Read and download the CBSE Class 12 Economics Forms Of Market VBQs Set 01. Designed for the 2026-27 academic year, these Value Based Questions (VBQs) are important for Class 12 Economics students to understand moral reasoning and life skills. Our expert teachers have created these chapter-wise resources to align with the latest CBSE, NCERT, and KVS examination patterns.

VBQ for Class 12 Economics Forms Of Market

For Class 12 students, Value Based Questions for Forms Of Market help to apply textbook concepts to real-world application. These competency-based questions with detailed answers help in scoring high marks in Class 12 while building a strong ethical foundation.

Forms Of Market Class 12 Economics VBQ Questions with Answers

FORMS OF MARKET AND PRICE DETERMINATION

Question. Under Perfect Competition price of the Product

(a) can be controlled by individual Firm

(b) cannot be controlled by individual Firm

(c) can be controlled within certain limit by individual Firm

(d) none of the above

Answer: B

Question. Under Perfect Competition, the condition for Industry Equilibrium, i.e. SMC = SAC = LAC = LMC = LMR = LAR = Price, is applicable for —

(a) short—run

(b) long—run

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: B

Question. In a perfectly competitive markets, if MR is greater than MC then a firm should—

(a) Increase its production

(b) Decrease its production

(c) Increase in sales

(d) Decrease in sales

Answer: A

Question. Under Perfect Competition, in the short—run, the condition AR = MR = MC = AC, means that the Firm is earning —

(a) Normal Profits only

(b) Super Normal Profits

(c) Losses

(d) All of the above.

Answer: A

Question. Under Perfect Competition, a Firm can earn in the long—run.

(a) Normal Profits only

(b) Super Normal Profits

(c) Losses

(d) All of the above.

Answer: A

Question. Under Perfect Competition, all output can be sold —

(a) at different prices

(b) at the same price only

(c) at zero price

(d) only when Buyers are willing to buy.

Answer: B

Question. Price under perfect competition is determined by —

(a) Firm

(b) Industry

(c) Government

(d) Society

Answer: B

Question. Under Perfect Competition, the condition for equilibrium is AR = MR = MC = AC. This is for

(a) short—run

(b) long—run

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: B

Question. In Perfect Competition, a Firm can maximize its profit in short—run only when —

(a) Average Revenue is more than Marginal Revenue

(b) Marginal Revenue is equal to Total Cost

(c) Average Revenue is equal to Marginal Cost

(d) Marginal Cost is equal to Marginal Revenue

Answer: D

Question. Under Perfect Competition, each Firm is a

(a) Price Maker

(b) Price Taker

(c) Price Maker for its own product.

(d) All of the above.

Answer: B

Question. Under Perfect Competition, in the long—run, a Firm

(a) will always be a Optimal Firm.

(b) will never be an Optimal Firm.

(c) may or may not be an Optimal Firm.

(d) will leave the industry.

Answer: A

Question. Under Perfect Competition, the Firm's Demand Curve is

(a) Horizontal Line, parallel to X Axis

(b) Vertical Line, parallel to Y Axis

(c) Negatively Sloped

(d) Kinked.

Answer: A

Question. In India which of the following best describes a perfectly competitive market?

(a) Sugarcane Cultivation

(b) Indian Railways

(c) Toilet Soap Industry

(d) Electricity Distribution

Answer: A

Question. Which industry best fits the description of a Perfectly Competitive market?

(a) Automobile

(b) PC

(c) Soft—drinks

(d) Agriculture

Answer: D

Question. Under Perfect Competition, in the long—run, a Firm

(a) will not have excess capacity.

(b) may have excess capacity

(c) has no capacity at all

(d) will leave the industry.

Answer: A

Question. In Perfect Competition, a Firm maximizing its profits will set its output at that level where —

(a) Average Variable Cost = Price

(b) Marginal Cost = Price

(c) Fixed Cost = Price

(d) Average Fixed Cost = Price

Answer: B

Question. Which of these is not a feature of Perfect Competition?

(a) Large Number of Buyers & Sellers

(b) Homogeneous Products

(c) Free Entry / Exit

(d) Preference of Consumers towards one Supplier

Answer: D

Question. The assumptions of large number of Sellers and product homogeneity in Perfect Competition, implies that all individual Firms in Perfect Competition are —

(a) Price Takers

(b) Price Movers

(c) Price Givers

(d) Price Offerers

Answer: A

Question. Which of the following is not an essential condition of Pure Competition?

(a) Large number of Buyers and Sellers

(b) Homogeneous Product

(c) Freedom of entry

(d) Absence of Transport Cost

Answer: D

Question. One of the essential conditions Perfect Competition is —

(a) Product Differentiation

(b) Multiplicity of prices for identical product at any one time

(c) Many Sellers and few Buyers

(d) Only one price for identical goods at any one time

Answer: D

Question. Which of the following is true about Perfect Competition?

(a) Firms can enter freely in the market but it is difficult to exit from the market

(b) Firms face difficulty in entering the market, but Firms can freely exit from the market

(c) Entry and exit in the market is highly restricted

(d) Firms are free to enter and exit the market

Answer: D

Question. Under Perfect Competition, in the long—run, the LAC Curve will be to the AR Curve.

(a) tangent

(b) perpendicular

(c) parallel

(d) coinciding

Answer: A

Question. Price Taker Firms —

(a) Advertise to increase the demand for their products.

(b) Do not advertise because most advertising is harmful for the society.

(c) Do not advertise because they can sell as much as they want at the current price.

(d) Who advertise will get more profits than those who do not.

Answer: C

Question. In Perfect Competition, in the long run, if a new Firm enters the industry, the Supply Curve shifts to the right resulting in —

(a) Fall in Price

(b) Rise in Price

(c) Reduction in Supply

(d) No change in Price

Answer: A

Question. In a perfectly competitive market, in the long run, competitive prices equal the minimum possible cost.

(a) Marginal

(b) Variable

(c) Total

(d) Average

Answer: D

Question. Under Perfect Competition, Total Revenue is equal to Marginal Revenue times the quantity sold. This statement is —

(a) True

(b) False

(c) Partially True

(d) None of the above

Answer: A

Question. Which of the following is not a characteristic feature of Perfect Competition?

(a) All the sellers sell at the same price

(b) All the products are homogenous

(c) Customers have no bargaining power

(d) Customers have no purchasing power

Answer: D

Question. Which of the following statements regarding Perfect Competition is false?

(a) The Marginal Revenue Curve is a straight line

(b) In the short run, Fixed Costs remain constant and cannot be changed

(c) The Firm becomes a Price—Taker and tries to achieve equilibrium

(d) Marginal Revenue is more than the price

Answer: D

Question. Under Perfect Competition, there are Sellers.

(a) Many

(b) Only one

(c) A Few

(d) No

Answer: A

Question. What is the shape of the Demand Curve faced by a Firm under Perfect Competition?

(a) Horizontal

(b) Vertical

(c) Positively sloped

(d) Negatively sloped

Answer: A

Question. In India, the Milk Market resembles a perfectly competitive industry. If the industry is an increasing cost industry, the long run supply curve of the industry

(a) Slopes upward to the right

(b) Slopes downward to the right

(c) Would be a vertical straight line

(d) Would be horizontal straight line

Answer: A

Question. Which of the following curves resembles the Demand Curve in a Perfect Competition?

(a) Average Cost Curve

(b) Marginal Utility Curve

(c) Average Utility Curve

(d) Average Variable Cost Curve

Answer: B

Question. Under Perfect Competition, in the long—run, Output is produced at —

(a) minimum feasible cost

(b) maximum cost

(c) optimal cost

(d) zero cost

Answer: A

Question. In Perfect Competition, a Firm's Profit diminishes when ________exceeds

(a) Marginal Revenue, Marginal Cost

(b) Marginal Cost, Marginal Revenue

(c) Marginal Revenue, Average Cost

(d) Average Revenue, Average Cost

Answer: B

Question. Which of the following is not true about perfect competition?

(a) Purchase and sale of homogeneous goods

(b) Mobility of factors of production

(c) Free entry and exit

(d) Presence of advertisement

Answer: D

Question. Under Pure Competition, there are Sellers.

(a) Many

(b) Only one

(c) A Few

(d) No

Answer: A

Question. Which of the following is not a characteristic of a "Price Taker"?

(a) TR = P xQ

(b) AR = Price

(c) Negatively — sloped Demand Curve

(d) Marginal Revenue = Price

Answer: C

Question. Under Perfect Competition, in the long—run, the ______ will be tangent to the AR Curve.

(a) LAC Curve

(b) LMC Curve

(c) Demand

(d) Supply

Answer: A

Question. Under Perfect Competition, each Firm's control over price is —

(a) Nil

(b) Full and Absolute

(c) Subject to Competing Firms' Strategies

(d) None of the above.

Answer: A

Question. Which of the following statements regarding Perfect Competition is false?

(a) Supply and Demand forces determine the price of a commodity

(b) All Buyers in the Market are always in position to influence the market

(c) In the short run, the Firm takes Market Price as given

(d) Considering the Market Price, Firm adjusts the level of output to maximize profits

Answer: B

Question. The Firm in a Perfectly Competitive Market is a Price Taker. This designation as a Price Taker is based on the assumption that —

(a) The Firm has some, but not complete, control over its product price

(b) There are so many buyers and sellers in the market that any individual Firm cannot affect the market

(c) Each Firm produces a homogeneous product

(d) There is easy entry into or exit from the market place

Answer: B

Question. A Perfectly Competitive Firm Producer has control over —

(a) Price

(b) Production as well as price

(c) Control over production, price and consumers

(d) None of the above

Answer: D

Question. The distinction between a single firm & an Industry vanishes in which of the following market condition

(a) Monopoly

(b) Perfect competition

(c) Monopolistic competition

(d) Imperfect competition

Answer: B

Question. A Purely Competitive Firm's Supply Schedule in the short run is determined by —

(a) Its Average Revenue

(b) Its Marginal Revenue

(c) Its Marginal Utility for money curve

(d) Its Marginal Cost curve

Answer: D

Question. Under Perfect Competition, Demand (D) = AR = MR = Price. This statement is —

(a) True

(b) False

(c) Partially True

(d) None of the above

Answer: A

Question. In which competition, firm has no control over price?

(a) Monopoly

(b) Perfect competition

(c) Monopolistic Competition

(d) Oligopoly

Answer: B

Question. Under Perfect Competition, Price Elasticity of Demand is

(a) Nil

(b) Less Elastic

(c) More Elastic

(d) Infinity

Answer: D

Question. Under Perfect Competition, the product is —

(a) Differentiated

(b) Homogeneous

(c) Influenced by Brand Name

(d) Always Intangible

Answer: B

Question. Which of the following statement is not true about Perfect Competition?

(a) The Demand Curve is also the Firm's Average Revenue Curve

(b) The Demand Curve is a horizontal line.

(c) Demand increases as price increases

(d) Supply increases as price decreases

Answer: C

Question. What are the conditions for long—run equilibrium of the Competitive Firm?

(a) LMC = LAC = P

(b) SMC = SAC = LMC

(c) P = MR

(d) All of these

Answer: D

Question. If a Competitive Firm doubles its output, its Total Revenue —

(a) doubles

(b) more than doubles

(c) less than doubles

(d) cannot be determined because the price of the good may rise or fall

Answer: A

Question. A Competitive Firm maximizes profit at the output level where —

(a) Price equals Marginal Cost.

(b) Slope of the Firm's profit function is equal to zero.

(c) Marginal Revenue equals Marginal Cost.

(d) All of the above.

Answer: D

Question. In the long—run, Industry Equilibrium is achieved if SMC = SAC = LAC = LMC = LMR = LAR = Price. This condition is applicable for —

(a) Perfect Competition

(b) Monopoly

(c) Monopolistic Competition

(d) Oligopoly.

Answer: A

Question. Which of the following market situations explains Marginal Cost equal to Price for attaining equilibrium?

(a) Perfect Competition.

(b) Monopoly

(c) Oligopoly.

(d) Monopolistic Competition.

Answer: A

Question. How are prices determined under Perfect Competition?

(a) At the equilibrium price of Firm

(b) At the equilibrium prices of Industry

(c) At the point where MR = MC

(d) All of these

Answer: B

Question. Which of the following is a feature of Perfect Competition?

(a) Firms are free to produce any number of units of different commodities

(b) Firms are free to enter and exit from the industry

(c) Firms are free to produce any type of a commodity

(d) None of the above

Answer: B

Question. In a Perfectly Competitive Market, if MC = Marginal Cost, MR = Marginal Revenue, AR = Average Cost and P = Price, the first order condition for profit maximization will be —

(a) MC< MR<AR< P

(b) MC= MR=AR=P

(c) MC> MR>AR> P

(d) MC=MR>AR=P

Answer: B

Question. Which of these is not a feature of Perfect Competition?

(a) Restriction in Entry of new Firms

(b) Perfect Knowledge

(c) Efficient Transportation Facilities

(d) Uniform Market Price

Answer: A

Question. Price—Taking Firms, i.e., Firms that operate in a perfectly competitive market, are said to be "small" relative to the market. Which of the following best describes this smallness?

(a) The individual Firm must have fewer than 10 employees

(b) The individual Firm faces a downward— sloping demand curve

(c) The individual Firm has assets of less than 20 la kh

(d) The individual Firm is unable to affect market price through its output decisions

Answer: D

Question. Under Perfect Competition, a Firm can earn in the short—run.

(a) Normal Profits only

(b) Super Normal Profits

(c) Losses

(d) All of the above.

Answer: B

Question. In a Perfect Competitive Market —

(a) Firm is the Price—Giver and Industry is the Price Taker

(b) Firm is the Price Taker and industry is the Price—Giver

(c) Both are Price Takers

(d) none of the above

Answer: B

Question. Which of these is not a feature of Perfect Competition?

(a) Free Entry / Exit

(b) Lack of Perfect Knowledge

(c) Inefficient Transportation Facilities

(d) Mobility of Factors of Production

Answer: C

Question. In the short run, if a Perfectly Competitive Firm finds itself operating at a loss, it will —

(a) reduce the size of its plant to lower fixed costs.

(b) raise the price of its product.

(c) shut down.

(d) continue to operate as long as it covers its variable cost.

Answer: D

Question. Under Perfect Competition, in the short—run, the condition for shut—down is —

(a) AR < AC

(b) AR > AC

(c) AR > AVC

(d) AR < AVC

Answer: D

Question. In a Perfectly Competitive Market, the Demand Curve is

(a) Relatively inelastic

(b) Unitary elastic

(c) Relatively elastic

(d) Infinitely elastic

Answer: D

Question. Which of the following is not a condition of Perfect Competition?

(a) Large Number of Firms

(b) Perfect Mobility of Factors

(c) Informative advertising to ensure that consumers have good information

(d) Freedom of entry and exit into and out of the market

Answer: C

Question. Which of the following is true with reference to shut down point in a Perfect Competition?

(a) The profits of the Firm equals its total costs

(b) At that output level the price covers the average fixed costs of the Firm

(c) At that output level the price covers the average variable costs of the Firm

(d) At that output level the price covers the average total costs of the Firm

Answer: C

Question. Which of the following is not a characteristic of a Perfectly Competitive Market?

(a) Large number of Firms in the industry

(b) Outputs of the Firms are perfect substitutes for one another

(c) Firms face downward—sloping Demand Curves

(d) Resources are very mobile

Answer: C

Question. If the price falls below the Minimum Average Variable Cost, a Firm operating under Perfect Competition should, in the short run,

(a) Produce an output where MR = MC

(b) Reduce its output so as to increase the price and profits

(c) Stop production (output) until price increases

(d) Continue to produce in the short run, but not in long run

Answer: C

Question. In Perfect Competition, a Firm increases profit when exceeds

(a) Total Cost, Total Revenue

(b) Marginal Cost, Marginal Revenue

(c) Total Revenue, Total Fixed Cost

(d) Average Revenue, Average Cost

Answer: D

Question. In Perfect Competition, when Marginal Cost Marginal Revenue, Profit is

(a) Maximum

(b) Average

(c) Zero

(d) Not Possible

Answer: A

Question. Which of the following statements is false in a Perfectly Competitive Market with constant returns to scale?

(a) The long run average cost curve will be horizontal at each Firm's minimum average cost

(b) The long run average cost curve will be horizontal at each Firm's zero—profit price

(c) The long run equilibrium in a competitive industry will be one with no economic profit

(d) With a constant increase in one input, keeping other inputs constant, the output could be increase

Answer: D

Question. Under Perfect Competition, in the long—run, the industry is said to be in equilibrium, if —

(a) All the Firms are earning normal profits only.

(b) There is no further entry or exit of Firms to / from the market.

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: C

Question. Under Perfect Competition, in the long—run, if SMC = SAC = LAC = LMC = LMR = LAR = Price, then the industry is said to be —

(a) Growing

(b) in troubled times

(c) in Equilibrium

(d) inefficient

Answer: C

Question. For the price—taking Firm —

(a) Marginal Revenue is less than Price

(b) Marginal Revenue is equal to Price

(c) Marginal Revenue is greater than Price

(d) The relationship between Marginal Revenue and Price is indeterminate

Answer: B

Question. Which of the following is not a characteristic of a Perfectly Competitive Market?

(a) Large number of Buyers and Sellers

(b) Homogeneous Product

(c) Free entry and exit of Firms

(d) Presence of high transportation costs

Answer: D

Question. In a perfect competition, who set the prices:

(a) Buyers

(b) Sellers

(c) Both buyers and sellers

(d) Government

Answer: C

Question. Which is the first order condition for the profit of a firm to be maximum*

(a) AC = MR

(b) MC = MR

(c) MR = AR

(d) AC = AR

Answer: B

Question. When the Perfectly Competitive Firm and industry are in long run equilibrium then —

(a) P=MR=SAC=LAC.

(b) D=MR=SMC=LMC.

(c) P=MR=Lowest point on the LAC curve.

(d) All of the above.

Answer: D

Question. Under Perfect Competition, in the short—run, if AR < AC at the point when MC = MR, it means that the Firm —

(a) Normal Profits only

(b) Super Normal Profits

(c) Losses

(d) All of the above.

Answer: C

Question. Under Perfect Competition, in the short—run, if AR > AC at the point when MC = MR, it means that the Firm —

(a) Normal Profits only

(b) Super Normal Profits

(c) Losses

(d) All of the above.

Answer: B

Question. In Perfect Competition, in the long run —

(a) There are large Profits for the Firm

(b) There are large Losses for the Firm

(c) There is no super—normal profit and no loss for the Firm

(d) There are negligible profits for the Firm

Answer: C

Question. Under Perfect Competition, in the long—run, LAC refers to —

(a) minimum feasible cost

(b) maximum cost

(c) optimal cost

(d) zero cost

Answer: A

Question. Under Perfect Competition, in the long—run, resources will be —

(a) fully used

(b) partially used

(c) not used at all

(d) wasted

Answer: A

Question. Excess Capacity is not found under —

(a) Monopoly

(b) Monopolistic Competition

(c) Perfect Competition.

(d) Oligopoly.

Answer: C

Question. Under the Perfect Competition a Firm will be in Equilibrium when —

(a) MC = MR

(b) MC cuts MR from below

(c) MC is rising when it cuts MR

(d) All of the above

Answer: D

Question. In Long run which of the following is true for a perfect competition

(a) Industry is operating at minimum point of AC curve

(b) MC is greater than MR

(c) AFC is less than AVC

(d) Price is less than AC

Answer: A

Question. Under Perfect Competition, Demand (D) =

(a) Average Revenue (AR)

(b) Marginal Revenue (MR)

(c) Price (P)

(d) All of the above

Answer: D

Question. Under Perfect Competition, the Firm's Demand Curve will be the same as —

(a) Marginal Revenue (MR) Curve

(b) Average Revenue (AR) Curve

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: C

Question. Under Perfect Competition, the Firm's MC Curve will be the same as —

(a) Supply Curve

(b) Demand Curve

(c) Production Possibility Curve

(d) Indifference Curve

Answer: A

Question. Under Perfect Competition, the Firm's Supply Curve will be the same as —

(a) Marginal Revenue (MR) Curve

(b) Average Revenue (AR) Curve

(c) Marginal Cost (MC) Curve

(d) Average Cost (AC) Curve

Answer: C

Question. Under Perfect Competition, the Firm's Supply Curve will be the same as Marginal Cost (MC) Curve for —

(a) the portion above AVC

(b) the portion below AVC

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: A

Question. Normally, in the short run, the supply curve of a perfectly competitive Firm slopes

(a) Downward from left to right

(b) Upward from right to left

(c) Upward from left to right

(d) Downward from right to left

Answer: C

Question. The short—run supply curve of the Perfectly Competitive Firm is given by —

(a) Rising Portion of its MC Curve over and above the Shut—Down Point

(b) Rising Portion of its MC Curve over and above the Break—Even Point

(c) Rising Portion of its MC Curve over and above the AC Curve

(d) Rising Portion of its MC Curve

Answer: A

Question. Under Perfect Competition, the burden of a specific tax would be borne by —

(a) Seller

(b) Buyer

(c) Seller and buyer equally

(d) Cannot say

Answer: D

Question. In the long run, the Pure Competition Firm can have

(a) Super Normal Profit

(b) Normal Profits

(c) Losses

(d) All of these

Answer: B

Question. Under Perfect Competition, the Firm's AR and MR Curve will be the same as —

(a) Supply Curve

(b) Demand Curve

(c) Production Possibility Curve

(d) Indifference Curve

Answer: B

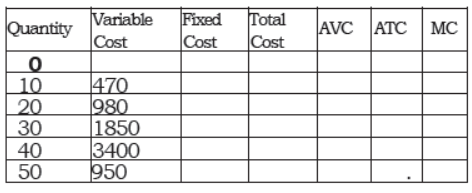

A Competitive Firm sells its product at Market Price of Z 51 per unit. The Fixed Cost is 300 and Variable Cost for different level of production are shown in the following table. Answer the following questions

Question. When production is 30 units, the Average Variable Cost is —

(a) 70.6

(b) 60.6

(c) 61.6

(d) 71.6

Answer: C

Question. To maximize profit, the Firm should produce —

(a) 30 units

(b) 10 units

(c) 20 units

(d) 40 units

Answer: C

Question. If the Market Price drops from Z 51 to Z 47, the Firm should —

(a) Close down

(b) Produce 10 units

(c) Produce 30 units

(d) Produce 20 units

Answer: B

Question. When Production is 50 units, Marginal Cost is —

(a) 265

(b) 255

(c) 245

(d) 275

Answer: B

Question. What is the relationship between AR curve and demand curve in a monopoly market?

Answer: Both AR curve and demand curve are the same in a monopoly market.

Question. What do you mean by price discrimination?

Answer: Price discrimination is a policy under which a seller sells a similar product at different prices to different buyers.

Question. Define oligopoly.

Answer: Oligopoly is a market structure where there are few firms competing for their homogenous or differentiated products.

Question. What will be the effect on equilibrium price when increase in demand is than increase in supply?

Answer: When increase in demand is more than increase in supply, equilibrium price will increase.

Question. Under what situation does the equilibrium price remains unaffected when there is simultaneous increase in demand and supply.

Answer:When increase demand is equal to increase in supply the equilibrium price will remain same.

Question. What is the relation between average revenue curve and demand curve under monopolistic competition?

Answer: Both AR and MR curves have negative slope

Question. ―Demand curve facing a monopoly firm is a constraint for the monopolist.‖ Comment

Answer: one seller, price maker

Question. Price discrimination should be socially desirable. How?

Answer: For the benefit of the poor

Question. How to reduce the incidence of selling cost under monopolistic competition because of which price tends to be higher than what it would have been if only the production cost would have been the sole basis.

Answer: reduce expenditure on advertisement, increase consumer awareness

Question. Why has power crisis increased in India?

Answer: demand is more, transmission and distribution losses and theft

Question. Explain the effect on the market equilibrium by imposing a ban on the sale of GUTKA in Delhi?

Answer: fall in supply, increase in supply of other related goods

Question. BPO offers attractive jobs to the educated urban youth in India. Though highly remunerative, these jobs involve long and inconvenient working hours. What is the impact of BPO on the supply of labour.

Answer: prevailing unemployment supply of labour is not affected by the long and inconvenient working hours( sweat shopping)

Question. A severe drought results in a drastic fall in the output of wheat. Analyze how it will affect the market price of wheat.

Answer: Market price will rise, price regulation may be required from the govt.

Question. Consumers often suffer because of their ignorance about the market situation and pay higher price than the equilibrium price. How this can be avoided.

Answer: consumer awareness about their rights and duties

Question. How are decisions taken by consumers and producers in a market coordinated?

Answer: Manifest in the form of demand and supply and the resultant price.

Free study material for Economics

VBQs for Forms Of Market Class 12 Economics

Students can now access the Value-Based Questions (VBQs) for Forms Of Market as per the latest CBSE syllabus. These questions have been designed to help Class 12 students understand the moral and practical lessons of the chapter. You should practicing these solved answers to improve improve your analytical skills and get more marks in your Economics school exams.

Expert-Approved Forms Of Market Value-Based Questions & Answers

Our teachers have followed the NCERT book for Class 12 Economics to create these important solved questions. After solving the exercises given above, you should also refer to our NCERT solutions for Class 12 Economics and read the answers prepared by our teachers.

Improve your Economics Scores

Daily practice of these Class 12 Economics value-based problems will make your concepts better and to help you further we have provided more study materials for Forms Of Market on studiestoday.com. By learning these ethical and value driven topics you will easily get better marks and also also understand the real-life application of Economics.

FAQs

The latest collection of Value Based Questions for Class 12 Economics Forms Of Market is available for free on StudiesToday.com. These questions are as per 2026 academic session to help students develop analytical and ethical reasoning skills.

Yes, all our Economics VBQs for Forms Of Market come with detailed model answers which help students to integrate factual knowledge with value-based insights to get high marks.

VBQs are important as they test student's ability to relate Economics concepts to real-life situations. For Forms Of Market these questions are as per the latest competency-based education goals.

In the current CBSE pattern for Class 12 Economics, Forms Of Market Value Based or Case-Based questions typically carry 3 to 5 marks.

Yes, you can download Class 12 Economics Forms Of Market VBQs in a mobile-friendly PDF format for free.