Read and download the CBSE Class 12 Economics Producer Behavior and Supply Assignment for the 2026-27 academic session. We have provided comprehensive Class 12 Economics school assignments that have important solved questions and answers for Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition. These resources have been carefuly prepared by expert teachers as per the latest NCERT, CBSE, and KVS syllabus guidelines.

Solved Assignment for Class 12 Economics Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition

Practicing these Class 12 Economics problems daily is must to improve your conceptual understanding and score better marks in school examinations. These printable assignments are a perfect assessment tool for Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition, covering both basic and advanced level questions to help you get more marks in exams.

Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition Class 12 Solved Questions and Answers

POINTS TO REMEMBER

❑ Total production refers to the sum total of production done by using all units of variable factors over a given period of time.

❑ Average production is the per unit output of variable factor (labour) employed.

AP = TP variable input

❑ Marginal product is addition to total product resulting from employing one additional unit of variable input.

❑ Returns to a factor : In a short period when additional units of variable factors are employed with given fixed factors, then returns to a factor operates. Returns to a factor shows the changes in total products, marginal product which arises due to change in ratio between fixed and variable factor.

They are as follows :

(A) Increasing returns to a factor : In the initial stage as more and more units of variable factor are employed with fixed factor total physical production increases at increasing rate.

(B) Diminishing returns to a factor : As more and more units of variable factors are employed with fixed factors, then total product increases at diminishing rate.

(C) Negative returns to a factor : This is the last stage of returns to a factor. As more and more units of variable factors are employed with given fixed factors, total production starts decreasing and marginal product becomes negative.

Relation between Total, Average and Marginal Product

1. So long as marginal product rises, total product increases at increasing rate.

2. Marginal product starts falling but remains positive, total product rises at diminishing rate in this stage.

3. When marginal product becomes negative, then total product starts falling in this stage.

4. So long as average production is less than marginal product, average production increases Marginal product intersects average product at the point where average product is maximum. After this average product

starts falling and is more than marginal product in this stage.

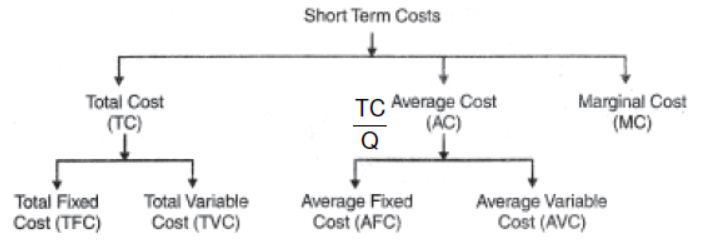

❑ Cost : Cost is the sum of direct (explicit cost) and indirect cost (implicit cost).

❑ Those monetary payments, which are incurred by producers for payment those of factor and non-factor inputs which are not owned by produces are called Direct Cost.

❑ Implicit cost is the cost of self owned resources of the production used in production process.

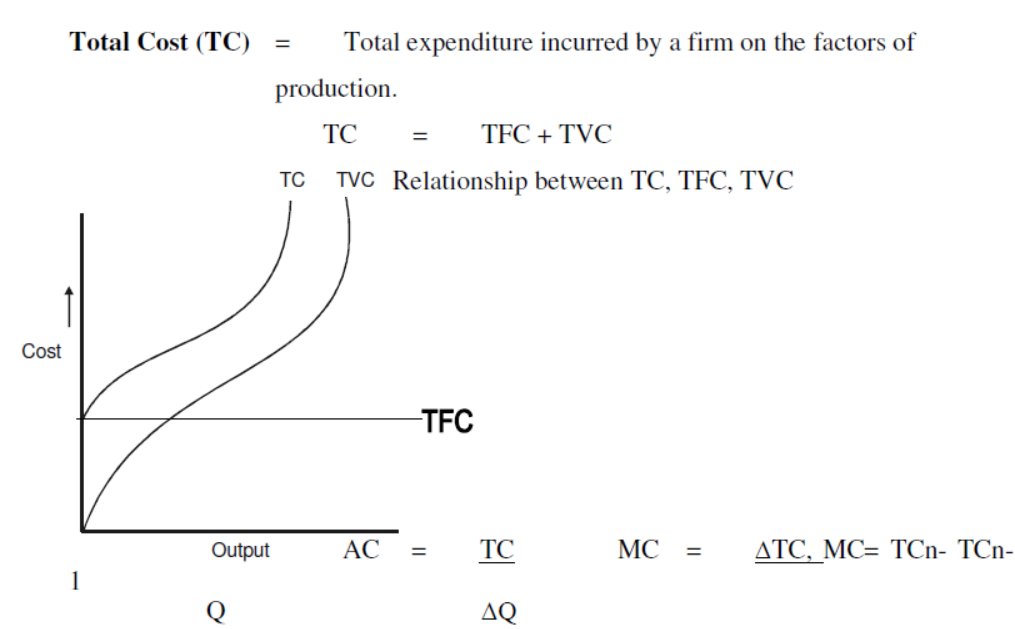

❑ Total cost is the sum of total fixed cost and total variable cost.

TC = TFC + TVC or TC = AC X Q

❑ Total fixed cost remains constant at all levels of output. It is not zero even at zero output level. Therefore, TFC curve is parallel to OX-axis.

TFC = TC – TVC or TFC = AFC × Q

❑ Total variable cost is the cost which vary with the quantity of output produced.

It is zero at zero level of output. TVC curve is parallel to TC curve.

TVC = TC – TFC or TVC = AVC × Q

❑ Average cost is per unit of total cost. It is the sum of average fixed cost and average variable cost.

AC = TC

or AC = AFC + AVC

❑ Average fixed cost is per unit of total fixed cost.

AFC = or AFC = AC – AVC

❑ Per unit of total variable cost is called average variable cost.

AVC = or AVC = AC – AFC

❑ Net increase in cost for producing one additional unit is called marginal cost.

MCn = TVCn – TVCn–1 or MC = TFC/Q

Relation Between Short-Term Costs

❑ Total cost curve and total variable cost curve remains parallel to each other. The vertical distance between these two curves is equal to total fixed cost.

❑ TFC curve remains parallel to X aixs and TVC curve remains parallel to TC curve.

❑ With increase in level of output, the vertical distance between AFC curve and AC curve goes on increasing. On contrary the vertical distance between AC curve and AVC curve goes on decreasing but these two curves never intersect because average fixed cost is never zero.

❑ Marginal cost curve intersects average cost curve and average variable cost curve at their minimum point. After the point of intersection with increase in output, AC curve and AVC curve starts rising.

❑ MC curve remains under the AC and AVC curve before inter section point but after inter section point AC and AVC curve remains under the MC curve.

❑ Average cost and average variable cost falls till they are more than marginal cost. When these two costs are less than marginal cost, in that situation both (AC and AVC) rise.

❑ Money received from the sale of product is called revenue.

❑ Total revenue is the amount received from the sale of given units of a commodity over a particular period of time.

TR = AR × Q or TR= SMR

❑ Per unit revenue received from the sale of given units of a commodity is called average revenue. Average revenue is equal to price.

AR = TR/Q or = P = Price.

❑ Marginal revenue is net addition to total revenue when one additional unit of output is sold.

MR = ΔTR/ΔQ PXQ/Q

❑ Behaviour of TR, AR and MR when per unit price remains constant or firm can sell additional quantity of a good at same price

(a) Average revenue and marginal revenue remains constant at all levels of output and AR and MR curves are parallel to ox-axis.

(b) Total revenue increases at constant rate and TR curve is positively sloped straight line passing through the origin.

❑ Behaviour of TR, AR and MR when price falls with additional unit of output sold or there is monopoly or monopolistic competition in the market

(a) Average revenue and marginal revenue curves have negative slope.

MR curve lies below AR curve.

(b) Marginal revenue falls, twice the rate of average revenue.

(c) So long as marginal revenue is positive, total revenue increases. When marginal revenue is zero, total revenue is maximum and when marginal revenue becomes negative, TR starts falling.

❑ Concept of Producer’s Equilibrium : If refers the stage where producer getting maximum profit.

(A) MR and MC Approach : Conditions of producers equilibrium according to this approach are :

(a) Equality between MR and MC

(b) MC curve should cut the MR curve from below at the point of equilibrium.

Or

MC should be more than MR after the equilibrium point, with increase in output.

❑ Supply : Refers to the amount of the commodity that a firm or seller is willing to offer or to sell in a given period of time at various prices.

❑ Individual Supply : Refers to quantity of a commodity that an individual firm is willing and able to offer for sale at each possible price during a given period of time.

❑ Stock : Refers to the total quantity of a particular commodity available with the firm at a particular point of time.

❑ Supply Schedule : Refers to a tabular presentation which shows various quantities of a commodity that a producer is willing to supply at different prices, during a given period of time.

Supply curve : Refers to the graphical representation of supply schedule which represents various quantities of a commodity that a producer is willing to supply at different prices during given period of time.

❑ Law of Supply : States the direct relationship between price and quantity supplied, keeping other factors constant.

Exceptions to Law of Supply

1. Future Expectation

2. Agricul

3. Perishable goods

4. Rare goods

5. Backward countries.

❑ Price Elasticity of Supply : Refer to the degree of responsiveness of supply of a commodity with reference to a change in price of such commodity.

It is always positive due to direct relationship between price and quantity supplied.

Price Elasticity of Supply (Es) = Percentage change in quantity supplied/Percentage change in price

❑ Methods for measuring price elasticity of supply :

1. Percentage Method 2. Geometric Method

❑ Degrees of Elasticity of Supply :

(a) If the tangent to the supply curve passes through the point of origin, Es at that point is equal to unity.

(b) If the tangent intersects the x-axis, Es at that point is less than unity

(c) if tangent intersects the y-axis Es at that point will be greater than unity.

Very Short Answer Type Questions

Question. Define production function.

Answer: Diminishing return to a facter

Question. Define marginal product.

Answer: Marginal product is net addition to total product when one additional unit of variable factor is used.

Question. What will be the behavior of total product when marginal product of variable input is falling but is positive?

Answer: Total product increases at diminishing rate.

Question. What is the relation between average and marginal product when average product is falling?

Answer: MP falls but it falls at faster rate than AP

Question. Define average production.

Answer: AP is a per unit output of a variable factor.

Question. What do you mean by fixed factors of production? Give example.

Answer: These factors of production which cannot be varied in short period e.g. machine, land.

Question. By which behaviour of marginal product will total product be maximum.

Answer: When marginal product of a factor is zero, then total product will be maximum.

Question. How does fall in total product affects marginal product?

Answer: When total product falls, marginal product becomes negative.

Question. What do you mean by cost?

Answer: Cost is the sum of explicit and implicit cost.

Question. Define explicit costs.

Answer: Those monetary payments by producer on factor and non factor payments is called explicit cost. Which are not owned by himself.

Question. Which cost curve is parallel to ox-axis? Why?

Answer: Total fixed cost because TFC remain constant at all level of output.

Question. What do you mean by implicit costs?

Answer: Implicit cost is the cost of self owned resources of producer.

Question. Define marginal cost.

Answer: Marginal cost is the net addition to total cost when one additional unit of output is produced.

Question. Why does the difference between average total cost and average variable cost falls with increase in output?

Answer: It is because average fixed cost goes on falling with increase in output.

Question. Define Revenue.

Answer: Revenue is the amount received from sale of output.

Question. At what rate average and marginal revenue falls, with fall in per unit price of a good?

Answer: Marginal revenue falls twice the rate of average revenue.

Question. What will be the behaviour of Average revenue when total revenue increases at constant rate?

Answer: Average revenue remains constant.

Question. What do you mean by marginal revenue?

Answer: Marginal revenue is net additions to total revenue by sale of one additional unit of output.

Question. What will be the behaviour of total revenue when marginal revenue is zero?

Answer: Total revenue will be maximum.

Question. Why does average cost curve and averages variable cost curve never intersect each other?

Answer: Because AFC can never be zero at any level of output.

Question. What do you mean by producer’s equilibrium?

Answer: Producer’s equilibrium is a situation where he gets maximum profit.

Question. State any two conditions of producers equilibrium according to marginal revenue and marginal cost approach.

Answer: 1. MR = MC

2. Rising portion of Marginal cost curve intersects marginal revenue curve.

Question. Define Market Supply

Answer: Supply refers to the amount of the commodity that a firm or seller is willing to offer for sale in a given period of time at various prices.

Question. Name two determinants of supply.

Answer: Individual supply schedule is a tabular representation showing various quantities of a commodity which a firm is ready to sell at different prices during a given period of time.

Question. What is meant by change in supply?

Answer: It referes the sum of tatal quantity supplied by all the firms in a market.

Question. What type of change in price is the cause of upward movement along a supply curve?

Answer: 1. Number of firms

2. Change in technology

Question. What effect does an increase is tax rates have on supply of a commodity?

Answer: Change in supply refers to increase or decrease in supply of a commodity due to change in factors other than price like technology, price of inputs, Goal of producer, Number of firms etc.

Question. What causes a downward movement along a supply curve?

Answer: Due to increase in price.

Question. What is meant by leftward shift of supply curve?

Answer: As a result of increase in tax rates production cost increase, so the profit margin of producer will fall and producer will decrease the supply.

Question. How does a decrease in price of input effect supply curve of the commodity?

Answer: Decrease in price.

Question. Why does a supply curve have a positive slope?

Answer: Due to change in other factors the supply of a commodity falls at same price than supply curve shifted to leftward.

Question. What is meant by elasticity of supply?

Answer: As a result of decrease in price of input production cost falls then producers profit margin will increase so producer will increase the supply of commodity.

Question. What is the price elasticity of supply, if supply curve is parallel to y-axis.

Answer: Because of positive relation between price and supply.

Question. When does the elasticity of supply of commodity called equal to unity?

Answer: Price Elasticity of Supply (Es) is a measure of degree of response of supply for a good to change in its price.

Question. When does the producer increase the supply of a good at given price, give two reasons.

Answer: Perfectly elastic.

Question. What causes an extension in supply?

Answer: When percentage change in price is equal to percentage change in supply.

Question. If the price of a commodity falls by 10% and, consequently, the quantity supplied decreases by 20%. What will be its price elasticity of supply?

Answer: Due to change in other factor like improvement in technology, decrease in price of inputs.

H.O.T.S.

Question. Why is total variable cost curve parallel to total cost curve?

Answer: Increase in price of a commodity.

Question. Why does average fixed cost fall with increase in output?

Answer: Es = % change in quantity/% change in price = 20%/10% = 2

Question. Why is total fixed cost curve parallel to ox-axis.

Answer: Total cost is the sum of total fixed cost and total variable cost.

Question. Under which situation will MR fall when an additional quantity of a good is sold?

Answer: TFC remains constant at all levels of output.

Question. What behaviour of per unit price will cause the equality of average and marginal revenue.

Answer:When per unit price falls by selling an additional unit of a good.

Question. Give one differences between law of supply and price elasticity of supply.

Answer: Per unit price remains constant.

Question. What is the price elasticity of supply associated when the supply curve passing through to intersect to x-axis?

Answer: Law of supply reflects the direction of change in supply where as price elasticity of supply measures the magnitude of change in supply.

Question. Why does a producer moves downward along a supply curve due to decrease in price of commodity?

Answer: Inelastic.

Question. What is the price elasticity of supply associated with when a supply curve passes through the origin at 40° angle?

Answer: Because profit margin of firm (producer) decreases.

Question. When does the supply curve shift rightward while price remains constant.

Answer: Equal to unity elastic.

Question. What effect does an increase in price of competitive good have on the supply of a commodity?

Answer: When the supply of commodity increases due to change in other factors.

Question. How does the imposition of a tax affect the supply curve of a firm?

Answer: Supply of the commodity will fall.

Key Points for Class 12 Economics Chapter 04 The Theory of the Firm under Perfect Competition

Meaning of Supply: - Supply refers to quantity of a commodity that a firm is willing and able to offer for sale, at each possible price during a given period of time.

Market Supply: - It refers to quantity of a commodity that all the firms are willing and able to offer for sale at each possible price during a given period of time.

Factors affecting the Supply:

1. Price of Commodity: Higher the price of a commodity, larger is the quantity supplied and vice-versa.

2. Technological Changes: Improved techniques reduce the cost of production and increase the supply and vice versa.

3. Input Prices: A fall in prices of factors of production will increase the supply of the commodity and vice-versa.

4. Goal of the firm: If the goal is profit maximization, more quantity will be supplied at higher price. If the goal is sales maximization more will be supplied at same price. If its aim is to minimize risk, less will be supplied.

5. Price of Related Goods: If price of a substitute goods increase, supply of the commodity concerned will fall. If price of a complementary good increases, supply of the commodity concerned increases.

5. Expectation about future prices: If there is an expectation of increase in price of the commodity in future, supply will be less at present and vice-versa.

6. Government Policy: Imposition of taxes reduces supply and subsidy increases supply.

7. Number of firm: The larger the number of firms, greater in the market supply and vice-versa.

Change in quantity supply: - when supply changes due to change in price of commodity. It is called movement along supply curve.

a) Extension in supply: - When supply increases due to increase in supply.

b) Contraction in supply: - When supply

decreases due to decrease in supply, is called contraction in supply.

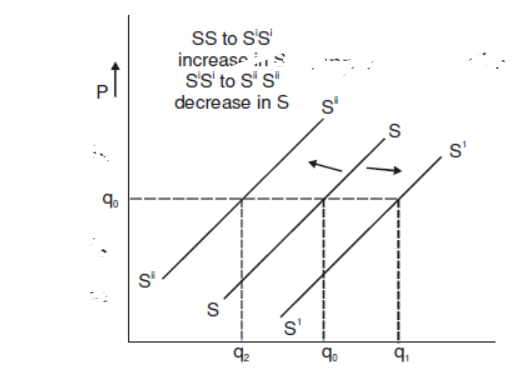

Change in supply/Shift of supply curve: -

It occurs due to change in other factors affecting supply like Technology, No. of Firms, etc.

a) Increase in supply: When more quantity is supplied at same price.

b) Decrease in supply: When less quantity is supplied on the same price is called Decrease in supply.

Price Elasticity of Supply: - It measures the degree of responsiveness of the quantity supplied of a commodity to a change in its price.

Measurement of Price Elasticity of Supply

1. Percentage Method

Cost concept

Cost:- The expenditure incurred on various inputs is known as the cost of production.

Types of Cost

1. Money Cost:- Total money expenses by a firm for producing a commodity.

2. Explicit Cost and Implicit Cost:- Actual payment made to outsiders is Explicit Cost.

Cost of self-supplied factors in implicit cost.

3. Real Cost:- All the pain, sacrifices, discomforts involved in producing factor services to produce commodity.

4. Opportunity Cost: - It is the cost of next best alternative foregone.

5. Short Run Cost:-

I. Fixed Cost: - Cost of fixed factors.

II. Variable Cost: - Cost of variable factors

Diagram

REVENUE CONCEPT

Revenue: - Money receipt by a firm by selling a commodity.

Types of Revenue

1. Total Revenue (TR) = Total Revenue is total money receipt of a firm on account of the total sale.

TR = Q X P

2. Marginal Revenue (MR) = Marginal Revenue is the change in total revenue as sale of one more unit of output.

MR = ΔTR/ΔQ MR=TRn-TRn-1

3. Average Revenue (AR) = Average Revenue is the per unit revenue received from sale of a commodity.

AR= TR/Q

Relationship between TR, MR in imperfect competition market.

1. When MR is O TR in maximum

2. When MR Negative TR falls.

HOTS

Question. Can MR be negative or zero.

Answer: Yes, MR can be zero or negative.

Question. If all units are sold at same price how will it affect AR and MR?

Answer: AR and MR will be equal at levels of output

Question. What is price line?

Answer: Price line is nothing but AR line and is horizontal to X-axis in perfect competition.

Question. Can TR be a horizontal Straight line?

Answer: Yes, when AR is zero.

Question. What happens to TR when a) MR is increasing, b) decreasing but remains positive and c) MR is negative?

Answer: a) TR increases at an increasing rate.

b) TR increases at a diminishing rate.

c) TR decreases.

Question. Why AR is more elastic in monopolistic competition than monopoly?

Answer: Monopolistic competition market has close substitutes. Monopoly market does not have close substitutes.

Question. Why TR is 45 0 angle in perfect competition market?

Answer: In perfect competition market the goods are sold at the same price so AR= MR and the TR increases at a constant rate.

Question. Can there be Break- even point with AR = AC

Answer: Yes there can be breakeven point with AR=AC

PRODUCERS EQUILIBRIUM

Meaning:- It is the situation where producer get maximum profit.

Determination of producer Equilibrium

2. Marginal Revenue and Marginal Cost Approach

Conditions:-

1. MR=MC

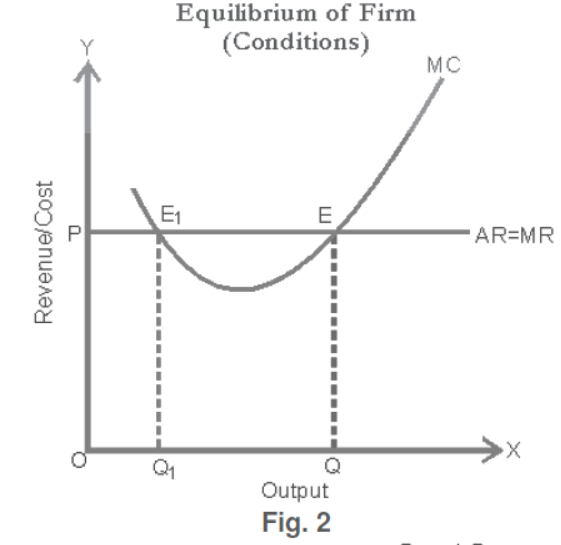

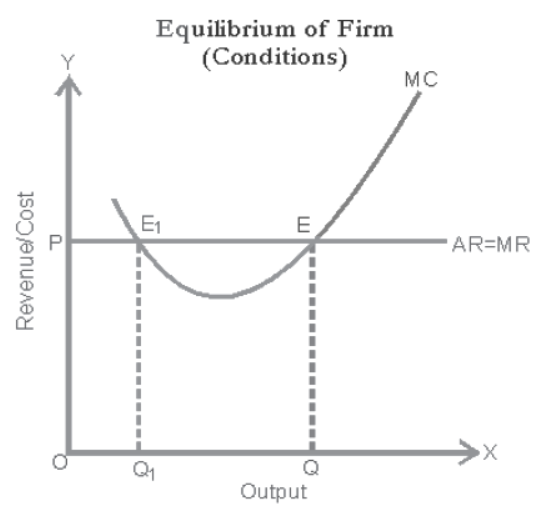

2. At Equilibrium Point MC curve intersect to MR curve from below Under perfect competition, a firm is in equilibrium in short-run when following two conditions are fulfilled.

(i) MR = MC

(ii) MC cuts MR from below or MC is rising at the point of equilibrium. Fig.

2 illustrates this situation.

In diagram, MR = MC at two levels of output: . However, is not

equilibrium level of output. Corresponding to point there is point which, no doubt, indicates that MR = MC.

However, MC is not rising here, rather it is falling. Therefore, second condition is not fulfilled here. Clearly E is the point where not only MR = MC, but MC is also rising. So Q is the equilibrium level of output.

In short-run, when a producer or firm is in equilibrium three situations are possible:

(i) SNP, (ii) NP, (iii) Minimum Loss.

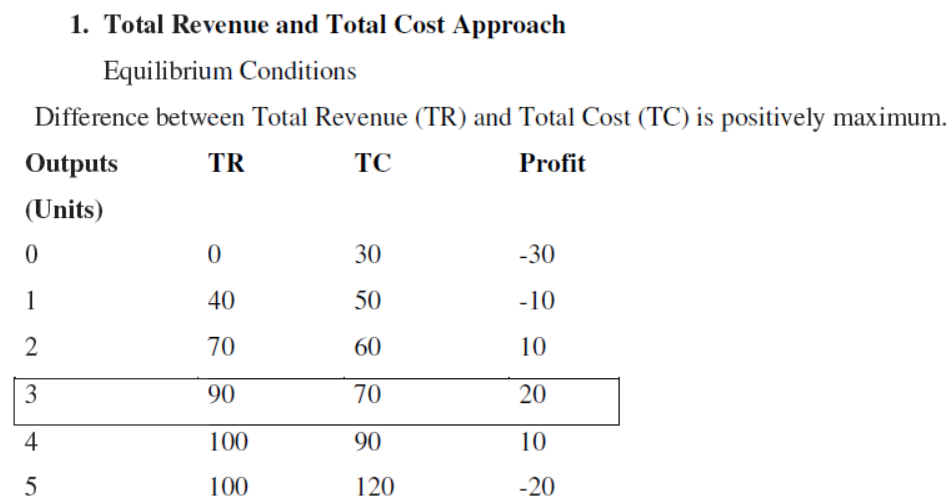

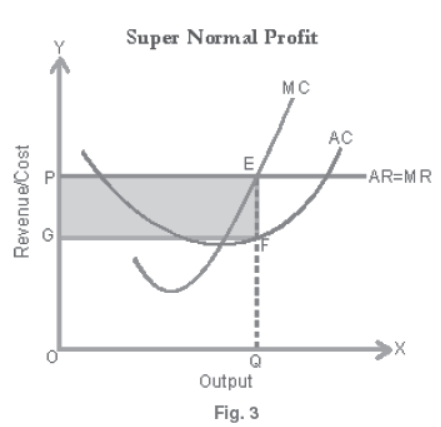

(i) Super Normal Profit (SNP): Super normal profits occur to the firm when its AR > AC and both the conditions of equilibrium are also met. Therefore, in this case AR > AC, MR = MC and MC cuts MR from below.

In Fig. 3 E is the point of equilibrium and corresponding to this Q is equilibrium level of output.

Here, AR is EQ, AC is FQ and clearly AR > AC.

π per unit = AR – AC

= EQ – FQ = EF. Firm is producing GF output.

Total Super Normal Profit of the firm is GF × EF = EFGP

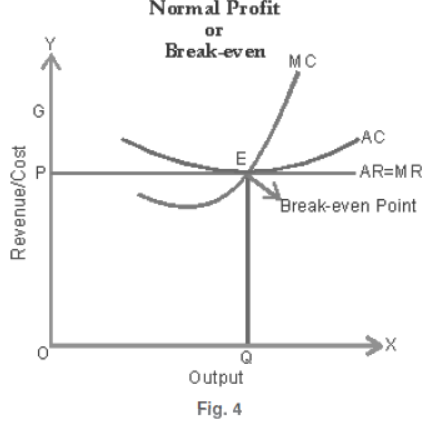

(ii) Normal Profit: Normal profits occur when AR = AC and both the conditions of equilibrium are also met.

In Fig. 4, E is the point of equilibrium, with normal profit.

Here, AR = EQ, AC = EQ

π per unit = AR – AC

= 0 as AR = AC

Firm is in equilibrium when it produces OQ level of output and it is earning just normal profit.

Point E is also known as Break-even point as AR = AC or TR = TC. The firm is just recovering its costs.

Important

Normal profit is a part of total cost of the firm. It is equal to reward to the producer for his entrepreneural services.

This is included in the estimation of TC. Thus, when AR = AC and π = 0 it generally refers to the absence of super normal profit.

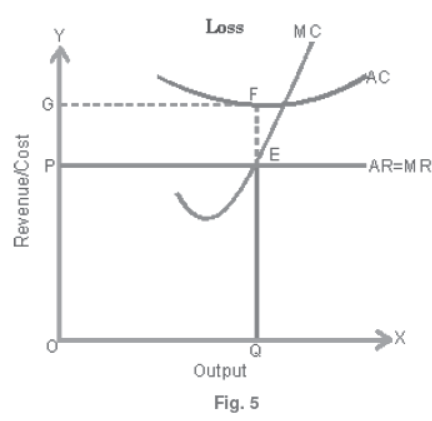

(iii) Minimum Loss: A firm incurs loss when its AR < AC (or TR < TC) and still, the firm is in equilibrium.

In Fig. 5, firm is in equilibrium at point E where not only MR = MC, but MC is also rising. OQ is equilibrium output.

However, firm is incurring loss as:

AR = EQ

AC = FQ

Clearly, AR < AC, per unit Loss

= AR – AC

= EQ – FQ

= – EF

Total Loss = Loss per unit of output × Total output

= – EF × PE

= – EFGP

Producer is in Equilibrium at Point E where both equilibrium conditions are satisfied.

Market

Market: - Market refers to an arrangement that contact between the buyers and seller for the sale and purchase of goods.

Types:

1. Perfect Competition Market:- Perfect Competition is a form of Market where there are large number of buyers and sellers of a commodity and selling homogeneous product.

Features:

1. Large Number of buyers and sellers

2. Homogenous product

3. Free entry free exit from Market

4. Perfect knowledge

5. Perfect Mobility

6. Zero transport cost

2. Monopoly Market: - There is single seller of a commodity which has no close substitutes.

Features:

1. Single seller

2. Restricted entry

3. No close substitutes

4. Full control

5. Price Discrimination

3. Monopolistic Competition:- This market situated where there are many seller of the product, and selling differentiate product from each other.

Features:

1. Large Numbers of buyers and seller

2. Product Differentiationsubstitutes.

3. Freedom of entry and exit of firms

4. Selling cost is applicable

Oligopoly: - This is the situation of market there are few seller selling homogeneous or differentiated products. Every seller influences by the behavior of other firms.

Features:-

1. Few firms

2. interdependence

3. no price competition

4. Group behavior

5. undetermined demand curve

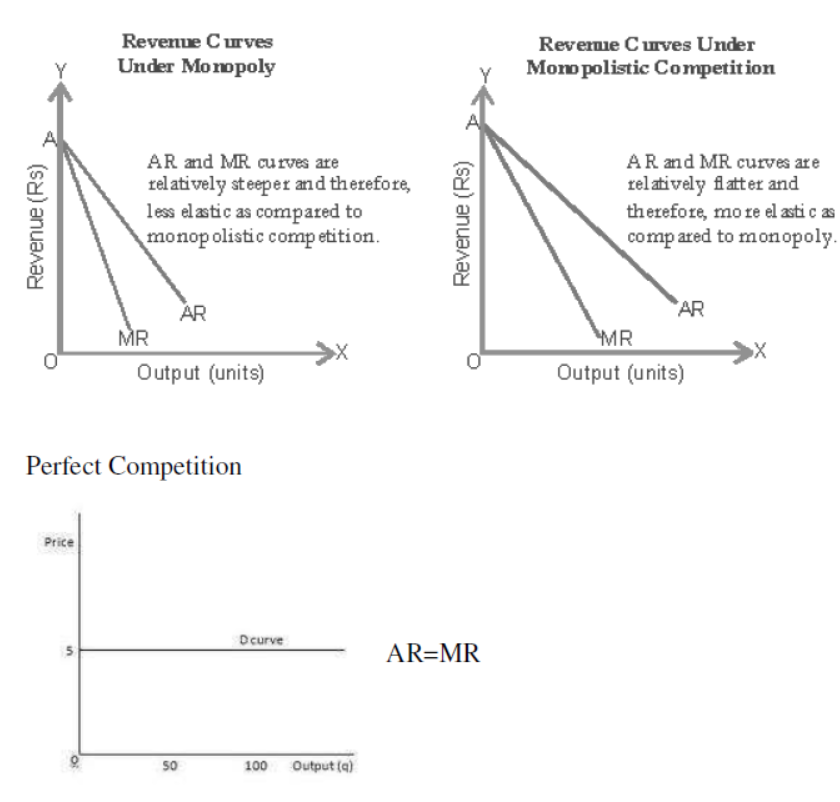

Shapes of Curves AR, MR in different markets.

Very short answer questions

Question. Define perfect competition

Answer: Perfect competition is a market with large number of buyers and sellers , selling homogeneous product at same price.

Question. Define monopoly.

Answer: Monopoly is a market situation dominated by a single seller who has full control over the price.

Question. Define monopolistic competition.

Answer: It refers to a market situation in which many buyers and sellers selling differentiated product and have partial control over the price.

Question. Under which market form firm is a price maker?

Answer: Perfect competition

Question. What are selling cost?

Answer: Cost incurred by a firm for the promotion of sale is known as selling cost.

Question. What is oligopoly?

Answer: Oligopoly is defined as a market structure in which there are few sellers of the commodity.

Question. In which market form is there product differentiation?

Answer: Monopolistic competition market

Question. What is product differentiation?

Answer: It means close substitutes offered by different producers to show their output differ from other output available in the market. Differentiation can be in color, size packing, brand name etc to attract buyers.

Question. What do you mean by patent rights?

Answer: Patent rights is an exclusive right or license granted to a company to produce a particular output under a specific technology.

Question. What is price discrimination?

Answer: It refers to charging of different prices from different consumers for different units of the same product.

Question. What do you mean by abnormal profits?

Answer: It is a situation for the firm when TR > TC.

Question. Why AR is equal to MR under perfect competition?

Answer: AR is equal to MR under perfect competition because price is constant.

Question. What are advertisement costs?

Answer: Advertisement cost are the expenditure incurred by a firm for the promotion of its sales such as publicity through TV , Radio , Newspaper , Magazine etc.

Question. What is meant by normal profit?

Answer: Normal profit is the minimum amount of profit which is required to keep an entrepreneur in production in the long run.

Question. What is break-even price?

Answer: In a perfectly competitive market, break- even price is the price at which a firm earn normal profit (Price=AC). In the long run, Break- even price is that price where

P=AR=MC

Short Answer Questions:

Question. Explain any four characteristics of perfect competition market.

Answer: i) Large number of buyers and sellers : The number of buyers and sellers are so large in this market that no firm can influence the price.

ii) Homogeneous products: Products are uniform in nature. The products are perfect substitute of each other. No seller can charge a higher price for the product. Otherwise he will lose his customers.

iii) Perfect knowledge: Buyers as well as sellers have complete knowledge about the product.

iv) Free entry and exit of firm: Under perfect competition any firm can enter or exit in the market at any time. This ensures that the firms are neither earning abnormal profits nor incurring abnormal losses.

Question. Explain briefly why a firm under perfect competition is a price taker not a price maker?

Answer: A firm under perfect competition is a price taker not a price maker because the price is determined by the market forces of demand of supply. This price is known as equilibrium price. All the firms in the industry have to sell their outputs at this equilibrium price. The reason is that, number of firms under perfect competition is so large. So no firm can influence the price by its supply. All firms produce homogeneous product.

Question. Distinguish between monopoly and perfect competition.

Answer:

| Perfect Competition | Monopoly |

| Very large number of buyers and sellers. | Single seller of the product. |

| Products are homogenous | Product has no close substitute |

| Firm is the price taker and not a maker | Firm is price maker not price taker |

| Price is uniform in the market ie price =AC | Due to price discrimination price is not uniform. |

| Free entry and exit of firms. | Very difficult entry of new firms. |

Question. Which features of monopolistic competition are monopolistic in nature?

Answer: i) Product differentiation

ii) Control over price

i) Downward sloping demand curve

Question. What are the reasons which give emergence to the monopoly market?

Answer: i) Patent Rights: Patent rights are the authority given by the government to a particular firm to produce a particular product for a specific time period.

ii) Formation of Cartel: Cartel refers to a collective decision taken by a group of firms to avoid outside competition and securing monopoly right.

iii) Government licensing: Government provides the license to a particular firm to produce a particular commodity exclusively.

HOTS

Question. Is abnormal profit possible in long-run for a monopoly firm?

Answer: Yes, because even in the long-run monopolist continues to have full control over price of the product and there is no possibility for the new firms to enter the market.

Question. What is the difference between pure competition and perfect competition?

Answer: When there are large number of buyers and sellers and each seller sells homogeneous product at the same price and when there are no barriers to enter the industry and firms have freedom to enter and exit the industry, pure competition is said to exist. However, when in addition to all these, there is not only perfect knowledge of price and perfect mobility but also absence of transport costs, perfect competition is said to exist.

Question. Why a firm under perfect competition will not lower the price to increase its sales?

Answer: A perfect competitive firm will not lower the price because of the following reasons:

(i) A firm under perfect competition can sell whatever amount it wishes to sell at the existing price. So that there is no rationality of lowering the price.

(ii) An individual firm under perfect competition is such a small supplier in the market that by lowering the price, it cannot ever cater to the entire market demand for the commodity.

Accordingly, reduction in price cannot be sustained by an individual firm.

Question. What is monopolistic competition? Can a seller in such a market influence the price? Explain.

Answer: Monoplistic competition is found in the industry where there is a large number of sellers selling differentiated product to a large number of buyers. There is freedom of entry and exit for the firms. In such a market, a seller has a partial control over price through product differentiation. However, full control over price is not possible owing to the fact that there is a large number of close substitutes in the market.

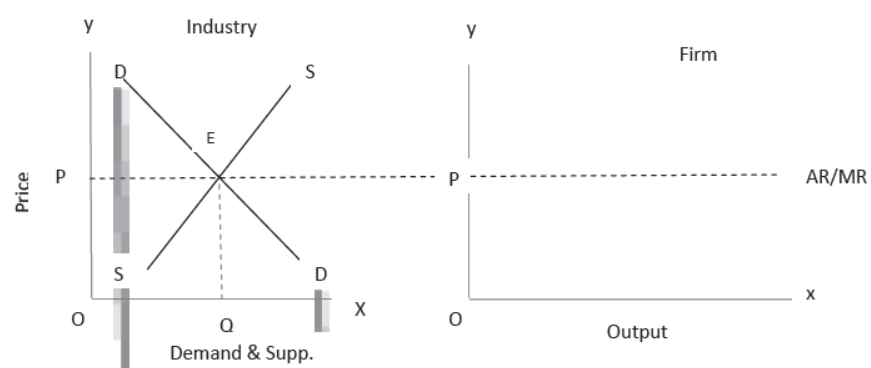

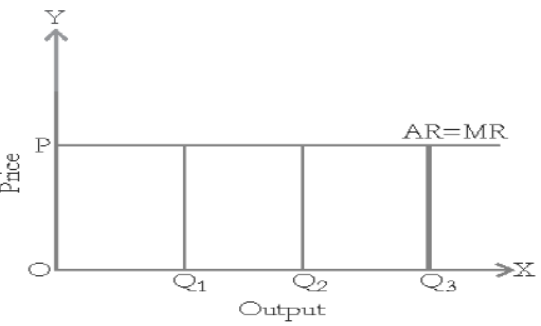

Question. Is a firm under perfect competition a price maker or a price taker? Illustrate your answer using a diagram.

Answer: A firm under perfect competition is a price taker and not a price maker. The price is determined by the industry so that the firm has to sell its product at the given price. It is owing to the following facts:

(i) The number of the firms under perfect competition is so large or that each firm under perfect competition sells such a small fragment of the total output that (by varying its sales) it cannot impact price of the product in the market.

(ii) All the firms in a perfectly competitive industry produce homogeneous product. Absence of product differentiation means the absence of even partial control over price.

(iii) Firm under perfect competition cannot take advantage of ignorance of the buyers, as buyers are assumed to have perfect knowledge of the market conditions. Price variation (or price control) is ruled out.

Diagrammatic Illustration

The following diagram, illustrates how a firm under perfect competition is a price taker not a price maker.

The figure shows that firm’s demand curve (AR curve) is a horizontal straight line.

It can sell any amount of output (Q1 , Q2 or Q3) at the prevailing price (OP). Price in the market is determined by the forces of market supply and market demand. It will change only when market demand or market supply changes. But, as we are aware, an individual firm under perfect competition cannot impact market supply. This is because an individual firm commands a very small segment of the market supply. It is so small that even a manifold increase/decrease in it would not make any difference to the total supply of the product in the market. This is implied in the very definition of perfect competition. This renders a firm under perfect competition as a ‘price taker’.

Note: If price control were possible, firm’s AR curve would no longer be a horizontal straight line. But perfect competition assumes the existence of only a horizontal straight line AR curve for a firm. Implying that a firm under perfect competition is always a price taker.

Free study material for Economics

CBSE Class 12 Economics Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition Assignment

Access the latest Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition assignments designed as per the current CBSE syllabus for Class 12. We have included all question types, including MCQs, short answer questions, and long-form problems relating to Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition. You can easily download these assignments in PDF format for free. Our expert teachers have carefully looked at previous year exam patterns and have made sure that these questions help you prepare properly for your upcoming school tests.

Benefits of solving Assignments for Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition

Practicing these Class 12 Economics assignments has many advantages for you:

- Better Exam Scores: Regular practice will help you to understand Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition properly and you will be able to answer exam questions correctly.

- Latest Exam Pattern: All questions are aligned as per the latest CBSE sample papers and marking schemes.

- Huge Variety of Questions: These Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition sets include Case Studies, objective questions, and various descriptive problems with answers.

- Time Management: Solving these Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition test papers daily will improve your speed and accuracy.

How to solve Economics Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition Assignments effectively?

- Read the Chapter First: Start with the NCERT book for Class 12 Economics before attempting the assignment.

- Self-Assessment: Try solving the Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition questions by yourself and then check the solutions provided by us.

- Use Supporting Material: Refer to our Revision Notes and Class 12 worksheets if you get stuck on any topic.

- Track Mistakes: Maintain a notebook for tricky concepts and revise them using our online MCQ tests.

Best Practices for Class 12 Economics Preparation

For the best results, solve one assignment for Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition on daily basis. Using a timer while practicing will further improve your problem-solving skills and prepare you for the actual CBSE exam.

FAQs

You can download free PDF assignments for Class 12 Economics Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition from StudiesToday.com. These practice sheets have been updated for the 2026-27 session covering all concepts from latest NCERT textbook.

Yes, our teachers have given solutions for all questions in the Class 12 Economics Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition assignments. This will help you to understand step-by-step methodology to get full marks in school tests and exams.

Yes. These assignments are designed as per the latest CBSE syllabus for 2026. We have included huge variety of question formats such as MCQs, Case-study based questions and important diagram-based problems found in Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition.

Practicing topicw wise assignments will help Class 12 students understand every sub-topic of Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition. Daily practice will improve speed, accuracy and answering competency-based questions.

Yes, all printable assignments for Class 12 Economics Part A Microeconomics Chapter 4 The Theory Of The Firm Under Perfect Competition are available for free download in mobile-friendly PDF format.