Read and download the CBSE Class 12 Accountancy Ratio analysis Assignment for the 2026-27 academic session. We have provided comprehensive Class 12 Accountancy school assignments that have important solved questions and answers for Part 2 Chapter 5 Accounting Ratios. These resources have been carefuly prepared by expert teachers as per the latest NCERT, CBSE, and KVS syllabus guidelines.

Solved Assignment for Class 12 Accountancy Part 2 Chapter 5 Accounting Ratios

Practicing these Class 12 Accountancy problems daily is must to improve your conceptual understanding and score better marks in school examinations. These printable assignments are a perfect assessment tool for Part 2 Chapter 5 Accounting Ratios, covering both basic and advanced level questions to help you get more marks in exams.

Part 2 Chapter 5 Accounting Ratios Class 12 Solved Questions and Answers

Question. Current Ratio is calculated by:

(a) Current Liabilities/Current Assets

(b) Current Assets/Current Liabilities

(c) Current Assets/Long-term Liabilities

(d) Long-term Assets/Long-term Liabilities

Answer. B

Question. The ideal Current ratio is:

(a) 1.25 : 1

(b) 2 : 1

(c) 1 : 2

(d) 10%

Answer. B

Question. The two basic measures of operational efficiency of a company are:

(a) Inventory Turnover Ratio and Working Capital Turnover Ratio

(b) Liquid Ratio and Operating Ratio

(c) Liquid Ratio and Current Ratio

(d) Gross Profit Margin and Net Profit Margin

Answer. A

Question. Compute Total Assets Turnover Ratio from the information given below:

Fixed Assets net of depreciation = Rs 4,00,000;

Current Assets = Rs 3,00,000;

Revenue from Operations = Rs 14,00,000.

(a) 3 times

(b) 2 times

(c) 1 time

(d) 4 times

Answer. B

Question. If Total Assets are Rs 13,20,000, Non-Current Assets Rs 6,00,000 and Capital Employed is Rs 12,00,000. Which of the following correctly represents the current ratio for the venture?

(a) 2 : 1

(b) 4 : 1

(c) 6 : 1

(d) 7 : 1

Answer. C

Question. In case if the current ratio of a business is 0.8:1, state if payment of final dividend already declared the current ratio:

(a) will improve

(b) will decline

(c) will have no impact on

(d) may or may not impact

Answer. B

Question. Current Ratio is 2 : 1. On the sale of fixed asset (Book value Rs 20,000) for Rs 18,000, state whether the Current Ratio will:

(a) Improve

(b) Decline

(c) Will not change

(d) Can’t say

Answer. A

Question. A transaction involving a decrease in both Current Ratio and Quick Ratio is:

(a) Sale of Non-current Asset for cash.

(b) Sale of Stock-in-Trade at loss.

(c) Cash payment of a Current Liability.

(d) Purchase of Stock-in-Trade on credit.

Answer. A

Question. The quick ratio of a company is 1.5 : 1. State with reason which of the following transactions would:

(i) increase;

(ii) decrease or

(iii) not change the ratio.

(a) Paid rent Rs 3,000 in advance.

(b) Trade receivable included a debtor Shri Ashok who paid his entire amount due Rs 9,700.

Answer. D

Question. From the following which ratio is not a part of Activity Ratio:

(a) Inventory Turnover Ratio

(b) Trade Receivables Turnover Ratio

(c) Working Capital Turnover Ratio

(d) Debt to Equity Ratio

Answer. D

Question. The ___________ may indicate that the firm is experiencing stock outs and lost sales:

(a) Average payment period

(b) Inventory turnover ratio

(c) Average collection period

(d) Quick ratio

Answer. B

Question. Current ratio of Vidur Pvt. Ltd. is 3 : 2. Accountant wants to maintain it at 2 : 1. Following options are available:

(i) He can repay Bills Payable

(ii) He can purchase goods on credit

(iii) He can take short term loan

Choose the correct option:

(a) Only (i) is correct

(b) Only (ii) is correct

(c) Only (i) and (iii) are correct

(d) Only (ii) and (iii) are correct

Answer. A

Question. Which of the following is not a type of Activity Ratio?

(a) Working Capital Turnover Ratio.

(b) Debt to Equity Ratio.

(c) Inventory Turnover Ratio.

(d) All of these.

Answer. B

Question. Debt equity ratio of a company is 1 : 2. Which of the following transactions will increase it:

(a) Issue of new shares for cash

(b) Redemption of Debentures

(c) Issue of Debentures for cash

(d) Goods purchased on credit

Answer. C

Question. Assuming that the current ratio is 2 : 1 purchase of goods on credit would:

(a) Increase current ratio

(b) Decrease current ratio

(c) No effect on current ratio

(d) Decrease gross profit ratio

Answer. A

Question. On the basis of following information received from a firm, its Proprietary Ratio will be:

Fixed Assets Rs 3,30,000; Current Assets Rs 1,90,000; Preliminary Expenses Rs 30,000; Equity Share Capital Rs 2,44,000; Preference Share Capital Rs 1,70,000; Reserve Fund Rs 58,000.

(a) 70%

(b) 80%

(c) 85%

(d) 90%

Answer. C

Question. Satisfactory Ratio between Long-term Debts and Shareholder’s Funds is:

(a) 1 : 1

(b) 3 : 1

(c) 1 : 2

(d) 2 : 1

Answer. D

Question. Opening Inventory of a firm is Rs 80,000. Cost of revenue from operations is Rs 6,00,000. Inventory Turnover Ratio is 5 times. Its closing Inventory will be:

(a) Rs 1,60,000

(b) Rs 1,20,000

(c) Rs 80,000

(d) Rs 2,00,000

Answer. A

Question. Inventory Turnover Ratio is:

(a) Average Inventory/Revenue from Operations

(b) Average Inventory/Cost of Revenue from Operations

(c) Cost of Revenue from Operations/Average Inventory

(d) G.P./Average Inventory

Answer. C

Question. Which of the following items is shown under the head ‘Current Assets’ while preparing the Balance Sheet of a company?

(a) Trade Investment

(b) Underwriting Commission

(c) Inventories

(d) Livestock

Answer. C

Question. Current assets of a company were Rs 1,00,000 and its current ratio was 2 : 1. Company paid Rs 25,000 to a trade payable. The current ratio after the payment will be:

(a) 5 : 1

(b) 2 : 1

(c) 3 : 1

(d) 4 : 1

Answer. C

Question. Which of the following is not a part of Activity Ratios/Turnover Ratios:

(a) Trade Receivable Turnover Ratio

(b) Trade Payable Turnover Ratio

(c) Interest Coverage Ratio

(d) Working Capital Turnover Ratio

Answer. C

Question. Amount (Rs)

I. EQUITY AND LIABILITIES 8,00,000

Current Liabilities

II. ASSETS 10,00,000

Current Assets

Subsequently it purchased goods for Rs 1,00,000 on credit. Quick ratio will be_________

(a) 1.11 : 1

(b) 1.22 : 1

(c) 1.38 : 1

(d) 1.25 : 1

Answer. A

Question. If Current Ratio of a company is 3 : 2, identify which combination is correct:

(a) Current Assets Rs 50,000 and Current Liabilities Rs 50,000

(b) Current Assets Rs 60,000 and Current Liabilities Rs 50,000

(c) Current Assets Rs 90,000 and Current Liabilities Rs 70,000

(d) Current Assets Rs 90,000 and Current Liabilities Rs 60,000

Answer. D

Question. Which of the following assets are not part of Current Assets while calculating the Current Ratio?

(a) Cash in hand

(b) Cash at bank

(c) Marketable securities

(d) Loose tools

Answer. D

Question.

Items Amount (Rs)

1. Paid-up Share Capital 6,00,000

2. 6% Debenture 3,00,000

3. 9% Loan 1,00,000

4. DRR 2,00,000

5. Closing Inventory 1,00,000

Debt equity ratio will be:

(a) 0.5 : 1

(b) 0.66 : 1

(c) 1.6 : 1

(d) 1.25 : 1

Answer. A

Question. In which of the following ratio RsRsTotal Assets’’ are used for calculation purpose:

(a) Proprietary Ratio

(b) Inventory Turnover Ratio

(c) Current Ratio

(d) Return on Investment

Answer. A

Question. Ratio analysis under financial analysis is significant as it.

(a) ignores qualitative factors

(b) helps in window-dressing

(c) does not requires any standards

(d) helps in locating weak points of the firm

Answer. D

Question. Normally absolute ratio is further refinement of liquid or quick ratio. Which of the following is considered fairly satisfactory?

(a) 1 : 1

(b) 0.5 : 1

(c) 1.5 : 1

(d) 1 : 1.5

Answer. A

Question. Test of solvency of a business undertaking means:

(a) its ability to meet the interest costs

(b) its ability to meet the long-term liabilities as and when they become due

(c) its ability to pay dividends to equity shareholders

(d) All of the above

Answer. D

Question. The immediate solvency ratio is:

(a) quick ratio

(b) current ratio

(c) debtors turnover ratio

(d) stock turnover ratio

Answer. A

Question. The following groups of ratios are primarily measure risk:

(a) liquidity, activity and profitability

(b) liquidity, activity and inventory

(c) liquidity, activity and debt

(d) liquidity, debt and profitability

Answer. D

Question. The _______ ratios are primarily measures of return.

(a) liquidity

(b) activity

(c) debt

(d) profitability

Answer. D

Question. The _______ of business firm is measured by its ability to satisfy its short-term obligations as they become due:

(a) activity

(b) liquidity

(c) debt

(d) profitability

Answer. B

Question. ______ ratios are a measure of the speed with which various accounts are converted into revenue from operations or cash. [NCERT]

(a) Activity

(b) Liquidity

(c) Debt

(d) Profitability

Answer. A

Question. The two basic measures of liquidity are:

(a) inventory turnover and current ratio

(b) current ratio and liquid ratio

(c) gross profit margin and operating ratio

(d) current ratio and average collection period

Answer. B

Question. The ______ is a measure of liquidity which excludes ______, generally the least liquid asset.

(a) current ratio, trade receivable

(b) liquid ratio, trade receivable

(c) current ratio, inventory

(d) liquid ratio, inventory

Answer. D

Question. The credit sale of M/s. Dinesh & Sons is Rs 21,00,000. It’s debtors and bills receivables of the end of the accounting period amounted to Rs 2,00,000 and Rs 1,50,000 respectively. What will be the debtor’s turnover ratio?

(a) 4 times

(b) 5 times

(c) 6 times

(d) 7 times

Answer. C

Question. Total purchase Rs 1,70,000, cash purchases Rs 16,000, purchase return Rs 8,000, creditors at the end of the year Rs 32,000,creditors inthe beginning Rs 24,000. What will be the creditors turnover ratio?

(a) 5.12 times

(b) 5.16 times

(c) 5.21 times

(d) 5.25 times

Answer. C

Question. Consider the following information.

Long-term borrowings Rs 2,00,000

Long-term provision Rs 1,00,000

Current liabilities Rs 50,000

Non-Current assets Rs 3,60,000

Current assets Rs 90,000

Proprietary ratio will be:

(a) 22.2%

(b) 2.8%

(c) 36%

(d) None of these

Answer. A

Question. Calculating Operating Ratio, if cost of revenue from operations Rs 50,000, Revenue from operations Rs 1,50,000 and Operating expenses Rs 20,000.

(a) 45%

(b) 46.7%

(c) 48.1%

(d) 42.2%

Answer. B

Question. The ______ is useful in evaluating credit and collection policies.

(a) average payment period

(b) current ratio

(c) average collection period

(d) current assets turnover

Answer. C

Question. The ______ measures the activity of a firm’s inventory.

(a) average collection period

(b) inventory turnover

(c) liquid ratio

(d) current ratio

Answer. B

Question. ABC Co. extends credit terms of 45 days to its customers. Its credit collection would be considered poor if its average collection period was.

(a) 30 days

(b) 36 days

(c) 47 days

(d) 37 days

Answer. C

Question. ______ are especially interested in the average payment period, since it provides them with a sense of the billpaying patterns of the firm.

(a) Customers

(b) Stockholders

(c) Lenders and suppliers

(d) Borrowers and buyers

Answer. C

Question. The ______ ratios provide the information critical to the long-run operation of the firm.

(a) liquidity

(b) activity

(c) solvency

(d) profitability

Answer. C

Question. Which of the following transactions will improve the current ratio:

(a) Cash collected from trade receivables

(b) Purchase of goods for cash

(c) Payment to trade payables

(d) Credit purchase of goods

Answer. C

Question. Operating ratio is:

(a) Cost of revenue from operations + Selling expenses/Net revenue from operations

(b) Cost of production + Operating expenses/Net revenue from operations

(c) Cost of revenue from operations + Operating expenses/Net revenue from operations

(d) Cost of production/Net revenue from operations

Answer. C

Question. Proprietary ratio is:

(a) Long-term debts/Shareholders’ funds

(b) Total assets/Shareholders’ funds

(c) Shareholders’ funds/Total assets

(d) Shareholders’ funds/Fixed assets

Answer. C

Question. Assertion : Tanmay Ltd. has a Proprietary Ratio of 25% to maintain this ratio at 30%, management may increase the current assets

Reason : To increase the proprietary ratio the management may increase equity or reduce the debts increase of current asset will reduce the ratio.

(A) Both A and R true and R is the correct explanation of A.

(B) Both A and R are true but R is not the correct explanation of A

(C) A is true and R is false

(D) A is false and R is true

Answer. D

Question. Assertion : Accounting ratio is a mathematical expression of relationship between one item of the group of item in the Financial Statement.

Reason : Accounting ratio is a mathematical expression of relationship between two items group of item in the Financial Statement.

(A) Both A and R true and R is the correct explanation of A.

(B) Both A and R are true but R is not the correct explanation of A

(C) A is true and R is false

(D) A is false and R is true

Answer. D

Question. Assertion : The objective of computing operating ratio is to assess the operational efficiency of the business.

Reason : It shows the percentage of Revenue from operations that is absorbed by the cost of Revenue from operations and operating expenses.

(A) Both A and R true and R is the correct explanation of A.

(B) Both A and R are true but R is not the correct explanation of A

(C) A is true and R is false

(D) A is false and R is true

Answer. A

Question. Assertion : Operating ratio establishes the relationship between Operating profit and Revenue from operations.

Reason : Operating ratio establishes the relationship between Operating Cost (Cost of revenue from operations + operating expenses) and Revenue from operations.

(A) Both A and R true and R is the correct explanation of A.

(B) Both A and R are true but R is not the correct explanation of A

(C) A is true and R is false

(D) A is false and R is true

Answer. D

Assuming that Debt Ratio is 2, state giving reasons whether this ratio would increase, decrease or reamin unchanged in the following cases:

Question. Purchase of fixed asset on a long-term deferred payment basis:

(a) Decrease

(b) Increase

(c) No change

(d) None of these

Answer. B

Question. Issue of new share for cash:

(a) Decrease

(b) Increase

(c) No change

(d) None of these

Answer. A

Question. Sale of fixed asset at a loss of Rs 3000:

(a) Decrease

(b) Increase

(c) No change

(d) None of these

Answer. B

Question. Purchase of fixed asset on a credit of 2 months:

(a) Decrease

(b) Increase

(c) No change

(d) None of these

Answer. D

Question.

Opening Inventory Rs 3,00,000

Closing Inventory Rs 4,20,000

Purchase Rs 14,00,000

Wages Rs 3,70,000

Carriage Inwards Rs 150000

Administrative Expenses Rs 84,000

Selling Expenses Rs 36,000

Income Tax Rs 1,00,000

Profit on sale of fixed assets Rs 20,000

Revenue from Operations (Sales) Rs 24,00,000

Based on above information you are reuired to answer the following questions:

Question. Calculate Gross profit Ratio:

(a) 20%

(b) 30%

(c) 40%

(d) 25%

Answer. D

Question. Calculate Operating Ratio:

(a) 30%

(b) 25%

(c) 80%

(d) None of these

Answer. C

Question. Calculate Operating profit ratio:

(a) 20%

(b) 29%

(c) 10%

(d) 5%

Answer. A

Question. Calculate Net profit ratio:

(a) 15.79%

(b) 16.67%

(c) 17.67%

(d) 18.67%

Answer. B

Following are the information obtained from the books of Kamakshi Ltd.

2016-2017 2017-2018

Inventory on 31st March Rs 7,00,000 Rs 17,00,000

Revenue from Operations Rs 50,00,000 Rs 75,00,000

(Gross profit is 25% on cost of revenue from operations)

In the year 2016-17 inventory increased by Rs 2,00,000

Based on above information you are required to answer the following questions:

Question. What will be the inventory turnover ratio for year 2017-18?

(a) 4 times

(b) 2 times

(c) 3 times

(d) 5 times

Answer. D

Question. What will be the Cost of Revenue from Operations for year 2016-17 ?

(a) Rs 10,00,000

(b) Rs 40,00,000

(c) Rs 20,00,000

(d) Rs 30,00,000

Answer. B

Question. What will be the Average Inventory for the year 2017-18?

(a) Rs 1,00,000

(b) Rs 30,00,000

(c) Rs 6,00,000

(d) Rs 1,50,000

Answer. C

Question. What will be the Inventory Turnover Ratio for year 2016-17?

(a) 4.57 times

(b) 4.00 times

(c) 6.67 times

(d) 8.87 times

Answer. C

Calculate Operating Profit Ratio in the following cases:

Case I- Revenue from operations (Sales) Rs 6,00,000; Operating Profit Rs 1,20,000.

Case II- Revenue from Operations (Sales) Rs 5,00,000; Cost of Revenue from operations Rs 4,00,000; Operating Expenses Rs 20000.

Case III- Revenue from Operations (Sales) Rs 10,00,000; Gross Profit 25% on sales; Operating Expenses Rs 70,000.

Based on above information you are required to answer the following questions:

Question. What will be the Operating Profit Ratio in Case I ?

(a) 12%

(b) 10%

(c) 14%

(d) 20%

Answer. D

Question. What will be the Operating Profit in case II ?

(a) Rs 40,000

(b) Rs 50,000

(c) Rs 80,000

(d) Rs 60,000

Answer. D

Question. What will be the Operating Profit Ratio in Case II ?

(a) 16%

(b) 17%

(c) 11%

(d) 13%

Answer. A

Question. What will be the Operating Profit Ratio in Case III ?

(a) 12%

(b) 13%

(c) 14%

(d) 18%

Answer. D

Q1. Rs.2,00,000 is the cost of goods sold, Inventory turnover ratio is 8 times; stock at the beginning is 1.5 times more than the stock at the end. Calculate the value of Opening and closing stock.

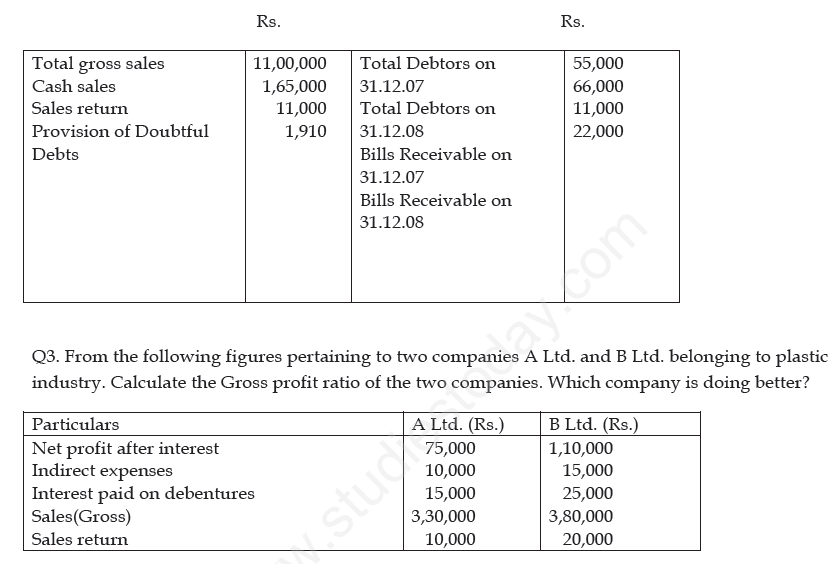

Q2. Calculate Debtors turnover ratio and Average collection period from the following particulars as on 31st Dec. 2008 assuming 365 working days in a year:-

Q4. Calculate Operating Ratio and Operating Profit Ratio from the following information:

Rs.

Net Sales 8,00,000

Cash Sales 2,00,000

Gross Profit Ratio 20%

Office & Selling Expenses 60,000

Depreciation 20,000

Loss on sale of plant 10,000

Q5. From the following details, calculate Return On Investment:-

Rs.

Equity share capital 4,00,000

Preference share capital 1,00,000

General Reserve 2,75,000

10% Debentures 4,00,000

Current liabilities 1,00,000

Discount on issue of shares 5,000

Net profit (after interest & tax) 80,000

Rate of Tax 50%

| CBSE Class 12 Accountancy Ratio analysis Assignment |

| CBSE Class 12 Accountancy Accounting Ratios Assignment |

CBSE Class 12 Accountancy Part 2 Chapter 5 Accounting Ratios Assignment

Access the latest Part 2 Chapter 5 Accounting Ratios assignments designed as per the current CBSE syllabus for Class 12. We have included all question types, including MCQs, short answer questions, and long-form problems relating to Part 2 Chapter 5 Accounting Ratios. You can easily download these assignments in PDF format for free. Our expert teachers have carefully looked at previous year exam patterns and have made sure that these questions help you prepare properly for your upcoming school tests.

Benefits of solving Assignments for Part 2 Chapter 5 Accounting Ratios

Practicing these Class 12 Accountancy assignments has many advantages for you:

- Better Exam Scores: Regular practice will help you to understand Part 2 Chapter 5 Accounting Ratios properly and you will be able to answer exam questions correctly.

- Latest Exam Pattern: All questions are aligned as per the latest CBSE sample papers and marking schemes.

- Huge Variety of Questions: These Part 2 Chapter 5 Accounting Ratios sets include Case Studies, objective questions, and various descriptive problems with answers.

- Time Management: Solving these Part 2 Chapter 5 Accounting Ratios test papers daily will improve your speed and accuracy.

How to solve Accountancy Part 2 Chapter 5 Accounting Ratios Assignments effectively?

- Read the Chapter First: Start with the NCERT book for Class 12 Accountancy before attempting the assignment.

- Self-Assessment: Try solving the Part 2 Chapter 5 Accounting Ratios questions by yourself and then check the solutions provided by us.

- Use Supporting Material: Refer to our Revision Notes and Class 12 worksheets if you get stuck on any topic.

- Track Mistakes: Maintain a notebook for tricky concepts and revise them using our online MCQ tests.

Best Practices for Class 12 Accountancy Preparation

For the best results, solve one assignment for Part 2 Chapter 5 Accounting Ratios on daily basis. Using a timer while practicing will further improve your problem-solving skills and prepare you for the actual CBSE exam.

You can download free PDF assignments for Class 12 Accountancy Chapter Part 2 Chapter 5 Accounting Ratios from StudiesToday.com. These practice sheets have been updated for the 2026-27 session covering all concepts from latest NCERT textbook.

Yes, our teachers have given solutions for all questions in the Class 12 Accountancy Chapter Part 2 Chapter 5 Accounting Ratios assignments. This will help you to understand step-by-step methodology to get full marks in school tests and exams.

Yes. These assignments are designed as per the latest CBSE syllabus for 2026. We have included huge variety of question formats such as MCQs, Case-study based questions and important diagram-based problems found in Chapter Part 2 Chapter 5 Accounting Ratios.

Practicing topicw wise assignments will help Class 12 students understand every sub-topic of Chapter Part 2 Chapter 5 Accounting Ratios. Daily practice will improve speed, accuracy and answering competency-based questions.

Yes, all printable assignments for Class 12 Accountancy Chapter Part 2 Chapter 5 Accounting Ratios are available for free download in mobile-friendly PDF format.