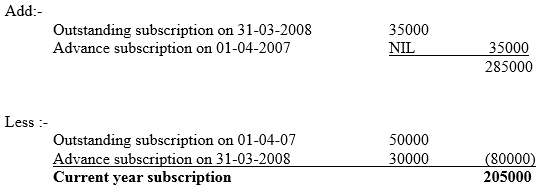

Question. As per Receipt and Payments account for the year ended on March 31, 2008, the subscription received were Rs. 2,50,000. Addition information given is as follows:-

(i) Subscriptions outstanding on 01-04-2007 Rs. 50,000.

(ii) Subscription outstanding on 31-03-2008 Rs. 35,000.

(iii)Subscription Received in advance as on 31-03-2008 Rs. 30000.

Ascertain the amount of income from subscription for the year 2007-08.

Answer : Calculation of current year subscription to be shown in Income and Expenditure A/C for the year ended March 31, 2008 :-

Total subscription received during the year 250000

Question. Give to main sources of income of a ‘Not for profit organisation’.

Answer : (i) Subscription

(ii) Donation.

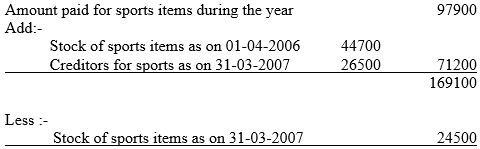

Question. Calculate the amount to be debited to Income and Expenditure account under the heading sports items for the year 2006-07 in respect of the Osmosis club:-

Stock of sports items on 01-04-2006 Rs. 44,700

Stock of sports items on 31-03-2007 Rs. 24,500

Paid for sports items during the year Rs. 97,900

Creditors for supplies of sports items 31-03-2007 Rs. 26,500.

Answer :

Sports items to be debited in the Income and expenditure A/C 144600

1. Bilochpur Ltd. has an outstanding balance of Rs. 4,00,000, 8% Debentures of Rs. 100 each. The Board of Directors decided to purchase 1, 00,000 debentures at a price of Rs. 96 for investment purposes but after few months they took a decision to sell them @ Rs. 99 in the market. Record necessary entries to show above transactions.

2. (a) (i) Z Ltd. purchased a building for Rs. 2,20,000. Half of the payment was made in cash and the balance by issue of 12% debentures at premium of 10% Pass the necessary journal entries in the books of Z Ltd.

(ii) A Ltd. issued Rs. 2,00,000. 12%. Debentures as collateral security. Pass necessary journal entries in the books of A Ltd.

(b) A company had issued 10% Rs. 100 debentures amounting to Rs. 80,000 redeemable at the option of the company by drawing at par or by purchase in the open market. The company decides to redeem Rs. 20,000 debentures by the purchase of Rs. 16,000 debentures in the open market at Rs. 98 each and draw Rs. 4,000 debentures.

Assuming that company had sufficient balance in the Debenture Redemption Reserve before the purchase of own debentures, pass the necessary journal entries in the books of the company.

3. X Ltd. invited applications for 2,00,000 equity shares of Rs. 10 each at a premium of Rs. 2 per share payable as to Rs. 2 on application, Rs. 5 on allotment including premium, Rs. 2 first call & Rs. 3 on final call.

Applications were received for 3,00,000 shares. Applications for 60,000 shares were rejected and pro-rata allotment was made to the remaining applicants. Ram, who applied for 9,600 shares, failed to pay allotment and two calls and Shyam the holder of 12,000 shares, failed to pay two calls. These shares were forfeited. Subsequently, all these shares were reissued at Rs.8 per share as fully paid up. Pass necessary journal entries in the books of X Ltd.

4. Beriwal Ltd. at present is having an equity share capital of Rs. 1, 00,000. The face value of one equity share is Rs. 10.It intends to make further issue of equity as follows:

(I) General public-10,000 equity shares at a discount of Re. 1 per share. Terms of issue:

Application Rs.2, Allotment Rs.2, First and Final Call Rs.5

The shares issued to the public were oversubscribed by 1,000 shares. The directors have refunded the entire excess application money. Jatin holding 200 shares failed to pay the final call and these shares have been forfeited after having notices of forfeited etc. Later these shares were issued to Bobby of maximum discount.

(II) The company acquired assets worth Rs. 9,00,000, the payment was settled by the issue of sufficient number of equity shares at a discount of Re. 1 per share. You are required to

(a) Give journal entrees to record the above Share Capital transactions including forfeiture and reissue.

(b) Give journal entries in respect of purchase of assets.

Please click the below link to access CBSE Class 12 Accountancy Revision Assignment Set D

| CBSE Class 12 Accountancy Accounting for Not for Profit Organisation Assignment |

CBSE Class 12 Accountancy Part 1 Chapter 1 Accounting For Not For Profit Organisation Assignment

Access the latest Part 1 Chapter 1 Accounting For Not For Profit Organisation assignments designed as per the current CBSE syllabus for Class 12. We have included all question types, including MCQs, short answer questions, and long-form problems relating to Part 1 Chapter 1 Accounting For Not For Profit Organisation. You can easily download these assignments in PDF format for free. Our expert teachers have carefully looked at previous year exam patterns and have made sure that these questions help you prepare properly for your upcoming school tests.

Benefits of solving Assignments for Part 1 Chapter 1 Accounting For Not For Profit Organisation

Practicing these Class 12 Accountancy assignments has many advantages for you:

- Better Exam Scores: Regular practice will help you to understand Part 1 Chapter 1 Accounting For Not For Profit Organisation properly and you will be able to answer exam questions correctly.

- Latest Exam Pattern: All questions are aligned as per the latest CBSE sample papers and marking schemes.

- Huge Variety of Questions: These Part 1 Chapter 1 Accounting For Not For Profit Organisation sets include Case Studies, objective questions, and various descriptive problems with answers.

- Time Management: Solving these Part 1 Chapter 1 Accounting For Not For Profit Organisation test papers daily will improve your speed and accuracy.

How to solve Accountancy Part 1 Chapter 1 Accounting For Not For Profit Organisation Assignments effectively?

- Read the Chapter First: Start with the NCERT book for Class 12 Accountancy before attempting the assignment.

- Self-Assessment: Try solving the Part 1 Chapter 1 Accounting For Not For Profit Organisation questions by yourself and then check the solutions provided by us.

- Use Supporting Material: Refer to our Revision Notes and Class 12 worksheets if you get stuck on any topic.

- Track Mistakes: Maintain a notebook for tricky concepts and revise them using our online MCQ tests.

Best Practices for Class 12 Accountancy Preparation

For the best results, solve one assignment for Part 1 Chapter 1 Accounting For Not For Profit Organisation on daily basis. Using a timer while practicing will further improve your problem-solving skills and prepare you for the actual CBSE exam.

You can download free PDF assignments for Class 12 Accountancy Chapter Part 1 Chapter 1 Accounting For Not For Profit Organisation from StudiesToday.com. These practice sheets have been updated for the 2025-26 session covering all concepts from latest NCERT textbook.

Yes, our teachers have given solutions for all questions in the Class 12 Accountancy Chapter Part 1 Chapter 1 Accounting For Not For Profit Organisation assignments. This will help you to understand step-by-step methodology to get full marks in school tests and exams.

Yes. These assignments are designed as per the latest CBSE syllabus for 2026. We have included huge variety of question formats such as MCQs, Case-study based questions and important diagram-based problems found in Chapter Part 1 Chapter 1 Accounting For Not For Profit Organisation.

Practicing topicw wise assignments will help Class 12 students understand every sub-topic of Chapter Part 1 Chapter 1 Accounting For Not For Profit Organisation. Daily practice will improve speed, accuracy and answering competency-based questions.

Yes, all printable assignments for Class 12 Accountancy Chapter Part 1 Chapter 1 Accounting For Not For Profit Organisation are available for free download in mobile-friendly PDF format.