Download the latest CBSE Class 11 Accountancy Accounts For Incomplete Records Notes Set 02 in PDF format. These Class 11 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 11 students.

Revision Notes for Class 11 Accountancy Chapter 11 Accounts from Incomplete Records

To secure a higher rank, students should use these Class 11 Accountancy Chapter 11 Accounts from Incomplete Records notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Chapter 11 Accounts from Incomplete Records Revision Notes for Class 11 Accountancy

UNIT:10

ACCOUNTS FOR INCOMPLETE RECORDS

“A system of book-keeping in which, as a rule, only records of cash and of personal accounts are maintained, it is always incomplete double entry system, varying with circumstances” Unit at a Glance:

- Introduction

- Salient features

- Uses

- Limitations

- Difference between double entry system and incomplete records

- Ascertainment of profit or loss from incomplete records

- Conversion into double entry method

- numerical exercises

Introduction:

Accounting records which are not prepared in accordance with double entry system method are described as accounts for incomplete records. SALIENT FEATURES

1. Apply of personal accounts only ( ignores nominal and real accounts)

2. Maintenance of cash book.( Cash book is prepared )

3. Based on original vouchers. (Collection of data is made with original vouchers)

4. Lack of Similarity. (Method of preparation of books differs from firm to firm, it prepared as per the need of the business.

5. Preparation of final accounts. (After converting the information into double entry system final accounts are prepared. Due to this Statement of affairs is prepared instead of Balance sheet)

Uses

1. Easy method (Not requires any specific knowledge)

2. Economical( Can be prepared by without having more staff)

3. Suitable for small concerns (Few assets and liabilities are to be recorded)

4. Not – rigid (Can be modified/changed as per requirement of business)

5. Easy finding of profit & losses. (Only opening and Closing capital is required)

Limitations

1. Impossible to find fraud (As Trial balance is ignored)

2. Incomplete system (No set rules are followed)

3. Unable to find adequate profit & losses. (Ignorance of nominal accounts)

4. Difficulty in preparation of balance sheet.(Lack of valuation of goodwill)

5. Unable to retain full control on asserts. (Real accounts are ignored, it is difficult to make full control on assets)

6. Unsuitable for planning in control(Lack of reliable figure)

7. Lack of internal checking(Fails to adopt double entry system)

8. Improper evaluation of asserts (Ignorance of certain information like depreciation etc.)

DIFFERENCE BETWEEN DOUBLE ENTRY SYSTEM & INCOMPLETE RECORDS

Basis of difference Recording of both aspects (Double entry records every transaction and incomplete records few transactions)

1. Type of accounts (All accounts are considered in double entry only personal account are considered in incomplete records)

2. Trial balance (Trial balance is prepared in double entry system,Trial balance is not prepared in incomplete records )

3. Net profit/ loss (Profit/Loss is calculated by preparing trading and profit &loss a/c in double entry system, Statement of profit is prepared in incomplete records to find the same.

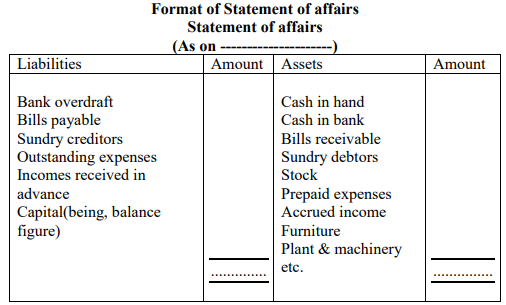

4. Financial position (Balance sheet is prepared in double entry and statement of affairs is prepared in incomplete records)

5. Adjustment (Adjustment are considered in double entry ,while adjustments are not considered in incomplete records)

ASCERTAINMENT OF PROFIT OR LOSS FROM INCOMPLETE RECORDS

1. Statements of affairs method

2. Conversion into double entry method

Statement of affairs method: Under this method Opening and Closing capital is calculated. Then statement of profit is prepared to find profit/loss during the year.

Please click the link below to download pdf file for CBSE Class 11 Accountancy Accounts For Incomplete Records Notes Set B.

Free study material for Accountancy

CBSE Class 11 Accountancy Chapter 11 Accounts from Incomplete Records Notes

Students can use these Revision Notes for Chapter 11 Accounts from Incomplete Records to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 11. Our teachers always suggest that Class 11 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Chapter 11 Accounts from Incomplete Records Summary

Our expert team has used the official NCERT book for Class 11 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 11. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Chapter 11 Accounts from Incomplete Records Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Chapter 11 Accounts from Incomplete Records. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 11 Accountancy Accounts For Incomplete Records Notes Set 02 from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 11 students get the best study material for Accountancy.

Yes, our CBSE Class 11 Accountancy Accounts For Incomplete Records Notes Set 02 include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 11 Accountancy Accounts For Incomplete Records Notes Set 02 provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 11 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 11 Accountancy Accounts For Incomplete Records Notes Set 02, Class 11 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 11 Accountancy Accounts For Incomplete Records Notes Set 02, are available for immediate free download. Class 11 Accountancy study material is available in PDF and can be downloaded on mobile.