Read and download the CBSE Class 12 Business Arithmetic Notes Worksheet in PDF format. We have provided exhaustive and printable Class 12 Other Subjects worksheets for Business Arithmetic Notes, designed by expert teachers. These resources align with the 2026-27 syllabus and examination patterns issued by NCERT, CBSE, and KVS, helping students master all important chapter topics.

Chapter-wise Worksheet for Class 12 Other Subjects Business Arithmetic Notes

Students of Class 12 should use this Other Subjects practice paper to check their understanding of Business Arithmetic Notes as it includes essential problems and detailed solutions. Regular self-testing with these will help you achieve higher marks in your school tests and final examinations.

Class 12 Other Subjects Business Arithmetic Notes Worksheet with Answers

"Take risks in your life. If you win, you can lead. If you lose, you can guide." – Swami Vivekananda

Question. Define the terms „Unit of sale‟ and „unit cost‟ in the case of multiple products.

Answer: Unit of sale could be in quantity (for example, one or a dozen) or in weight (kilograms) and the entrepreneur will use it for pricing, determining the cost per unit, gross profit per unit, establishing the sales trend, fixing sales target etc. While some businesses may deal in only one item, the majority of them deal in many or large number of items. For example, a grocery shop has hundreds of items on its shelves and if it is a super market, it has thousands of items OR a restaurant will have the menu card that runs to a few pages and each page may have 10 to 20 items. A beauty parlour offers many treatments for the customers. In spite of such large number of items, the business person needs some quick and easy way of checking the progress of the business or plan corrective actions. How does one do it?

We all know that a customer does not buy all the items from the grocer at a given time, nor does he/she order all the items on the menu when visiting a restaurant. A customer coming to the beauty parlor does not avail of all the offered services. Neither do all customers buy or order or avail of same items or services. If this be the case, and it is, how does the business owner figure out what is going on in his/her business? This is when ―averages come in to play and help the business owner.

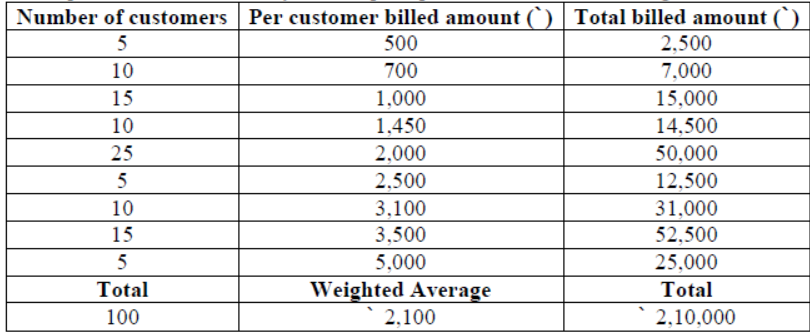

Let us take the example of a grocery store. Each customer coming in to buy things will have different requirements. This, then results in the ―billed amount (or invoiced amount) being different for different people. For example, at the end of the day, the shop keeper found out the following.

In the above example 100 customers bought items worth ₹ 2, 10,000/- , thus giving an average of ₹ 2,100/- per customer. You would notice that no one bought items worth "exactly" ₹ 2,100. The collective purchase by all of them yielded the average. It is possible that on another day the average could be different. In a month, the average (derived on a daily basis) at the beginning of the month could be higher than towards the end.

If the average is arrived for all the customers in a month then it will provide a more realistic picture, which will be much greater than the given sample.

In this particular case, Customer is the unit of sale and the average purchase made by the customer is the "Unit Price" and the Unit Price per Customer (or per Unit of Sale) would be ₹ 2,100/-.

In the case of a restaurant, unit of sale would be a Diner. This is different from the person who pays the bill. A group may consist of 10 people or 5 or 2. At times it may even be one. In each case, the number of persons paying the bill would most likely be one. So it is more accurate to go by the number of Diners.

The Diner is the Unit of Sale and the average amount billed per Diner would be the Unit Price. In the case of a restaurant that provides only Buffet Lunch or Dinner, life is simple. It is like a single product business.

In a beauty parlor or saloon can also use the same concept. The Customer is the Unit of Sale and average billing per customer is unit Price‖.

Unit Cost

Unit cost refers to variable cost (also referred to as cost of goods sold).

How do we calculate the unit cost in the case of multi product or service situations?

Let us take the grocery store again.

Grocery store is a Trading Business and the cost at which the items are purchased is known (just like MRP) Therefore, at the end of the day, it is possible to know the purchase price of all the items and quantities that were sold. Let us suppose that it works out to ₹ 1, 70,000/-. There were 100 units of Sale. So the unit cost is ₹ 1,700/-.

In some cases, there could be another way. For every item, if the purchase price is 80% of selling price, then in that particular case, the Unit Cost would be ₹ 1,680/- (= 80% of ` 2,100/-). Gross Profit would then be ` 400/- per unit of sale (₹ 2,100 - ₹ 1,700) in the first case and ₹ 420/- per Unit of sale (₹ 2,100 - ₹ 1,680) in the second case.

Many industries have their unique thumb rules for the relationship between Unit Price and Unit Cost. In Fast Moving Consumer Goods Industry it could be 80 or 85% (cost as percentage age of selling price). In food industry, it could be 30 to 35% (COG as percentage age of selling price).

Electronic items may have a different thumb rule. Where none exists, you may be able to develop your own. However, the more accurate way is to actually compute the costs as explained.

Some formulas:

Question. Define Break even analysis in the case of multiple products or services.

Answer: Breakeven point is the level of sales (or revenue generated) that equals all the expenses required for generating that revenue. It is not more than the expenses (i.e. no profit) nor is it less than the expenses (i.e. no loss). In other words there is neither loss nor profit.

At the breakeven level

Total revenue = Total expenses

(Quantity x Unit Price) = (Quantity x Unit Cost) + Fixed Expenses

Quantity x (Unit Price – Unit Cost) = Fixed Expenses

Quantity x Gross Margin (or Profit) per Unit = Fixed Expenses

Gross margin and gross profit are one and the same.

Question. Discuss the usefulness of calculating Breakeven point in a manufacturing environment.

Answer: Usefulness of breakeven analysis continues to be the same whether businesses are operating a single product or multiple product business. It helps in setting profit goal and sales target. In a manufacturing environment, it helps in determining the products that are not contributing to meet the fixed expenses and thus brings up the item for discussion in management meetings about its continuity.

Question. Define „Sales mix‟ break-even point calculation. What are the assumptions in the Sales mix for the calculation of breakeven point?

Answer: Sales mix is the proportion in which two or more products are sold. For the calculation of breakeven point for sales mix, following assumptions are made:

1. The proportion of sales mix must be predetermined.

2. The sales mix must not change within the relevant time period.

3. All cost can be categorized as variable or fixed.

4. Sales price per unit, variable cost per unit and total fixed cost are constant.

5. All units produced are sold.

The calculation method for the break-even point of sales mix is based on the contribution approach method. Since businesses have multiple products in their sales mix therefore it is dealing with products with different contribution margin per unit and contribution margin ratios. This problem is overcome by calculating weighted average contribution margin per unit and contribution margin ratio. These are then used to calculate the break-even point for sales mix. The calculation procedure and the formulas are discussed via following example:

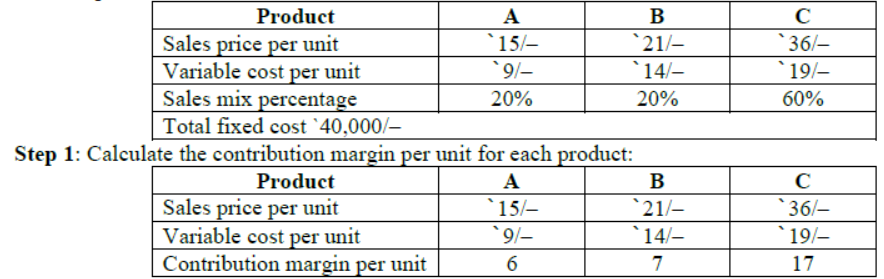

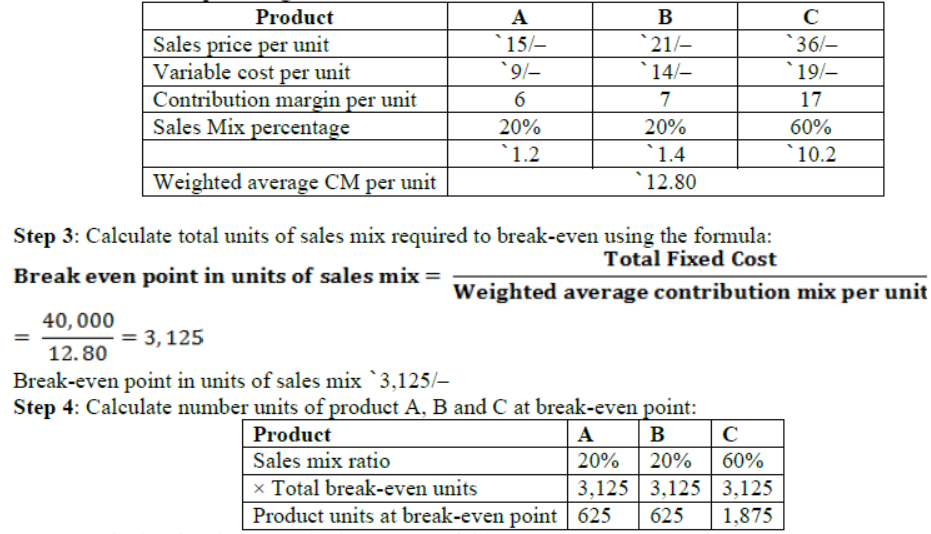

Following information is related to sales mix of product A, B and C. Calculate the break-even point in units and in rupees.

Step:2 Calculate the weighted-average contribution margin per unit for the sales mix using the following formula:

Weighted average unit contribution margin = Product A CM (contribution mix) per Unit × Product a sales mix percentage + Product B CM per unit × Product B sales mix percentage + Product C CM per unit × Product C sales mix percentage

Step 5: Calculate break-even point in rupees as follows:

BE analysis helps in such decision making. Please note that such decisions are product related and not business related. So it is clear from the above calculations as to how we can calculate weighted average sales price per unit and weighted average variable cost so that we can arrive at breakeven point.

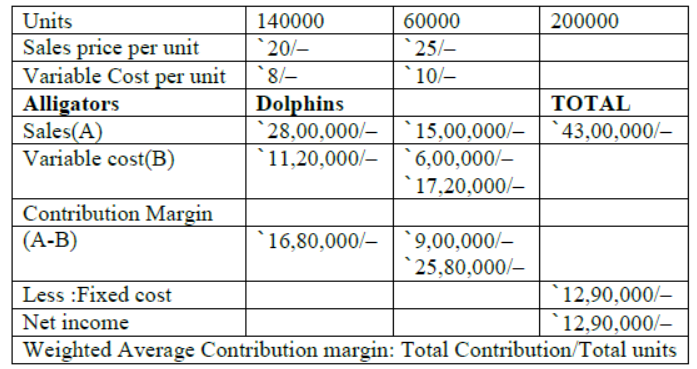

Multiple-product break even analysis

Toy craft produces toy alligators and toy dolphins. Fixed costs are `12,90,000 per year. Sales revenue and variable costs per unit are as follow:

Question.

A. Suppose the company currently sells 140,000 alligators per year and 60,000 dolphins per year (Sales Mix Percentage 14:6). Assuming the sales mix stays constant how many alligators and Dolphins must the company sell to break even?

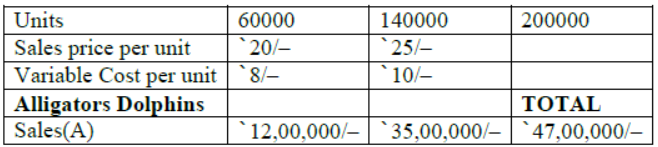

B. Suppose the company currently sells 60,000 alligators per year and 140,000 dolphins per year (Sales mix percentage 6:14). Assuming the sales mix stays constant, how many alligators and dolphins must the company sell to break even per year?

C. Explain why the total number of toys needed to break even in (A) is the same as or different from the number in (B).

Answer: A.

= ₹ 2580000/200000

= ₹ 12.90/–

Breakeven Point = Fixed Cost/Weighted Average Contribution

= ₹ 1,290,000/₹ 12.90

= 100000 units

Allocating TOTAL UNITS to each product based on EXPECTED UNITS PROPORTION= 14:6 Alligators to be produced for Breakeven =

= 70000 units

Dolphins to be produced for Breakeven =

= 30000 units

So, Toy Crafts has to produce 70000 toy alligators and 30000 toy dolphins for breakeven.

B.

Weighted Average Contribution margin: Total Contribution/Total units

= ₹ 2820000/200000

= ₹ 14.10/–

Breakeven Point = Fixed Cost/Weighted Average Contribution

= ₹ 1,290,000/₹ 14.10 = 91489 units

Allocating TOTAL UNITS to each product based on EXPECTED UNITS PROPORTION = 6:14 Alligators to be produced for Breakeven = 91489 x 6/20 = 27446

= 27446 units

Dolphins to be produced for Breakeven = 91489 x 14/20 = 64042

= 64042 units

So, Toy Crafts has to produce 27446 toy alligators and 64042 toy dolphins for breakeven.

C. The total number of toys needed to break even in (a) is different from the number in (b) and lower also. This is due to the reason as weighted contribution per unit has increased; fixed cost spreads over greater number of rupees letting the breakeven to be achieved early. Perhaps (b) sales mix is more efficient and gives the firm a hint to produce toy dolphins more as contribution per unit of a toy dolphin is also higher.

Question. Define cash flow.

Answer: Cash is the lifeblood of every business. It is the most important asset for the operations of a business. Cash Flow refers to the movement of money in and out of a business during a specific period of time. It is a record of a company₹s inflows and outflows. Cash inflow is defined as the movement of money into a business and cash outflow is defined as the movement of money out of a business.

Question. What does a cash flow indicate?

Answer: Cash Flow Projection shows how cash is expected to flow in and out of your business. For you, its an important tool for cash management, letting you know when your outflows are too high or when you might want to arrange short term investment to deal with a cash surplus.

Question. How is the requirement of cash in a business projected/estimated? What is the name of the statement that shows the cash requirements of a business?

Answer: A cash flow projection gives a better idea of how much capital investment your business idea needs. The Cash Flow Projection shows the cash that is anticipated to be generated or expended over a chosen period of time in the future.

A Cash Flow Projection is NOT a Cash Flow Statement.

The Cash Flow Statement shows how cash has flowed in and out of your business. In other words, it describes the cash flow that has occurred in the past. Cash Flow Statement, like Balance Sheet and Income Statement, deals with the past. It does not help in managing the current, day to day requirement. Cash Flow Projection, on the other hand, is a very critical management tool for the successful operation of the business.

Question. Distinguish between cash flow projection and cash flow statement.

Answer:

| Cash Flow Projection | Cash Flow Statement |

| A cash flow projection shows how much capital investment for business idea needs | Cash Flow Statement shows how cash has flowed in and out of your business |

| It is anticipated to be generated or | Cash Flow Statement deals with the past. |

| It is a very critical management tool for the successful operation of the business | It is a very critical management tool for the assessing business success |

Question. Why cash flow projection?

Answer: Every business must want to manage its affairs in a very efficient manner. Which means it must pay its suppliers as per agreed terms, pay the employees their wages on stipulated dates, pay government levies etc as per rules, procure services and pay for the same, pay utility bills & rent etc on time. The list is endless. Similarly it must collect what is due to it also in a timely manner.

It should strive to sell more so it can collect more. Very often, when business is expanding, your outflows can be more than in your inflows. This is so because there is always a lag between your spending (on raw materials, labor etc) and your receiving the sales revenue. Receipt of sales revenue may be delayed because you might have given credit or you have produced ahead of the sales (to cater to the high demand during festive season) and are temporarily holding finished goods stock. In such situations, you should be equipped with sufficient information to be able to arrange for needed funds.(More on this in Working Capital lesson).

Very nature of any business is uncertainty. You base your calculations on certain (hopefully realistic) assumptions. You plan the funds required using these assumptions. However, your actual performance, say of sales, could be higher or lower than your plan. It will rarely be exactly per plan. Or your collection from credit customers has lagged and you are running short of funds. There could be many other reasons as to why your well laid out funding plan has gone for a toss. To avoid such situations and be on top of things, reviewing your projections periodically and recasting the future based the current status (and not assumptions of the past) and what is likely to happen in the near future is very crucial. Cash Flow Projections is not a static document. It must be used as a dynamic tool.

An important question that arises is about the frequency and period (unit of time) of preparing Cash flow projections. The answer depends on the purpose for which the projection will be used.

♦ If it is for a Business Plan (to attract investors and lenders), it will be prepared at the initial stage – monthly for the first year, quarterly for the next two years and annual thereafter. These projections are not of much use for day to day cash management but meant for demonstrating the fluctuating need of the short term funds (working capital or overdraft facility). In fact, it almost takes the form of Cash Flow Statement and because it is for the future, it is also referred to as Pro-Forma Cash Flow Statement. (Pro Forma, a Latin word, means potential or expected in relation to a planned act).

♦ If it is for running the day to day operations, then the projections would cover a much shorter period of say 3 to 6 months (13 to 26 weeks). The unit of time could be a month or even a week. The length of the period is closely related to the volatility of the business and one‘s ability to forecast accurately.

♦ Once you have decided on the frequency of preparing a Cash Flow Projection, say weekly (period) to cover 13 weeks (horizon), or monthly to cover 6 months or even daily to cover a month, develop a format that suits your business. While there are generic formats, it will be helpful to develop one appropriate for your business, keeping the generic ones in mind.

♦ As you would be preparing this projection on periodic basis, please make sure that when one ―period‖ is over, it is dropped and a new period is added, keeping the length of the horizon intact.

♦ How accurate a Cash Flow Projection is depends on the period and horizon involved. A forecast covering the next 30 days could be taken as extremely reliable as the payments due to be made and received during that time may already be known. This means that the forecast will be extremely accurate unless there are unforeseen issues such as a customer going out of business before paying their bills. A forecast for the next 12 months may be less reliable as it will include estimates of future sales. This does not make the forecast

worthless: even if overall sales are unpredictable, a business owner may still have a very good idea of seasonal variations.

Question. How to develop a cash flow projection?

Answer:

♦ Based on your business characteristics like time period

♦ Develop the format, with items appropriate to the business

♦ A projected cash flow begins with the existing cash balance for the business. It then lists the sources of inflow and the anticipated payment dates (length of operating cycle). Add all other inflows like interest on deposits, sale of scrap, rent from space sub-let etc.

♦ The statement then looks at forthcoming expenditure (Fixed expenses such as regular sum such as staff costs and variable costs such as buying stock or materials.

♦ Where payment dates are variable, it is usually safest to work on the basis that you will pay suppliers as soon as possible but not receive payment from customers until the last possible date.

♦ Adding all outflows then enables you arrive at the surplus or deficit for the period. This, when combined with the opening balance, leads to deriving the closing balance – which becomes opening balance for the next period.

Question. What is financial management? What are the Objectives of financial management?

Answer: Financial Management means planning, organizing, directing and controlling the financial activities such as procurement and utilization of funds of the enterprise. It means applying general management principles to financial resources of the enterprise.

The financial management is generally concerned with procurement, allocation and control of financial resources of a concern. The objectives can be Main objective of Wealth maximization of shareholder‘s wealth.

1. To ensure regular and adequate supply of funds to the concern.

2. To ensure adequate returns to the shareholders.

3. To ensure optimum funds utilization. Once the funds are procured, they should be utilized in maximum possible way at least cost.

Question. Explain the process involved in planning a sound financial management strategy.

Answer: There are three key elements to the process of financial management:

1) Financial planning: Management need to ensure that enough funding is available at the right time to meet the needs of the business. In the short term, funding may be needed to invest in equipment and stocks, pay employees and fund sales made on credit. In the medium and long term, funding may be required for significant additions to the productive capacity of the business or to make acquisitions.

2) Financial control: Financial control is a critically important activity to help the business ensure that the business is meeting its objectives. Financial control addresses questions such as:

♦ Are assets being used efficiently?

♦ Are the businesses assets secure?

♦ Does management act in the best interest of shareholders and in accordance with business rules?

3) Financial decision-making: The key aspects of financial decision-making relate to investment, financing and dividends:

♦ Investments must be financed in some way – however there are always financing alternatives that can be considered. For example it is possible to raise finance from selling new shares, borrowing from banks or taking credit from suppliers

♦ A key financing decision is whether profits earned by the business should be retained rather than distributed to shareholders via dividends.

♦ If dividends are too high, the business may be starved of funding to reinvest in growing revenues and profits further.

Question. Define Budgeting

Answer: The word Budget is used in common parlance to mean allocation of resources. For any business, a budget is a quantitative expression of a plan for a defined period of time. It may include planned sales volumes and revenues, resource quantities, costs and expenses etc.

Question. Why are the essentials considerations while preparing a budget?

Answer:

• To control resources

• To communicate plans to various responsibility centre managers.

• To motivate managers to strive to achieve budget goals.

• To evaluate the performance of managers

• For accountability

Question. Name and briefly explain the different types of budgets prepared by an enterprise.

Answer:

• Sales budget: an estimate of future sales, often broken down into both units and currency. It is used to create company sales goals.

• Production budget: an estimate of the number of units that must be manufactured to meet the sales goals. The production budget also estimates the various costs involved with manufacturing those units, including labour and material.

• Capital budget: It is used to determine whether an organization₹s long term investments such as new machinery, replacement machinery, new plants, new products, and research development projects are worth pursuing.

• Cash flow/cash budget: a prediction of future cash receipts and expenditures for a particular time period. It usually covers a period in the short term future. The cash flow budget helps the business determine when income will be sufficient to cover expenses and when the company will need to seek outside financing.

• Marketing budget: an estimate of the funds needed for promotion, advertising, and public relations in order to market the product or service.

• Project budget: a prediction of the costs associated with a particular company project. These costs include labour, materials, and other related expenses. The project budget is often broken down into specific tasks, with task budgets assigned to each. A cost estimate is used to establish a project budget. While budget is the final product, the process of arriving at a budget is the budgeting process.

Question. Distinguish between Budgets and budgeting.

Answer:

| Budgets | Budgeting |

| A budget is an allocation of money for some purpose | Budgeting is a budgetary process is managed with extreme skill and care |

| Budgets predict income, profits, and returns on investment a year ahead | Budgeting is a tool of control and are also used as a means of determining such rewards as profit-sharing and bonuses |

Question. Explain the process of Budgeting in an enterprise.

Answer: In large corporations, budgeting is a collective process in which operating units (Departments) prepare their plans according to the corporate goals issued by top management. Each unit (Department) plan is intended to contribute to the achievement of the corporate goals. Unit managers prepare projections of sales, operating costs, overhead costs, and capital requirements. They calculate operating profits and returns on the investment they intend to use. As part of this process, each unit presents its plans and budget for review by the top management panel and may, thereafter, make whatever changes result from instructions from or negotiations with the higher level.

Normally, monthly or quarterly budget reviews track performance against the budget. As part of such reviews, changes to the budget may be approved. At yearend managers are judged by their performance against the budget.

Question. What are the known benefits of budgeting for an enterprise?

Answer:

• For start-up entrepreneurs, a budget is like a roadmap that can help them set goals and assess the validity of their business concept.

• For established small businesses, a budget determines how the business is performing through the years, and in helping to identify possible future investments.

• Business leaders can compare actual figures and catch potential business shortfalls or other problems early.

• Budgets can also be used to prove credit worthiness to banks or for bringing on new partners or customers.

• The most important benefit of formal budgeting lies in ensuring that responsible managers take time in thinking about their operation by looking at all of its aspects.

• Budgeting creates a comprehensive picture of the future and makes both opportunities and barriers conscious.

Question. What is the main cost involved in the process of budgeting?

Answer: The chief cost of the budget process is time. In some corporations the process takes on a life of its own and becomes a difficult exercise of excessive difficulty which, moreover, prevents unit managers from doing any thinking: their time is consumed in efforts to fulfil the corporate requirements dictated by the top management.

Question. What are the different forms of budgeting process used by an enterprise?

Answer: The two dominant forms of budgeting processes are traditional and zero-based. Business planning is usually a combination of the two.

• Traditional budgeting is based on a review of past performance and then the projection of such findings to the future with modifications. For example: If inflation is high, cost trends of the last several years are projected forward but with adjustments both for inflation and for projected growth or decline in business activity. Past sales patterns, using established trends in sales growth, are projected; new sales from planned new product introductions are then added.

• Zero-based budgeting is the creation of a completely new budget, if no history existed. When using this method, the operation must justify and document every item of expenditure and income again.

Question. Name and explain the different types of budgets prepared by a small scale enterprise?

Answer:

• Operational budget - It forecasts and tries to predict yearly revenue and expenses for a business. This budget can be updated with actual figures on a monthly basis and then revised for the year, if needed.

• Cash flow budget - A cash flow budget details the amount of cash you collect and pay out. This is generally tallied on a monthly basis, but some businesses tabulate this weekly. A positive cash flow is essential to grow your business.

• Capital budget - The capital budget helps to know how much money is required to purchase new equipment or procedures to launch new products or increase production or services. This budget estimates the value of capital purchases you need for your business to grow and increase revenues.

Question. What is the importance of budgeting for an enterprise?

Answer: Budgeting is an important and integral part of running a business. Various future strategies planned in the business like sales quantity and revenue, costs, resources required, fixed expenses must be translated in to numbers. Budget and budgeting help managers to manage business. One of the reasons businesses fail is due to lack of discipline.

Question. Why does an enterprise need capital?

Answer:

a) For procuring or investing in longer term assets: land, building, machinery, equipment etc. These are typically known as Fixed Assets. Once pushed in to service, they last over a reasonably longer period. These are placed in service for carrying out production and sales or service etc. and are not traded or sold to receive money. In other words, money invested on these items does not result in direct cash inflow for the business.

b) For buying raw materials, packing materials, paying rent, insurance premium, utility bills, wages and salaries and for many other services and/or materials used in the production or service. In other words this is the money needed for the day-to-day operations of the business. Money needed to fund the normal, day to day operations is known as the Working Capital. It ensures that the enterprise has enough cash to pay its debts and expenses as they fall due.

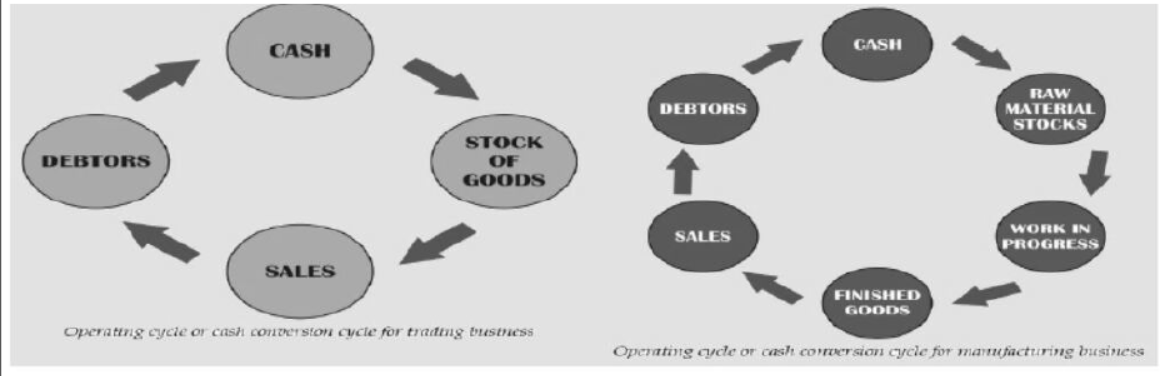

Question. What is meant by „Operating cycle‟ or Cash Conversion cycle‟? explain the working of an Operating Cycle.

Answer: In manufacturing activity, one starts with buying raw materials and packing materials etc. These materials are then ―converted‖ in to the end product. During the time required to convert raw material to end product, various expenses like wages, rent, salary, utility bill, insurance etc. are to be paid. Once the end product is ready, it has to be sold and money received from the customer. If it is a cash sale, the money is received immediately and for credit sale, it is received after the credit period. The duration between buying the raw material and receiving the cash from the customer is known as the Operating Cycle or Cash Conversion Cycle.

The cash conversion cycle (CCC or Operating Cycle) is the length of time between a firm₹s purchase of inventory and the receipt of cash from accounts receivable. It is the time required for a business to turn purchases into cash receipts from customers. CCC represents the number of days a firm₹s cash remains tied up within the operations of the business. Different products will have different operating cycles. If the conversion takes longer then the cycle will be longer. For trading, where there is no manufacturing, the operating cycle will be shorter. Longer the operating cycle, working capital quantum is more; shorter the cycle, less working capital is needed.

Question. What do you mean by Gross working capital?

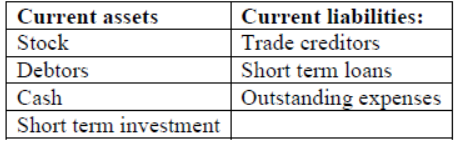

Answer: Gross working capital OR Circulating Capital is the sum total of all current assets of the business. These include cash, inventory (raw materials, work in process, finished goods, spares etc.) and accounts receivable (or trade debtors).

Current assets comprise items that would get converted in to cash in the short-run, say, within the normal operating cycle (cash conversion cycle) of the business.

Current liabilities represent short-term source of funds and are expected to fall due or mature for payment in a short period, generally within a year. These typically consist of payables to vendors and service providers, employees, other short term borrowings and provisions.

A list of current assets and current liabilities for reference:

Question. Define Inventory

Answer: The word inventory, in the most common means collection of things and a list of those items in our mind. In business, inventory are required directly or indirectly to make a sale (final product) and may also represent different stages in the process of getting the final product.

Inventory, in manufacturing business deals with tangible items.

Inventory in trading business (wholesale or retail), certain service industries there may be use of tangible material like spare parts, consumables like rags, solvents, lubricants etc. in repair shop.

In the accounting, inventory refers to the value of all the items in the inventory list that is owned by the business. It refers to the stock of goods held by a business.

Question. Define Inventory Control

Answer: When we use the word control, it simply means things are under control. In a business enterprise, inventory control to help achieve desirable behaviour of the inventory items. Desirable behaviour of any inventory item would in business mean that there should never be ‘Out of Stock” or there should be the right quantity of stocks, Not too much stock OR Not too less Stock. However, holding stock also has cost like carrying cost, which should be low. Management of stock is therefore called Inventory Control.

Question. What are the physical and fiscal (money expenses) items that make up the inventory?

Answer: A good inventory control system takes care of both physical and fiscal aspects. The nature of items that make up the inventory are:

• Stock keeping unit (SKU) code: Each and every item in the inventory is to be identified with a unique code which signifies certain aspects of the item. It can be colour, size, weight or any other characteristic that is of importance in its use. The SKU code can be a combination of alpha and numeric. SKU is the very basic unit for data collection. Bar Codes and RFID (Radio Frequency Identification) tags are used in tracking etc. using SKU.

• Motley crowd: In business, inventory in also expressed in money value in the accounting statement. Inventory can be classified as Raw Materials, Packing Materials, Spare Parts, Semi Finished Goods (or WIP Work In Progress), Finished Goods, Consumables etc. The SKU code should definitely help us identify which class the item belongs but not much else. The treatment for each class will have to be different, keeping in mind some of the factors identified here.

• Space: Space requirement for all items will not be identical; neither will it have proportionate relationship with the cost of the item. There can be many bulky items with low value (straw for use in paper mill) as well as high value items with low volume (Diamonds). Good Inventory Control system will have to take due note of this.

• Value: Not all SKUs have same value.

• Lead time: Lead time to manufacture or procure an item depends on many factors. Combined effect of factors - like standard or special raw material, processing time, scheduling of machines, distance between source and user point etc. - makes up the lead time for an item.

• Standard v/s made to order: Some of the items in the inventory could be commodity items with no significant differentiation and hence easy to substitute, or many suppliers produce to same specifications and hence easy to choose from. Others may be specifically made to order and hence possibly limited sources to order from.

• Seasonality of supply: If the item is an agricultural product (grains, vegetables, fruits etc.), its supply would be seasonal. This can play a role in designing the inventory control system.

• Demand not uniform or not predictable: Demand for an item could be seasonal weather, festival seasons, events, school opening etc. can play a significant part in this. In some cases it is easy to forecast raw material for items produced to order; but in others not so easy requirement of a spare part.

• Shelf life: Items like vegetables, fruits, flowers and fish are perishable in nature. This calls for

special storage conditions and equipment like cold storage, freezers etc. These have financial implications. Similarly some of the manufactured food or medicinal products have expiry dates beyond which they are not fit for consumption. This imposes certain constraints on inventory management.

• Safety aspects: Some of the items are hazardous in nature and special precautions have to be taken in their storage. Examples are – gasoline, other combustible items, some hazardous chemicals etc. In a factory manufacturing safety matches, phosphorous and potassium chlorate are not stored in the same or even adjoining areas, for fear of accidental mix up. In fact, even their path of delivery to the respective end use points do not cross.

• Obsolescence: Due to advancement in technology, certain items may not be used and their demand drops off. These are the various characteristics of SKUs that have to be kept in mind while designing inventory control systems – one size will not fit all.

Question. Explain in details the Pareto₹s Principle and ABC analysis for inventory control

Answer: The principle is named for Vilfredo Pareto, an Italian economist. Pareto₹s Principle, holds that in a given system, a relative handful of "causes" will produce the majority of "effects." For example, one may find that 20% of customers are responsible for 80% of sales, or that 30% of the product lines result in 70% of returns.

Pareto found that roughly 20% of the population held title to about 80% of the land. Legend has it that he further developed the theory upon observing that 20% of the pea pods in his garden produced 80% of the peas. For this reason, Pareto₹s Principle is often referred to as the "80/20" rule. There₹s nothing "magic" about the 80% figure, though. Many business systems do in fact show an 80/20 relationship; others don₹t. A relatively handful of things will generate the bulk of the results or in any group will have “vital few and trivial many”.

Pareto₹s law has applications in business, including inventory control, where it forms the basis for a technique called ABC analysis. The value of the Pareto Principle in management is in reminding us to stay focused on the 20% that matters.

Businesses that maintain an inventory of goods to sell to customers or for use in manufacturing commonly observe a Pareto distribution in the value of that inventory. For example, a company might determine that 20% of the products in its inventory account for 80% of the total value of inventory. Managing inventory is time-consuming and expensive.

ABC analysis

In ABC analysis, a company reviews its inventory and sorts all SKUs into three categories, called "A”, "B" and "C" items. The typical breakdown might look like this:

"A" inventory: 20 % of SKUs. 80% of value.

"B" inventory: 30 % of SKUs, 15 % of value.

"C" inventory: 50 % of SKUs, 5 % of value.

Once a company has conducted its ABC analysis, it can devise an inventory-control strategy that focuses effort where it will have the greatest effect. Items in "A" inventory are tightly controlled, meaning the company keeps close watch on how much it has in stock; pays close attention to current demand and forecasts for future demand; and carefully plans its ordering so that it neither runs out nor finishes up with too much excess inventory that can become obsolete.

Items in "B" inventory are also watched closely, but the company reviews its ordering strategy less often. Since items in "C" inventory are the least expensive, the company can order them in bulk and exercise minimal controls; all that really matters is that the company doesnt run out.

A - Outstandingly important

B - of average importance

C - Relatively unimportant as a basis for a control scheme

Each category has to be handled in a different way, with more attention being devoted to category A, less to B, and still less to C.

Thus, applied in the context of inventory, it₹s a determination of the relative ratios between the number of items and the currency value of the items purchased/consumed on a repetitive basis:

• 10-20% of the items ('A' class) account for 70-80% of the consumption.

• The next, 15-25% (₹B₹ class) account for 10-20% of the consumption and.

• The balance, 65-75% ('C'class) account for 5-10% of the consumption.

₹A₹ class items are closely monitored because of the value involved (70-80%).

Question. Explain the Economic order quantity (EOQ) of inventory control.

Answer: An effective Inventory Control System focus on the objective to ensure that there is no stock-out situation. If that were the only principles, then it is easy to order large quantity and be very safe. However, there is cost associated with ordering and holding inventory.

Assuming that the future demand is known, one needs to determine when to place an order (Reorder Point) and how much to order (Order Quantity). Reorder point takes due note of the lead time and demand during lead time.

For example, if manufacturing lead time is 2 months, and demand during this period is expected to be 300 units per month, then an order is to be placed when the stock or inventory level reaches 600 pieces (Reorder point = usage rate x lead time).

Reorder formula = Average daily usage rate × Lead time in days

Under perfect situation, the new quantity will arrive, just as the stock reaches zero.

Real life is not that simple or straightforward. There is variability in the rate of demand (or consumption) as well as in the supply or manufacturing lead time etc. Therefore, it may reach a zero stock status, before the supply arrives. To cater to such variability, the concept of safety stock is used.

In this particular case, 150 may be added as safety stock. The reorder level then would be 750 pieces i.e. place new order when the stock level reaches 750.

A level of safety stock is determined keeping the possible variation in lead time and variation in demand during lead time in mind.

Question. What are the Costs involved in Economic Order Quantity method of inventory control?

Answer:

There are two costs involved:

• Ordering Cost: It includes paperwork for placing order, receiving, inspection, warehouse handling etc. and another for holding the inventory.

• Inventory Carrying Cost: this cost includes cost of money tied up i.e. interest, space cost, insurance etc.

Question. What are the assumptions of Economic Order Quantity (EOQ) of inventory control?

1. Future demand is known and is uniform throughout the period.

2. Unit price of item does not vary with quantity ordered.

Question. Explain the method of calculating inventory levels using the Economic Order Qunatity (EOQ) method of inventory control.

Answer: Let us use following symbols:

D: Annual demand for the item (SKU)

P: Cost of placing and receiving one order (does not include purchase price)

C: Inventory carrying cost per unit. This may be derived by multiplying the unit price of the item by the carrying cost expressed as %age of the unit price.

S: Safety Stock level for the item.

Q*: Economic order quantity

Total number of orders being placed during the year will be = D/Q

Total ordering cost = PD/Q

Average inventory = S+Q/2

Inventory carrying cost = C x (S+Q/2)

Total annual cost = PD/Q + C x (S +Q/2)|

safety stock S is not dependent on Q. Irrespective of the value of Q, value of S depends on variability of lead time and demand rate. So it can be removed from the equation and get a modified total cost as follows:

Modified annual cost =PD/Q+(CxQ/2)

Table 4:

The ordering cost PD/Q and inventory carrying cost (C x Q/2) equal each other when the total cost is the lowest.

Or PD/Q = (C x Q/2)

Or 2 PD = CQ2

Or Q = √2PD/2 OR ECONOMIC ORDER QUANTITY = √2PD/C

Therefore, EOQ is the value when derivative of modified annual cost is zero. Therefore, differentiating the equation, with respect to Q,

Formula for calculating EOQ =

• D: Annual Demand for the item (SKU)

• P: Cost of placing and receiving one Order (does not include purchase price)

• C: Inventory carrying cost per unit. This may be derived by multiplying the unit price of the item by the carrying cost expressed as %age of the unit price.

• S: Safety Stock level for the item.

• Q: Economic Order Quantity

Q = √2PD/2 ECONOMIC ORDER QUANTITY = √2PD/C

Example 1:

Annual Quantity of jeans sold by a shop is 1,200 at the rate of ` 100/- per month. Cost of placing an order and receiving goods is ₹ 500/- per order. Inventory holding cost is ₹ 30/- per annum. What is the economic order Quantity for the shop keeper?

Here, D = 1,200;

P = 500 and

C = 30.

Q = √2PD/C

Q = √2 X 500 X 1200/30 = √40000 = 200

Therefore, EOQ is 200 jeans.

Question. What are the various aspects of inventory control by EOQ method?

Answer: Inventory control has many sides which range from monetary, physical, safety and many others. It is crucial to understand these aspects in designing an inventory control system. ABC system is one such. There are other different system, including Just-in- time (JIT), perpetual inventory etc.

Economic Order Quantity is a key factor (but not the only one) in managing any inventory.

Question. Name and briefly explain some commonly used Measures of profitability.

Answer: The purpose of any economic activity is earning profit. While profit is the motive, question arises as to how to measure or compare profit from one activity or project with profit from many others. Suppose we spend ` 1,000/- and earn a profit of ₹ 400/- in one case and in another case spend ₹100,000/- and earn profit of ₹ 10,000/- which makes more profit?

The answer obviously is the later one. However, if we ask which is more profitable then the answer is the first one. That is because; relationship between profit and spending is being compared. However, in both cases, the time taken to earn the profit is not considered. Therefore, the need arises for some common understanding and yardstick or measurement technique.

Return on Investment (ROI) and Return on Equity (ROE) are two such critical profitability ratios. These measures are applicable to individual projects, such as the purchase and subsequent sale of an apartment, a small grocery business or a multinational conglomerate. Therefore, it pays to understand ROE and ROI.

Question. Define Return on investment. Show ROI with a working example.

Answer: Return on investment equals the net income from a business or a project divided by the total money invested in the venture multiplied by 100.

Return to Investment = Net Profit/Total Capital Invested x 100

For example, you spend `100,000/- to open a grocery shop and make a net profit of ` 20,000/- in one year, your annual ROI equals

Return to Investment = Net Profit x 100 = 20000/100000 x 100 = 20%%

When calculating ROI, the investment will include not only what the investor spent out of his/her pocket, but also all borrowed funds. In the example, the owner might have invested ` 40, 000/- of his own money (equity) and secured a loan for ` 60, 000/-.

Question. Define Return on equity. Show Return on equity with help of a working example.

Answer: Return on equity

Return on equity OR ROE is calculated by dividing the net income by the equity of the investor and multiplying the result by 100.

Retuen to Equity = Net Income/Equity x 100

In the example, the grocery owner has an equity stake of `40,000/- in the business. He has borrowed ` 60,000/-. This will attract an interest of ` 6,000/- @ of 10% per annum. The net profit, then would be ` 14,000/- (= 20,000 – 6,000). So, ROE is (14,000 / 40,000) x 100 = 35%.

Retuen to Equity = Net Income/Equity x 100 = 14000/40000 x 100 = 35%

This means that for every Rupee of own money the owner put into the business, he made 35 paisa. The ROI of 20%, on the other hand, means that for every Rupee of combined assets and loans invested, the business yielded a 20 paisa average profit per Rupee invested (equity plus loan).

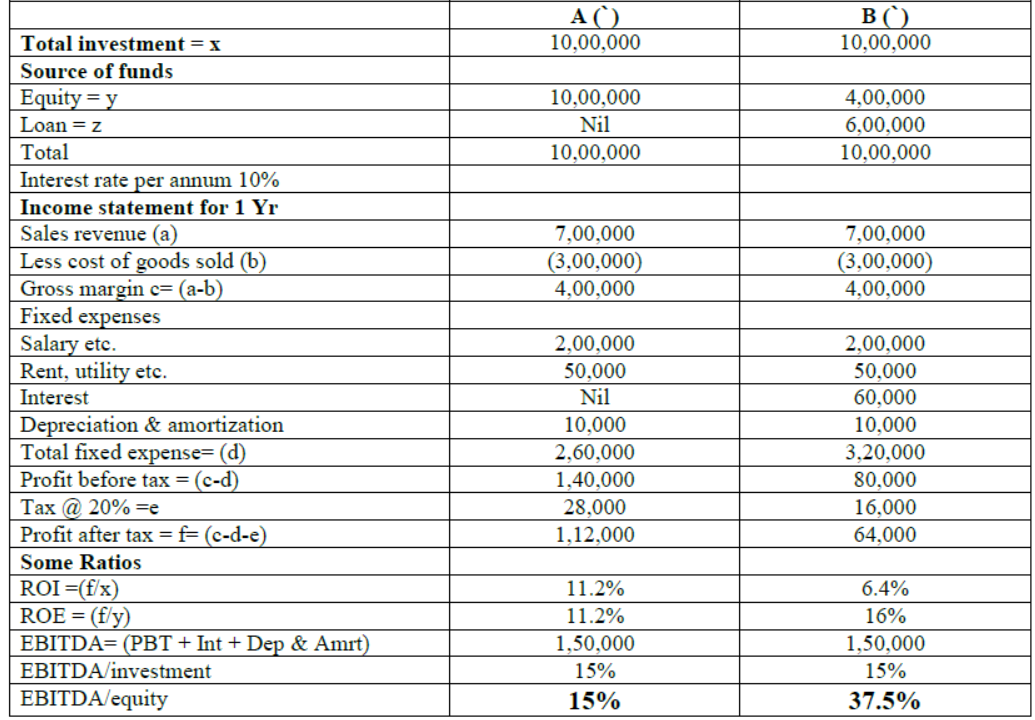

Question. Which one to use? ROI or ROE? OR What are the benefits of Trading on Equity?

Answer: Let us take the case of two people, A & B starting identical business and performing identically in terms of sales, variable cost, fixed costs etc. The only difference is A did not borrow any money and B did. Interest rate is 10% per annum. Here are some numbers for both A & B.

Table 5:

EBITDA – stands for Earnings Before interest, Tax, Depreciation and Amortization. This is arrived at by adding interest, depreciation and amortization to Profit Before Taxes.

In this example, we can see that B makes less profit (whether before or after tax) than A. This is reflected in lower ROI for B. However, B has invested lesser amount than A and as a result, when we compare profit in relation to own funds or equity, B comes out ahead of A – 16% V/s 11.2%.

For a true measure of how own money is being used, ROE is a good indicator. ROI, on the other hand, gives an indication of how the total money is being used.

Question. What is EBITDA?

Answer: The acronym EBITDA stands for earnings before interest, taxes, depreciation and amortization.

Question. Why is EBITDA calculated? What its usefulness in Business?

Answer: When financial statements are prepared, the results are a combination of different factors: some are managerial decisions, others entrepreneurial and some others are government policies. To measure or compare true effectiveness of one operation and the managerial decisions with another one, the extraneous factors must be normalized.

♦ Interest: If one business is started with all equity and another one with some loan, the second one will have an interest element in its cost. This interest is strictly not because of the operational efficiency or otherwise, but due to the funding decision. Adding back the interest to PBT, takes away the effect of this funding decision.

♦ Taxes: Taxes are levied by the government. If you are comparing profits of one period to another, the rates might have changed. There may be other reasons why the ―tax treatment‖ is different for two companies state taxes, special levies etc. The business owner or manger has no control over these. To avoid distortion in the profit, tax component is added back to the profit.

Question. What are „Depreciation‟ and „Amortization‟?

Answer: There are different options available to depreciate (tangible asset) or amortize (intangible asset). One company may use a particular method and another one a totally different one. One may write off slowly and another one fast – both being allowed by the authorities. So to avoid distortion due to differing practices being followed, Depreciation & Amortization is added back. When one wants to assess the efficiency of operations either for acquisition or comparison with benchmarked operations or over different time periods, ability to generate cash by business is crucial.

EBITDA is one such measurement. It is one of the most widely used measures for evaluating a business for acquisition etc. Price for a business is often quoted in terms of a multiple of its EBITDA – say (M) x (EBITDA). M has numerical value that varies from industry to industry.

Free study material for Other Subjects

CBSE Other Subjects Class 12 Business Arithmetic Notes Worksheet

Students can use the practice questions and answers provided above for Business Arithmetic Notes to prepare for their upcoming school tests. This resource is designed by expert teachers as per the latest 2026 syllabus released by CBSE for Class 12. We suggest that Class 12 students solve these questions daily for a strong foundation in Other Subjects.

Business Arithmetic Notes Solutions & NCERT Alignment

Our expert teachers have referred to the latest NCERT book for Class 12 Other Subjects to create these exercises. After solving the questions you should compare your answers with our detailed solutions as they have been designed by expert teachers. You will understand the correct way to write answers for the CBSE exams. You can also see above MCQ questions for Other Subjects to cover every important topic in the chapter.

Class 12 Exam Preparation Strategy

Regular practice of this Class 12 Other Subjects study material helps you to be familiar with the most regularly asked exam topics. If you find any topic in Business Arithmetic Notes difficult then you can refer to our NCERT solutions for Class 12 Other Subjects. All revision sheets and printable assignments on studiestoday.com are free and updated to help students get better scores in their school examinations.

FAQs

You can download the latest chapter-wise printable worksheets for Class 12 Other Subjects Business Arithmetic Notes for free from StudiesToday.com. These have been made as per the latest CBSE curriculum for this academic year.

Yes, Class 12 Other Subjects worksheets for Business Arithmetic Notes focus on activity-based learning and also competency-style questions. This helps students to apply theoretical knowledge to practical scenarios.

Yes, we have provided solved worksheets for Class 12 Other Subjects Business Arithmetic Notes to help students verify their answers instantly.

Yes, our Class 12 Other Subjects test sheets are mobile-friendly PDFs and can be printed by teachers for classroom.

For Business Arithmetic Notes, regular practice with our worksheets will improve question-handling speed and help students understand all technical terms and diagrams.