Download the latest CBSE Class 12 Business Studies Financial Management Notes Set 01 in PDF format. These Class 12 Business Studies revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Business Studies Chapter 9 Financial Management

To secure a higher rank, students should use these Class 12 Business Studies Chapter 9 Financial Management notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Chapter 9 Financial Management Revision Notes for Class 12 Business Studies

Introduction :-

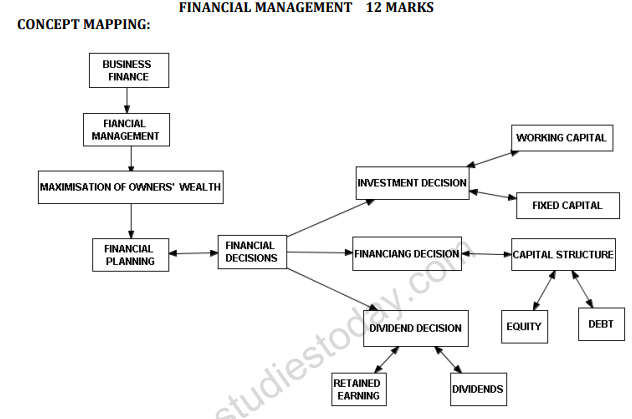

Money required for carrying out business activities is called business finance. Finance is needed to establish a business, to run it, to modernise, it to expand or diversify it. Finanicial management is the activity concerned with the planning, raising controlling and dministering of funds used in the business. It is concerned with optimal procurement as well as usuage of finance. It aims at ensuring availability of enough funds whenever required as well as avoiding idle finance.

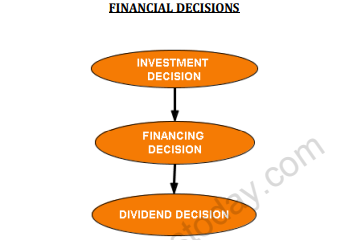

The Main Objective of Financial Management : is to maximise shareholder’s wealth, for which achievement of optimum capital structure and proper utilisation of funds is a must. Every company is required to take three main financial decisions which are as follow

1. Investment Decision :-

It relates to how the firm’s funds are invested in different assets. Investment decision can be long-term or short term. A long term investment decision is called capital budgeting decisions which involve huge amounts of investments and are irreversible except at a huge cost while short term investment decisions are called working capital decisions which affect day to day working of a business.

2. Financing Decison :-

It relates to the amount of fincance to be raised from various long term sources. The main sources of funds are owner’s funds i.e. equity / share holder’s funds and the borrowed funds i.e. Debts. Borrowed funds have to be repaid at a fixed time and thus some amount of financial risk (i.e. risk of default on payment) is there in debt financing. Morever interest on borrowed funds have to be paid regardless of whether or not a firm has made a profit. On the other hand shareholder funds involve no commitment regarding payment of returns or repayment of capital. A firm mixes both debt and equity in making financing decisions.

3. Dividend Decision :-

Dividend refers to that part of the profit which is distributed to shareholders. A company is required to decide how much of the profit earned by it should be distributed among shareholders and how much should be retained. The decision regarding dividend should be taken keeping in view the overall objective of maximising shareholder’s wealth.

Financial Planning :-

The process of estimating the fund requirement of a business and specifying the sources of funds is called financial planning. It ensure that enough funds are available at right time so that a firm could honour its commitments and carry out, its plans.

Importance of Financial Planning

1. To ensure availbility of adequate funds at right time.

2. To see that the firm does not raise funds unnecessarily.

Factors affecting Investment Decisions / Capital Budgeting decisions

1. Cash flows of the project : The series of cash receipts and payments over the life of an investment proposal should be considered and analysed for selecting the best proposal.

2. Rate of Return : The expected returns from each proposal and risk involved in them should be taken into account to select the best proposal.

3. Investment Criteria Involved : The various investment proposals are evaluated on the basis of capital budgeting techniques. Which involve calculation regarding investment amount, interest rate, cash flows, rate of return etc.

Factors Affecting Financing Decision

1. Cost :- The cost of raising funds from different sources are different. The cheapset source should be selected.

2. Risk :- The risk associated with different sources is different, More risk is associated with borrowed funds as compared to owner’s fund as interest is paid on it and it is rapaid also.

3. Floatation Cost :- The cost involved in issuing securities such as broker’s commission, underwriters fees, expenses on prospectus etc is called floatation cost. Higher the floatation cost, less attractive is the source of finance.

4. Cash flow position of the business :- In case the cash flow position of a company is good enough then it can easily use borrowed funds.

5. Control Considerations : In case the existing shareholders want to retain the complete control of business then finance can be raised through borrowed funds but when they are ready for dilution of control over business, equity can be used for raising finance.

6. State of Capital Markets : - During boom, finance can easily be raised by issuing shares but during depression period, raising finance by means of debt is easy.

Factors affecting Dividend Decision :

1. Earnings : - Company having high and stable earning could declare high rate of dividends are paid out of current and past earnings.

2. Stability od Dividends : Companies generally follow the policy of stable dividend. The dividend per share is not altered/changed in case earning changes by small proportion or increase in earning is temporary in nature.

3. Growth Prospects : In cse there are growth prospects for the company in the near future them it will retain its earning and thus, no or less dividend will be declared.

4. Cash Flow Positions : Dividends involve an outflow of cash and thus, availability of adequate cash is foremost requirement for declaration of dividends.

5. Preference of Shareholders : While deciding about divident the preference of shareholders is also taken into account. In case shareholders desire for dividend then company may go for declaring the same.

6. Taxation Policy : A company is required to pay tax on dividend declared by it. If tax on dividend is higher, company will prefer to pay less by way of dividends whereas if tax rates are lower then more dividends can be declared by the company.

Capital Structure

Capital structure refers to the mix between owner’s funds and borrowed funds. It will be said to be optimal when the proportion of debt and equity is such that it results in an increase in the value of the equity share.

The proportion of debt in the overall capital of a firm is called financial Leverage or capital gearing. When the proportion of debt in the total capital is high then the firm will be called highly levered firm but when the proportion of debts in the total capital is less then the firm will be called low levered firm.

Factors affecting Capital Structure.

1. Cash flow position : In case a company has strong cash flow position then it may raise finance by issuing debts.

2. Interest Coverage Ratio : If refers to the number of times earning before interest and taxes of a company covers the interest obligation. High Interest coverage ratio indicate that company can have more of borrowed funds.

3. Return on Investment : If return on investment is higher than the rate of interest on debt then it will be beneficial for a firm to raise finance through borrowed funds.

4. Floatation Cost : The cost involved in issuing securities such as brokers comission, under writers fees, cost of prospectus etc is called floatation cost. While selecting the source of finance floatation cost should be taken into account.

5. Control : When existing shareholders are ready to dilute their control over the firm then new equity shares can be issued for raising finance but in reverse sitation debts should be used.

6. Tax Rate : Interest on debt is allowed as a deduction, thus in case of high tax rate debts are prefered over equity but in case of low tax rate more preference is given to Equity.

In addition, cost of debt, cost of equity flexibility, risk consideration etc are other factors affecting capital structure.

Fixed Capital and Factors affecting Fixed Capital

Fixed capital refers to investment in long-term assets. Investment in fixed assets is for longer duration and they must be financed through long-term sources of capital. Decisions relating to fixed capital involve huge capital/ funds and are not reversible without incurring heavy losses. The factorsaffecting the requirement of fixed capital are the follows.

1. Nature of Business : Manufacturing concern require huge investment in fixed assets & thus huge fixed capital is required for them but trading concern needs less fixed capital as they doesn’t require to purchase plant and machinery etc.

2. Scale of Operations : An organisation operating on large scale require more fixedd capital as compare to an organisation operating on small scale.

3. Choice of Technique : An organisation using capital intensive techniques require more investment in plant & machinery as compare to organisation using labour intensive techniques.

4. Technology upgradation : Organisations using assets which become obsolete faster require more fixed capital as compare to other organisations.

5. Growth Prospects : Companies having higher growth plan require more fixed capital. In order to expand production capacity more plant & machinery are required.

6. Diversification : In case a company go for diversification then it will require more fixed capital to invest in fixed assets like plant and machinery.

Working Capital and Factors affecting working capital

Working Capital refers to the capital required for day to day working of an organisation. Apart from the investment in fixed assets every business organisation needs to invest in current assets, which can be converted into cash or cash equivalents within a period of one year. They provide liquidity to the business. Working capital is of two types : Gross working capital

and Net working capital Investment in all the current assets is called gross working capital whereas the excess of current assets over current liabilities is called net working capital. Following are the factors which affect working capital requirements of an organisation.

1. Nature of Business : A trading organisation needs a lower amount of working capital as compared to a manufacturing organisation as trading organisation undertake no processing work.

2. Scale of operations : - An organisation operating on large scale wille require more inventory and thus, its working requirement will be more as compared to small organisation.

3. Business Cycle ; In the time of boom more production will be undertaken and so more working capital will be required during that time as compared to depression.

4. Seasonal Factors : During peak season demand of a product will be high and thus high working capital will be required as compared to lean season.

5. Credit allowed : If credit is allowed by a concern to its customers than it will require more working capital but if goods are sold on cash basis than less working capital is required.

6. Credit availed : If a firm is able to purchase raw material on credit from its suppliers then less working capital will be required.

In addition to above growth prospects, operating efficiency, inflation, level of competition etc also affect working capital requirement.

Trading on Equity :

It refers to the increase in profit earned by the equity shareholders due to the presence of fixed financial charges like interest. Trading on equity happen when the rate of earning of an organisation is higher than the cost at which funds have been borrowed and a as result equity shareholders get higher rate of dividend per share.

Key Concepts in nutshell:

Meaning of Business Finance: Money required for carrying out business activities is called business finance.

Financial Management: It is concerned with optimal procurement as well as usage of finance.

Role of Financial Management: It cannot be over‐emphasized, since it has a direct bearing on the financial health of a business. The financial statements such as Profit and Loss A/C and B/S reflect a firm’s financial position and its financial health.

i) The size as well as the composition of fixed assets of the business

ii) The quantum of current assets as well as its break‐up into cash, inventories and receivables used.

iii) The amount of long‐term and short‐term financing to be used.

iv) Break‐ up of long‐term financing into debt, equity etc.

v) All items in the profit and loss account e.g., interest, expenses, depreciation etc.

Objectives of Financial Management: Maximisation of owners’ wealth is sole objective of financial management. It means maximization of the market value of equity shares. Market price of equity share increases if the benefits from a decision exceed the cost involved.

Investment Decision: It relates to how the firm’s funds are invested in different assets . Investment decision can be long‐term or short‐term. A long‐term investment decision is also called a Capital Budgeting decision.

Factors affecting Capital Bud geting Decision/Investment Decision:

1. Cash flows of the project: If anticipated cash flows are more than the cost involved then such projects are considered.

2. The rate of return: The investment proposal which ensures highest rate of return is finally selected.

3. The investment criteria involved: Through capital budgeting techniques, investment proposals are selected.

Financing Decision: It refers to the quantum of finance to be raised from various sources of long‐term of finance. It involves identification of various available sources. The main sources of funds for a firm are shareholders funds and borrowed funds. Shareholders funds refer to equity capital and retained earnings. Borrowed funds refer to finance raised as debentures or other forms of debt.

Factors Affecting Financing Decision:

a) Cost: The cost of raising funds through different sources is different. A prudent financial manager would normally opt for a source which is the cheapest. (b) Risk: The risk asso ciated with different sources is different.

(c) Floatation Costs: Higher the floatation cost, less attractive the source.

(d) Cash Flow Position of the Business: A stronger cash flow position may make debt financing more viable than funding through equity.

(e) Level of Fixed Operating Costs: If a business has high level of fixed operating costs (e.g., building rent, Insurance premium, Salaries etc.), It must opt for lower fixed financing costs. Hence, lower debt financing is better. Similarly, if fixed operating cost is less, more

f) Control Considerations: Issues of more equity may lead to dilution of management’s control over the business. Debt financing has no such implication. Companies afraid of a takeover bid may consequent ly prefer debt to equity.

g) State of Capital Markets: Health of the capital market may also affect the choice of source of fund. During the period when stock market is rising, more people are ready to invest in equity. However, depressed capital market may make issue of equity shares difficult for any company.

DIVIDEND DECISION:The decision involved here is how much of the profit earned by company (after paying tax) is to be distributed to the shareholders and how much of it should be retained in the business for meeting the investment requirements.

FACTORS AFFECTING DIVIDEND DECISION:

a) Earnings: Dividends are paid out of current and past earning. Therefore, earnings is a major determinant of the decision about dividend.

(b) Stability of Earnings: Other things remaining the same, a company having stable earning is in a position to declare higher dividends. As against this, a company having unstable earnings is likely to pay sma ller dividend.

c) Stability of Dividends: It has been found that the companies generally follow a policy of stabilising dividend per share.

(d) Growth Opportunities: Companies having good growth opportunities retain more money out of their earnings so as to finance the required investment.

(e) Cash Flow Position: Dividends involve an outflow of cash. A company may be profitable but short on cash. Availability of enough cash in the company is necessary for declaration of dividend by it.

(f) Shareholder Preference: While declaring dividends, managements usually keep in mind the preferences of the shareholders in this regard.

(g) Taxation Policy: The choice between payment of dividends and retaining the earnings is, to some extent, affected by difference in the tax treatment of dividends and capital gains.

(h) Stock Market Reaction: Investors, in general, view an increase in dividend as a good news and stock prices react positively to it. Similarly, a decrease in dividend may have a negative impact on the share prices in the stock market.

(i) Access to Capital Market: Large and reputed companies generally have easy access to the capital market and therefore may depend less on retained earnings to finance their growth. These companies tend to pay higher dividends than the smaller companies which have relatively low access to the market.

(j) Legal Constraints: Certain provisions of the Company’s Act place restrictions on payouts as dividend. Such provisions must be adhered to while declaring the dividends.

(k) Contractual Constraints: While granting loans to a company, sometimes the lender may impose certain restrictions on the payment of dividends in future.

FINANCIAL PLANNING

Financial Planning is essentially preparation of financial blueprint of an organisations’s future operations. The objective of financial planning is to ensure that enough funds are available at right time.

OBJECTIVES

(a) To ensure availability of fundswhenever these are required: This include a proper estimation of the funds required for different purposes such as for the purchase of long‐term assets or to meet day‐ to‐ day expenses of business etc.

(b) To see that the firm does not raise resources unnecessarily: Excess funding is almost as bad as inadequate funding.

IMPORTANCE OFFINANCIAL PLANNING

(i) It tries to forecast what may happen in future under different business situations. By doing so, it helps the firms to face the eventual situation in a better way. In other words, it makes the firm better prepared to face the future.

(ii) It helps in avoiding business shocks and surprises and helps the company in preparing for the future.

(iii) If helps in co‐ordinating various business functions e.g., sales and production functions, by providing clear policies and procedures.

(iv) Detailed plans of action prepared under financial planning reduce waste, duplication of efforts, and gaps in planning.

(v) It tries to link the present with the future.

(vi) It provides a link between investment and financing decisions on a continuous basis.

(vii) By spelling out detailed objectives for various business segments, it makes the evaluation of actual performance easier.

CAPITAL STRUCTURE: Capital structure refers to the mix between owners and borrowed funds.

FACTORS AFFECTING THE CHOICE OF CAPITAL STRUCTURE

1. Cash Flow Position: Size of projected cash flows must be considered before issuing debt.

2. Interest Coverage Ratio (ICR): The interest coverage ratio refers to the number of times earnings before interest and taxes of a compab ny covers the interest oligation.

3. Debt Service Coverage Ratio(DSCR): Debt Service Coverage Ratio takes care of the deficiencies referred to in the Interest Coverage Ratio (ICR).

Meaning Of Business Finance

The money needed to run business activities is known as business finance. Finances are essential to operate a business, as well as to carry out day to day activities of the business.

Financial Management

Financial Management is focused on the proper sourcing and use of finance. It covers business activities such as getting funds, lowering the cost of funds, managing the risk under control and putting such funds to work.

Financial management includes two aspects, that is finance and management. Hence, Financial management can be described as the use of the management functions, particularly planning and controlling functions in the finance function of the business.

Financial Management is very important as it has a direct effect on the financial health of a business. Financial management decisions touch all the items of the financial statement directly or indirectly.

Role Of Financial Management

- Size and composition of fixed assets: Too much investment in fixed assets may block funds and increase the size of fixed assets which may not be healthy for business whereas, little investment may slow the growth of business.

- The quantum of current assets and its break up into cash, inventory and receivables: The financial decisions about investments in fixed assets, the credit policy, inventory management, etc., shape the amount of working capital needed by a business enterprise.

- The amount of long term and short financing: Financing decision chooses the proportion of funds raised from long term and short term sources.

- Break-up of long-term financing into debt, equity etc: It is important for a financial manager to choose the way by which the proportion of debt and/or equity in a business has to be put in. The decisions of the finance managers touch debt, equity share capital, preference share capital and are an integral part of financing management.

- All items in Profit and Loss account: Financing decisions touch the value of items appearing in the profit and loss account.

Objectives Of Financial Management

- Profit maximization: This was the primary objective of firms which are focused on the increasing earnings per share (EPS) of the company. It is also the traditional objective of the financial management that points to the fact that all the financial efforts should be made to grow the overall profit of the company.

- Wealth Maximization concept:

- 'Owners' of a company are the shareholders.

- The term wealth refers to wealth of owners as shown by the market price of their shares.

- The market price of shares is linked to three basic financial decisions:

- Investment decision

- Financing decision

- Dividend decision

- Market price of a share will rise if benefits from a decision are greater than the cost involved in it.

- The goal of a firm should be to grow the wealth of owners in the long run.

- Increase in the market price of shares is an indicator of the financial health of a firm.

- Other objectives: It helps a firm achieve the primary objective are:

- Ensure availability of funds at reasonable costs.

- Ensure effective use of funds.

- Ensure safety of funds through creation of reserves.

- Maintain liquidity and solvency.

Financial Decisions

The financial functions relate to three major decisions which every finance manager has to take:

- (i) Investment decision

- (ii) Financing decision

- (iii) Dividend decision

I. Investment Decision (Capital Budgeting Decision)

Each and every organization has limited resources in comparison to the uses of the resources. So it is very important for a firm to choose the source in which the funds should be invested in so as to fetch the best returns.

- Investment decisions in an organization are taken in both long term and short term.

- There are two types of decisions:

- Long term investment decisions: These are also called capital budgeting decisions. This also means that the funds are invested in a resource for a longer period of time. These decisions touch the profitability and size of assets.

- Short term investment decision: These are also known as working capital decisions. This also means that the funds are invested in a resource for a shorter period of time. These decisions touch the day to day operations and activities of the organization. It also touches the liquidity and profitability of the business.

- The essential contents in a working capital are:

- Inventory management

- Receivables management and

- Efficient cash management.

Factors Affecting Investment Decisions/Capital Budgeting Decisions

- Cash flows of the project: The series of cash receipts and payments over the life of an investment proposal should be looked at and studied for selecting the best proposal.

- Rate of Return: The expected returns from each proposal and risk involved in them should be looked at to select the best proposal.

- Investment Criteria Involved: The various investment proposals are looked at on the basis of capital budgeting techniques. These include calculation regarding investment amount, interest rate, cash flows, rate of return etc.

II. Financing Decision

- Under this the financial managers of the organization choose the sources from which to raise long-term funds. The main source of funding is shareholders' funds and borrowed funds.

- Shareholders' funds include share capital, reserves and surpluses and retained earnings.

- Borrowed funds refer to funds raised through issue of debentures and other forms of debt.

- The choice of raising funds from various sources in appropriate proportion lies in the hands of the financial managers.

- Interest on loan has to be paid regardless of the profitability of the project.

- Debt is considered to be the cheapest form of finance.

Factors Affecting Financing Decision

- Cost: The cost of raising funds from different sources is different. The cheapest source should be picked.

- Risk: The risk associated with different sources is different. More risk is associated with borrowed funds as compared to the owner's fund as interest is paid on it and it is paid back also, after a fixed period of time or on expiry of its tenure.

- Flotation Cost: The costs involved in issuing securities such as brokers commission, underwriters' fees, expenses on prospectus etc. are called flotation costs. Higher the flotation cost, less attractive is the source of finance.

- Cash flow position of the business: In case the cash flow position of a company is good enough then it can easily use borrowed funds and pay interest on time.

- Control Considerations: In case the existing shareholders want to keep the complete control of business then finance can be raised through borrowed funds but when they are ready for dilution of control over business, equity can be used for raising finance.

- State of Capital Markets: During boom, finance can easily be raised by issuing shares but during the depression period, raising finance by means of debt is easy.

- Period of Finance: For permanent capital requirement, Equity shares must be issued as they are not to be paid back and for long and medium term requirement, preference shares or debentures can be issued.

III. Dividend Decision

- Dividend is that part of profit which has to be shared among the shareholders of a company. This decision relates to the sharing of dividends among various groups. In this choice, it must be decided that:

- If all profits are to be given out,

- Whether all earnings will be kept in the business, or

- Whether a portion of profits will be kept in the business and the remainder shared among shareholders.

Factors Affecting Dividend Decision

- Earnings: Companies having high and stable earnings could declare a high rate of dividends as dividends are paid out of current and past earnings.

- Stability of Dividends: Companies generally follow the policy of stable dividend. The dividend per share is not changed and altered in case earnings change by small proportion or increase in earnings is temporary in nature.

- Growth Prospects: In case there are growth prospects for the company in the near future then it will keep its earnings and thus, no or less dividend will be declared.

- Cash Flow Positions: Dividends involve an outflow of cash and thus, availability of adequate cash is for most requirements for declaration of dividends.

- Preference of Shareholders: While deciding about dividend the preference of shareholders is also looked at. In case shareholders desire a dividend then the company may go for declaring the same.

- Taxation Policy: A company is needed to pay tax on the dividend declared by it. If tax on dividends is higher, companies will prefer to pay less by way of dividends whereas if tax rates are lower, more dividends can be declared by the company.

- Issue of bonus shares: Companies with large reserves may also share bonus shares to grow their capital base as it shows growth of the company and improves its reputation also.

- Legal constraints: Under provisions of Companies Act, all earnings can't be shared and the company has to provide for various reserves. This limits the capacity of the company to declare a dividend.

Financial Planning

It means choosing in advance how much to spend, on what to spend according to the funds at your disposal.

Objectives Of Financial Planning

- To ensure availability of funds whenever these are needed.

- To see that the firm does not raise resources unnecessarily.

Importance Of Financial Planning

- Forecasting: It helps in forecasting the future under different circumstances. This helps the firms and organizations in dealing with contingencies.

- Prepares for uncertainties: It helps in preparing firms for various future ventures by avoiding business shocks and surprises.

- Coordination: It helps in better coordination of various business functions like production, sales, etc.

- Building links: It builds a link between the present of the organization with its future. It also gives a link between the financing and investment decisions on a regular basis.

- Easy Performance Evaluation: It makes the evaluation of the performance easier and in a detailed way.

Capital Structure

- On the basis of ownership, funds = owners funds + borrowed funds.

- Owners funds = equity share capital + preference share capital + reserves and surpluses + retained earnings = EQUITY

- Borrowed funds = loans + debentures + public deposits = DEBT

- Capital Structure = The mix of long-term sources of funds

- Refers to the proportion of debt and equity used for financing the operations of a business.

- Cost and risk- Debt vs Equity

- Cost of Debt is lower than the cost of equity but Debt is more risky than equity.

- Cost of debt < cost of equity as lenders risk < owners risk.

- Lender earns an assured interest and repayment of capital.

- Interest on debt is a tax deductible expense so brings down the tax liability for a business whereas dividends are paid out of profit after tax.

- Debt is more risky for the business as it adds to the financial risk faced by a business.

- Any default w.r.t payment of interest or repayment of principal amt may lead to liquidation.

- Capital structure touches both the profitability and the financial risk faced by a business.

- Optimal Capital Structure is that combination of debt and equity that grows the market value of shares of that company

Factors Affecting The Choice Of Capital Structure

- Cash Flow Position: Before raising finance business must look at the projected flow to ensure that it has sufficient cash to pay fixed cash obligations. A company with high liquidity and a good cash flow position can issue debt capital, as the company will have less chances of facing financial risk than the company with a low cash position.

- Interest Coverage Ratio: It refers to the number of times a company can cover its interest obligations from the profits and higher ICR reduces the risk of failing to meet interest obligations.

- Debt Service Coverage Ratio: It shows the company's ability to meet cash commitments for interest and principal amount of debt.

- Return on Investment: If a company earns hai returns it has the capacity to opt for death as a source of finance.

- Cost of debt: A company may raise funds from debts if it has the capacity to borrow funds at a lower interest rate.

- Tax Rate: Higher the tax rate, more preference for debt capital in the capital structure, as interest on debt capital being a tax deductible expense makes the debt cheaper.

- Cost of equity: If a company has high risk, its shareholder may expect a high rate of return resulting in increased cost of capital.

- Floatation cost: Choosing a source of fund depends on the flotation cost to be spent to raise such funds, flotation cost makes this show less attractive.

- Risk Consideration: A company picks debts as a source of finance depending on its operating risk and overall business risk.

- Flexibility: The choice of debts depends on the company's potential to borrow and the level of flexibility it wants to keep for choosing a source of funds in future.

- Control: Debt normally does not cause dilution of control whereas a public issue makes the firm vulnerable to takeovers. To keep control, firms should issue debt.

Fixed Capital

Fixed capital refers to investment in long-term assets. Investment in fixed assets is for longer duration and they must be financed through long-term sources of capital. Choices relating to fixed capital involve huge capital funds and are not reversible without spending heavy losses.

Factors Affecting Requirement Of Fixed Capital

- 1. Nature of Business: Manufacturing concerns need huge investment in fixed assets & thus huge fixed capital is needed for them but trading concerns need less fixed capital as they are not needed to purchase plant and machinery etc.

- 2. Scale of Operations: An organization operating on a large scale needs more fixed capital as compared to an organization operating on a small scale. For Example - A large scale steel enterprise like TISCO needs large investment as compared to a mini steel plant.

- 3. Choice of Technique: An organization using capital intensive techniques needs more investment in plant & machinery as compared to an organization using labour intensive techniques.

- 4. Technology upgradation: Organizations using assets which become obsolete faster need more fixed capital as compared to other organizations.

- 5. Growth Prospects: Companies having more growth plans need more fixed capital. In order to expand production capacity more plant & machinery are needed.

- 6. Diversification: In case a company goes for diversification then it will need more fixed capital to invest in fixed assets like plant and machinery.

- 7. Distribution Channels: The firm which sells its product through wholesalers and retailers needs less fixed capital.

- 8. Collaboration: If companies are under collaboration, Joint venture, then they need less fixed capital as they share plant & machinery with their collaborators.

Working Capital

- Working capital is that amount of capital which is used in the day-to-day operations of the business this may be in cash or cash equivalents. The working capital is used by the business within one year. For example: stocks and inventories, debtors, bills receivables, etc.

- Various type of Current assets that give to the working capital are:

- Cash in hand/cash at Bank

- Marketable securities

- Bills receivable

- Debtors

- Finished goods

- Inventory

- Work-in-progress

- Raw material

- Prepaid expenses

- Various sources of Current liabilities that give to the working capital are:

- Bills payable

- Creditors

- Outstanding expenses and advances got from customers.

Factors Affecting The Working Capital Requirements Advance From Customers

- Nature of Business: A trading organization needs a lower amount of working capital as compared to a manufacturing organization, as trading organizations undertake no processing work.

- Scale of Operations: An organization operating on a large scale will need more inventories and thus, its working capital requirement will be more as compared to a small organization.

- Business Cycle: In the time of boom more production will be undertaken and so more working capital will be needed during that time as compared to depression.

- Seasonal Factors: During peak season demand of a product will be high and thus high working capital will be needed as compared to lean season.

- Credit Allowed: If credit is allowed by a concern to its customers then it will need more working capital but if goods are sold on a cash basis then less working capital is needed.

- Credit Availed: If a firm is able to purchase raw materials on credit from its suppliers then less working capital will be needed.

- Inflation: Working capital requirement is also found by price level changes. For example, during inflation prices of raw material, wages also rise resulting in increase in working capital requirements.

- Operating Cycle/Turnover of Working Capital: Turnover means speed with which the working capital is turned into cash by sale of goods. If it is speedier, the amount of working capital needed will be less.

Free study material for Business Studies

CBSE Class 12 Business Studies Chapter 9 Financial Management Notes

Students can use these Revision Notes for Chapter 9 Financial Management to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Chapter 9 Financial Management Summary

Our expert team has used the official NCERT book for Class 12 Business Studies to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Business Studies.

Chapter 9 Financial Management Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Chapter 9 Financial Management. All study material on studiestoday.com is free and updated according to the latest Business Studies exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Business Studies Financial Management Notes Set 01 from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Business Studies.

Yes, our CBSE Class 12 Business Studies Financial Management Notes Set 01 include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Business Studies principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Business Studies Financial Management Notes Set 01 provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Business Studies are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Business Studies Financial Management Notes Set 01, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Business Studies Financial Management Notes Set 01, are available for immediate free download. Class 12 Business Studies study material is available in PDF and can be downloaded on mobile.