Read and download the CBSE Class 12 Accountancy Partnership Fundamentals VBQs Set 01. Designed for the 2026-27 academic year, these Value Based Questions (VBQs) are important for Class 12 Accountancy students to understand moral reasoning and life skills. Our expert teachers have created these chapter-wise resources to align with the latest CBSE, NCERT, and KVS examination patterns.

VBQ for Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts

For Class 12 students, Value Based Questions for Part 1 Chapter 1 Accounting for Partnership Basic Concepts help to apply textbook concepts to real-world application. These competency-based questions with detailed answers help in scoring high marks in Class 12 while building a strong ethical foundation.

Part 1 Chapter 1 Accounting for Partnership Basic Concepts Class 12 Accountancy VBQ Questions with Answers

1. A,B and C are partners sharing profits in the ratio 3:2:1 and contribute capital ₹1,00,000; ₹ 80,000 and 60,000 respectively. Profit before adjustments is 84,000. Interest on capital is to be provided @ 10% p.a. Since C has to take care of his physically challenged brother, his share of profit should not be less than ₹15,000. A and B have agreed to bear the deficiency.

Value Based

What values are reflected on the part of A and B that they are ready to sacrifice their share to meet the deficiency of guaranteed profit?

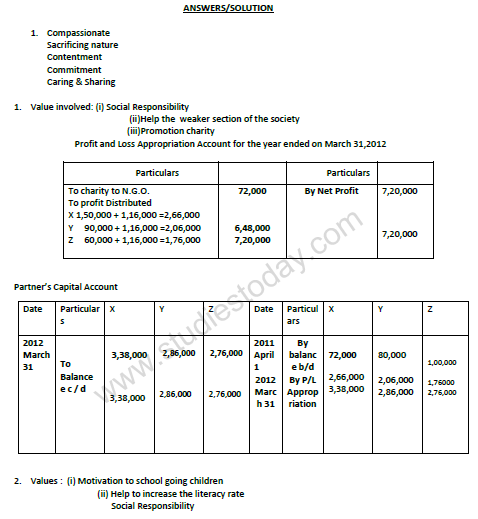

2. X,Y and Z are partners with ₹ 72,000, 80,000 and ₹ 1,00,000 as their capitals respectively. The profit for the year ending March 31,2012 was ₹7,20,000. Before distributing profits they donated 10% of profits to a ‘Non-Govt. organisation’ as charity for welfare of educationally backward section of the society. Out of the remaining profit, ₹4,00,000 is divisible as 5:3:2 ratio and the remaining is to be divided amongst them equally.

Identify the value followed by the partnership firm of X,Y and Z. Prepare Profit and Loss Appropriation Account and Partner’s Capital Account.

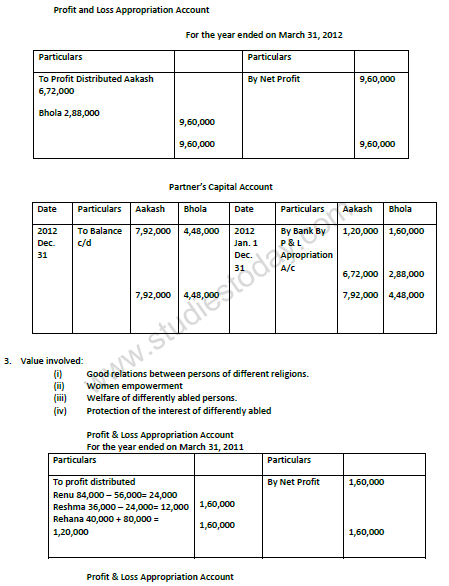

3. Aakash and Bhola entered into partnership on January ₹1,2012 contributing ₹1,20,000 and ₹1,60,000 as capitals respectively. Their partnership firm started the business of manufacturing shoes. They decided to donate 30% of the shoes produced for school going children. They share profits in the ratio of 7:3. The profits for the year were ₹96,000. Prepare Profit and Loss Appropriation Account and the Partner’s Capital Accounts. Also identify the value involved in this question.

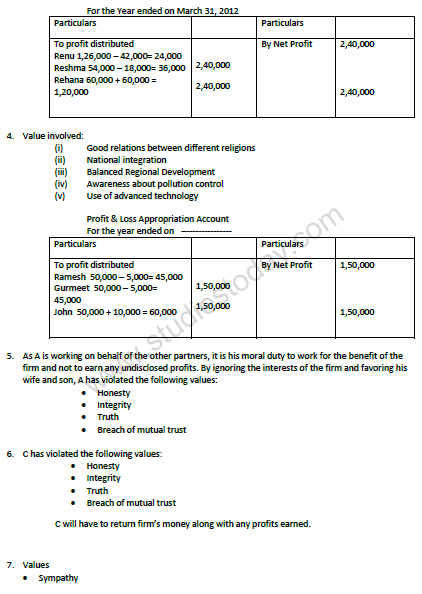

4. Renu and Reshma shared profits as 7:3. Renu want to give admission to her friend Rehana as a new partner. Reshma agrees with this decision of Renu. Rehana is a physically challenged lady and admitted with a ¼ th share in profits. Renu and Reshma gave her a guarantee that her share of profit will never be less than ₹1,20,000 p.a., the profits for the last two years ended March 31, 2011 and March 31, 2012 were ₹1,60,000 and ₹2,40,000 respectively. Identify the human value involved in this case and Profit and Loss Appropriation Account for the two years.

5. Ramesh and Gurmeet are two friends belonging to Hindu and Sikh religion respectively. They started a business of wire manufacturing in the form of a partnership firm. They know that the factory of wire manufacturing pollutes the environment. Therefore there are two options available before them. First option is that the factory can be opened in rural area where local residents are poor and illiterate. Second option is that an advanced pollution control plant can be installed in their factory to control the pollution. They decided to choose the second option which involves an additional cost of ₹2,00,000. To arrange this amount, they admitted their rich friend John as a new partner for equal share in the future profits. John brought ₹2,50,000 as his share of capital. Ramesh and Gurmeet gave him a guarantee that his share of profit will not be less than ₹60,000 p.a. At the end of first year the firm earns a profit of ₹1,50,000.

Mention the value involved in this question. Write the effects of choosing option available before Ramesh and Gurmeet. Prepare Profit and Loss Appropriation Account for the first year.

6. A,B and C are in a partnership. A is appointed for carrying on the business of the firm by the other partners. A has decided to purchase the goods from a firm in which his wife and his son are partners at a double rate than the prevailing market rate without disclosing this fact to others partners of the firm. State which values have been violated by A by not disclosing this information to B and C.

7. A,B and C are partners in a firm. C used firm’s money to buy shares without disclosing it other partners. Which value C is violating and what will be the treatment of profit earned by C?

SHORT ANSWER TYPE QUESTIONS

Question. W, X, and Y were partners sharing profits and losses in the ratio of 2:2: 1. X was guaranteed a profit of ₹ 10,00,000. The firm earned a profit of ₹ 17,50,000 for the year ended 31st March 2020.

Pass Journal entries for the year ended 31st march 2020.

Answer : Profit and loss A/C Dr 17,50,000

To profit and Loss Appropriation A/C 17,50,000

profit and Loss Appropriation A/C 17,50,000

To W’s capital A/C 5,00,000

To X’s capital A/C 10,00,000

To Y’s capital A/C 2,50,000

Question. X and Y are partners in the firm sharing profits and losses in the ratio of 3:2 with capitals of ₹ 10,00,000 and ₹ 5,00,000 respectively. As per the partnership deed, they are to be allowed interest on capital @ 8% p.a. The net profit for the year ended 31st March 2021 before providing for interest on capital amounted to ₹ 45,000. Show the distribution of profit.

Answer : Interest on capital allowed to X Rs.30,000 and Y Rs.15,000

(Insufficient profit. Hence 45,000 is distributed among the partners in the ratio of 2:1)

Question. A firm earned profits of ₹ 80,000, ₹ 1,00,000, ₹ 1,20,000 and ₹ 1,80,000 during 2010-11, 2011-12, 2012-13 and 2013-14 respectively. The firm has a capital investment of ₹5,00,000. A fair rate of return on investment is 15% pa. Calculate goodwill of the firm

based on three years' purchase of average super profits of last four yours.

Answer : Goodwill Rs. 1,35,000

Question. A Firm's average profits are 70,000. It includes an abnormal profit of 5,000. Capital invested in the business is 5,50,000 and the normal rate of return is 10%. Calculate goodwill at four times the super profit.

Answer : Goodwill Rs.40,000

Question. The goodwill of the firm is valued at 4 years purchase of average profit of five years. The profits for the last five years were:

Year Profit

2013-14 : 2,00,000

2014-15 : (3,00,000)

2015-16 : 4,50,000 ( including an abnormal gain of ₹ 50,000)

2016-17 : 3,50,000 (after charging an abnormal loss of ₹ 90,000)

2017-18 : 2,60,000

Calculate the amount of goodwill.

Answer : Goodwill Rs.8,00,000

Question. Aman, Babita, and Suresh are partners in a firm. Their profit-sharing ratio is 2:2:1. How-ever, Suresh is guaranteed a minimum amount of ₹ 10,000 as a share of profit every year. Any deficiency arising on that account shall be met by Babita. The profits for the two years ending 31st March 2020 and 2021 were ₹ 40,000 and ₹ 60,000 respectively. Prepare Profit and Loss Appropriation Account for the two years.

Answer : For the year ending 31st March 2020

Aman :40,000*2/5 = 16,000

Babitha : 40,000*2/5 =16,000

Suresh : 40,000*1/5 = 8,000

Deficiency of Suresh Rs.2,000 will be bore by Babitha

For the year ending 31st march 2021

Aman :60,000*2/5 = 24,000

Babitha : 60,000*2/5 =24,000

Suresh : 60,000*1/5 = 12,000

Suresh share of profit is more than the guaranteed amount , no adjustment is needed.

Question. The average profit of a firm is ₹ 48,000. The total assets of the firm are ₹ 8,00,000. The value of other liabilities is ₹ 5,00,000. The average rate of return in the same business is 12%.

Calculate goodwill from 22capitalization of average profits method.

Answer : Goodwill Rs.1,00,000 (capital employed = Asset-Liabilities)

Question. Gupta is a partner in a firm. He drew regularly ₹ 8,00 at the beginning of every month for the six months ending 31st March 2022. Calculate interest on drawings @15% p.a.

Answer : Interest on drawings Rs.240

Question. The capital of the firm of Anuj and Benu is ₹ 10,00,000 and the market rate of interest is 15%. The annual salary of the partners is ₹ 60,000 each. The profit for the last three years were ₹ 2,80,000, ₹ 3,80,000, and ₹ 4,20,000. Goodwill of the firm is to be valued on the basis of two years’ purchases of the last three years’ average super profits. Calculate the goodwill of the firm.

Answer : Goodwill Rs.1, 80,000

LONG ANSWER TYPE QUESTIONS

Question. The capital accounts of Alka and Archana showed a credit balance of Rs.4,00,000 and 3,00,000 respectively, after taking into account drawings and a net profit of RS.2,00,000. The drawings of the partners during the year 2018-19 were

a. Alka withdrew Rs.10,000 at the end of each quarter

b. Archana’s drawings were

31st May 2018 Rs.8,000

1st November 2018 Rs. 7,000

1st February 2019 Rs. 5,000

Calculate interest on partner’s capitals@10% p a and interest on partners’ drawings @ 6% p a for the year ended 31st March 2019.

Answer : Interest on capital: Alka Rs.34,000 Archana Rs.22,000

Interest on drawings: Alka 40,000*6/100*4.5/12 = 900/-

Archana 1,25,000*6/100*1/12 =625/-

Question. A and B started a partnership business on 1st April 2021. They contributed ₹ 6,00,000 and ₹ 4,00,000 respectively, as their capitals. The terms of the partnership agreement are as under:

(i) Interest on capital and drawings @ 6% per annum.

(ii) B is to get a monthly salary of ₹ 2,500.

(iii) Sharing of profit or loss will be in the ratio of their capital contribution.

The profit for the year ended 31st March 2022, before making the above appropriations was ₹ 2,07,400. The drawings of A and B were ₹ 48,000 and ₹ 40.000 respectively. Interest on drawings amounted to ₹ 1,500 for A and ₹ 1,100 for B.

Prepare profit and loss appropriation accounts and partner's capital accounts

assuming that their capitals are fluctuating.

Answer : Divisible profit Rs.1,20,000.

Capital balance : A ‘s capital Rs. 6,58,500 B’s capital Rs. 4,60,900

Question. Lata and Mamata are partners with capitals of ₹3,00,000 and ₹ 2,00,000 respectively sharing profits as Lata 70% and Mamata 30%. During the year ended 31st March 2021, they earned a profit of ₹ 2,26,440 before allowing interest on the partner's loan. The terms of the part-nership are as follows:

(i) Interest on Capital is to be allowed @ 7% p.a.

(ii) Lata is to get a salary of ₹ 2,500 per month.

(iii) Interest on Mamata’s Loan account of 80,000 for the whole year.

(iv) Interest on drawings of partners at 8% per annum. Drawings being Lata ₹36,000 and Mamata ₹ 48,000.

(v) 1/10th of the distributable profit should be transferred to General Reserve.

Prepare the Profit and Loss Appropriation Account.

Answer : Share of profit : Lata Rs.1,00,800 Mamata Rs.43,200

( interest on drawings will be calculated for an average period of 6 months.

Transfer to general reserve will be 10% of Rs.1,60,000)

Question. The capitals of X, Y, AND Z as of 31st march 2021 amounted to Rs. 1,50,000, 5,50,000 and 11,00,000 respectively. Divisible profit amounting to Rs.3,00,000 for the year ended 31st March 2021 was distributed in the ratio of 4:1:1 after allowing interest on capital @10% p a. During the year each partner withdrew Rs. 50,000 per month at the beginning of each month. The partnership deed was silent as to profit sharing ratio and interest on drawings but provided for interest on capital @12 p.a.

Showing your workings, pass necessary adjusting entries to rectify the above error.

Answer : X’s capital A/C Dr 1,10,000

To Y’s capital A/C 50,000

To Z’s capital A/C 60,000

Question. P and Q were partners in the firm sharing profits in the 3:1 ratio. Their respective fixed capitals were ₹ 10,00,000 and ₹ 6,00,000. The partnership deed provided interest on capital @ 12% p.a. The partnership deed further provided that interest on capital will be allowed fully even if it will result in a loss to the firm. The net profit of the firm for the year ended 31st March 2018 was ₹ 1,50,000.

Pass necessary journal entries in the books of the firm allowing interest on capital

and division of profit/loss among the partners.

Answer : Net loss transferred to current Account : P Rs.31,500 Q Rs.10,500

Question. Rohit, Raman, and Raina are partners in a firm. Their capital accounts on 1st April, 2019, stood at ₹ 2,00,000, ₹ 1,20,000 and ₹ 1,60,000 respectively. Each partner withdrew ₹ 15,000 during the financial year 2019-20.

As per the provisions of their partnership deed:

(a) Interest on capital was to be allowed @5% per annum.

(b) Interest on drawings was to be charged @4% per annum.

(c) Profits and losses were to be shared in the ratio of 5:4:1.

The net profit of ₹ 72,000 for the year ended 31st March 2020, was divided equally amongst the partners without providing for the terms of the deed.

You are required to pass a single adjustment entry to rectify the error (show workings clearly).

Answer : Raina’s capital A/C Dr 11,410

To Rohit’s capital A/C 10,150

To Ramana’s capital A/C 1,260

Question. The goodwill of the firm is valued at rs.1,35, 000 at three years purchase of the super profit. Determine the missing values.

Average profit = 3,60,000/3= Rs.1,20,000

Normal profit= ________*15/100 =?

Super profit = ?

Answer : Goodwill = super profit* no. of years purchase

1,35,000 = super profit*3

Then super profit =1,35,000/3= 45,000

Super profit = average profit-normal profit

45,000 = 1,20,000-normal profit

Then Normal profit =1,20,000-45,000 = 75,000

Normal profit = capital employed*rate/100

75,000 = capital employed *15/100

Then capital employed 75,000*100/15 =5,00,000

Question. Y and Z are partners with capitals of ₹ 25,000 and ₹ 15,000 respectively on 1st April 2020. Each partner is entitled to 9% p.a. interest on his capital. Z is entitled to a salary of ₹ 6,000 p.a. together with a commission of 6% of Net Profit remaining after deducting interest on capital and salary and after charging his commission. The profits for the year ended 31st March 2021 before making any of the above-mentioned adjustments amount to ₹ 30,800. Prepare Partner's Capital Accounts:

(1) when capitals are fixed, and

(2) when capitals are fluctuating.

Answer : Divisible profit of Rs.20,000

When capitals are fixed: current a/c balance Y Rs.12,250( cr ) Z Rs. 18,550(cr)

When capitals are fluctuating: capital accounts Y Rs. 37,250 (cr) Z Rs.33,550(cr)

Free study material for Accountancy

VBQs for Part 1 Chapter 1 Accounting for Partnership Basic Concepts Class 12 Accountancy

Students can now access the Value-Based Questions (VBQs) for Part 1 Chapter 1 Accounting for Partnership Basic Concepts as per the latest CBSE syllabus. These questions have been designed to help Class 12 students understand the moral and practical lessons of the chapter. You should practicing these solved answers to improve improve your analytical skills and get more marks in your Accountancy school exams.

Expert-Approved Part 1 Chapter 1 Accounting for Partnership Basic Concepts Value-Based Questions & Answers

Our teachers have followed the NCERT book for Class 12 Accountancy to create these important solved questions. After solving the exercises given above, you should also refer to our NCERT solutions for Class 12 Accountancy and read the answers prepared by our teachers.

Improve your Accountancy Scores

Daily practice of these Class 12 Accountancy value-based problems will make your concepts better and to help you further we have provided more study materials for Part 1 Chapter 1 Accounting for Partnership Basic Concepts on studiestoday.com. By learning these ethical and value driven topics you will easily get better marks and also also understand the real-life application of Accountancy.

FAQs

The latest collection of Value Based Questions for Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts is available for free on StudiesToday.com. These questions are as per 2026 academic session to help students develop analytical and ethical reasoning skills.

Yes, all our Accountancy VBQs for Part 1 Chapter 1 Accounting for Partnership Basic Concepts come with detailed model answers which help students to integrate factual knowledge with value-based insights to get high marks.

VBQs are important as they test student's ability to relate Accountancy concepts to real-life situations. For Part 1 Chapter 1 Accounting for Partnership Basic Concepts these questions are as per the latest competency-based education goals.

In the current CBSE pattern for Class 12 Accountancy, Part 1 Chapter 1 Accounting for Partnership Basic Concepts Value Based or Case-Based questions typically carry 3 to 5 marks.

Yes, you can download Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts VBQs in a mobile-friendly PDF format for free.