Refer to CBSE Class 12 Accountancy HOTs Admission Of A Partner. We have provided exhaustive High Order Thinking Skills (HOTS) questions and answers for Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner. Designed for the 2026-27 exam session, these expert-curated analytical questions help students master important concepts and stay aligned with the latest CBSE, NCERT, and KVS curriculum.

Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Class 12 Accountancy HOTS with Solutions

Practicing Class 12 Accountancy HOTS Questions is important for scoring high in Accountancy. Use the detailed answers provided below to improve your problem-solving speed and Class 12 exam readiness.

HOTS Questions and Answers for Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner

Admission Of A Partner

MCQ Questions for NCERT Class 12 Accountancy Reconstitution of Partnership Firm – Admission of a Partner

Question: Profit or loss on revaluation of assets is transferred to Partners’ Capital account in which ratio?

(a) Equally

(b) Profit sharing ratio

(c) Fixed capital ratio

(d) Current capital ratio

Answer: B

Question. Which of the following is not the reconstitution of partnership?

(a) Admission of a partner

(b) Dissolution of Partnership

(c) Change in Profit Sharing Ratio

(d) Retirement of a partner

Answer : B

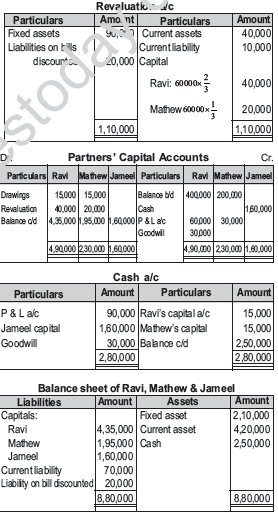

Question. A and B are partners sharing profit and losses in ratio of 5:3. C is admitted for 1/4th share. On the date of reconstitution, the debtors stood at Rs 40,000, bill receivable stood at Rs. 10,000 and the provision for doubtful debts appeared at Rs. 4000. A bill receivable, of Rs 10,000 which was discounted from the bank, earlier has been reported to be dishonored. The firm has sold, the debtor so arising to a debt collection agency at a loss of 40%. If bad

debts now have arisen for Rs 6,000 and firm decides to maintain provisions at same rate as before then amount of Provision to be debited to Revaluation Account would be:

(a) Rs 4,400

(b) Rs 4,000

(c) Rs 3,400

(d) None of the above

Answer : C

Question. A, and B are partners sharing profits in the ratio of 2:3. Their balance sheet shows machinery at ₹ 2,00,000; stock ₹ 80,000, and debtors at ₹ 1,60,000. C is admitted and the new profit sharing ratio is 6:9:5. Machinery is revalued at ₹ 1,40,000 and a provision is made for doubtful debts @5%. A’s share in loss on revaluation amount to ₹ 20,000. Revalued value of stock will be:

(a) ₹62,000

(b) ₹1,00,000

(c) ₹60,000

(d) ₹98,000

Answer : C

Question. As per ----------- , only purchased goodwill can be shown in the Balance Sheet.

(a) AS 37

(b) AS 26

(c) Section 37

(d) AS 37

Answer : B

Question. On the admission of a new partner:

(a) Old partnership is dissolved

(b) Both old partnership and firm are dissolved

(c) Old firm is dissolved

(d) None of the above

Answer : A

Question. At the time of admission of a partner, Employees Provident Fund is:

(a) Distributed to partners in the old profit sharing ratio

(b) Distributed to partners in the new profit sharing ratio

(c) Adjusted through gaining ratio

(d) None of the above

Answer : B

Question. Premium brought by newly admitted partner should be:

(a) Credited to sacrificing partners

(b) Credited to all partners in the new profit sharing ratio

(c) Credited to old partners in the old profit sharing ratio

(d) Credited to only gaining partners

Answer : A

Question. Which statement is true with respect to AS-26?

(a) Purchased goodwill can be shown in the Balance Sheet

(b) Revalued goodwill can be shown in the Balance Sheet

(c) Both purchased goodwill and revalued can be shown in the Balance Sheet

(d) None of the above

Answer : A

Question: New partner may be admitted to partnership:

(a) With the consent of all the old partners

(b) With the consent of any one partner

(c) With the consent of 2/3rd of the old partners

(d) With the consent of 3/4th of the old partners

Answer: A

Question: When is Revaluation A/c prepared?

(a) At the time of admission

(b) At the time of retirement

(c) At the time of death

(d) All of the above

Answer: D

Question: On admission of a partner, which of the following items of the balance sheet is transferred to the credit of capital accounts of old partners in the old profit sharing ratio, if capital accounts are maintained on fluctuating capital accounts method:

(a) Deferred revenue expenditure

(b) Profit and loss account (debit balance)

(c) Profit and loss account (credit balance)

(d) Balance in drawing account of partners

Answer: C

Question:The proportion in which old partners make a sacrifice:

(a) Ratio of capital

(b) Ratio of sacrifice

(c) Gaining ratio

(d) Profit sharing ratio

Answer: B

Question: General reserve at the time of admission of a partner is transferred to:

(a) Revaluation a/c

(b) Partners’ capital a/c

(c) Neither of two

(d) Profit and loss a/c

Answer: B

Question: When a new partner is admitted into the firm the old partner stands to :

(a) Gain in profit sharing ratio

(b) Lose in profit sharing ratio

(c) Not affected at all

(d) Only one partner gain other loose

Answer: B

Question: When goodwill is not recorded in the books at all on admission of a partner:

(a) If paid privately

(b) If brought in cash

(c) If not brought in cash

(d) If brought in kind

Answer: A

Question: All accumulated losses are transferred to the capital a/c of the partners in:

(a) New profit sharing ratio

(b) Old profit sharing ratio

(c) Capital ratio

(d) None of the above

Answer: B

Question: The need of revaluation of assets and liabilities on admission:

(a) Assets and liabilities should appear at revised value

(b) Any profit and loss on account of change in values belong to old partners

(c) All unrecorded assets and liabilities get recorded

(d) None of the above

Answer: B

CASE STUDEY BASED QUESTIONS

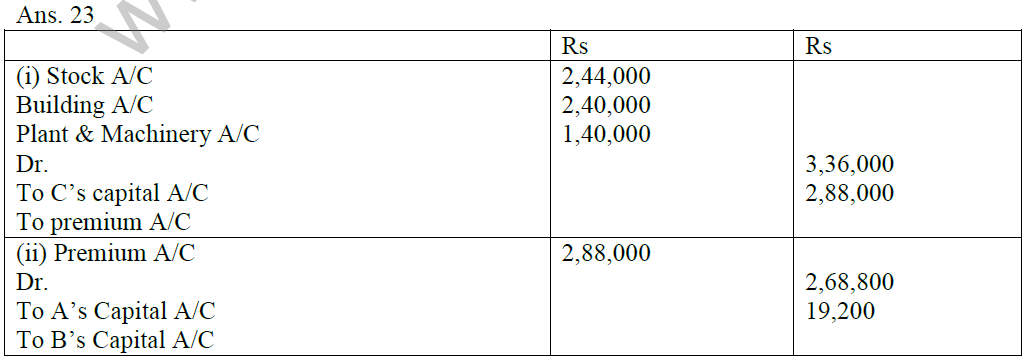

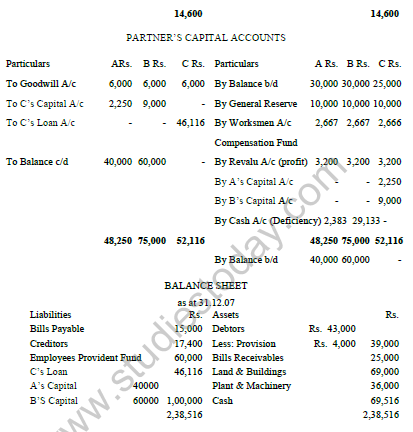

A, B and C are partners sharing profits and losses in the ratio of 5 : 3 : 2. Their Balance Sheet as at 31st March, 2019 stood as follows:

They decided to share profits equally w.e.f. 1st April, 2019. They also agreed that: (i) Value of Land and Building be decreased by 5%. (ii) Value of Machinery be increased by 5%. (iii) A Provision for Doubtful Debts be created @ 5% on Sundry DebtoRs. (iv) A Motor Cycle valued at Rs. 20,000 was unrecorded and is now to be recorded in the books. (v) Out of Sundry Creditors, Rs. 10,000 is not payable. (vi) Goodwill is to be valued at 2 years' purchase of last 3 years profits. Profits being for 2018-19 − Rs. 50,000 (Loss); 2017-18 − Rs. 2,50,000 and 2016-17 − Rs. 2,50,000. (vii) C was to carry out the work for reconstituting the firm at a remuneration (including expenses) of Rs. 5,000. Expenses came to Rs. 3,000.

Question: Remuneration expenses will be:

(a) Rs. 3000 Debited to Revaluation A/c

(b) Rs. 5000 Debited to Revaluation A/c

(c) Rs.3000 Shown on Liability side of the Balance Sheet

(d) Rs.3000 Shown on Asset side of the Balance Sheet

Answer: C

Question: What journal entry will be passed for Investment Fluctuation Reserve?

(a) Dr. Investment Fluctuation Reserve A/c Rs. 30,000, Cr. Investment Rs. 10,000; Cr. A’s Capital A/c Rs. 10,000; Cr. B’s Capital A/c Rs. 6,000; Cr. C’s Capital A/c Rs. 4,000 A

(b) Dr. Investment Fluctuation Reserve A/c Rs. 30,000, Cr. A’s Capital A/c Rs. 10,000; Cr. B’s Capital A/c Rs. 10,000; Cr. C’s Capital A/c Rs. 10,000 A

(c) Dr. A’s Capital A/c Rs. 10,000; Dr. B’s Capital A/c Rs. 10,000; Dr. Investment Rs. 10,000; Cr. Workmen’s Compensation Reserve A/c Rs. 30,000

(d) Dr. Revaluation Rs. 10,000; Cr. Investment Rs. 10,000

Answer: A

Question: Profit (gain) on Revaluation of Assets and Reassessment of Liabilities is:

(a) Rs. 17,000

(b) Rs. 22,000

(c) Rs. 57,000

(d) Rs. 2,000

Answer: A

Question: What journal entry is passed for goodwill?

(a) B’s Capital A/c Dr.10,000; C ’s Capital A/c Dr.40,000; A’s Capital A/c Cr. 50,000

(b) Dr. Goodwill A/c Rs. 3,00,000; Cr. A’s Capital A/c Rs. 1,50,000; Cr. B’s Capital A/c Rs. 90,000; Cr. C’s Capital A/c Rs. 60,000

(c) A’s Capital A/c Cr.50,000; B’s Capital A/c Cr.10,000; C ’s Capital A/c Dr.60,000;

(d) Dr. Goodwill A/c Rs. 50,000; Cr. Revaluation A/c Rs. 50,000

Answer: B

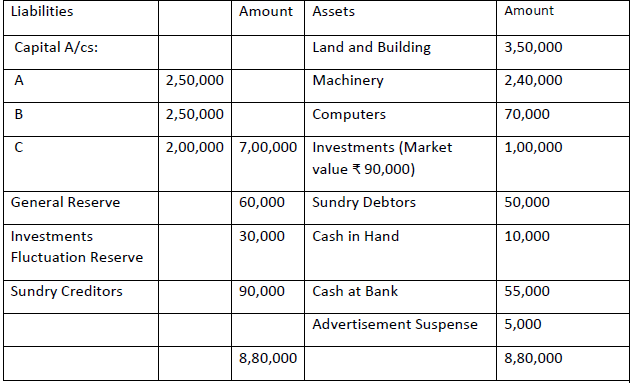

Balance Sheet of X and Y, who share profits and losses as 5 : 3, as at 1st April, 2019 is:

On the above date, they decided to change their profit-sharing ratio to 3 : 5 and agreed upon the following:

(a) Goodwill be valued on the basis of two years' purchase of the average profit of the last three yeaRs. Profits for the years ended 31st March, are: 2016-17 − Rs. 7,500; 2017-18 − Rs. 4,000; 2018-19 − Rs. 6,500.

(b) Machinery and Stock be revalued at Rs. 45,000 and Rs. 8,000 respectively.

(c) Claim on account of workmen compensation is Rs. 6,000.

Question: Employees' Provident Fund of Rs. 1,000 to be:

(a) Debited to Revaluation A/c

(b) Credited to Revaluation A/c

(c) Shown on Liability side of the Balance Sheet

(d) Credited to Partners capital A/c

Answer: C

Question: Advertisement suspense a/c of Rs. 800 will be:

(a) Debited to Revaluation A/c

(b) Credited to Revaluation A/c

(c) Debited to Partners capital A/c

(d) Credited to Partners capital A/c

Answer: C

Question: What journal entry is passed for goodwill?

(a) Y’s Capital A/c Dr.3,000; X’s Capital A/c Cr.3,000

(b) Dr. Goodwill A/c Rs. 12,000; Cr. X’s Capital A/c Rs. 6,000; Cr. Y’s Capital A/c Rs. 6,000

(c) Y’s Capital A/c Cr.3,000; X’s Capital A/c Cr.3,000

(d) Dr. Goodwill A/c Rs. 12,000; Cr. Revaluation A/c Rs. 12,000

Answer: A

Question: What journal entry will be passed for Workmen’s Compensation Fund?

(a) Dr. Workmen’s Compensation Fund Rs. 10,000, Cr. Claim for Workmen’s Compensation Rs. 6,000; Cr. X’s Capital A/c Rs. 2,500; Cr. Y’s Capital A/c Rs. 1,500

(b) Dr. Workmen’s Compensation Fund Rs. 10,000; Cr. X’s Capital A/c Rs. 6,250; Cr. Y’s Capital A/c Rs. 3,750

(c) Dr. X’s Capital A/c Rs. 1,500; Dr. Y’s Capital A/c Rs. 2,500; Dr. Claim for Workmen’s Compensation Rs. 6,000; Cr. Workmen’s Compensation Reserve A/c Rs. 10,000

(d) Dr. Revaluation Rs. 4,000; Cr. Claim for Workmen’s Compensation Rs. 4,000

Answer: A

X, Y and Z are partners sharing profits and losses in the ratio of 5 : 3 : 2. From 1st April, 2018, they decided to share profits and losses equally. The profit and loss account showed adebit balance of Rs.10,000. The Partnership Deed provides that in the event of any change in the profit-sharing ratio, the goodwill should be valued at two years' purchase of the average profit of the preceding five yeaRs. The profits and losses of the preceding years ended 31st March, are:

Question: State the ratio in which the partners share the accumulated profits when there is a change in the profit sharing ratio amongst existing partneRs.

(a) Old ratio

(b) New ratio

(c) Equal ratio

(d) Sacrificing ratio

Answer: A

Question: Change in the existing agreement of profit sharing ratio is considered as

(a) Reconstitution of a partnership firm

(b) Revaluation of a partnership firm

(c) Dissolution of a partnership firm

(d) None of the above

Answer: A

Question: What is the amount of Goodwill credited to X Capital A/c?

(a) Rs. 15,000

(b) Rs. 90,000

(c) Rs. 12,000

(d) Rs. 3,000

Answer: A

Question: How is the sacrificing ratio determined?

(a) Old ratio – New ratio

(b) New ratio – old ratio

(c) Old ratio + New ratio

(d) None of the above

Answer: A

U, V and W are partners sharing profits in the ratio of 2:2:1. They decided to share future profits in the ratio 5:3:2. On that date the profit and loss account showed the credit balance of Rs. 90,000. Instead of closing the profit and loss account, it was decided to record an adjustment entry reflecting the change in profit sharing ratio They also decide to record the effect of the following revaluations and reassessments without affecting the bookvalues of assets and liabilities by passing a single adjustment entry:

Question: Record an adjustment entry reflecting the change in profit sharing ratio when the profit and loss account is not closed

(a) Dr.W capital a/c Rs.9,000 and Cr.U capital a/c Rs.9,000

(b) Dr.U capital a/c Rs.9,000 and Cr.V capital a/c Rs.9,000

(c) Dr.V capital a/c Rs. 90,000 and Cr.U capital a/c Rs.90,000

(d) Dr.W capital a/c Rs. 90,000 and Cr.V capital a/c Rs.90,000

Answer: B

Question:The single adjustment entry on revaluations and reassessments without affecting the bookvalues of assets and liabilities will be

(a) Dr.W capital a/c Rs.3,000 and Cr.U capital a/c Rs.3,000

(b) Dr.U capital a/c Rs.3,000 and Cr.V capital a/c Rs.3,000

(c) Dr.V capital a/c Rs. 30,000 and Cr.U capital a/c Rs.30,000

(d) Dr.W capital a/c Rs. 30,000 and Cr.V capital a/c Rs.30,000

Answer: B

Question: In case of change in profit-sharing ratio, the gaining partner must compensate the sacrificing partners by paying the proportional amount of

(a) Capital

(b) Cash

(c) Goodwill

(d) None of the above

Answer: C

Question: Calculate U’s gain or sacrifice.

(a) 1/10(sacrifice)

(b) 1/10(gain)

(c) 1/30(Gain)

(d) 1/30(sacrifice)

Answer: B

R, S and T are sharing profits and losses in the ratio of 1:2:3, decided to share future profit and losses equally. The sacrificing and gaining ratio was calculated. The asset and liabilities were revalued and reassessed respectively. The Capital accounts of partners was prepared.

Answer the following questions:

Question: The ratio in which a partner receives a rise in his share of profits is known as:

(a) New Ratio

(b) Sacrificing Ratio

(c) Capital Ratio

(d) Gaining Ratio

Answer: D

Question: The ratio in which a partner surrenders his share in favour of a partner is known as:

(a) New profit-sharing ratio

(b) Sacrificing Ratio

(c) Gaining Ratio

(d) Capital Ratio

Answer: B

Question: Increase and decrease in the value of assets and liabilities are recorded through

(a) Partners' Capital Account

(b) Revaluation Account

(c) Profit and Loss Appropriation Account

(d) Balance Sheet

Answer: B

Question: Partner's capital account is credited when there is

(a) Profit on revaluation

(b) Transfer of general reserve

(c) Transfer of accumulated profits

(d) All of the above

Answer: D

Case Based Question :

Ajay & Vijay were started the business of Air purifiers .Their capitals contributions were Rs. 50,00,000 and Rs.20,00,000 respectively and they decided to share the profit and loss in the

firm as 3:2 . As the demand of Air Purifiers increased ,they decided to expand their business.They did not want to introduce additional capital . To meet the need of further capital , they gave consent for admission of new partner ‘Sanjay’ .He was agreed to contribute capital of Rs.30,00,000 for 1/6th share and to bring sufficient amount of Goodwill. Goodwill was valued at 3 years’ purchase of Average profits of previous 4 years .The previous four years profits are I- Rs. 5,00,000 ; ll – Rs. 4,00,000 ; lll – Rs. 3,00,000 : lV – Rs.4,00,000. Based on the above information ,you are required to answer the following questions :-

Question. What is the amount of Goodwill brought by Sanjay ?

(a) Rs.2,00,000

(b) Rs.3,00,000

(c) Rs. 4,00,000

(d) Rs. 5,00,000

Answer : A

Question. What will be the correct entry for withdrawal of premium for Goodwill, brought in by Sanjay ?

(a) Ajay ‘s Capital A/c …Dr. XX Vijay ‘s Capital A/c …Dr. XX To Sanjay ‘s Capital A/c XX

(b) Ajay ‘s Capital A/c …Dr .XX Vijay ‘s Capital A/c …Dr .XX To Cash A/c XX

(c) Premium for Goodwill A/c…Dr. XX To Ajay ‘s Capital A/c XX To Vijay ‘s Capital A/c XX

(d) Cash A/c……Dr. XX To Ajay ‘s Capital A/c XX To Vijay ‘s Capital A/c XX.

Answer : B

Question. What is the new profit sharing ratio of Ajay , Vijay and Sanjay after Sanjay’s admission ?

(a) 3 : 2 : 1

(b) 5 : 4 : 1

(c) 1 : 1 : 1

(d) 5 : 4 : 1

Answer : A

Question. What is the value of Goodwill of the firm ?

(a) Rs. 3,00,000

(b) Rs. 12,00,000

(c) Rs. 13,00,000

(d) Rs. 14,00,000

Answer : B

CASE STUDEY BASED QUESTIONS

X, Y and Z who are sharing profits in the ratio of 5 : 3 : 2, decide to share profits in the ratio of 2 : 3 : 5 with effect from 1st April, 2019. Workmen Compensation Reserve appears at Rs.1,20,000 in the Balance Sheet as at 31st March, 2019.

Question: Workmen Compensation Claim is estimated at Rs.80,000.

(a) Debited to Revaluation A/c Rs.80,000

(b) Credited to Revaluation A/c Rs. 1,20,000

(c) Shown on Liability side of the Balance Sheet Rs.1,20,000

(d) Credited to Partners Capital A/c Rs.40,000

Answer: D

Question: Workmen Compensation Claim is estimated at Rs.1,50,000.

(a) Debited to Revaluation A/c Rs.1,50,000

(b) Credited to Revaluation A/c Rs.1,20,000

(c) Shown on Liability side of the Balance Sheet Rs.1,50,000

(d) Credited to Partners Capital A/c Rs.1,20,000

Answer: C

Question: Workmen Compensation Claim is estimated at Rs.1,30,000.

(a) Debited to Revaluation A/c Rs.10,000

(b) Credited to Revaluation A/c Rs. 1,30,000

(c) Shown on Liability side of the Balance Sheet Rs.1,20,000

(d) Credited to Partners Capital A/c Rs.10,000

Answer: A

Question: There is no Workmen Compensation Claim

(a) Debited to Revaluation A/c Rs.1,20,000

(b) Credited to Revaluation A/c Rs. 1,20,000

(c) Shown on Liability side of the Balance Sheet Rs.1,20,000

(d) Credited to Partners Capital A/c Rs.1,20,000

Answer: D

Ashish, Aakash and Amit are partners sharing profits and losses equally. The Balance Sheet as at 31st March, 2019 was as follows:

The partners decided to share profits in the ratio of 2 : 2 : 1 w.e.f. 1st April, 2019. They also decided that: Answer the following questions:

Question: Value of machinery to be decreased by 10%. a) Debit Revaluation a/c Rs.25,000

b) Credit Revaluation a/c Rs.1,25,000

c) Machinery will be shown in Balance Sheet Rs.25,000

d) Credit Revaluation a/c Rs.25,000

Answer: A

Question: Land and Building to be appreciated by Rs. 62,000.

a) Debit Revaluation a/c Rs.62,000

b) Credit Revaluation a/c Rs.62,000

c) Land and Building will be shown in Balance Sheet Rs.62,000

d) Credit Revaluation a/c Rs.4,62,000

Answer: B

Question: Value of stock to be reduced to Rs. 1,25,000.

a) Debit Revaluation a/c Rs.15,000

b) Credit Revaluation a/c Rs.15,000

c) Stock will be shown in Balance Sheet Rs.15,000

d) Credit Revaluation a/c Rs.1,25,000

Answer: A

Question: Provision for Doubtful Debts to be made @ 5% on Sundry DebtoRs.

a) Debit Revaluation a/c Rs.4,000

b) Credit Revaluation a/c Rs.4,000

c) Sundry Debtors will be shown in Balance Sheet Rs.84,000

d) Debit Revaluation a/c Rs.40,000

Answer: A

A, B and C are partners sharing profits and losses in the ratio of 5 : 4 : 1. they decided to change their future profit-sharing ratio and agreed upon C acquiring 1/10th share of A and 1/2 share of B.

Question: Calculate A’s sacrifice

(a) 7/20

(b) 5/20

(c) 1/20

(d) 4/20

Answer: C

Question: Calculate C’s gain

(a) 7/20

(b) 5/20

(c) 1/20

(d) 4/20

Answer: B

Question: Calculate New Profit Sharing Ratio

(a) 7:4:9

(b) 4:9:7

(c) 4:7:9

(d) 9:4:7

Answer: D

Question:Calculate B’s sacrifice

(a) 7/20

(b) 5/20

(c) 1/20

(d) 4/20

Answer: D

Jatin, Vimal and Kumar are partners sharing profits equally and decide to share profits in the ratio of 3 : 2 : 1 w.e.f. 1st April, 2019. Their existing agreement came to an end and a new agreement came into existence. They computed the sacrifice and gain made by each partner.

Question: Why is it important to compute the sacrifice and gain made by each partner at the time of change in profit sharing ratio.

a. Because sacrificing partner compensates the gaining partner

b. Because gaining partner compensates the sacrificing partner

c. Both a. and b.

d. None of the above

Answer: B

Question: A change in profit sharing ratio amounts to

a. Dissolution of a firm

b. Dissolution of partnership

c. Both a. and b.

d. None of the above

Answer: B

Question: At the time of change in profit sharing ratio between partners in the case, whose share of profit is not affected.

a. J

b. V

c. K

d. J and K

Answer: B

Question: At the time of change in profit sharing ratio between partners, which statement is true.

a. The gain made by one/more partner/s equals the sacrifice made by another/other partners

b. The gain made by one/more partner/s less than the sacrifice made by another/other partners

c. The gain made by one/more partner/s more than the sacrifice made by another/other partners

d. None of the above is true

Answer: A

Raja and Suraj were partners sharing Profit and Losses in 3 : 2 with affect from 1st April 2021, they decided to share future profits equally. The goodwill was adjusted at the time of change in profit sharing ratio between partneRs.

Question: Which partner’s capital account is debited at the time of adjusting goodwill through capital accounts?

a. Gaining partner’s capital account

b. Sacrificing partner’s capital account

c. All partner’s capital account

d. None of the above

Answer: A

Question: State the need for treatment of goodwill on change in profit sharing ratio.

a. The gaining partner is required to compensate the sacrificing partner.

b. The sacrificing partner is required to compensate the gaining partner.

c. Both a. and b.

d. None of the above

Answer: A

Question: Goodwill can be recorded in the books only when

a. It is internally generated

b. It is purchased

c. Both a. and b.

d. None of the above

Answer: B

Question: In which ratio is goodwill already existing in the books of account written-off?

a. Sacrificing ratio

b. New ratio

c. Old ratio

d. Gaining ratio

Answer: C

A,B and C are partners sharing profits and losses in the ratio of 5:4:1. C acquires 1/5th share from A. There is an accumulated profit or losses of Rs.90,000. The assets have to be revalued and liabilities reassessed. They decided not to record the revised values of assets and liabilities in the books.

Question: Revaluation account is prepared …………… the value of assets.

a. To revise

b. Not to revise

c. To distribute

d. None of these

Answer: A

Question: The steps to be followed in case of change in profit sharing ratio, when revised values are not to be recorded in the books are

1. Pass a single adjustment entry

2. To find share of sacrifice/gain of partners

3. Calculation of the net effect of revaluation

4. Calculation of proportional amount of net effect of revaluation.

The options are

a. 2,3,4,1

b. 3,2,4,1

c. 4,3,2,1

d. None of these

Answer: B

Question: In case of change in profit sharing ratio, the question is silent, then accumulated profit or losses of Rs.90,000 are

a. Distributed

b. Not distributed

c. Adjusted

d. None of these

Answer: A

Question: Calculate new profit sharing ratio

a. 5:4:2

b. 5:4:1

c. 3:4:3

d. None of these

Answer: C

CHAPTER – II

RECONSTITUTION OF PARTNERSHIP

(CHANGE IN PROFIT SHARING RATIO AMONG THE EXISTING PARTNERS,ADMISSION OF A PARTNER, RETIREMENT/DEATH OF A PARTNER)

Admission of a Partner

Learning objectives:-

After studying this lesson, the students will be able to:

* Identify and deal effectively with the situation of reconstitution of partnership.

* Identify the problem arising due to admission of a partner in the firm.

* Calculate new and sacrifice ratio in different cases.

* Understand, calculate and make treatment of goodwill in different cases.

* Make accounting treatment of the revaluation of assets and liabilities and distribute the

profit and loss on revaluation among the old partners.

* Make accounting treatment of unrecorded assets and liabilities

* Prepare capital Accounts, Cash A/c and Balance Sheet of the New firm

* Adjust the Partners‘ Capital Accounts

Salient Points:-

1. Goodwill is the monetary value of business reputation. It is an intangible asset.

2. Goodwill may be of two types:

a. Purchased goodwill

b. Non-purchased goodwill

3. When existing firm faces problem of limited financial resources and man power then one new additional partner enters into firm.

4. There are three methods of valuation of goodwill:

a. Average Profit Method

b. Super Profit method

c. Capitalisation Method

5. When new partner is admitted into existing partnership then existing partners have to sacrifice in favour of new partner, it is called sacrificing ratio.

6. Share of goodwill of new partner will be credited to sacrificing partners into their

Question: At the time of change in profit sharing ratio among the existing partners, where will you record an unrecorded liability?

CASE STUDY BASED QUESTIONS

A, B and C are partners sharing Profit and losses in the ratio 3:2:1. From 1st April 2018, A,B and C decided to share profit and losses equally. This may result in the gain to a few partners and loss to othe Rs.

Question: As there is a change in profit sharing ratio. Which of the following is calculated?

a. Sacrificing ratio

b. Gaining ratio

c. Both a. and b.

d. None of the above

Answer: C

Question: From 1st April 2018, A,B and C decided to share profit and losses equally. It is a

a. Revaluation of the firm

b. Dissolution of the firm

c. Reconstitution of the firm

d. None of the above

Answer: C

Question: What is the formula of Gaining Ratio.

a. Gaining Ratio = Old ratio – New ratio

b. Gaining Ratio = Old ratio +New ratio

c. Gaining Ratio = New ratio – Old ratio

d. None of the above

Answer: C

Question: What is the formula of Sacrificing Ratio.

a. Sacrificing ratio = Old ratio – New ratio

b. Sacrificing ratio = Old ratio +New ratio

c. Sacrificing ratio = New ratio – Old ratio

d. None of the above

Answer: A

Tina and Mira were partners sharing Profit and Losses in 5 : 2 with affect from 1st April 2021, they decided to share future profits equally. There was an unrecorded liability and an unrecorded asset. Expenses were incurred by the firm to give effect to the change in profit sharing ratio. The partner Tina had to be paid remuneration for the services rendered by her relating to reconstitution of the firm .

Question: When expenses were to be borne by Tina but are paid by the firm, which of the following journal is correct.

a. Revaluation a/c Dr.; Tina’s capital a/c Cr.

b. Tina’s capital a/c Dr.; Cash/Bank a/c Cr.

c. Cash/Bank a/c Dr.; Tina’s capital a/c Cr

d. None of these

Answer: B

Question: When expenses are incurred and paid by the firm, which of the following journal is correct.

a. Revaluation a/c Dr.; Tina’s capital a/c Cr.

b. Tina’s capital a/c Dr.; Cash/Bank a/c Cr.

c. Revaluation a/c Dr.; Cash/Bank a/c Cr.

d. None of these

Answer: C

Question: When remuneration is paid by the firm to Tina and expenses are borne by the firm, which of the following journal is correct.

a. Revaluation a/c Dr. ; Tina’s capital a/c Cr.

b. Tina’s capital a/c Dr.; Revaluation a/c Cr.

c. Cash a/c Dr.; Tina’s capital a/c Cr.

d. None of these

Answer: A

Question: Unrecorded liabilities and Unrecorded assets are recorded in

a. Revaluation a/c ;where they are credited and debited respectively

b. Revaluation a/c ;where they are debited and credited respectively

c. Partners capital a/c ; where they are credited and debited respectively

d. Partners capital a/c ; where they are credited and debited respectively

Answer: B

X, Y and Z are sharing profits and losses in the ratio of 3 : 2 : 1. They decide to share future profits and losses in the ratio of 5 : 3 : 2 with effect from 1st April, 2019. On this date, the Balance sheet showed Contingency Reserve Rs. 9,000 and Deferred Advertisement Expenditure Rs.30,000.

Goodwill was valued at Rs. 4,80,000.

Question: What is the journal entry for Contingency Reserve Rs. 9,000

a. Dr. Contingency Reserve a/c Rs.9,000; Cr. X Capital a/c Rs.4,500; Cr. Y Capital a/c Rs.3,000; Cr. Z Capital a/c Rs. 1,500

b. Dr. Contingency Reserve a/c Rs.9,000; Cr. X Capital a/c Rs.4,500; Cr. Y Capital a/c Rs.2,700; Cr. Z Capital a/c Rs. 1,800

c. Dr. Z Capital a/c Rs.300; Cr. Y Capital a/c Rs.300

d. None of the above

Answer: A

Question: What is the journal entry for Deferred Advertisement Expenditure Rs.30,000

a. Dr. X Capital a/c Rs.15,000; Dr. Y Capital a/c Rs.10,000; Dr. Z Capital a/c Rs.5,000; Cr. Deferred Advertisement Expenditure a/c Rs. 30,000

b. Dr. X Capital a/c Rs.15,000; Dr. Y Capital a/c Rs.9,000; Dr. Z Capital a/c Rs.6,000; Cr. Deferred Advertisement Expenditure a/c Rs. 30,000

Page 29 of 152

c. Dr. Z Capital a/c Rs.10,000; Cr. Y Capital a/c Rs.10,000

d. None of the above

Answer: A

Question: The partner(s) whose share will be unaffected

a. Y

b. Z

c. X

d. Z and Y

Answer: C

Question: What is the journal entry for Goodwill was valued at Rs. 4,80,000.

a. Dr Goodwill a/c Rs. 16,000; Cr. Y Capital a/c Rs. 16,000

b. Dr. Y Capital a/c Rs. 16,000; Cr. Z Capital a/c Rs. 16,000

c. Dr. Z Capital a/c Rs. 16,000; Cr. Y Capital a/c Rs.16,000

d. None of the above

Answer: C

R, K and S are sharing profits and losses in the ratio of 5 : 4 : 1. They decide to share future profits and losses in the ratio of 1 : 4 : 5 with effect from 1st April, 2019. On that date, they revalued their assets and reassessed their liabilities. They had an unrecorded asset.

Question: Revaluation of assets is necessary because their present value may be different from their ………………………..

a. Book value

b. Market value

c. Both a. and b.

d. None of the above

Answer: A

Question: Revaluation a/c is a

a. Real a/c

b. Nominal a/c

c. Personal a/c

d. None of the above

Answer: B

Question: The partner(s) who will share Gain or loss on revaluation are

a. R,K,S

b. Both R and S

c. Only S

d. Only R

Answer: A

Question: What is unrecorded asset?

a. Assets which physically exist but not shown in the Balance sheet

Page 30 of 152

b. Assets which physically do not exist and not shown in the Balance sheet

c. Assets which physically exist but shown in the Balance sheet

d. None of the above

Answer: A

A and B are partners in a firm sharing profits in the ratio of 2 : 1. They decided with effect from 1st April, 2018, that they would share profits in the ratio of 3 : 2. But, this decision was taken after the profit for the year ended 31st March, 2019 of Rs. 90,000 was distributed in the old ratio.

Firm’s goodwill was valued on the basis of aggregate of two years profits preceding the date decision became effective.

The profits for the year ended 31st March, 2017 and 2018 were Rs. 60,000 and Rs. 75,000 respectively. It was decided that Goodwill Account will not be opened in the books of the firm and necessary adjustment be made through Capital Accounts which on 31st March, 2019 stood at Rs. 1,50,000 for A and Rs. 90,000 for B.

Question: Adjustment of goodwill made on change in profit sharing ratio, the journal entry is

a. Dr. A’s Capital A/c Rs.9,000; Cr. B’s Capital A/c Rs. 9,000

b. Cr. A’s Capital A/c Rs.9,000 ;Dr. B’s Capital A/c Rs. 9,000

c. Dr. A’s Capital A/c Rs.1,35,000; Cr. B’s Capital A/c Rs. 1,35,000

d. Cr. A’s Capital A/c Rs. 1,35,000; Dr. B’s Capital A/c Rs. 1,35,000

Answer: B

Question: In adjustment of profit for 2018-19 on change in profit sharing ratio, the journal entry is

a. Dr. A’s Capital A/c Rs.6,000; Cr. B’s Capital A/c Rs. 6,000

b. Cr. A’s Capital A/c Rs.6,000; Dr. B’s Capital A/c Rs. 6,000

c. Dr. A’s Capital A/c Rs.90,000 ;Cr. B’s Capital A/c Rs. 90,000

d. Cr. A’s Capital A/c Rs.90,000; Dr. B’s Capital A/c Rs. 90,000

Answer: A

Question: What is the closing balance of Partners Capital accounts?

Page 31 of 152

a. A-Rs.1,53,000; B-Rs.87,000

b. A-Rs.1,59,000; B-Rs.96,000

c. A-Rs.1,44,000; B-Rs.81,000

d. A-Rs.1,24,000; B-Rs.89,000

Answer: A

Question: Calculate New Goodwill.

a. Rs. 60,000

b. Rs. 75,000

c. Rs. 1,35,000

d. Rs. 67,500

Answer: C

Amar and Akbar are partners sharing profits in the ratio of 2 : 1. On 31st March, 2019, their Balance Sheet showed General Reserve of Rs. 60,000. It was decided that in future they will share profits and losses in the ratio of 3 : 2.

Question: When General Reserve is to be shown in the new Balance Sheet. Pass necessary Journal entry.

a. Dr. General Reserve A/c Rs. 60,000; Cr. Amar’s Capital A/c Rs.40,000; Cr. Akbar’s Capital A/c Rs.20,000

b. Dr. Amar’s Capital A/c Rs.40,000; Dr. Akbar’s Capital A/c Rs.20,000; Cr. General Reserve A/c Rs. 60,000

c. Cr. Amar’s Capital A/c Rs.4,000; Dr. Akbar’s Capital A/c Rs.4,000

d. None of the above

Answer: C

Question: When General Reserve is not to be shown in the new Balance Sheet. Pass necessary Journal entry.

a. Dr. General Reserve A/c Rs. 60,000; Cr. Amar’s Capital A/c Rs.40,000; Cr. Akbar’s Capital A/c Rs.20,000

b. Dr. Amar’s Capital A/c Rs.40,000; Dr. Akbar’s Capital A/c Rs.20,000; Cr. General Reserve A/c Rs. 60,000

c. Cr. Amar’s Capital A/c Rs.60,000; Dr. Akbar’s Capital A/c Rs.60,000

d. None of the above

Answer: A

Question: Calculate the sacrificing share?

a. 1/15

b. 2/15

c. 1/30

d. None

Answer: A

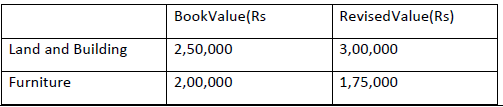

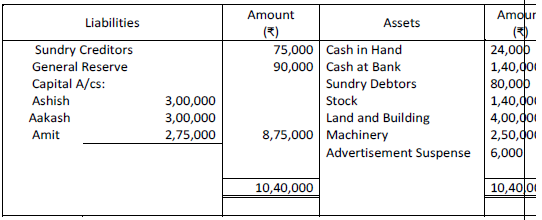

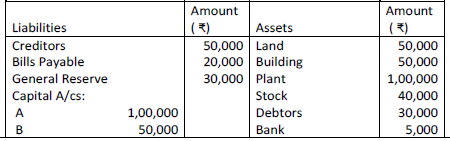

A, B and C were partners in a firm sharing profits in the ratio of 3 : 2 : 1. Their Balance Sheet as on 31st March, 2015 was as follows:

From 1st April, 2015, A, B and C decided to share profits equally. For this it was agreed that: (i) Goodwill of the firm will be valued at Rs. 1,50,000. (ii) Land will be revalued at Rs. 80,000 and building be depreciated by 6%. (iii) Creditors of Rs. 6,000 were not likely to be claimed and hence should be written off.

Answer the following questions:

Question: What will be the Land value shown in new Balance sheet?

a. Rs. 30,000

b. Rs. 50,000

c. Rs. 80,000

d. Rs. 1,30,000

Answer: C

Question: Calculate the gain on Revaluation?

a. Rs. 33,000

b. Rs. 36,000

c. Rs. 30,000

d. None of the above

Answer: A

Question: What will be the journal entry for Goodwill?

a. Dr. C’s capital a/c Rs.25,000; Cr. A’s capital a/c Rs. 25,000

b. Cr. C’s capital a/c Rs.25,000; Dr. A’s capital a/c Rs. 25,000

c. Dr. C’s capital a/c Rs.1,50,000; Cr. A’s capital a/c Rs. 1,50,000

d. Cr. C’s capital a/c Rs.1,50,000; Dr. A’s capital a/c Rs. 1,50,000

Answer: A

Question: What will be the Creditors value shown in new Balance sheet?

a. Rs. 44,000

b. Rs. 50,000

c. Rs. 56,000

d. Rs. 6,000

Answer: A

Free study material for Accountancy

HOTS for Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Accountancy Class 12

Students can now practice Higher Order Thinking Skills (HOTS) questions for Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner to prepare for their upcoming school exams. This study material follows the latest syllabus for Class 12 Accountancy released by CBSE. These solved questions will help you to understand about each topic and also answer difficult questions in your Accountancy test.

NCERT Based Analytical Questions for Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner

Our expert teachers have created these Accountancy HOTS by referring to the official NCERT book for Class 12. These solved exercises are great for students who want to become experts in all important topics of the chapter. After attempting these challenging questions should also check their work with our teacher prepared solutions. For a complete understanding, you can also refer to our NCERT solutions for Class 12 Accountancy available on our website.

Master Accountancy for Better Marks

Regular practice of Class 12 HOTS will give you a stronger understanding of all concepts and also help you get more marks in your exams. We have also provided a variety of MCQ questions within these sets to help you easily cover all parts of the chapter. After solving these you should try our online Accountancy MCQ Test to check your speed. All the study resources on studiestoday.com are free and updated for the current academic year.

FAQs

You can download the teacher-verified PDF for CBSE Class 12 Accountancy HOTs Admission Of A Partner from StudiesToday.com. These questions have been prepared for Class 12 Accountancy to help students learn high-level application and analytical skills required for the 2026-27 exams.

In the 2026 pattern, 50% of the marks are for competency-based questions. Our CBSE Class 12 Accountancy HOTs Admission Of A Partner are to apply basic theory to real-world to help Class 12 students to solve case studies and assertion-reasoning questions in Accountancy.

Unlike direct questions that test memory, CBSE Class 12 Accountancy HOTs Admission Of A Partner require out-of-the-box thinking as Class 12 Accountancy HOTS questions focus on understanding data and identifying logical errors.

After reading all conceots in Accountancy, practice CBSE Class 12 Accountancy HOTs Admission Of A Partner by breaking down the problem into smaller logical steps.

Yes, we provide detailed, step-by-step solutions for CBSE Class 12 Accountancy HOTs Admission Of A Partner. These solutions highlight the analytical reasoning and logical steps to help students prepare as per CBSE marking scheme.