UNIT-IV

FORMS OF MARKET AND PRICE DETERMINATION

QUESTIONS BASED ON HOTS WITH MODEL ANSWERS

FORMS OF MARKET AND PRICE DETERMINATION

VERY SHORT ANSWER TYPE QUESTIONS (1 MARK)

Question. How is price determined under perfect competition?

Answer. Price is determined by an industry by the forces of demand and supply.

Question. What is the common feature shared by perfect and monopolistic competition?

Answer. (i) Free entry and exit of firms

(ii) Perfect mobility of factors.

Question. If the firms are earning abnormal profits, how will the number of firms in the industry change?

Answer. The number of firms in the industry will increase.

Question. Define the monopoly market.

Answer. It is a form of market under which there is a single seller, selling a product which does not have close substitutes.

Question. Under which market there is no difference between firm and industry?

Answer. Monopoly.

Question. What is normal profit?

Answer. It is the minimum profit which a firm must get to stay in business.

QUESTIONS BASED ON HOTS WITH MODEL ANSWERS

Q 1. Who determines price under perfect competition?

Ans: Price under perfect competition is determined by the forces of market demand and market supply in industry.

Q 2. If the firms are earning abnormal profits, how will the number of firms in the industry change?

Ans: The number of firms in the industry will tend to increase.

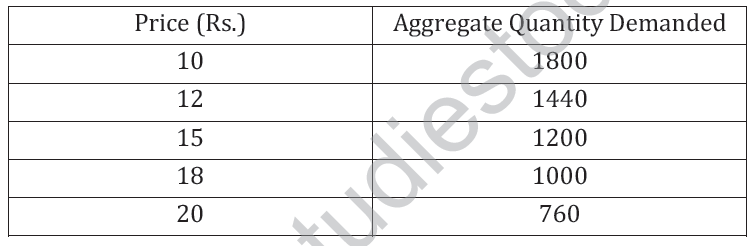

Q 3. The technology is such that the LAC is minimized at the firm output equal to 10 and minimum LAC is Rs. 15. Suppose the demand schedule for the product is given as follows:

(a) What will be total quantity sold in the market and how many firms will operate in the long run competitive equilibrium?

(b) Suppose that because of technological progress the LAC curve shifts down such that the minimum average cost is equal to Rs. 12 and it occurs at output level 8. How many firms will now operate in the market in the long run?

Ans: Long run equilibrium occurs when: AC = AR

Initially, AC is given as = Rs. 15

(At equilibrium, Quantity demanded = Quantity sold)

When P= AC = Rs. 15: Quantity Sold = 1200 units

When each firm is producing 10 units. No. of firms = 1200/10=120

When AC = Rs. 12

Then price (AR) = AC = Rs. 12, Quantity Sold= 1440 units.

When each firm is producing 8 units, No. of firms =1440/8 = 180

(a) Before change in technology: Quantity Sold = 1200 units and No. of firms =120

(b) After change in technology: Quantity Sold = 1440 units and No. of firms =180

Q 4. How much loss can a firm bear?

Ans: A firm can bear losses upto its total fixed costs.

Q 5. Explain the motivation behind granting patent rights.

Ans: Motivation behind granting patent rights are:

(A) To encourage research and development; and

(B) To encourage new discoveries and innovations.

Q 6. Explain how the efficiency may increase if two firms merge?

Ans: When the two firms merge, their combined efficiency is expected to improve owing to:

(A) Increase in the scale of output and the consequent economies of scale.

(B) Better division of labour and specialization; and

(C) Use of better technology, saving the cost of production.

Q 7. Why is the demand curve facing a monopolistically competitive firm likely to be very elastic?

Ans: It is because the products produced by the monopolistically competitive firms are close substitutes to each other. If products are close substitutes to each other the elasticity of demand is high, which is what makes the firm’s demand curve(under monopolistic competition) very elastic.

Q 8. Why is the demand curve facing a firm perfectly elastic under perfect competition but less than perfectly elastic under monopolistic competition?

Ans. The demand curve under perfect competition is perfectly elastic. Perfectly elastic demand curve means any quantity can be sold only at a given price. Under perfect competition, the price of the product is determined by the industry by the forces of demand and supply and the firm has no option but to accept it. Uniform price prevails because all firms are selling a homogeneous product. A firm cannot influence or alter the price. Implying that a firm can sell any quantity at the given price. Therefore, the demand curve will be a straight line parallel to the X-axis as shown in Fig. ; which is perfectly elastic, showing Ed=infinity The demand curve under monopolistic competition is less than perfectly elastic. It means more can be sold only at lower price. Under monopolistic competition, the seller sells a differentiated product, so he exercises partial control over price. But he can sell more only by lowering the price; certainly not at the existing price.

This is what makes the demand curve less than perfectly elastic.

Q 9. Which features of monopolistic competition are monopolist in nature?

A.9 (i) Control over price

(ii) Downward sloping demand curve

Q 10. How does an increase in the price of a substitute good in consumption affect the equilibrium price?

Ans: With increase in the price of the substitute good, the equilibrium price of the concerned good will increase owing to shift in demand curve to the right.

Q 11. ‘Changes in both demand any supply of a commodity may or may not affect its equilibrium price.’ Explain.

Ans: If the demand and supply of a commodity change equally, and in the same direction there will be no effect on its price. On the other hand, an unequal change in demand and supply will affect equilibrium price. When demand increases more than supply, equilibrium price will rise. On the other hand, when supply increases more than demand, equilibrium price will fall.

Q 12. When will the equilibrium price of a commodity not change even if its demand and supply both increase? Explain with the help of a diagram.

Ans. If both increases equally.

Q 13. A severe drought results in a drastic fall in the output of wheat. Analyze how will it affect the market price of wheat?

Ans: As a result of severe drought, the output of wheat is reduced. It means the supply of wheat in the market will reduce, causing a shift of supply curve to the left. Accordingly, market price of wheat will increase.

Q 14. Suppose the demand for jeans increases. At the same time, because of an increase in price of cotton, the supply of jeans decreases. How will it affect the price and quantity sold of jeans?

Ans: Increase in market demand for jeans along with a decrease in the supply of jeans should raise the price of jeans and the quantity sold will decline.

Q 15. China is a big manufacturer of technology of telephone instruments. It has recently become a member of W.T.O., which means it can sell its products in other member countries like India. Suppose that it does export a large number of telephone instruments to India:

(A) How will it affect the price and quantity sold of telephone instruments in India?

(B) Suppose that the demand for telephone instruments is relatively elastic. How will if affect India’s total expenditure on telephone instruments?

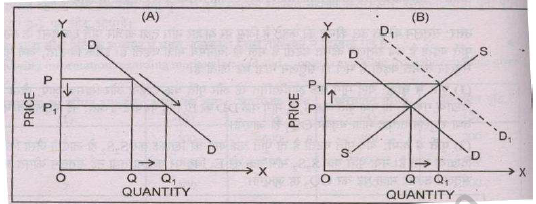

Ans: (A) As a result of large export of telephone instruments by Chine to India, the market supply of telephone instruments increases. It reduces the price of telephone instruments while the quantity sold will increase.

(B) If the demand for telephone instruments is relatively elastic, reduction in price should increase total expenditure on telephone instruments in India.

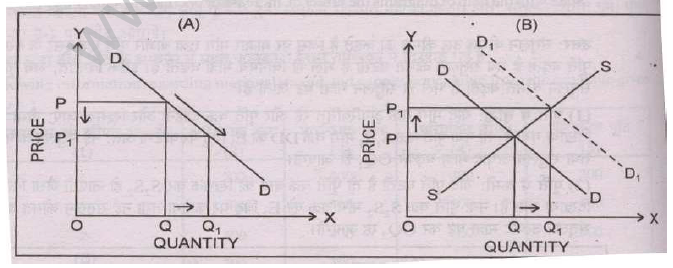

Q 16. Mrs. Ramgopal says that economists say inconsistent things: as price falls, demand rises, but as demand rises, price rises. Defend or refute.

Ans: The statement of Mrs. Ramgopal that “as price falls, demand rises, but as demand rises, price rises”, can be defended. The first part of the statement i.e. as price falls demand rises is the general behavior of the consumer in the market. This is simply a forward movement along a demand curve. Demand changes due to change in the price of the commodity. But, there may also be situation when increase in demand leads to increase in price. When the supply of the commodity remains unchanged. And demand increases (due to factors other than price such as increase in income of the consumer or change in taste preference of the consumer.) The demand curve shifts upward and it raises the market price. Fig. illustrates the two situations:

Q 17. Answer all the questions in terms of shifts in or movements along the demand and supply curves.

(A) In 2001, the Supreme Court of India banned smoking in public places. How is this likely to affect the average price of cigarettes and the quantity sold?

(B) New discoveries of oil reduce the price of petrol and diesel. Consider their effects on the market for new cars.

(C) New environmental regulations require the drug industry to use a more environment friendly technology whose running cost are higher but which discharges less chemicals than before. How would it affect the price of drug?

Ans: (A) A ban on cigarette smoking in public places should cause a backward shift in demand curve. Consequently average price of cigarettes should fall. Fall in average price of cigarette should cause a fall in quantity sold.

(B) New discoveries of oil reducing the price of petrol/diesel should imply increase in demand for cars (in terms of shift in demand curve to the right), as cars and petrol/diesel are complementary goods.

(C) Due to the use of costlier (environment friendly) technology, supply curve of drug will shift to the left, causing a rise in the price of drug.

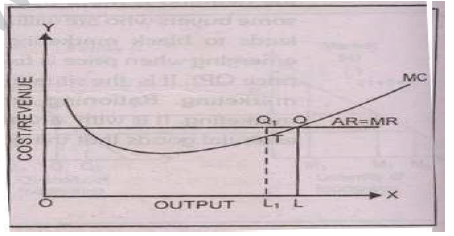

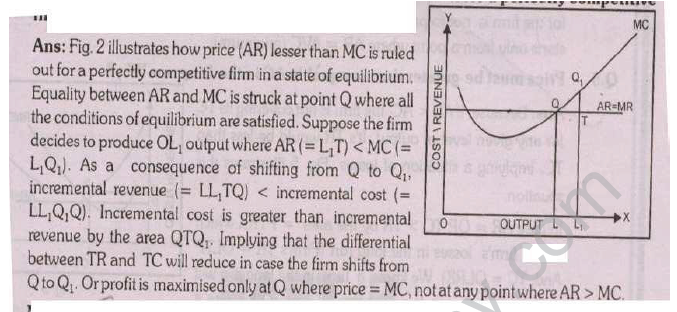

Q 18. In a state of equilibrium, price greater than MC is ruled out for a perfectly competitive firm. Show diagrammatically.

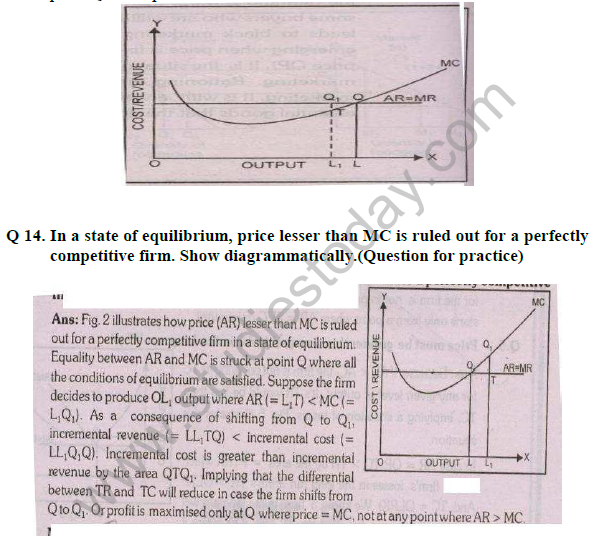

Ans: Fig illustrates how prices greater than MC is ruled out for a perfectly competitive firm in a state of equilibrium. Equality between price (AR) and MC is struck at point Q where all the conditions of equilibrium are satisfied. OL is the equilibrium level of output. Suppose the firm decides to produce OL1 output where AR(=L1Q1)>MC(=L1T1). As a consequence of shifting from Q to Q1; loss of TR=Q1L1LQ, while the TC is saved to the tune of Q1TQ.

Evidently, reduction in TC (=Q1TQ) is only a part of reduction in TR(=Q1L1LQ). Implying that the differential between TR and TC(= profit) would reduce in case the firm shifts from Q to Q1 Profit is maximized only at point Q where price = MC.

Q 19. In a state of equilibrium, price lesser than MC is ruled out for a perfectly competitive firm. Show diagrammatically.(Question for practice)

Q 20. What is firm’s supply curve in the short run, operating under perfect competition?

Ans: It is MC curve of the firm starting from a point where MC=AVC (minimum).

In Figure, short period supply curve of the firm is MC curve starting from point Q where AR= AVC (minimum).

Q.21 In which market situation , the influence of an individual seller is zero?

A.21 In the Perfectly Competitive market situation.

Q.22 How is a single buyer a price taker in perfect competition?

A.22 A single buyer’s share in total market demand is so significant that the buyer can not influence the market price on his own by changing his demand.

Q.23 Normal profit means zero economic profit. Why?

A.23 Suppose the existing firms are earning above normal profits. Attracted by the positive profits , the new firms enter the industry .The market supply increases and the price comes down. New firms continue to enter and the price continues to fall till economic profits are reduced to zero.

In case of losses, firms start leaving the industry , supply falls and prices starts going up and all this continues till losses are wiped out. Remaining firms in the industry then once again earn just normal profits / zero profit.

VERY SHORT ANSWER TYPE QUESTIONS: - (1 Mark Each)

Q. 1. What is the value of MR when demand curve is elastic?

Ans. MR is positive.

Q. 2. In which market DD curve is indeterminate?

Ans.- Oligopoly Market.

Q 3. Who determines price under perfect competition?

Ans: Price under perfect competition is determined by the forces of market demand and market supply in industry.

Q 4. How much loss can a firm bear?

Ans: A firm can bear losses upto its total fixed costs in short run.

Q 5. Explain the motivation behind granting patent rights.

Ans: Motivation behind granting patent rights are:

(A) To encourage research and development; and

(B) To encourage new discoveries and innovations.

SHORT ANSWER TYPE QUESTIONS: - (3 /4 Marks Each)

Q 1. Explain how the efficiency may increase if two firms merge?

Ans: When the two firms merge, their combined efficiency is expected to improve owing to:

(A) Increase in the scale of output and the consequent economies of scale.

(B) Better division of labour and specialization; and

(C) Use of better technology, saving the cost of production.

Q 2. Why is the demand curve facing a monopolistically competitive firm likely to be very elastic?

Ans: It is because the products produced by the monopolistically competitive firms are close substitutes to each other. If products are close substitutes to each other the elasticity of demand is high, which is what makes the firm‟s demand

curve(under monopolistic competition) very elastic.

Q 3. Why is the demand curve facing a firm perfectly elastic under perfect competition but less than perfectly elastic under monopolistic competition?

Ans. The demand curve under perfect competition is perfectly elastic. Perfectly elastic demand curve means any quantity can be sold only at a given price. Under perfect competition, the price of the product is determined by the industry by the forces of demand and supply and the firm has no option but to accept it. Uniform price prevails because all firms are selling a homogeneous product. A firm cannot influence or alter the price. Implying that a firm can sell any quantity at the given price. Therefore, the demand curve will be a straight line parallel to the X-axis as shown in Fig. ; which is perfectly elastic, showing Ed=infinity

The demand curve under monopolistic competition is less than perfectly elastic. It means more can be sold only at lower price. Under monopolistic competition, the seller sells a differentiated product, so he exercises partial control over price. But he can sell more only by lowering the price; certainly not at the existing price. This is what makes the demand curve less than perfectly elastic.

Q 4. Which features of monopolistic competition are monopolist in nature?

Ans. (i) Product differentiation

(ii) Control over price

(iii) Downward sloping demand curve

Q 5. How does an increase in the price of a substitute good in consumption affect the equilibrium price?

Ans: With increase in the price of the substitute good, the equilibrium price of the concerned good will increase owing to shift in demand curve to the right.

Q 6. „Changes in both demand any supply of a commodity may or may not affect its equilibrium price.‟ Explain.

Ans: If the demand and supply of a commodity change equally, and in the same direction there will be no effect on its price. On the other hand, an unequal change in demand and supply will affect equilibrium price. When demand increases more than supply, equilibrium price will rise. On the other hand, when supply increases more than demand, equilibrium price will fall.

Q 7. When will the equilibrium price of a commodity not change even if its demand and supply both increase? Explain with the help of a diagram.

Ans. If both increases equally.

Q 8. A severe drought results in a drastic fall in the output of wheat. Analyze how will it affect the market price of wheat?

Ans: As a result of severe drought, the output of wheat is reduced. It means the supply of wheat in the market will reduce, causing a shift of supply curve to the left. Accordingly, market price of wheat will increase.

Q 9. Suppose the demand for jeans increases. At the same time, because of an increase in price of cotton, the supply of jeans decreases. How will it affect the price and quantity sold of jeans?

Ans: Increase in market demand for jeans along with a decrease in the supply of jeans should raise the price of jeans and the quantity sold will decline.

Q 10. China is a big manufacturer of technology of telephone instruments. It has recently become a member of W.T.O., which means it can sell its products in other member countries like India. Suppose that it does export a large number of telephone instruments to India:

(A) How will it affect the price and quantity sold of telephone instruments in India?

(B) Suppose that the demand for telephone instruments is relatively elastic. How will it affect India‟s total expenditure on telephone instruments?

Ans: (A) As a result of large export of telephone instruments by Chine to India, the market supply of telephone instruments increases. It reduces the price of telephone instruments while the quantity sold will increase.

(B) If the demand for telephone instruments is relatively elastic, reduction in price should increase total expenditure on telephone instruments in India.

Q 11. Mrs. Ramgopal says that economists say inconsistent things: as price falls, demand rises, but as demand rises, price rises. Defend or refute.

Ans: The statement of Mrs. Ramgopal that “as price falls, demand rises, but as demand rises, price rises”, can be defended. The first part of the statement i.e. as price falls demand rises is the general behavior of the consumer in the market. This is simply a forward movement along a demand curve. Demand changes due to change in the price of the commodity. But, there may also be situation when increase in demand leads to increase in price. When the supply of the commodity remains unchanged. And demand increases (due to factors other than price such as increase in income of the consumer or change in taste preference of the consumer.) The demand curve shifts upward and it raises the market price. Fig. illustrates the two situations:

Q 12. Answer all the questions in terms of shifts in or movements along the demand and supply curves.

(A) In 2001, the Supreme Court of India banned smoking in public places. How is this likely to affect the average price of cigarettes and the quantity sold?

(B) New discoveries of oil reduce the price of petrol and diesel. Consider their effects on the market for new cars.

(C) New environmental regulations require the drug industry to use a more environment friendly technology whose running cost are higher but which discharges less chemicals than before. How would it affect the price of drug?

Ans: (A) A ban on cigarette smoking in public places should cause a backward shift in demand curve. Consequently average price of cigarettes should fall. Fall in average price of cigarette should cause a fall in quantity sold.

(B) New discoveries of oil reducing the price of petrol/diesel should imply increase in demand for cars (in terms of shift in demand curve to the right), as cars and petrol/diesel are complementary goods.

(C) Due to the use of costlier (environment friendly) technology, supply curve of drug will shift to the left, causing a rise in the price of drug.

Q 13. In a state of equilibrium, price greater than MC is ruled out for a perfectly competitive firm. Show diagrammatically.

Ans: Fig illustrates how prices greater than MC is ruled out for a perfectly competitive firm in a state of equilibrium. Equality between price (AR) and MC is struck at point Q where all the conditions of equilibrium are satisfied. OL is the equilibrium level of output. Suppose the firm decides to produce

OL1 output where AR(=L1Q1)>MC(=L1T1). As a consequence of shifting from Q to Q1; loss of TR=Q1L1LQ, while the TC is saved to the tune of Q1TQ.

Evidently, reduction in TC (=Q1TQ) is only a part of reduction in

TR(=Q1L1LQ). Implying that the differential between TR and TC(= profit) would reduce in case the firm shifts from Q to Q1 Profit is maximized only at point Q where price = MC.

Q 15. What is firm‟s supply curve in the short run, operating under perfect competition?

Ans: It is MC curve of the firm starting from a point where MC=AVC (minimum). In Figure, short period supply curve of the firm is MC curve starting from point Q where AR= AVC (minimum).

Q.16 In which market situation, the influence of an individual seller is zero?

Ans. In the Perfectly Competitive market situation.

Q.17 How is a single buyer a price taker in perfect competition?

Ans. A single buyer‟s share in total market demand is so significant that the buyer cannot influence the market price on his own by changing his demand.

Q.18 Normal profit means zero economic profit. Why?

Ans. Suppose the existing firms are earning above normal profits. Attracted by the positive profits, the new firms enter the industry .The market supply increases and the price comes down. New firms continue to enter and the price continues to fall till economic profits are reduced to zero. In case of losses, firms start leaving the industry, supply falls and prices starts going up and all this continues till losses are wiped out. Remaining firms in the industry then once again earn just normal profits / zero profit.

Q. 19. Why does there are few firms in oligopoly market?

Ans.- There are only few firms in oligopoly market because there are some restrictions on the entry of firms in the market. Which are inter-dependence of firms, big requirements of funds, great competition among the firms. The only

firms which can break these restrictions are able to enter the market.

Q. 20. Does a monopolist has full control over the price?

Ans. No, because price is determined by the forces of demand and supply . a monopolist controls only the supply side and demand side remain uncontrolled.

Q.1 Explain the implication of large number of buyers in a perfectly competetive market.

Ans. The implication is that no single buyer is in a position to influence the market price on its own because an individual buyer’s purchase forms a negligible proportion of the total purchase of the good in the market.

Q. 2 Explain why are firms mutually interdependent in an oligopoly market.

Ans. Firms are mutually interdependent because an individual firms takes decision about price and output after considering the possible reactions by the rival firms.

Q. 3 Explain the inplication of ‘freedom of entry and exit to the firms’ under perfect competition.

Ans. The firms enter the industry when they firnd that the existing firms are earning super normal profits. Their entry raises output of the industry, brings down the market price and thus reduce profits. The entry continues till profits are reduced to normal (or zero) The firms start leaving the industry when they are facing losses. This reduces output of the industry, raises market price and reduces losses. The exit continues till the losses are wiped out.

Q. 4 Explain the implication of ‘perfect knowledge about market’ under perfect competition.

Ans. Perfect knowledge means that both buyers and sellers are fully informed about the market price. Therefore no firm is in a position to charge a different price and no buyer will pay a higher price. As a result a uniform price prevails in the market.

Q. 5 Why is the demand curve more elastic under monopolistic competition than under monopoly.

Ans. The elasticity of demand is high when the product has close substitutes and that elasticity of demand tends to be low when the product does not have close substitutes as we know in monopolistic competition there is large number of close substitutes while in monopoly there is no close substitutes hence the demand curve under monopolistic competition is more elastic than under monopoly.

Q. 6 Why is a firm under perfect competition a price taken while under monopoly a price maker? Explain in brief.

Ans. A firm under perfect competition a price taker by the following reasons:

1. Number of firms : The number of firms under perfect competition is so large that no individual firm by changing sale, can cause any meaningful change in the total market supply. Hence, market price remains unaffected.

2. Homogenuous product : All firms in a perfectly competitive industry produce homogeneous product. Hence, price remains same.

3. Perfect knwledge : All the buyers and sellers have perfect knowledge about market price so no firm charge a different price than market price. Hence a uniform price prevails in the market.

A firm under monopoly a price maker by the following reasons :

1. A monopolist is a single seller of the product in the market. Hence it has full control over supply

2. There are no close substitutes of the monopoly product, hence the demand is less elastic or ‘inelastic.

3. There are legal, technical and natural barriers to the entry of new firms so that there is no fear of increase in market supply.

Q. 7 Differentiate between price discrimination and product differentiation.

Ans. Price discrimination : Price discrimination is a situation when a monopolist charges different price from different buyers of the same product. This is generally done to maximise profits.

Product Differentiation : Product differentitation is a situation when different producers under monopolistic competition, try to differentiate their product in terms of its shape, size, packaging, trade mark or brand name. This is done to attract buyers from the rival firms in the market.

Q. 8 Distinguish between perfect competition and monopoly.

Ans. Perfect competition Monopoly

1. Large numer of buyers and seller 1. One seller & large and sellers no. of buyers.

2. Products are 2. There is no close substitutes homogeneous of goods.

3. Free entry & exit 3. Barriers to entry

4. There is no control over price 4. There is full control over over price market price.

Q. 9 Differentiate between monopoly & monopolistic competition.

Ans. Monopoly Monopolistic competition

1. Single seller & large 1. Large number of buyers and seller.

no. of buyers.

2. No. close substitutes of product. 2. There is product differentiation.

3. Barriers to entry 3. Free entry and exit.

4. Selling cost is zero. 4. Heavy selling costs are incurred.

Q. 10 What is oligopoly? State its main properties/features.

Ans. Oligopoly : It is a form of the market in which there are a few big sellers of a commodity and a large number of buyers. There is a high degree of interdependence among the sellers regarding their price & output policy.

Following are some principal features of oligopoly :

1. A few firms

2. High degree of interdependence.

3. Non-price competition.

4. Entry barriers.

5. Formation of cartels.

6 MARKS QUESTIONS

Q.1 Distinguish between collusive and non-collusive oligopoly. Explain how the oligopoly firms are interdependent in taking price and output decisions.

Ans. Collusive oligopoly is one in which the firms cooperate with each other in deciding price and output where as, non-collusive oligopoly is one in which the firms compete with each other. The firms are interdependent because each firm takes into consideration the likely reactions of its rival firms when deciding its output and price policy.

It makes a firm dependent on other firms. The firm may have to reconsider the change in the light of the likely reactions.

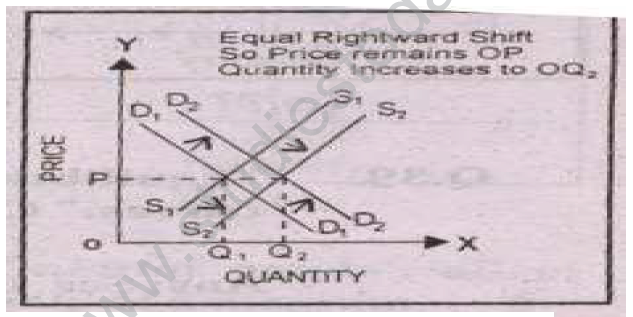

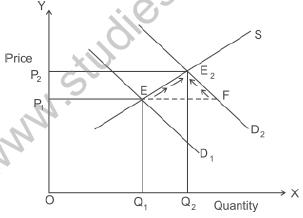

Q. 2 Market for a good is in equilibrium. There is an ‘increase’ in demand for this good. Explain the chain of effects of this change. Use diagram.

– Increase in demand shifts the demand curve from D1 to D2 to the right leading to excess demand E1 F at the given price OP1.

– Since the consumers will not be able to buy all they want to buy at this price, there will be competition among buyers leading rise in price.

– As price rises, demand starts falling (along D2) and supply starts rising (along S) as shows by arrows in the diagram.

– This change continue till D and S are equal at E2.

– The quantity rises to OQ and price to OP2.

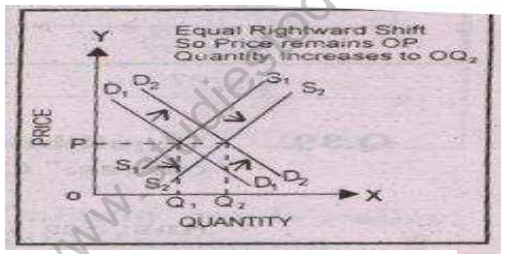

Q. 3 Market for a good is in equilibrium. There is simultaneous ‘decrease’ both in demand and supply of the good. Explain its effect on market price.

Ans. There are three possibilities :

1. If the relative (percentage) decrease in demand is greater than the decrease in supply, price will fall. The price will fall because of excess supply in the market.

2. If the relative (percentage) decrease in demand is less than the decrease in supply price will rise. The price will rise because of excess demand in the market.

3. If the relative (percentage) decrease in demand is equal to the decrease in supply price will remain unchanged The price will remain unchanged because there is neither excess demand nor excess supply in the market.

Q.4 Explain why the equilibrium price of commodity is determined at that level of output at which its demand equals its supply.

Ans. Suppose demand is greater than supply. Since the buyers will not be able to buy all what they want, there will be competition among the buyers. It will have on upward influence on the price. As a reasult demand will start falling and supply rising. It will go on till demand is equal to supply again.

It demand is less than supply. Since the sellers will not able to sell all what they want, there will be competition among the sellers. It will have a downward influence on the price. As a reasult demand will start rising and supply falling. It will go on till demand is equal to supply again.

Hence, the equilibrium price of a commodity is determined at that level of output at which its demand equals its supply.