Read and download the CBSE Class 12 Economics Producers Behaviour And Supply To Economics Worksheet in PDF format. We have provided exhaustive and printable Class 12 Economics worksheets for Producers Behaviour And Supply Economics, designed by expert teachers. These resources align with the 2026-27 syllabus and examination patterns issued by NCERT, CBSE, and KVS, helping students master all important chapter topics.

Chapter-wise Worksheet for Class 12 Economics Producers Behaviour And Supply Economics

Students of Class 12 should use this Economics practice paper to check their understanding of Producers Behaviour And Supply Economics as it includes essential problems and detailed solutions. Regular self-testing with these will help you achieve higher marks in your school tests and final examinations.

Class 12 Economics Producers Behaviour And Supply Economics Worksheet with Answers

Question. Function showing relationship between input and output is known as ...... .

a) consumption function

b) investment function

c) production function

d) cost function

Answer. C

Question. If the Average Product (AP) of a labour is 30 units of outputs, then find total product of 2 labours.

a) 10 units of output

b) 15 units of output

c) 30 units of output

d) 60 units of output

Answer. D

Question. Average Product (AP) is at its maximum when

a) MP > AP

b) MP < AP

c) MP = AP

d) MP becomes negative

Answer. C

Question. ...... is the variable factor of production.

a) Land

b) Labour

c) Capital

d) Factory

Answer. B

Question. Increasing returns is applicable because of ...... .

a) increased efficiency of variable factor

b) fuller utilisation of fixed factor

c) indivisibility of factors

d) Both (a) and (b)

Answer. D

Question. Under the relationship between TP, MP and AP curves, MP becomes negative when

a) TP increases

b) TP decreases

c) TP remain constant

d) TP becomes zero

Answer. B

Question. If the total product of 5 labours is 50 units of output and total product of 6 labours is 66 units of output, find Average Product (AP) of 6th unit oflabour.

a) 10 units of output

b) 11 units of output

c) 50 units of output

d) 16 units of output

Answer. B

Question. When total product falls, then ...... .

a) average product is equal to zero

b) marginal product is equal to zero

c) marginal product is negative

d) average product continues to rise

Answer. C

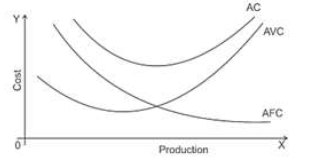

Question. Which of the following curve is not ‘U’ shaped?

a) AFC

b) AVC

c) MC

d) AC

Answer. A

Question. What is ‘production’ in economics?

a) Creation/Addition to the value of output

b) Production of foodgrains

c) Creation of services

d) Manufacturing of goods

Answer. A

Question. In the first stage of law of variable proportions, total product increases at an ...... .

a) decreasing rate

b) increasing rate

c) constant rate

d) Both (a) and (b)

Answer. B

Question. In which time period, all factors of production become variable and factors of production change with the change in level of production?

a) Long period

b) Market period

c) Short period

d) All of these

Answer. A

Question. Payment made to outsiders for their goods and services are called ...... .

a) opportunity cost

b) real cost

c) explicit cost

d) implicit cost

Answer. C

Question. Law of variable proportion is valid when ....... .

a) atleast one input is fixed and all other inputs are kept variable

b) all factors are kept constant

c) all inputs are varied in the same proportion

d) None of the above

Answer. A

Question. Cost function explain the relationship between

a) income and expenditure

b) input and output

c) fixed cost and variable cost

d) output and cost of production

Answer. D

Question. Which of the stages is relevant for a firm which aims at maximum economic efficiency in the law of variable proportion?

a) Stage I

b) Stage II

c) Stage III

d) Stage IV

Answer. B

Question. Total revenue generated from sale of output of a firm can be calculated as

a) TR = P × Q

b) TR = AR × Q

c) TR = ∑MR

d) All of these

Answer. D

Question. At the point of inf lexion, the marginal product is ...... .

a) increasing

b) decreasing

c) maximum

d) negative

Answer. C

Question. When average cost curve is rising, then marginal cost ...... .

a) must be decreasing

b) must be constant

c) must be rising

d) Any of these

Answer. C

Question. Average Revenue is equal to ..... .

a) Total Revenue/ Quantity Sold

b) Average Revenue/2

c) Total Revenue/100

d) Average Quantity/Quantity Sold × 2

Answer. A

Question. Area under MC curve is ...... .

a) total cost

b) total fixed cost

c) total variable cost

d) None of these

Answer. C

Question. Short-run supply curve of the firm is ..... .

a) rising portion of MC curve

b) rising portion of MC curve which lies above AVC curve

c) rising portion of MC curve which lies above AFC curve

d) entire MC curve

Answer. B

Question. ...... are not zero at zero level of output.

a) Fixed costs

b) Variable costs

c) Marginal costs

d) Average variable costs

Answer. A

Question. When the firm is producing 3 tonnes of sugar, it receives total revenue of Rs 24. Raising production to 4 tonnes, increases total revenue to Rs 28. Thus, marginal revenue is ...... .

a) Rs 4

b) Rs 8

c) Rs 28

d) Rs 52

Answer. A

Question. As output increases, average fixed cost ...... .

a) remains constant

b) starts falling

c) starts rising

d) None of these

Answer. B

Question. Under imperfect competition, slope of AR is generally ...... of slope of MR.

a) half

b) twice

c) equal

d) one-third

Answer. B

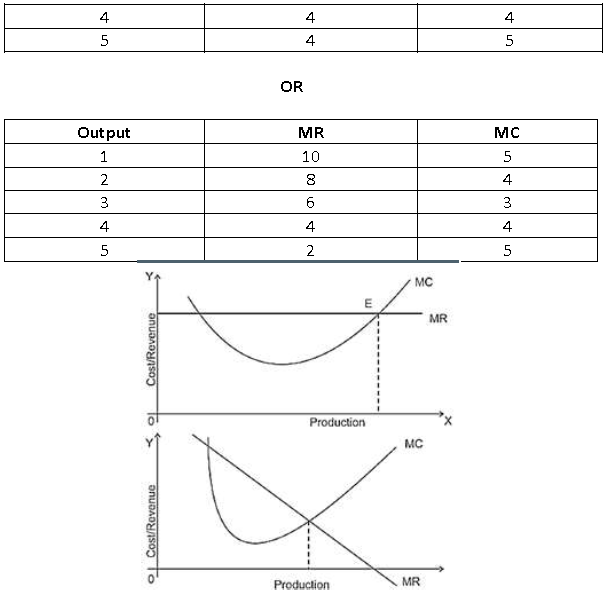

Question. A perfectly competitive firm attains equilibrium at a point where ...... .

a) MR is equal to MC and MC curve intersects MR curve from below

b) MC is equal to MR

c) MC is falling but is equal to AC

d) Both (a) and (b)

Answer. A

Question. If AR is Rs 40 per unit from the sale of 3 goods and it is Rs 30 per unit from the sale of 4 goods. Find the marginal revenue of 4th unit of goods.

a) Rs 10

b) Rs 30

c) Rs 40

d) 0

Answer. D

Question. In the process of production, fixed factors and variable factors are combined in a particular ratio, which gives equilibrium output. What is this ratio called?

a) Factor output ratio

b) Capital output ratio

c) Ideal factor ratio

d) None of these

Answer. C

Question. When MC is greater than MR after producer equilibrium, it means

a) profit of firm

b) producing more will lead to decline in profit

c) no profit no loss

d) firm enjoys economic efficiency

Answer. B

Question. Marginal Revenue (MR) curve is a straight horizontal line in ....... .

a) perfectly competitive market

b) monopolistic competitive market

c) oligopoly market

d) monopoly market

Answer. A

Question. Which of the following statement is true?

a) For a monopoly firm, average revenue can be zero.

b) For a monopoly firm, marginal revenue can be zero or negative.

c) For a monopoly firm, marginal revenue and average revenue are identical.

d) For a monopoly firm, marginal revenue and average revenue are positively sloped.

Answer. B

Question. In monopoly and monopolistic competitions, AR and MR curve are downward sloping because the firms can sell more by

a) increasing the price

b) lowering the price

c) keep in price constant

d) All of the above

Answer. B

Question. When marginal revenue is zero, ...... .

a) total revenue is also zero

b) total revenue is the maximum

c) total revenue is the minimum

d) total revenue starts increasing sharply

Answer. B

Question. In the long-run, a firm in a perfectly competitive market earns ...... .

a) normal profit

b) abnormal profit

c) atleast 15% profit on capital employed

d) None of the above

Answer. A

Question. When total product is 100 units and units of variable factor are 5, average product will be

a) 20

b) 95

c) 105

d) 500

Answer. A

Question. The firm in perfect competition maximises profit by producing at the rate of output where price equals to ...... .

a) revenue cost

b) marginal

c) revenue

d) marginal cost

Answer. D

Question. Average revenue of a monopolist firm is ....... .

a) always more than the marginal revenue

b) always less than the marginal revenue

c) equal to marginal revenue

d) None of the above

Answer. A

Question. ....... is a person who purchase factors of production (inputs) to convert them into outputs.

a) Buyers

b) Consumer

c) Producer

d) Government

Answer. C

Question. A firm break-even point occurs when ...... . At this point, firm is earning zero economic profit or normal profits. The market price passes through the minimum point of AC curve.

a) AR = AC

b) TR = TC

c) AR = AVC

d) Both (a) and (b)

Answer. D

Question. Which of the following is true about shape of marginal product and average product curves?

a) Average product is ‘U’ shaped and marginal product is inverted ‘U’ shaped

b) Marginal product is ‘U’ shaped and average product is inverted ‘U’ shaped

c) Both average product and marginal product are ‘U’ shaped

d) Both average product and marginal product are inverted ‘U’ shaped

Answer. D

Question. In perfect competition,

a) AR = MR

b) AR = P

c) TR is positively sloped straight line from origin

d) All of the above

Answer. D

Question. A seller can sell 5 smart phones at a price of Rs 12,000 each. If he sell 6th unit of mobile, his marginal revenue will be 10,500. The Price/AR of the 6th unit will be

a) Rs 11,000

b) Rs 12,000

c) Rs 11,700

d) Rs 11,750

Answer. D

Question. Which cost curve is parallel to ox-axis? Why?

Answer. Total fixed cost because TFC remain constant at all level of output.

Answer. Diminishing return to a factor

Answer. Marginal product is net addition to total product when one additional unit of variable factor is used.

Answer. AP is a per unit output of a variable factor.

Answer. MP falls but it falls at faster rate than AP

Answer. Those monetary payments by producer on factor and non factor payments is called explicit cost. Which are not owned by himself.

Question. How does fall in total product affects marginal product?

Answer. When total product falls, marginal product becomes negative.

Question. What do you mean by cost?

Answer. Cost is the sum of explicit and implicit cost.

Question. What do you mean by implicit costs?

Answer. Implicit cost is the cost of self owned resources of producer.

Answer. These factors of production which cannot be varied in short period e.g. machine, land.

Question. By which behaviour of marginal product will total product be maximum

Answer. When marginal product of a factor is zero, then total product will be maximum.

Question. Define marginal cost.

Answer. Marginal cost is the net addition to total cost when one additional unit of output is produced.

Question. At what rate average and marginal revenue falls, with fall in per unit price of a good?

Answer. Marginal revenue falls twice the rate of average revenue.

Answer. It is because average fixed cost goes on falling with increase in output.

Question. Define Revenue.

Answer. Revenue is the amount received from sale of output.

Question. What will be the behaviour of Average revenue when total revenue increases at constant rate?

Answer. Average revenue remains constant.

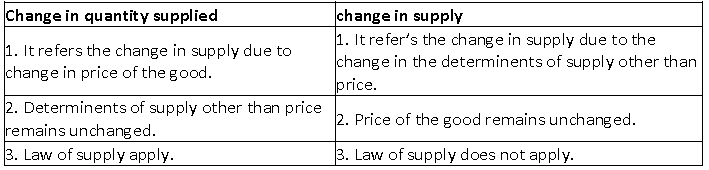

Question. When does the elasticity of supply of commodity called equal to unity?

Answer. When percentage change in price is equal to percentage change in supply.

Question. When does the producer increase the supply of a good at given price, give two reasons.

Answer. Due to change in other factor like improvement in technology, decrease in price of inputs.

Question. What causes an extension in supply?

Answer. Increase in price of a commodity.

Question. What happens to TP when MP is zero?

Answer. TP is maximum.

Question. What happens to MPP when TPP increases at decreasing rate?

Answer. MPP falls but remains positive.

Question. As the variable input is increased by one unit, total output falls. What would you say about of marginal productivity labour?

Answer. Marginal productivity of labour is negative.

Question. Why MC curve is in short run U-shaped?

Answer. MC Curve in short run is U-shaped due to operation of the law of returns to a factor.

Question. Why does fixed cost not influence marginal cost?

Answer. Because marginal cost does not include fixed cost.

Question. When a seller sells his entire output at a fixed price, what will be the shape of AR & MR curves?

Answer. Both AR & MR are equal and coincide with each other on a horizontal line.

Question. Show that average revenue equals price.

Answer. AR = TR / Q = P x Q / Q = P = price

Question. What effect does a cost saving technical progress have on the supply curve?

Answer. Supply curve will shift to the right.

Question. What effect does an increase in excise tax have on the supply curve?

Answer. Supply curve will shift to the left.

Question. What happens to TPP when marginal productivity of variable input is negative?

Answer. TPP falls.

Question. When is TPP maximum in relation to MPP?

Answer. When MPP is zero.

Question. What happens to MPP when TPP is declining?

Answer. MPP declines and remains negative.

Question. Explain the relation between average revenue and marginal revenue when a firm can sell an additional unit or a good by lowering the price.

Answer. 1. AR and MR both decreases.

2. MR decrease at the rate of twice than AR.

3. MR become zero and negative but AR can never be zero.

Question. Explain how does change in price of input affect the supply of a good.

Answer. A. Increase in price of input : increase in price of input is cause of a decrease in the supply of a good because the production cost of a good will increase due to increase in price of input. It will reduced the profit. So producer will decrease the supply of the good.

B. Decrease in price of Input : Decrease in price of input is a cause of increase in supply because when the price of input decrease the production cost of a good also also decreases. Decrease in cost increases the profit margin. It motivate to producer to increase the supply of the good.

Question. Explain how changes in prices of other products influence the supply of a given product.

Answer. The supply of a good is inversly influenced with the change in price of other product which can explain as fallows.

A. Rise in price of other product :– When there is rise in the price of other product the production of these product become more profitable due to unchanged cost in comparison of the production of given produce. As a result the producer will produce more quantity of other product so the supply of given good will decrease.

B. Fall in the price of other product :– When there is fall in the price of other product the production of these product become less profitable due to unchanged cost in comparison of the production of given product. As a result producer will produce less quantity of other product so the factors of production shifted for the production of given good. It cause an increase in supply of given good.

Question. Explain how technological advancement influence the supply of a given product.

Answer. Technological advancement brings a positive impact in the supply of a given product. It reduces per unit cost and increase the productivity of given factors of production. Due to these reasons production of given product becomes more profitable.

Question. What are the factors which give rise to increasing returns to variable factors?

Answer. 1. Fuller utilization of the fixed factors- Generally fixed factors are indivisible and underutilized. With greater application of variable factor these factors are better utilized its MPP tends to rise.

2. Increased efficiency of variable factor- Application of specialization and division of labour among the units of variable factors leads to greater efficiency and increase in MPP.

CBSE Economics Class 12 Producers Behaviour And Supply Economics Worksheet

Students can use the practice questions and answers provided above for Producers Behaviour And Supply Economics to prepare for their upcoming school tests. This resource is designed by expert teachers as per the latest 2026 syllabus released by CBSE for Class 12. We suggest that Class 12 students solve these questions daily for a strong foundation in Economics.

Producers Behaviour And Supply Economics Solutions & NCERT Alignment

Our expert teachers have referred to the latest NCERT book for Class 12 Economics to create these exercises. After solving the questions you should compare your answers with our detailed solutions as they have been designed by expert teachers. You will understand the correct way to write answers for the CBSE exams. You can also see above MCQ questions for Economics to cover every important topic in the chapter.

Class 12 Exam Preparation Strategy

Regular practice of this Class 12 Economics study material helps you to be familiar with the most regularly asked exam topics. If you find any topic in Producers Behaviour And Supply Economics difficult then you can refer to our NCERT solutions for Class 12 Economics. All revision sheets and printable assignments on studiestoday.com are free and updated to help students get better scores in their school examinations.

You can download the latest chapter-wise printable worksheets for Class 12 Economics Chapter Producers Behaviour And Supply Economics for free from StudiesToday.com. These have been made as per the latest CBSE curriculum for this academic year.

Yes, Class 12 Economics worksheets for Chapter Producers Behaviour And Supply Economics focus on activity-based learning and also competency-style questions. This helps students to apply theoretical knowledge to practical scenarios.

Yes, we have provided solved worksheets for Class 12 Economics Chapter Producers Behaviour And Supply Economics to help students verify their answers instantly.

Yes, our Class 12 Economics test sheets are mobile-friendly PDFs and can be printed by teachers for classroom.

For Chapter Producers Behaviour And Supply Economics, regular practice with our worksheets will improve question-handling speed and help students understand all technical terms and diagrams.