Read and download the CBSE Class 12 Accountancy Reconstitution Of Partnership Assignment Part A for the 2026-27 academic session. We have provided comprehensive Class 12 Accountancy school assignments that have important solved questions and answers for Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner. These resources have been carefuly prepared by expert teachers as per the latest NCERT, CBSE, and KVS syllabus guidelines.

Solved Assignment for Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner

Practicing these Class 12 Accountancy problems daily is must to improve your conceptual understanding and score better marks in school examinations. These printable assignments are a perfect assessment tool for Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner, covering both basic and advanced level questions to help you get more marks in exams.

Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner Class 12 Solved Questions and Answers

MCQ Questions for NCERT Class 12 AccountancyReconstitution of Partnership Firm – Admission of a Partner

Question: As per _________ , only purchased goodwill can be shown in the Balance Sheet.

(a) AS 37

(b) AS 26

(c) Section 37

(d) AS 37

Answer: B

Question: A, and B are partners sharing profits in the ratio of 2:3. Their balance sheet shows machinery at Rs.2,00,000; stock Rs.80,000, and debtors at Rs.1,60,000. C is admitted and the new profit sharing ratio is 6:9:5. Machinery is revalued at Rs.1,40,000 and a provision is made for doubtful debts @5%. A’s share in loss on revaluation amount to Rs.20,000. Revalued value of stock will be:

(a) Rs.62,000

(b) Rs.1,00,000

(c) Rs.60,000

(d) Rs.98,000

Answer: C

Question: Heena and Sudha share Profit & Loss equally. Their capitals were Rs.1,20,000 and Rs.80,000 respectively. There was also a balance of Rs.60,000 in General reserve and revaluation gain amounted to Rs.15,000. They admit friend Teena with 1/5 share. Teena brings Rs.90,000 as capital. Calculate the amount of goodwill of the firm.

(a) Rs..85,000

(b) Rs.1,00,000

(c) Rs..20,000

(d) None of the above

Answer: A

Question: If at the time of admission if there is some unrecorded liability, it will be -------------to -- ------------ Account.

(a) Debited, Revaluation

(b) Credited, Revaluation

(c) Debited, Goodwill

(d) Credited, Partners’ Capital

Answer: A

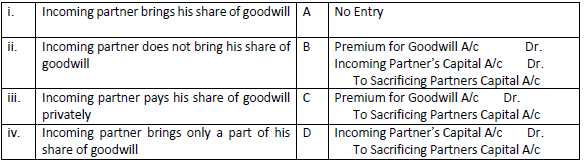

Question: Match the following:

(a) i- B, ii-C, iii-A, iv-D

(b) i- D, ii-B, iii-A, iv-C

(c) i- D, ii-C, iii-A, iv-B

(d) i- D, ii-C, iii-B, iv-A

Answer: C

Question: Sacrificing ratio is calculated because:

(a) Profit shown by Revaluation Account can be credited to sacrificing partners

(b) Goodwill brought in by the incoming partner can be credited to the new partner

(c) Goodwill brought in by the incoming partner can be credited to the sacrificing partners

(d) Both a and

Answer: C

Question: Match the following with respect to journal entries for treatment of goodwill.

(a) i- B, ii-C, iii-A, iv-D

(b) i- C, ii-D, iii-A, iv-B

(c) i- D, ii-C, iii-A, iv-B

(d) i- D, ii-C, iii-B, iv-A

Answer: B

Question: Share of goodwill brought by the new partner in cash is shared by old partners in:

(a) ratio of sacrifice

(b) old profit sharing ratio

(c) new profit sharing ratio

(d) none of the above

Answer: A

Question: A and B are partners sharing profits in the ratio of 3:1. C is admitted to partnership firm for 1/4th share. The sacrificing ratio of A and B will be:

(a) Equal

(b) 2:1

(c) 3:2

(d) 3:1

Answer: D

Question: A and B are partners sharing profits and losses in the ratio of 3:2. A’s capital is Rs.1,20,000 and B’s capital is Rs.60,000. they admit C for 1/5th share of profits. C should bring as his capital:

(a) Rs.36,000

(b) Rs.48,000

(c) Rs.58,000

(d) Rs.45,000

Answer: D

Question: At the time of admission of a partner, Employees Provident Fund is:

(a) Distributed to partners in the old profit sharing ratio

(b) Distributed to partners in the new profit sharing ratio

(c) Adjusted through gaining ratio

(d) None of the above

Answer: D

Question: If at the of admission, some balance of profit and loss account appears in the books, it will be transferred to :

(a) Profit and loss adjustment account

(b) All partners’ capital account

(c) Old partners’ capital account

(d) Revaluation account

Answer: C

Question: A and B are partners in a firm sharing profits in 4:1. They admit Pal as a new partner for ¼ share in the profits, which he acquired wholly from A. New profit sharing ratio of the partners is:

(a) 4:1:1

(b) Equally

(c) 11:4:5

(d) none of the above

Answer: C

Question: When new partner does not bring his share of goodwill in cash, the amount is debited to:

(a) Current account of the new partner

(b) Premium account

(c) Capital account of the old partners

(d) Cash account

Answer: C

Question: A, B, C, and D are partners. A and B share 2/3rd of profits equally and C and D share remaining profits in the ratio of 3:2. Find the profit sharing ratio of A, B, C and D.

(a) 5:5:3:2

(b) 7:7:6:4

(c) 2.5:2.5:8:6

(d) 3:9:8:3

Answer: A

True/ False:

Question: Reserve and accumulated profits are distributed in old profit sharing ratio at the time of admission of a partner.

Answer: True

Question: Claim of workmen compensation if more than workmen compensation reserve, is debited to revaluation account.

Answer: True

Question: New partner brings goodwill in the firm to get share in the past profits.

Answer: False

Question: Hidden goodwill arises when total capital is computed based on the new partner’s capital is less than total capitals of remaining partners after all adjustments.

Answer: False

Question: At the time of admission, reserves may be carried forwarded by the partners.

Answer: True

Fill in the blanks

Question: If, at the time of admission of a new partner, provision for doubtful debts is to be reduced, it shall be …………to profit and loss adjustment account.

Answer: credited capital accounts

Question: At the time of admission, the assets are revalued and liabilities are reassessed. The increase or decrease in the values is debited or credited in ……………..

Answer: Revaluation account

Question: In the case of downward revaluation of an asset, revaluation account is ………………

Answer: Debited

Question: If the revaluation account finally shows a debit balance then it indicates ………….., which will be transferred to …………

Answer: Net loss, debit side of old partners’ capital accounts

Question: Revaluation account shows ………….in the values of assets and liabilities.

Answer: Increase or decrease

Question: In case of upward revaluation of a liability, revaluation account is …………….

Answer: Debited

Question: On what occasions does the need for valuation of goodwill arise?

Question: Why is it necessary to revalue assets and liabilities at the time of admission of a new partner?

Question: What is meant by sacrificing ratio?

Question: State two occasions when sacrificing ratio may be applied.

Question: A business has earned average profit of Rs. 60,000 during the last few years. The assets of the business are Rs. 5,40,000 and its external liabilities are Rs. 80,000. The normal rate of return is 10%. Calculate the value of goodwill on the basis of capitalisation of super profits.

Question: The capital of a firm of Arpit and Prajwal is Rs. 10,00,000. The market rate of return is 15% and the goodwill of the firm has been valued Rs. 1,80,000 at two years purchase of super profits. Find the average profits of the firm.

Question: The average profits for last 5 years of a firm are Rs. 20,000 and goodwill has been worked out Rs. 24,000 calculated at 3 years purchase of super profits. Calculate the amount of capital employed assuming the normal rate of interest is 8 %.

Question: Rahul and Sahil are partners sharing profits together in the ratio of 4:3. They admit Kamal as a new partner. Rahul surrenders 1/4th of his share and Sahil surrenders 1/3rd of his share in favour of Kamal. Calculate the new profit sharing ratio.

Question: Ajay and Naveen are partners sharing profits in the ratio of 5:3. Surinder is admitted in to the firm for 1/4th share in the profit which he acquires from Ajay and Naveen in the ratio of 2:1. Calculate the new profit sharing ratio.

Question: A and B were partners sharing profits in the ratio of 3:2. A surrenders 1/6th of his share and B surrenders 1/4th of his share in favour of C, a new partner. What is the new ratio and the sacrificing ratio.

Question: Aarti and Bharti are partners sharing profits in the ratio of 5:3. They admit Shital for 1/4th share and agree to share between them in the ratio of 2:1 in future. Calculate new and sacrificing ratio.

Question: X and Y divide profits and losses in the ratio of 3:2. Z is admitted in the firm as a new partner with 1/6th share, which he acquires from X and Y in the ratio of 1:1. Calculate the new profit sharing ratio of all partners.

Question: Rakhi and Parul are partners sharing profits in the ratio of 3:1. Neha is admitted as a partner. The new profit sharing ratio among Rakhi, Parul and Neha is 2:3:2. Find out the sacrificing ratio.

Question: X and Y are partners sharing profits in the ratio of 5:4. They admit Z in the firm for 1/3rd profit, which he takes 2/9th from X and 1/9th from Y and brings Rs. 1500 as premium. Pass the necessary Journal entries on Z‘s admission.

Question: Ranzeet and Priya are two partners sharing profits in the ratio of 3:2. They admit Nilu as a partner, who pays Rs. 60,000 as capital. The new ratio is fixed as 3:1:1. The value of goodwill of the firm was determined at Rs. 50,000. Show journal entries if Nilu brings goodwill for her share in cash.

Question:A and B are partners sharing profits equally. They admit C into partnership, C paying only Rs. 1000 for premium out of his share of premium of Rs. 1800 for 1/4th share of profit. Goodwill account appears in the books at Rs. 6000. All the partners have decided that goodwill should not appear in the new firms books.

Question: A and B are partners sharing profits in the ratio of 3:2. Their books showed goodwill at Rs. 2000. C is admitted with 1/4th share of profits and brings Rs. 10,000 as his capital but is not able to bring in cash goodwill Rs. 3000. Give necessary Journal entries.

Question: Piyush and Deepika are partners sharing in the ratio of 7:3. they admit Seema as a new partner. The new ratio being 5:3:2. Pass journal entries.

Question: A and B are partners with capital of Rs. 26,000 and Rs. 22,000 respectively. They admit C as partner with 1/4th share in the profits of the firm. C brings Rs. 26,000 as his share of capital. Give journal entry to record goodwill on C‘s admission.

Question:A and B are partners sharing profits in the ratio of 3:2. They admit C into partnership for 1/4th share. C is unable to bring his share of goodwill in cash. The goodwill of the firm is valued at Rs. 21,000. give journal entry for the treatment of goodwill on C‘s admission.

Question: A and B are partners with capitals of Rs. 13,000 and Rs. 9000 respectively. They admit C as a partner with 1/5th share in the profits of the firm. C brings Rs. 8000 as his capital. Give journal entries to record goodwill.

Question:A, B and C were partners in the ratio of 5:4:1. On 31st Dec. 2006 their balance sheet showed a reserve fund of Rs. 65,000, P&L A/C (Loss) of Rs. 45,000. On 1st January, 2007, the partners decided to change their profit sharing ratio to 9:6:5. For this purpose goodwill was valued at Rs. 1,50,000. The partners do not want to distribute reserves and losses and also do not want to record goodwill. You are required to pass single journal entry for the above.

Question: A and B were partners in the ratio of 3:2. They admit C for 3/13th share. New profit ratio after C‘s admission will be 5:5:3. C brought some assets in the form of his capital and for the share of his goodwill.

")

At the time of admission of C goodwill of the firm was valued at Rs. 12,48,000. Pass necessary journal entries.

Question: X, Y and Z are sharing profits and losses in the ratio of 5:3:2. They decide to share future profits and losses in the ratio of 2:3:5 with effect from 1st April, 2002. They also decide to record the effect of the reserves without affecting their book figures, by passing a single adjusting entry. Book Figure

General Reserve Rs. 40,000

Profit & loss A/C Rs. 10,000

Advertisement Suspense A/C Rs. 20,000

Pass the necessary single adjusting entry.

Please refer to attached file for CBSE Class 12 Accountancy Reconstitution Of Partnership Assignment Part A

Free study material for Accountancy

CBSE Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner Assignment

Access the latest Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner assignments designed as per the current CBSE syllabus for Class 12. We have included all question types, including MCQs, short answer questions, and long-form problems relating to Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner. You can easily download these assignments in PDF format for free. Our expert teachers have carefully looked at previous year exam patterns and have made sure that these questions help you prepare properly for your upcoming school tests.

Benefits of solving Assignments for Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner

Practicing these Class 12 Accountancy assignments has many advantages for you:

- Better Exam Scores: Regular practice will help you to understand Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner properly and you will be able to answer exam questions correctly.

- Latest Exam Pattern: All questions are aligned as per the latest CBSE sample papers and marking schemes.

- Huge Variety of Questions: These Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner sets include Case Studies, objective questions, and various descriptive problems with answers.

- Time Management: Solving these Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner test papers daily will improve your speed and accuracy.

How to solve Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner Assignments effectively?

- Read the Chapter First: Start with the NCERT book for Class 12 Accountancy before attempting the assignment.

- Self-Assessment: Try solving the Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner questions by yourself and then check the solutions provided by us.

- Use Supporting Material: Refer to our Revision Notes and Class 12 worksheets if you get stuck on any topic.

- Track Mistakes: Maintain a notebook for tricky concepts and revise them using our online MCQ tests.

Best Practices for Class 12 Accountancy Preparation

For the best results, solve one assignment for Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner on daily basis. Using a timer while practicing will further improve your problem-solving skills and prepare you for the actual CBSE exam.

FAQs

You can download free PDF assignments for Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner from StudiesToday.com. These practice sheets have been updated for the 2026-27 session covering all concepts from latest NCERT textbook.

Yes, our teachers have given solutions for all questions in the Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner assignments. This will help you to understand step-by-step methodology to get full marks in school tests and exams.

Yes. These assignments are designed as per the latest CBSE syllabus for 2026. We have included huge variety of question formats such as MCQs, Case-study based questions and important diagram-based problems found in Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner.

Practicing topicw wise assignments will help Class 12 students understand every sub-topic of Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner. Daily practice will improve speed, accuracy and answering competency-based questions.

Yes, all printable assignments for Class 12 Accountancy Part 1 Chapter 2 Reconstitution Of A Partnership Firm Admission Of A Partner are available for free download in mobile-friendly PDF format.