Read and download the CBSE Class 12 Accountancy Admission of a Partner Assignment for the 2026-27 academic session. We have provided comprehensive Class 12 Accountancy school assignments that have important solved questions and answers for Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner. These resources have been carefuly prepared by expert teachers as per the latest NCERT, CBSE, and KVS syllabus guidelines.

Solved Assignment for Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner

Practicing these Class 12 Accountancy problems daily is must to improve your conceptual understanding and score better marks in school examinations. These printable assignments are a perfect assessment tool for Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner, covering both basic and advanced level questions to help you get more marks in exams.

Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner Class 12 Solved Questions and Answers

MCQ Questions for NCERT Class 12 Accountancy Reconstitution of Partnership Firm – Admission of a Partner

Question: The balance in the investment fluctuation fund after meeting the fall in book value of investment, at the time of admission of partner will be transferred to:

(a) Revaluation account

(b) Capital accounts of old partners

(c) General reserve

(d) Capital account of all partners

Answer: B

Question: Revaluation account is a :

(a) Real account

(b) Nominal account

(c) Personal account

(d) None of the above

Answer: B

Question: If the new partner brings any additional cash other than his capital contributions then it is termed as:

(a) Capital

(b) Reserves

(c) Profits

(d) Premium for goodwill

Answer: D

Question: When new partner brings cash for goodwill, the amount is credited to:

(a) Realization account

(b) Cash account

(c) Premium for goodwill account

(d) Revaluation account

Answer: C

Question: If the new partner brings his share of goodwill in cash, it will be shared by old partners in:

(a) Sacrificing ratio

(b) Old profit sharing ratio

(c) New ratio

(d) Capital ratio

Answer: A

Question: Goodwill of the firm is valued at Rs..100000. Goodwill also appears in the books at Rs.50000. C is admitted for ¼ share. The amount of goodwill to be brought in by C will be:

(a) Rs.20000

(b) Rs.25000

(c) Rs.30000

(d) Rs.40000

Answer: B

Question: A and B are partners sharing profits in the ratio of 3:2. They admit C for ¼ Rs.30000 for his share of goodwill. The total value of the goodwill of the firm will be:

(a) Rs.150000

(b) Rs.120000

(c) Rs.100000

(d) Rs.160000

Answer: B

Question: A and B are partners sharing profits and losses in the ratio of 3:2. C is admitted for 1/5 share in profits which he gets from A. New profit sharing ratio will be:

(a) 12:8:5

(b) 8:12:5

(c) 2:2:1

(d) 2:2:2

Answer: C

Question: Ajay and Vijay are partners sharing profits in the ratio of 2:1. Ajay’s son Anil was admitted for ¼ share of which 1/8 was gifted by Ajay to his son. The remaining was contributed by Vijay. Goodwill of the firm is valued at Rs..40,000. How much of the goodwill will be credited to each of old partners’ capital account:

(a) Rs.2500

(b) Rs.5000

(c) Rs.20000

(d) None of the above

Answer: B

Question: The credit balance of profits and loss account appears in the books at the time of admission of partner will be transferred to:

(a) Profit and loss Appropriation account

(b) All partners’ capital account

(c) Old partners’ capital account

(d) Revaluation account

Answer: C

Question: On the admission of a new partner, increase in the value of assets is debited to :

(a) Profit and loss adjustment account

(b) Assets account

(c) Old partners’ capital account

(d) None of the above

Answer: B

Question: Yash and Manan are partners sharing profits in the ratio of2:1. They admit Kushagra into partnership for 25% share of profit. Kushagra acquired the share from old partners in the ratio of 3:2. The new profit sharing ratio will be:

(a) 14:31:15

(b) 3:2:1

(c) 31:14:15

(d) 2:3:1

Answer:C

Question: Which of the following is not the reconstitution of partnership?

(a) Admission of a partner

(b) Dissolution of Partnership

(c) Change in Profit Sharing Ratio

(d) Retirement of a partner

Answer: B

Question: On the admission of a new partner:

(a) Old partnership is dissolved

(b) Both old partnership and firm are dissolved

(c) Old firm is dissolved

(d) None of the above

Answer: A

Question: Sacrificing ratio is used to distribute ____________ in case of admission of a partner.

(a) Goodwill

(b) Revaluation Profit or Loss

(c) Profit and Loss Account (Credit Balance)

(d) Both b and c

Answer: A

Question: At the time of admission of a partner, undistributed profits appearing in the balance sheet of the old firm is transferred to the capital accounts of :

(a) Old partners in old profit sharing ratio

(b) Old partners in new profit sharing ratio

(c) All the partner in the new profit sharing ratio

(d) None of the above

Answer: B

Question: Himanshu and Naman share profits & losses equally. Their capitals were Rs..1,20,000 and Rs.80,000 respectively. There was also a balance of Rs.60,000 in General reserve and revaluation gain amounted to Rs.15,000. They admit friend Ashish with 1/5 share. Ashish brings Rs.90,000 as capital. Calculate the amount of goodwill of the firm.

a. Rs.1,00,000

b. Rs. 85,000

c. Rs.20,000

d. None of the above

Answer: B

Question: A and B are partners sharing profit and losses in ratio of 5:3. C is admitted for 1/4th share. On the date of reconstitution, the debtors stood at Rs. 40,000, bill receivable stood at Rs.10,000 and the provision for doubtful debts appeared at Rs.4000. A bill receivable, of Rs. 10,000 which was discounted from the bank, earlier has been reported to be dishonored. The firm has sold, the debtor so arising to a debt collection agency at a loss of 40%. If bad debts now have arisen for Rs. 6,000 and firm decides to maintain provisions at same rate as before then amount of Provision to be debited to Revaluation Account would be:

(a) Rs. 4,400

(b) Rs.4,000

(c) Rs. 3,400

(d) None of the above

Answer: C

Question: Which of the following is not true with respect to Admission of a partner?

(a) A new partner can be admitted if it is agreed in the partnership deed.

(b) If all the partners agree, a new partner can be admitted.

(c) A new partner has to bring relatively higher capital as compared to the existing partners

(d) A new partner gets right in the assets of the firm

Answer: C

Question. Which amongst the following adjustment(s) is/are required at the time of admission of a new partner?

a) Computation of new profit sharing ratio and sacrificing ratio

b) Adjustment for goodwill

c) Revaluation of assets

d) All of these

Answer : D

Question. Asha and Nisha are partners’ sharing profit in the ratio of 2 : 1. Asha’s son Ashish was admitted for 1/4 share of which 1/8 was gifted by Asha to her son. The remaining was contribited by Nisha. Goodwill of the firm is valued at Rs 40,000. How much of the goodwill be credited to the old partners’ capital account?

a) Rs 2,500 each

b) Rs 5,000 each

c) Rs 20,000 each

d) None of these

Answer : C

Question. ‘A’ and ‘B’ share profits in the ratio of 3 : 2. ‘A’s’ capital is Rs 40,000, ‘B’s’ capital is Rs 30,000. ‘C’ is admitted for 1/5th share in profits. What is the amount of capital which ‘C’ should bring?

a) Rs 17,500

b) Rs 16,000

c) Rs 1,00,000

d) Rs 64,000

Answer : A

Question. Reserve or general reserve appearing in the balance sheet will be divided among old partners during admission in ………… ratio.

a) gaining

b) new

c) sacrificing

d) old

Answer : D

Question. Amount of premium brought in by a new partner will be shared by the existing partners in ……… .

a) old ratio

b) new ratio

c) gaining ratio

d) sacrificing ratio

Answer : D

Question. Which of the following is not a right of newly admitted partner?

a) Right to share profits of firm

b) Right to inspect the books of accounts

c) Right to participate in affairs of busniess

d) None of the above

Answer : D

Question. The balance of memorandum revaluation account (second part), is transferred to the capital accounts of the partners in

a) new profit sharing ratio

b) old profit sharing ratio

c) capital ratio

d) sacrificing ratio

Answer : A

Question. ‘X’ and ‘Y’ are partners sharing profits equally. ‘Z’ was admitted for 1/5 share. Calculate new profit sharing ratio.

a) 2 : 3 : 1

b) 3 : 3 : 1

c) 6 : 5 : 2

d) 2 : 2 : 1

Answer : D

Question. A firm has an unrecorded investment of Rs 5,000. Entry in the firm’s journal on admission of a partners will

a) Unrecorded Investment A/c Dr 5,000

To Revaluation A/c 5,000

b) Partners’ Capital A/c Dr 5,000

To Unrecorded Investment A/c 5,000

c) Revaluation A/c Dr 5,000

To Unrecorded Investment A/c 5,000

d) None of the above

Answer : A

Question. ‘A’ and ‘B’ are partners in a firm sharing profits in 3:2 ratio. They admitted ‘C’ as a new partner and the new profit sharing ratio will be 2:1:1. ‘C’ brought in Rs 40,000 as premium for goodwill for it’s share. What will be the journal entry for the premium of goodwill shared by old partners as per sacrificing ratio?

a) Premium for Goodwill A/c Dr 40,000

To A’s Capital A/c 16,000

To B’s Capital A/c 24,000

b) A’s Capital A/c Dr 16,000

B’s Capital A/c Dr 24,000

To Premium for Goodwill A/c 40,000

c) Premium for Goodwill A/c Dr 40,000

To Bank A/c 40,000

d) Bank A/c Dr 40,000

To Premium for Goodwill A/c 40,000

Answer : A

Question. X and Y share profits in the ratio pf 3 : 2. Z was admitted as a partner who gets 1/5 share. New profit sharing ratio, if Z acquires 3/20 from X and 1/20 from Y would be

a) 9 : 7 : 4

b) 8 : 8 : 4

c) 6 : 10 : 4

d) 10 : 6 : 4

Answer : A

Question. At the time of admission of a new partner, general reserve appearing in the old balance sheet is transferred to

a) all partners’ capital account

b) new partners’ capital account

c) old partners’ capital account

d) None of the above

Answer : C

Question. At the time of admission of a new partner in the firm, the new partner compensates the old partners for their loss of share in the super-profits of the firm for which he brings in an additional amount which is known as ……… .

a) capital share

b) premium for goodwill

c) Both (a) and (b)

d) None of these

Answer : B

Question. Sacrificing ratio is computed

a) when profit sharing ratio is changed

b) when a new partner is admitted

c) Both (a) and (b)

d) when a partner leave the firm

Answer : C

Question. On the admission of a new patner, increase in the value of assets is debited to

a) profit and loss adjustment account

b) assets account

c) old partners’ capital account

d)None of the above

Answer : A

Question. ‘A’ and ‘B’ carry on business and share profits and losses in the ratio of 3 : 2. Their respective capitals are Rs 1,20,000 and Rs 54,000. ‘C’ is admitted for 1/5th share in profit and brings Rs 1,20,000 as his share of capital. Capitals of ‘A’ and ‘B’ to be adjusted according to ‘C’s’ share.

Calculate the amount required to bring by ‘A’.

a) Rs 30,000

b) Rs 1,68,000

c) Rs 60,000

d) Rs 28,000

Answer : B

Question. At the time of admission of a partner, undistributed profits appearing in the balance sheet of the old firm is transferred to the capital account of

a) old partners in old profit sharing ratio

b) old partners in new profit sharing ratio

c) all the partner in the new profit sharing ratio

d) None of the above

Answer : A

Question. ……… of a new partner results in reconstitution of the firm.

a) Admission

b) Retirement

c) Death

d) Change in profit sharing ratio

Answer : A

Question. A new partner is admitted in the firm

a) for procuring additional capital

b) for acquiring additional managerial skills

c) to benefit from the goodwill of the admitted partner

d) All of the above

Answer : D

Question. For which of the following situations, the old profit sharing ratio of partners is used at the time of admission of a new partner?

a) When new partner brings only a part of his share of goodwill.

b) When new partner is not able to bring his share of goodwill.

c) When at the time of admission, goodwill already appears in the balance sheet.

d) When new partner brings his share of goodwill in cash.

Answer : B

Question. If at the time of admission, there is some unrecorded liabilitity, it will be

a) debited to revaluation account

b) credited to revaluation account

c) debited to goodwill account

d) credited to partners’ capital account

Answer : A

Question. At the time of admission, incoming partner become liable for the …… of the firm and also acquires right on the ………… .

a) assets, liabilities

b) goodwill, capital

c) liabilities, assets

d) None of these

Answer : C

Question. On account of admission, the assets are revalued and liabilities are reassessed in

a) partners’ capital account

b) revaluation account

c) realisation account

d) balance sheet

Answer : B

Question. …… goodwill is the excess of desired total capital of firm over the actual combined capital of all partners.

a) Premium

b) Share

c) Hidden

d) Old

Answer : C

Question. ‘A’ and ‘B’ are partners sharing profits and losses in the ratio of 5 : 3. On admission, ‘C’ brings Rs 70,000 cash and Rs 48,000 against goodwill. New profit sharing ratio between ‘A’, ‘B’ and ‘C’ is 7 : 5 : 4. The sacrificing ratio among ‘A’ and ‘B’ is

a) 4 : 1

b) 4 : 7

c) 5 : 4

d) 3 : 1

Answer : D

Question. A and B are partners sharing profits in the ratio of 3 : 1. They admit C for 1/4 share in the future profits. The new profit sharing ratio will be

a) A 9/16, B 3/16, C 4/16

b) A 8/16, B 4/16, C 4/16

c) A 10/16, B 2/16, C 4/16

d) A 8/16, B 9/16, C 10/16

Answer : A

Question. A, B and C are partners’ in a firm. If D is admitted as a new patner

a) old firm is dissolved

b) old firm and old partnership is dissolved

c) old partnership is reconstituted

d) None of the above

Answer : C

Question. The new partner, at the time of admission, may acquire his share from old partners in

a) old profit sharing ratio

b) some agreed ratio

c) particular fraction from some of the partners

d) All of the above

Answer : D

Question. A and B share profts and losses in the ratio of 3 : 1, C is admitted into partnership for 1/4 share. The sacrificing ratio of A and B is

a) equal

b) 3 : 1

c) 2 : 1

d) 3 : 2

Answer : B

Question. Taxation fund should never be distributed among the old partners at the time of admission of partners.

a) True

b) False

c) Partially true

d) Can’t say

Answer : A

True/ False:

Question: “As per Section 26 of the Indian Partnership Act, 1932, a person can be admitted as a new partner if it is agreed in the Partnership Deed”.

Answer: False

Question:“Unless agreed otherwise, Sacrificing Ratio of the old partners will be the same as their Old Profit Sharing Ratio”.

Answer: True

Question: “A newly admitted partner cannot pay his share of the goodwill to the sacrificing partners privately”.

Answer:False

Question: “At the time of admission, old partnership comes to an end”.

Answer: True

Question: New partner may or may not contribute capital at the time of admission.

Answer:True

Question: The goodwill brought at the time of admission of partner will be distributed among all the partners in new profit sharing ratio.

Answer: False

Question: New partner may bring his share of goodwill premium in kind.

Answer:True

Question: In the case of admission of a partner, all existing partners sacrifice.

Answer: False

Question: At the time of admission of partner, the partnership firm is dissolved.

Answer:False

Question: Increase in provision for doubtful debts will credited to revaluation account.

Answer: False

Fill in the blanks

Question: Vinay and Naman are partners sharing profit in the ratio of 4:1. Their capitals were Rs..90000 and Rs.70000 respectively. They admitted Pratik for 1/3 share in the profits. Pratik brings Rs.100000 as his capital. The value of firm’s goodwill be……

Answer: Rs.40000……..

Question: Goodwill appearing in the books oat the time of admission of a new partner is written off by debiting …………..and crediting ………….

Answer: Old partners’ capital accounts, goodwill account

Question: When the value of goodwill of the firm is not given but has to be inferred on the basis of net worth of the firm, it is called…………….

Answer: Hidden goodwill

Question: On the admission of a new partner, after revaluation has been done, the value of assets and liabilities appear in the books of the firm at………….

Answer: 4. their current value

Question: General reserve account indicates ………..and shows ………..balance.

Answer: Accumulated profits, credit

Question: Debit balance in the profit and loss account indicates…………….

Answer: Accumulated loss

Question: Gain or loss arising from revaluation is shared by ………..partners in …………ratio.

Answer: Old partners, old profit sharing ratio

Question: A and B are partners sharing profits equally. They admit C for 1/3 share in profits. A debtor whose dues of Rs.5000 were written off as bad debts, paid Rs.4000 in full settlement.

Bad debts recovered Rs.4000 will be debited to …………and credited to ……………

Answer: Cash account, revaluation account

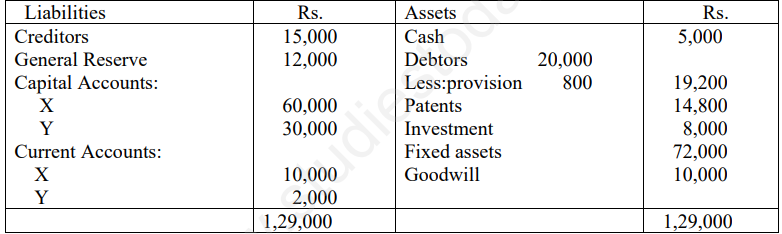

They admit C into partnership from 1st April, 2010.The terms of agreement are as under:

a. C to bring in Rs.6,000 as capital and rs.4,800 for goodwill in order to get 2/7th share in profit.

b. Rs.4,800 paid by C to be credited to the loan accounts of A and B in respective proportions.

c. Freehold premises is undervalued by Rs.5,000.

d. Machinery and Plant is overvalued by Rs.500.

e. Stock to be discounted at 10% and provision for doubtful debts be reduced by Rs.1,000.

f. Investment are to be brought down at their market price being Rs.3,200. Prepare revaluation, capital a/c and balance sheet.

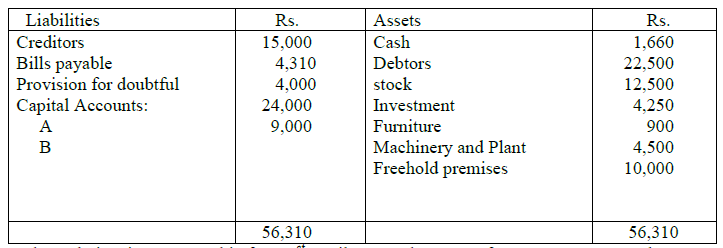

6. X and Y are in partnership, sharing profits in the ratio of 5:3 respectively.Their balance sheet is as follows:

Z admitted into partnership on the following terms:-

a. The new profit sharing ratio will be 4:3:2 between X, Y and Z respectively.

b. Z’s loan should be treated as his capital.

c. Goodwill of the firm is valued at Rs.27,000.

d. Rs.8,000 of investment were to be taken over by X and Y in their profit sharing ratio.

e. Stock be reduced by 10%.

f. Provision for doubtful debts should be@5% on debtors and a provision for discount on debtors @2% should also be made.

g. X is to withdrawn Rs.6,000 in cash. Prepare necessary accounts

7. The following is the Balance sheet of R and S who share profits in the ratio of 2:1.

Please click the below link to access CBSE Class 12 Accountancy Admission of a Partner Assignment

Free study material for Accountancy

CBSE Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner Assignment

Access the latest Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner assignments designed as per the current CBSE syllabus for Class 12. We have included all question types, including MCQs, short answer questions, and long-form problems relating to Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner. You can easily download these assignments in PDF format for free. Our expert teachers have carefully looked at previous year exam patterns and have made sure that these questions help you prepare properly for your upcoming school tests.

Benefits of solving Assignments for Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner

Practicing these Class 12 Accountancy assignments has many advantages for you:

- Better Exam Scores: Regular practice will help you to understand Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner properly and you will be able to answer exam questions correctly.

- Latest Exam Pattern: All questions are aligned as per the latest CBSE sample papers and marking schemes.

- Huge Variety of Questions: These Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner sets include Case Studies, objective questions, and various descriptive problems with answers.

- Time Management: Solving these Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner test papers daily will improve your speed and accuracy.

How to solve Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner Assignments effectively?

- Read the Chapter First: Start with the NCERT book for Class 12 Accountancy before attempting the assignment.

- Self-Assessment: Try solving the Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner questions by yourself and then check the solutions provided by us.

- Use Supporting Material: Refer to our Revision Notes and Class 12 worksheets if you get stuck on any topic.

- Track Mistakes: Maintain a notebook for tricky concepts and revise them using our online MCQ tests.

Best Practices for Class 12 Accountancy Preparation

For the best results, solve one assignment for Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner on daily basis. Using a timer while practicing will further improve your problem-solving skills and prepare you for the actual CBSE exam.

FAQs

You can download free PDF assignments for Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner from StudiesToday.com. These practice sheets have been updated for the 2026-27 session covering all concepts from latest NCERT textbook.

Yes, our teachers have given solutions for all questions in the Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner assignments. This will help you to understand step-by-step methodology to get full marks in school tests and exams.

Yes. These assignments are designed as per the latest CBSE syllabus for 2026. We have included huge variety of question formats such as MCQs, Case-study based questions and important diagram-based problems found in Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner.

Practicing topicw wise assignments will help Class 12 students understand every sub-topic of Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner. Daily practice will improve speed, accuracy and answering competency-based questions.

Yes, all printable assignments for Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner are available for free download in mobile-friendly PDF format.